Introduction

A company giving loans to a director or their related parties will have to comply with various provisions of law. The said provisions are introduced to achieve objectives stated below:

1. Ensures proper use of Public Funds lent by Financial Institution.

2. Ensures that objectives for which public issue is done is fulfilled.

3. Ensures that Director is not misusing the funds by transferring it for its personal purpose.

4. Ensures avoidance to evasion of taxation.

As Per Companies Act 2013

As per Section 185(1) of Companies Act 2013, a Company cannot provide loan, give guarantee or provide security to:

1. Director of Company

2. Director of Holding Company

3. Partner or Relative of such director

4. Firm in which director or relative of such director is partner

However, as per Section 185(2), a Company can provide loan, guarantee, or security related to any loan taken, to the following person in whom any director of the company is interested:

1. private company of which any such director is a director or member

2. any body corporate, where > 25% of the total voting power is with such director, or jointly by two or more Directors

3. any body corporate controlled by such director.

Below-mentioned conditions shall be complied with for such a transaction:

1. Passing Special Resolution (SR) in General Meeting (GM),

2. Purpose must be for performing principal business activities only

Section 185(1) & 185(2) shall not be applicable if:

1. Any loan given to a managing or whole-time director as a part of the conditions of service extended by the company to all its employees

2. A company that provides loans or gives guarantees or securities in the ordinary course of its business (Rate charged >/= Prevailing market rate) e.g. Lending Companies, Financials Institutions.

3. Loan made, guarantee given, security provided by Holding Company to its Wholly owned Subsidiary Company.

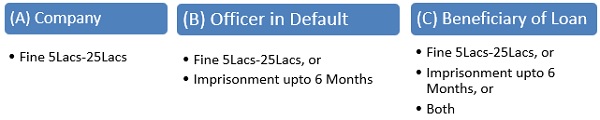

Penalty for non-compliance [Section 185(4)]

Non-Applicability

Section 185 shall not be applicable to the following companies if below-mentioned conditions are fulfilled:

Private Companies

- No investment in share capital by other Corporate entity,

- Company’s Borrowings from Banks/FS/Corporate entities <[2*(PUSC) or 50 Cr. w.e.i.lower] AND

- No outstanding defaults in repaying borrowings subsisting on the date of transaction under this section.

Nidhi Companies

- If the loan is given to a director or their relative in their capacity as members and such transaction is disclosed in Annual accounts through a note.

Government Companies

- If the Company obtain prior approval from the Ministry or Department of the Central Government responsible for administratively overseeing the company or from the respective State Government.

Disclosure

The company shall disclose to the members in the FS the full particulars of Loan, guarantee or Security given and the purpose for which following is proposed to be utilised by the recipient.

Once the loan is granted to a director, proper recording should be made in that register by administrators.

As Per Income Tax Act, 1961

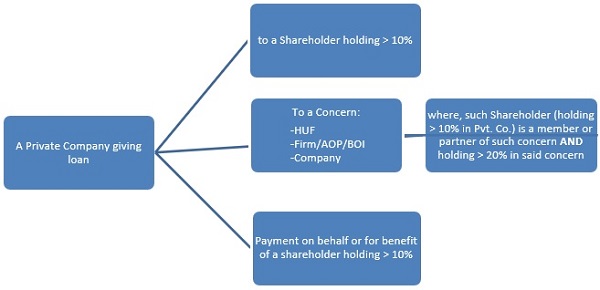

As per Section 2(22)(e ) of the Income Tax Act, 1961, taxability in the hands of the shareholder where a Company provides loan to a shareholder or an entity related to a shareholder is as below:

The loan provided by the Private Company to its shareholder or any other concern shall be taxable in the hands of the shareholder as per Section 2(22)(e)

Thus, if a director receiving loan or advance from the company has:

1. Substantial interest in the lending company, then the said loan shall be taxed as deemed dividend u/s 2(22)(e).

2. Employment Relationship with the lending company, then the said loan shall be taxed as a perquisite.

However, if the director is neither employee nor having substantial interest in company, the loan given by lending company to the director without any interest (i.e. interest free loan) would not be treated as perquisite and not be taxed in the hands of director

[DCIT Vs Shri Shekhar G. Patel (ITAT Ahmedabad)]

| Yash Agrawal Consultant yash.agrawal@masd.co.in |

Prabhjot Kaur Tax Manager prabhjotkaur.nara@masd.co.in |