In this article we shall discuss the significance of making distinctions between ordinary business and special business

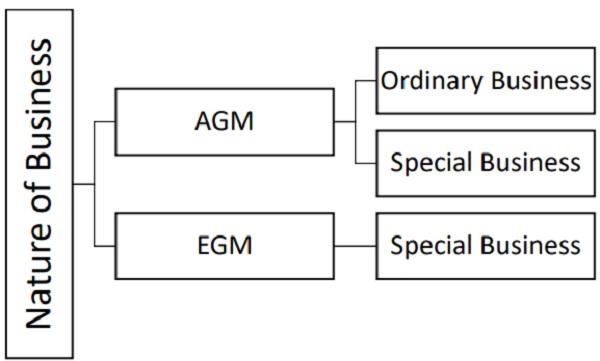

Under the Companies Act, 2013 the term ‘General Meeting’ means shareholder’s meetings which includes Annual General Meeting as well as Extra-Ordinary General Meeting.

It is mandatory for every Company to hold in each calendar year an Annual General Meeting. No Company is exempt from this requirement. An Annual General Meeting is in addition to any other general meeting of the company.

The significance of Annual General Meeting arises out of the nature of business that are transacted at this meeting. There are two types of Business that are transacted at an Annual General Meeting ordinary business and special business.

Extra-Ordinary General Meeting is convened for transacting special or urgent business that may arise between two Annual General Meeting. All Business transacted at an Extra-Ordinary General Meeting are called Special Business.

1. Why it is important to make distinction between ordinary and special business in Notice calling Annual General Meeting?

This distinction between ordinary and special business is made for the purpose of attaching explanatory statement to the notice calling the General Meeting.

2. What is explanatory statement? What is the purpose of explanatory statement?

In respect of every business other than ordinary business i.e., Special Business to be transacted in Annual General Meeting and in respect of all business that is to be transacted at Extra-Ordinary General Meeting, an explanatory statement must be annexed to the notice of the meeting.

The purpose of explanatory statement is, it shall contain material facts which would help a member to understand the meaning, scope and impact of the business item and to take prudent decision before voting for such resolution.

3. Ordinary Business and Special Business

Ordinary Business

Ordinary business is the business which must be transacted at an annual general meeting. As per section 102 of the Companies Act, 2013 following are ordinary business-

(a) The consideration of financial statements and the reports of the Board of directors and auditors;

(b) The declaration of dividend;

(c) The appointment of directors in place of those retiring;

(d) The appointment of, and the fixing of remuneration of, the auditors.

Thus, if the four items of business mentioned above is transacted at Annual General Meeting, then it is considered as ordinary business and every other business transacted at Annual General Meeting will be considered as special Business.

Special Business

Special business can be transacted either at an Annual General Meeting or an Extra-ordinary general meeting. Its pertinent to note that every business transacted at Extra-ordinary general meeting is special business.

Let us try to understand this distinction with an example

|

Items of Business |

Meeting | Ordinary business | Special business |

Explanatory statement |

|

Declaration of Dividend |

AGM | YES | – | Not Required |

|

Declaration of Dividend |

EGM | – | YES | Required |

|

Issue of Bonus Shares |

AGM | – | YES |

Required |

|

Issue of Bonus Shares |

EGM |

– | YES |

Required |

4. Business vs Resolution

The terms “ordinary business” and “special business” are not to be confused with terms “ordinary resolution” and “special resolution”. This distinction of business is exclusively made for the purpose of explanatory statement, it has nothing to do with the type of resolution.

5. Important differences between Ordinary Business and Special Business

|

Nature |

Ordinary Business |

Special Business |

|

Resolution (Refer Note) |

Resolutions are not required to be stated in the Notice. For example: To declare dividend for the financial year ended 31st March 2022. |

Special Business shall be in the form of a Resolution |

|

Postal Ballot |

Ordinary Business shall not be transacted by means of a postal ballot |

Special Business may be considered by means of a postal ballot. |

Note:

1. Resolutions are broadly of two types: Ordinary Resolutions and Special Resolutions

2. Ordinary Resolution require simple majority whereas Special Resolution require three-fourth majority.

3. In case of a special resolution, the notice should state that a particular resolution is proposed to be passed as a special resolution.

Author Bio

I’m not sure about all special business requires to be in the form of a resolution. As per secretarial standard for board and general meetings only decesions need to be in the form of resolution and mere notings and recordings by shareholders or board members need not be in the form of a resolution.