Divya Jayakumar

Applicability of Section 188: Section 188 Related to related Party Transaction applies to Both Public Limited and Private Limited Companies.

Related Party with reference to a Company, means –

- a director or his relative;

- a Key Managerial Personnel or his relative;

- a firm, in which a director , manager or his relative is a partner;

- a private company in which a director or a manager is a member or director;

- a public company in which a director or a manager is a director or holds along with his relatives, more than 2% of its paid-up share capital;

- any Body corporate whose Board of Directors, managing director or a manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager;

- any person on whose advice, directions or instructions a director or a manager is accustomed to act

Provided that nothing in sub-clauses (vi) and (vii) shall apply to the advice, directions or instructions given in a professional capacity;

- any company which is—

- a holding, subsidiary or an associate company of such company; or

- a subsidiary of a holding company to which it is also a subsidiary

- For example, Mr. Y is a practicing Company Secretary and if the Board of X Ltd considers his advice and acts upon it, he cannot be considered as a related party to any one or to that Company in anyway as Mr. Y is in a Professional Capacity

Relative:

- Relative, with reference to any person, means anyone who is related to another, if –

(i) they are members of a Hindu Undivided Family

(ii) they are husband and wife; or

(iii) one person is related to the other in such manner as may be prescribed;

A person shall be deemed to be the relative of another, if he or she is related to another in the following manner:-

- Father – includes step – father

- Mother – includes step- mother

- Son – includes step – son

- Son’s Wife

- Daughter

- Daughter’s husband

- Brother – includes step- brother

- Sister – includes step – sister

Transactions:

“Office or place of profit”

(i) where such office or place is held by a director, if the director holding it receives from the Company anything by way of remuneration over and above the remuneration to which he is entitled as director, by way of salary, fee, commission, perquisites, any rent – free accommodation, or otherwise;

(ii) where such office or place Is held by an individual other than a director or by any firm, private company or other body corporate, if the individual , firm, private company or body corporate holding it receives from the company anything by any way of remuneration, salary, fee, commission, perquisites, any rent-free accommodation, or otherwise;

Arm Length Transaction

- It means a transaction between two unrelated parties that is conducted as if they were unrelated, so that there is no conflict of interest. (i.e.) there is no need to put any interest by any party in such contract by any way.

- In short, there is no interest in any contract; such contract automatics cover the meaning of Arm Length Transactions.

- The ultimate scope of this section is “interest”, if any interest is there by anyway the Section shall be effective, if there is no interest is there, the section shall be in neutral.

Approval

♠ BOARD APPROVAL:

- All Companies must get Board’s approval irrespective of the Capital of the company or value of the transaction.

- The Approval Should be sought at a duly convened Board Meeting.

- The Approval cannot be obtained by passing a circulation resolution

- All the directors of the Company including the “Interested Directors” (Related parties to such contract) can participate in the Board Meeting.

- But the Directors who are related to the contracts which are going to be discussed in the meeting shall not be present at the meeting during the discussion alone.

- The Directors who are related parties to such contract or agreement cannot vote for the same.

Quorum

- The Quorum for the Board Meeting where Related Party Transaction is discussed should form 2/3rd majority excluding the Interested directors.

- For example, X Ltd is having 6 Directors in which 2 directors are related parties. When the Board Meeting is held and the Quorum for the Meeting should be (6*2/3= 4). Therefore excluding the related parties, the rest of the directors fulfilled the quorum and so meeting was held.

Shareholder’s Approval

- Companies having paid-up share capital of Rs.10 Crores or more

Or

- Sale, purchase or supply of any goods or materials directly or through appointment of agents exceeding 25% of the annual turnover

- Selling or otherwise disposing of, or buying, property of any kind directly or through appointment of agents exceeding 10% of net worth

- Leasing of property of any kind exceeding 10% of the net worth or exceeding 10% of turnover

- Availing or rendering of any services directly or through appointment of agents exceeding 10% of the net worth

- Appointment to any office or place of profit in the company, its subsidiary company or associate company at a monthly remuneration exceeding Rs. 2.5 Lakhs

- Remuneration for underwriting the subscription of any securities or derivatives thereof of the company exceeding 1% of the net worth

Important Points:

- Turnover or net worth shall be on the basis of the Audited Financial Statements of the preceding financial year.

- No Member of the Company shall vote on such special resolution to approve any contract or arrangement if such member is a related party

- In case of wholly owned subsidiary, the special resolution passed by the holding company shall be sufficient for the purpose of entering into the transactions between wholly owned subsidiary and holding company.

Exemption

- The Section will not apply to transactions entered by the Company in its Ordinary course of business, on arm’s length basis.

- The term “Ordinary Course of business” will cover the usual transactions, practices and customs of a business and of a Company.

Disclosures

Disclosures to be made in notice of the Board:

The Board Meeting agenda at which the resolution is proposed to be moved shall disclose the following:

- name of the related party and nature of relationship;

- nature, duration of the contract and particulars of the contract or arrangement;

- material terms of the contract or arrangement including the value, if any;

- any advance paid or received for the contract or arrangement, if any; and

- the manner of determining the pricing and other commercial terms, both included as part of contract and not considered as part of the contract;

- whether all factors relevant to the contract have been considered, if not, the details of factors not considered with the rationale for not considering those factors; and

- any other information relevant or important for the Board to take a decision on the proposed transaction.

Disclosure by interested Directors:

Every director of a company who is in any way, whether directly or indirectly, concerned or interested in a contract or arrangement or proposed contract or arrangement entered into or to be entered into:

- with a body corporate in which such director or such director in association with any other director, holds more than 2% shareholding of that body corporate, or

- with a body corporate in which such director is a promoter, manager, Chief Executive Officer of that body corporate; or

- with a firm or other entity in which, such director is a partner, owner or member, as the case may be

shall disclose the nature of his concern or interest at the meeting of the Board at which the contract or arrangement is discussed.

Disclosures to be made in the explanatory statement to be annexed to notice of general meeting:

- name of the related party ;

- name of the director or key managerial personnel who is related, if any;

- nature of relationship;

- nature, material terms, monetary value and particulars of the contract or arrangement;

- any other information relevant or important for the members to take a decision on the proposed resolution.

Disclosures to be made in Board’s Report:

- Every related party transaction or contract shall be disclosed in the Board’s report along with the justification for entering into such contract or arrangement.

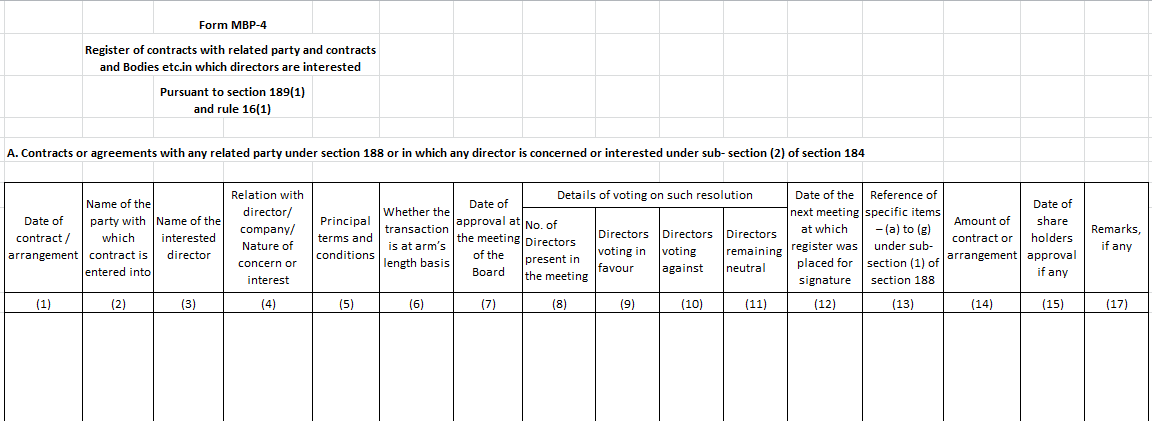

Disclosures to be made in Register of contracts or arrangements in which directors are interested

- Every company shall maintain one or more registers in Form MBP 4, and shall enter therein the particulars of contracts or arrangements with a related party with respect to transactions to which section 188 applies.

Format of MBP-4

Non-Compliance

- Any contract or arrangement entered into by any Director or any other employee, without obtaining the consent of the Board or approval by special resolution in the general meeting and if it is not ratified by the Board or, as the case may be, by the shareholders at the meeting within 3 months from the date on which such contract or arrangement was entered into, then in case if such contract or arrangement is entered with related party to any director, or is authorised by any other director, the Directors concerned shall indemnify the Company against any loss incurred by it.

- No Central Government approval is required for entering into any related party transactions.

- No approval of Central Government is required for appointment of any Director or any other person to any office or place of profit in the Company or its Subsidiary.

Penalty

- The Company can take necessary actions against any Director or employee in case any transaction is entered without the consent of the Board or Company for recovery of any loss sustained by it.

- In case of default of any Director or other employee of the company, who had authorized the contract or arrangement in violation of the provisions of this section shall –

(i) In case of Unlisted Company, be punishable with fine which shall not be less than Rs.25,000 but which may extend to Rs.5,00,000.

(ii) In case of Listed Company, be punishable with an imprisonment for a term which may extend to 1 year or with fine which shall not be less that Rs. 25,000 but which may extend to Rs.5,00,000, or with both.

Sir,

A company X having director A & B enters into a transaction (non Ordinary) with a company Y with Director C & D. Company X & Y are related.

A & B are Interested in the contract as they hold more than 2 % in company Y.

Now as they are interested director they cannot participate in a meeting in which such contract with related party is held. As there are only two directors they cannot give consent on the contract.

How will the company approve such transaction. Will passing Special Resolution suffice or there is any other way.

Thanks

This article is not updated with the amendment in Rules.

Thanks for updating mam!

Dear Sir,

Regarding stipulation of Quorum in the Board Meeting , would you mind to inform from where you have got that provisions ?

Regarding stipulation of Quorum in the Board Meeting , would you mind to inform from where you have got that provisions ?

Sec 188 of co’s Act,Related party transactions casts a very wide net.Its an Auditors nightmare.

Commendable article. Can u pl clarify, how resolution will be passed if 2 persons are the only members and only directors of a Co. and appoint any related party to any office or place of profit in the Co. at a monthly salary below 2.5 lacs?

The statement that, shareholders approval will be required, if the PSC of the Company is more than 10 crores is inappropriate as there was Amendment on 14.08.2014 which removed the limit of 10 crores and increased the threshold limit.

Dear Sir,

Pl clarify the below;

If we are sending Excisable As such Inputs under rule 4(5) CCR 2004 to a related party. This sec 188 of CA 2013 will applicable or not?