If one has to put a finger on the most far reaching Reform with transformative outreach of the past hundred years in the Indian economy, then probably, many of us would likely select the Insolvency Reform unleashed in 2016.

Like in 1991, when the economy was on the verge of Bankruptcy, in came the Doctor, pulled out of UGC, who presented the reformist budget of all time, in June 1991. His impassioned speech still echoes,

“I do not minimise the difficulties that lie ahead on the long and arduous journey on which we have embarked. But as Victor Hugo once said, “no power on earth can stop an idea whose time has come.” I suggest to this august House that the emergence of India as a major economic power in the world happens to be one such idea.”

Fast forward, about 25 years once again, it is reforms in the space of Bankruptcy, that is set to transform the Indian economy.

Visionaries like Dr Raghuram Rajan and N. Rangachary had set the ball rolling in 2014. On 26th May 2015, the lawyer turned politician Arun Jaitley took charge as Finance Minister. The legal background helped as he introduced Bill No. 349 of 2015 in the Lok Sabha on 21st Dec that eventually culminated in the Insolvency and Bankruptcy Code (CODE) to get the Presidential assent on 28th May 2016.

It is time there is an enhanced awareness of these tectonic changes that are changing and consolidating the foundations. This series of articles on the CODE looks at the elephant from different perspectives, to understand how the economy is changing at a deep structural level, beyond the inferno of NPAs raging all around us.

The first in the series looks at the Need for Speed, and how the Code matches up to this Need for Speed.

In Nov 2017, when the World Bank released its report on Ease of Doing Business, India was ranked 100th out of the 190 countries. In itself that would have been a matter of shame, but shame, like most other things, is also relative. The ranking had improved, 30 places, from 130 to 100 in 2017.

The Ease of Doing Business Index that was created by the Bulgarian economist, Simon Djankov for World Bank, is a second derivative arising from various components in doing business, right from “Starting a Business”, to “Dealing with permits”, “Getting Electricity”, “Registering Property”, “Getting Credit”. “Protecting investors”, “Paying taxes”, “Cross Border trading”, “Enforcing Contracts” and lastly, “Resolving Invsolvency”.

The last component had been a millstone for the Indian economy, which was finally crunched in November 2016. This reflected in the “significant” jump in 2017 ranking.

“An Act to consolidate and amend the laws relating to reorganization and insolvency resolution of corporate persons, partnership firms, and individuals in a time bound manner for maximization of value of assets…”

The Insolvency and Bankruptcy Code, 2016 was promulgated in late 2016, with Resolution being the soul of the Code. There are many pillars of the Code, but when it comes to implementation, the main pillar is time bound execution, which we look at in this part.

The soul of the Code is resolution of insolvency of a firm by a collective effort to keep it going, to maximize the value of its assets, and to balance the interest of all the stakeholders. As a collective body of creditors the Committee of Creditors act in unison to resolve insolvency through a process that does not have petitioner/respondent or plaintiff/defendant.

In the year or so of its operation, the newly started process of unlocking value stuck in insolvent businesses, has seen good amount of traction.

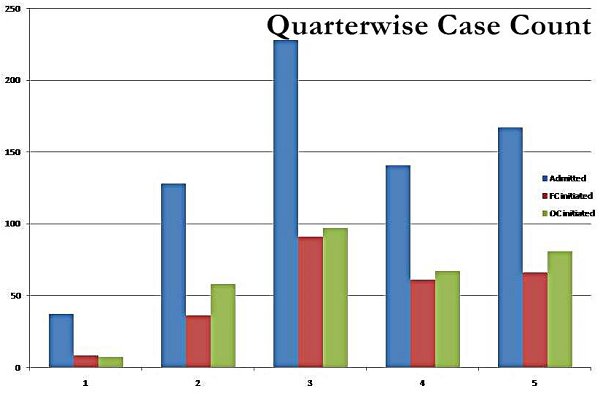

In the five quarters (sixth quarter numbers are awaited), since the Code has been in action, a total of 701 cases have been referred to the Insolvency and Bankruptcy Board of India. Interestingly, most of the cases referred to the Board, have been initiated by the Operational Creditors (green bar), accounting for almost half of the total.

The innovative jugaad spirit of the promoters is also seen, as some promoters attempted to use the new CODE to escape from the dreaded SARFAESI. The provision for Moratarium u/s 14 of the CODE prohibits any action to foreclose, recover or enforce any security interest created by the corporate debtor in respect of its property including any action under the SARFAESI. The 180+90 days moratorium is very lucrative as unscrupulous promoters work on buying time, by filing Insolvency petitions either themselves or through their operational creditors.

The innovative jugaad spirit of the promoters is also seen, as some promoters attempted to use the new CODE to escape from the dreaded SARFAESI. The provision for Moratarium u/s 14 of the CODE prohibits any action to foreclose, recover or enforce any security interest created by the corporate debtor in respect of its property including any action under the SARFAESI. The 180+90 days moratorium is very lucrative as unscrupulous promoters work on buying time, by filing Insolvency petitions either themselves or through their operational creditors.

This has always been the bane of Indian economy as intelligent professionals, who advise these unscrupulous promoters, have worked hard to find ways to beat the system rather than clean up the mess. This is but another way that promoters had found in the ever green concept of evergreening stressed assets. NCLT has passed orders reprimanding promoters in cases like Unigreen Global, Leo Duct Engineers.

On one hand the Indian economy is mired with the NPA problem, with many banks going down under as was detailed in another article on the State of Banking in India, however banks were found to be reluctant in using the provisions of the Code, to initiate Insolvency & Bankruptcy proceedings. A mere 37% of the total admitted cases have been initiated by Financial Creditors, inspite of directives from RBI to leverage the Code for resolving NPAs.

On the other hand, the Government of India is leaving no stone unturned to ensure that the newly launched reform is a success, for eg. when it was found that the Resolution Plan could create book profits, from write off of debts in the books of the firm. Such book profits could attract MAT, and consequently could discourage the prospect of resolution. So the Central Government allowed to set off such book profits against the losses brought forward.

Similarly, a resolution plan would have entailed possible allotment of shares at discount to creditors. The Companies Amendment Act 2017, allowed Companies to issue shares at a discount to its creditors when its debt is converted into equity shares in pursuance of any resolution plan. The Government also clarified that approval of shareholders of the company for a particular action required for implementation of a Resolution Plan, which would have been required under the Companies Act 2013, or any other regulation, is deemed to have been given on approval of the Resolution Plan by the Adjudicating Authority.

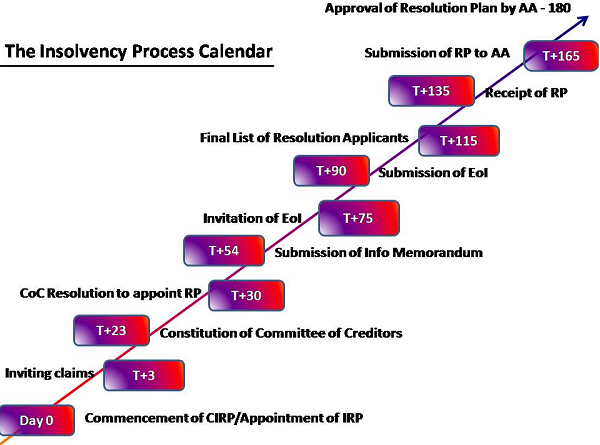

However, in any business, particularly, in a failing business time is the most crucial factor, as with every passing day, there is continuous erosion in the Business Capital of the Company. Suppliers suffer from faith erosion, employees start fleeing a sinking ship, and customers don’t want to deal with a company that is facing prospect of insolvency and bankruptcy. Need for Speed is felt acutely. Most of the time, an early detection of the problems can ensure prevention of insolvency itself. However, early detection is a necessary condition, not sufficient; once detected treatment has to follow a strict calendar.

The Code envisages a strict time bound process. Section 12 of Chapter II in Part II, clearly states “the corporate insolvency resolution process shall be completed within a period of one hundred and eighty days”.

180 days is more or less carved in stone from the date of admission of a Corporate Insolvency Resolution Application. Thereafter the whole ecosystem centered around the Insolvency Resolution Professional works towards ensuring that the Resolution is achieved, and failing which Liquidation is initiated.

This is a newly launched reform, and yet it is a good time to see how the process is working, in terms of time taken to complete the process.

Out of the total 701 cases, a total of 109 cases have been dispensed off with, and while Resolution is the prime objective, bulk of the dismissals were Liquidations, at 87 cases. The ability of the process to unlock value deserves a separate article and as such is detailed in a later article.

The intial quarters saw the process find its feet, as the six cases admitted in Jan 2017, took an average of 264 days for closure, while the eleven cases filed in Sep 2017, took (median & average) of 184 days to closure. Not just the average is coming down but the falling variation has brought much needed predictability to the process.

However these numbers, in particular the falling Closure Time, is arrived from the subset of Closed Cases. Of the 701 cases admitted, 525 are still open. When we look at the ageing, 308 cases have been admitted in the past two quarters. Excluding these 308 that have not yet completed the 180 day timeframe, there are still 217, which are at various stages of extension or judicial reviews and have not yet been closed.

Sub Clause 3 of the same Section 12, provides for extension, “the Adjudicating Authority may by order extend the duration of such process beyond one hundred and eighty days by such further period as it thinks fit, but not exceeding ninety days, provided that any such extension of the period of CIRP under this section shall not be granted more than once.”

Now while the Code is very particular about the timelines, however, the Adjudicating Authority also looks at the spirit and soul of the Code, which is to strive for Resolution.

In the case between M/s Brasher Boot Company Ltd Vs M/s Forward Shoes (India) Pvt Ltd, the issue addressed was, whether more than one extension can be granted, within the limitations of 180+90 days.

In the said Insolvency matter, the AA had already granted an extension of 30 days, and then it was requested a further extension of 60 days. In terms of the letter of the Code, this was perhaps not possible. However, the AA went by the spirit of the Code, it held that the language of Sec 12(3) speaks the intention of the legislature. The sub-provision cannot take away the effect of the main provision or to remove any doubt in relation to its implementation. If another extension is not granted beyond the extension of 30 days, it will render sec 12(3) of the Code otiose. Accordingly the AA had granted the second extension of sixty days.

Not just the additional 90 days as provided u/s 12(3), quite often legal reviews and appeals add to the Closure time. For instance in the matter of Quantum Ltd, the process was not completed in 180 days. Neither was any application made for extension, before the end of 180 days.

When the application for extension was filed after the expiry of 180 days, the Adjudicating Authority rejected the application and denied extension, on the grounds that there is no provision to file such application after the expiry of 180 days.

The RP went for an appeal against the AA Order in the NCLAT.

The NCLAT held that in terms of section 12(2) of the Code, an RP can file an application to AA for extension of the period of CIRP only if instructed to do so by the CoC by a vote of 75% of the voting shares. The provision does not stipulate that such application is to be filed before the AA within 180 days. If within 180 days, a resolution is passed by the CoC by a majority vote of 75% of the voting shares instructing the RP to file an application for extension of period, the AA should allow time up to 90 days beyond 180 day.

Not just that NCLAT, also upheld that the time lost in between while the Extension application was put up before the AA and the NCLAT, would not be considered in the extended period.

The NCLAT accordingly extended the period of resolution process for another 90 days and excluded the period between 181st day and passing of the order by the NCLAT for all purposes. It observed that it is the duty of the AA to find out whether a suitable resolution plan is there to be approved instead of going for liquidation, which is the last recourse on failure of resolution process.

The Closure Time of the I&B process would only improve as the process moves up the curve and gains maturity. It is still being comprehended by the concerned stakeholders and in particular the Insolvency Resolution Professional, who is effectively the legendary TurnAround Artist.

Part B of the Code Series, looks at the quality of the Process Output, in terms of the Haircuts suffered by Creditors in the Resolution effort.

Part C of the Code Series looks at the differentiator between the Insolvency Code and SICA.

Author Bio