As per the information provided by Mr. Rathi, he registered the website with the name www.ibbivaluer.com on 21st March 2019. The website uses the abbreviation ‘ibbi’ as part of domain name i.e. ibbivaluer.com at that time when he did not even pass the examination for registration as a valuer.

There is no evidence on record to show that he has derived any direct benefit but his intention behind such registration is malafide. The domain name ibbivaluer.com was registered on 21st March 2019 when Mr. Mukesh Kumar Rathi was not even a registered valuer with IBBI. At that time, he had not even passed the examination to become eligible for registration with IBBI as a registered valuer. These facts create more severity since such an act cannot be treated as an innocent mistake though he cannot be held responsible under the Companies (Registered Valuers and Valuation) Rules, 2017 for the period when he was not registered with the IBBI as a registered valuer. However, for the period after his registration i.e. 23rd August 2019 till the date when he surrendered his domain name i.e. 7th December 2019, he is responsible.

Mr. Mukesh Kumar Rathi, through such registration, has misled the stakeholders and IBBI. His conduct is in violation of Rule 3(1)(k) and Rule 7(a), (b) and (g) of the Companies (Registered Valuers and Valuation) Rules, 2017, and Clauses 1, 2, 3 and 4 of the Model Code of Conduct for Registered Valuers stipulated under Annexure – I of the said Rules. He has attempted to conduct business which in the opinion of this Authority discredits valuation profession against clause 30 of the above said Model Code of Conduct.

In view of the above, the Authority, in exercise of powers conferred under Section 458 of the Companies Act, 2013 read with Rule 15 and 17 of the Companies (Registered Valuers and Valuation) Rules, 2017, hereby, directs that Mr Mukesh Kumar Rathi’s registration as a registered valuer shall be suspended for three months.

INSOLVENCY AND BANKRUPTCY BOARD OF INDIA

[Authority delegated by the Central Government under section 458 of the Companies

Act, 2013 read with rule 2(1)(b) of the Companies (Registered Valuers and Valuation) Rules, 2017]

No. IBBI/DC/16/2020-21

Dated: 8th January 2020

Order

In the matter of Mr. Mukesh Kumar Rathi, Registered Valuer under Rule 17 read with 15 of the Companies (Registered Valuers & Valuation) Rules, 2017.

1. Background

1.1 The Insolvency and Bankruptcy Board of India (‘IBBI’) has been delegated by the Central Government to perform the functions as the Authority under the Companies (Registered Valuers and Valuation) Rules, 2017 (‘Rules’). The IBBI has granted registration to Mr. Mukesh Kumar Rathi as valuer in the asset class of Securities or Financial Assets on 23rd August 2019 with registration number IBBI/RV/03/2019/12240.

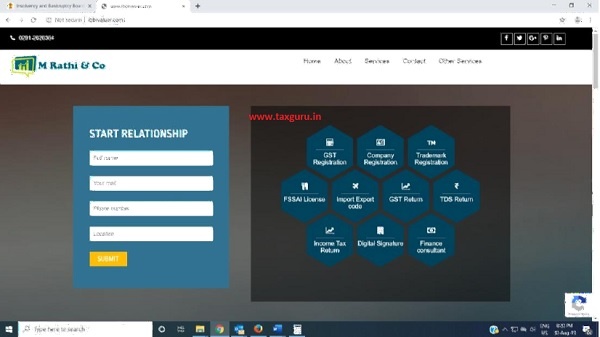

1.2 It has come to the notice of the IBBI that Mr. Mukesh Kumar Rathi created a Universal Resource Locator (‘URL’) by the name of ‘www.ibbivaluer.com’ which is misleading and giving a wrong impression that the registered valuer is closely associated with or is in some way related to the IBBI. A screenshot of the website is reproduced as below:

1.3 Upon consideration of the material available on record, the authorised officer of IBBI was of the prima facie opinion that sufficient cause existed to take actions under Rule 17 of the Rules and accordingly issued a show-cause notice (‘SCN’) dated 30th August 2019 to Mr. Mukesh Kumar Rathi, seeking his written reply and offering him an opportunity of seeking a personal hearing for disposal of the same, in accordance with the Rules.

1.4 Mr. Rathi responded to the SCN vide his reply dated 9th September 2019 requesting to grant him a personal hearing before taking any decision in the matter. A personal hearing was scheduled on 2nd December 2019 which was availed of by Mr. Rathi along with his partner, Mr Ankit Malani.

2. Consideration of SCN

The authorised officer has considered the SCN, the reply to SCN, oral submissions of Mr. Rathi during the course of personal hearing, his submissions dated 9th December 2019, other material available on record and proceeds to dispose of the SCN.

3. Show Cause Notice

The following are noted from the SCN:

a) IBBI is a statutory body established under the Insolvency and Bankruptcy Code, 2016 (Code) and it is not in the interest of its stakeholders and also in the public interest to use its name randomly by anyone and in any manner they like. Use of its name anywhere, including in the URL of a website, is misleading as this is bound to give a wrong impression to the stakeholders and to the general public that the registered valuer is being endorsed or is closely associated with IBBI.

b) Rule 3(1)(k) of the Rules prescribes that a person shall be eligible to be a registered valuer if he is a ‘fit and proper person’. For determining whether an individual is a ‘fit and proper person’ under the Rules, the Authority may take into account any relevant consideration, inter-alia, integrity, reputation and character.

c) The contraventions committed by Mr. Rathi are serious in nature making him a person who is not “fit and proper” to continue as a registered valuer and has further led to breach of his conditions of registration.

d) Clause 1 of the Model Code of Conduct for Registered Valuers under Annexure – I of the Rules stipulates that a valuer shall, in the conduct of his/its business, follow high standards of integrity and fairness in all his/its dealings with his/its clients and other valuers. Clause 2 stipulates that a valuer shall maintain integrity by being honest, straightforward, and forthright in all professional relationships. Clause 3 stipulates that a valuer shall endeavour to ensure that he/it provides true and adequate information and shall not misrepresent any facts or situations. Clause 4 stipulates that a valuer shall refrain from being involved in any action that would bring disrepute to the profession.

e) Clause (a) of Rule 7 of the Rules prescribes that the registration of the valuer is subject to the condition that the valuer shall at all times possess the eligibility and qualification and experience criteria as specified under Rule 3 and Rule 4, while Clause (b) of Rule 7 prescribes that the registration of the valuer is subject to the condition that the valuer shall at all times comply with the provisions of the Act, the Rules and the Bye-laws or internal regulations, as the case may be, of the respective registered valuers organisation. Further, clause (g) of Rule 7 prescribes that the registration of the valuer is subject to the condition that the valuer shall comply with the Code of Conduct (as per Annexure-I of the Rules) of the registered valuers organisation of which he is a member.

4 Submissions by Mr. Rathi:

A summary of written submissions made by Mr. Rathi in reply dated 9th September 2019 and oral submissions made on 2nd December 2019 (and letter dated 9th December 2019) is as under:

Written Submissions:

a) Mr Rathi, being a registered valuer with IBBI, inadvertently chose and got the domain name ibbivaluer.com registered without any intention of violation of any Rules.

b) Government establishments use either gov.in or nic.in and he has not used either of these domains. He has used .com which indicates a commercial organisation and not a government organisation. Since there was no restriction while booking the domain name so the same was registered in good faith. That he has already informed his mail ID to ICSIRVO and IBBI in advance and none of them objected to use of ‘ibbivaluer’ at the time of registration.

c) That he has started the profession of registered valuer to earn his livelihood and has created the website for the same purpose without any intention to defraud anyone.

d) That IBBI is an acronym and can have many meanings in different parts of the world as well as different parts of the society. Further, like IBBI, the name of other statutory authorities is also used by many people without any restrictions.

e) That if he surrenders his domain name there cannot be any certainty that no one else will use the same domain name in future. Further, he stated that he is a sincere member of IBBI and will not be involved in any action which brings disrepute to the profession.

Oral Submissions:

a) The domain name was registered online from ‘BigRock’ in ignorance of the fact that the abbreviation ‘IBBI’ cannot be used as a part of domain name.

b) By use of ‘ibbivaluer’ as part of his domain name, he had neither any intention to mislead anyone nor his act was malafide.

c) He also confirmed that he has discontinued use of domain name ‘ibbivaluer’ from 14th November 2019.

d) He undertook to forward an official confirmation regarding the surrender of domain name to the IBBI which was received by the IBBI on 12th December 2019.

e) The letter (dated 9th December 2019) was sent by Mr Rathi confirming that ‘BigRock’ company has deleted the domain name ‘com’. He further confirmed that the domain name was registered on 21st March 2019 while the same was deleted on 7th December 2019.

5 Analysis and Findings:

The Corporate Insolvency Resolution Process under the Code envisages estimation of fair value and liquidation value of the assets of the corporate debtor. These values serve as reference for evaluation of choices, including liquidation; and selection of the choice that decides the fate of the corporate debtor and consequently of the stakeholders. In consequence of an error in valuation, a viable corporate debtor could be liquidated, or a non-viable corporate debtor could be rehabilitated. Further, if market participants undertake transactions at a value which is not reflective of market or different from price, the resources in the economy could be misallocated. Such outcomes are disastrous for the economy and also impinge economic growth. Thus, there exists a need for transparent and credible determination of value of the assets of the corporate debtor to facilitate comparison of choices and for taking informed decisions.

To ensure accountability in valuation services, valuation standards and ethical principles are followed across the world. India has adopted a two-tier, regulated self-regulation where valuers are enrolled with an RVO as a member, and thereafter registered with the Authority. They are subject to a detailed Code of Conduct in the interest of impartiality, credibility and objectivity.

The SCN has been examined, and the oral and written submissions of Mr Rathi and other material available on record, have been carefully considered, and it is found as follows:

a) Undisputedly IBBI is a statutory authority. By custom and also by practice, the abbreviation ‘IBBI’ denotes and stands for Insolvency and Bankruptcy Board of India. The market has also been using the term ‘IBBI’, and ‘Insolvency and Bankruptcy Board of India’ interchangeably. Further, the website of IBBI is also registered as ibbi.gov.in.

b) The website of Mr. Rathi i.e. www.ibbivaluer.com uses domain name ‘ibbivaluer.com’. Mr. Rathi, in his personal capacity is neither related to IBBI nor is endorsed by it. There is no relationship between IBBI and the website of Mr. Rathi, except that Mr. Rathi is registered by IBBI (the Authority under the Rules) as a registered valuer w.e.f. 23rd August 2019. The use of abbreviation ‘ibbi’ to derive commercial benefits, in the absence of any authorisation from the IBBI, is, thus not permissible.

c) Further, the internet has developed from a mere means of communication to a mode of carrying on commercial activity. With increase of such commercial activity on the internet, a domain name is also used as a business identifier. Consequently, a domain name must be unique and must not give a wrong impression to the general public at large.

d) As per the information submitted by Mr. Rathi, the website was registered by him on 21st March 2019 i.e. much before his registration was done as a valuer with the IBBI on 23rd August 2019.

e) Rathi is a qualified registered valuer with the IBBI under the Rules in the asset class of Securities or Financial Assets. Rule 3(1)(k) of the Rules require a valuer to be a fit and proper person. Thus, only an individual with absolute integrity and unblemished reputation must be registered as a valuer since reputation, character and competence of the applicant is of material consideration while granting registration.

f) The gravity of the contraventions committed by Mr Rathi is to be judged from the intention behind such registration though the only defence taken by Mr Rathi was that he does not have any intention or motive to gain any material benefit by the use of the abbreviation ‘IBBI’ as part of his domain name. It is too naïve to believe that Mr. Rathi does not have intent to make any gain by using ‘IBBI’ as a part of the name of his website.

g) Mr Rathi, vide letter dated 9th December 2019, has confirmed that neither he nor any of his partner has received any valuation assignment through the website i.e. www.ibbivaluer.com during the period when the website was active. However, not getting any assignment cannot be a ground for not holding a person liable for use of the abbreviated name of the IBBI.

h) However, the intention of Mr Rathi behind getting the registration of the website i.e. www.ibbivaluer.com on 21st March 2019 which is much before his registration as a Registered valuer with IBBI is not clear.

6. Conclusion

6.1 In the valuation profession, it is imperative that only individual with absolute integrity and unblemished reputation is registered as a valuer. As a profession is known by the individuals practicing it, the members of the profession must inspire confidence of the stakeholders and the society at large. They have a collective responsibility to build and preserve the reputation of the fledgling valuation profession.

6.2 Mr. Rathi is a Chartered Accountant by profession having sufficient experience as such and is a registered valuer. He is expected to know the law and must demonstrate respect for the law. By virtue of him being a professional, he is fully aware that using the URL ‘www.ibbivaluer.com’ is deceptive and is capable of misleading the general public and causes confusion among them.

6.3 Undisputedly and admittedly, Mr Rathi has used the word ‘ibbivaluer’ as part of domain name in his website www.ibbivaluer.com (from 21st March 2019 to 7th December 2019). However, since the profession of valuation is new and evolving in India, it requires a lenient view.

6.4 Mr Rathi has surrendered the domain name ‘ibbivaluer’ as part of his website and has submitted a confirmation of the same. However, Mr Rathi has used the domain name ‘ibbivaluer’ much before he got himself registered as a Valuer with the IBBI. This cannot be said to have been done by him unknowingly and without understanding the consequences of the same even though the same has been contended by him in his written submissions and also during his oral submissions at the time of personal hearing.

6.5 Vide Notification no. S.O. 3401 (E) dated 23rd October 2017, the Central Government specified Insolvency and Bankruptcy Board of India as the ‘authority’ under section 458 of the Companies Act 2013. The notification provides:

“In exercise of the powers conferred by section 458 of the Companies Act, 2013 (18 of 2013), the Central Government hereby delegates the powers and functions vested in it under section 247 of the said Act to the Insolvency and Bankruptcy Board of India, subject to the condition that the Central Government may revoke such delegation of powers or it may exercise the powers under the said section, if in its opinion such a course of action is necessary in the public interest.”

Rule 17(5) of the Rules empowers the Authority to provide as below: “The order in disposal of a show-cause notice may provide for-

a. no action;

b. warning; or

c. suspension or cancellation of the registration or recognition; or

d. change in any one or more partner or director or the governing board of the registered valuers’ ”

Thus, the above rules empower the authority to pass any of the above orders while disposing of the SCN and vide Notification no. S.O. 3401 (E) dated 23rd October 2017, IBBI has been specified as the ‘authority’ by the Central Government under section 458 of the Companies Act 2013.

7 ORDER

7.1 As per the information provided by Mr. Rathi, he registered the website with the name www.ibbivaluer.com on 21st March 2019. The website uses the abbreviation ‘ibbi’ as part of domain name i.e. ibbivaluer.com at that time when he did not even pass the examination for registration as a valuer.

7.2 There is no evidence on record to show that he has derived any direct benefit but his intention behind such registration is malafide. The domain name ibbivaluer.com was registered on 21st March 2019 when Mr. Mukesh Kumar Rathi was not even a registered valuer with IBBI. At that time, he had not even passed the examination to become eligible for registration with IBBI as a registered valuer. These facts create more severity since such an act cannot be treated as an innocent mistake though he cannot be held responsible under the Companies (Registered Valuers and Valuation) Rules, 2017 for the period when he was not registered with the IBBI as a registered valuer. However, for the period after his registration i.e. 23rd August 2019 till the date when he surrendered his domain name i.e. 7th December 2019, he is responsible.

7.3 Mr. Mukesh Kumar Rathi, through such registration, has misled the stakeholders and IBBI. His conduct is in violation of Rule 3(1)(k) and Rule 7(a), (b) and (g) of the Companies (Registered Valuers and Valuation) Rules, 2017, and Clauses 1, 2, 3 and 4 of the Model Code of Conduct for Registered Valuers stipulated under Annexure – I of the said Rules. He has attempted to conduct business which in the opinion of this Authority discredits valuation profession against clause 30 of the above said Model Code of Conduct.

7.4 In view of the above, the Authority, in exercise of powers conferred under Section 458 of the Companies Act, 2013 read with Rule 15 and 17 of the Companies (Registered Valuers and Valuation) Rules, 2017, hereby, directs that Mr Mukesh Kumar Rathi’s registration as a registered valuer shall be suspended for three months.

7.5 In accordance with provisions of Rule 17(8) of the Rules, the directions of this order shall come into force on expiry of 30 days from the date of its issue.

7.6 A copy of this order shall be forwarded to ICSI Registered Valuers Organisation where Mr. Mukesh Rathi is enrolled as a professional member.

7.7 Accordingly, the show cause notice is disposed of.

-sd-

(Dr. Navrang Saini)

Whole Time Member, IBBI

Dated: 08th January 2020

Place: New Delhi