1. This article has been discussed in detailed regarding the determination of Residential Status of an Individual in India as per the Income Tax Act,1961-2020.

2. For computing the taxable income of an Individual, it is important to determine the residential status of an individual in India as per the Income Tax Act,1961 for each assessment year. For the purpose of Income Tax, there are three classes of Individual which as under:

i) Ordinary Resident

ii) Resident but not ordinarily resident (RNOR)

iii) Non Resident (NR)

3. On the basis of the above status of an individual, the income will be computed of an individual for each assessment year. As per Section 5, incidence of tax on the taxpayer depends on his residential status and place of accrual or receipt of income. In this topic, we are exclusively dealing with first limb i.e determination residential status of an Individual.

4. For determination of residential status of an individual, there are certain condition which are required to be fulfilled which will be discussed in detail as under:

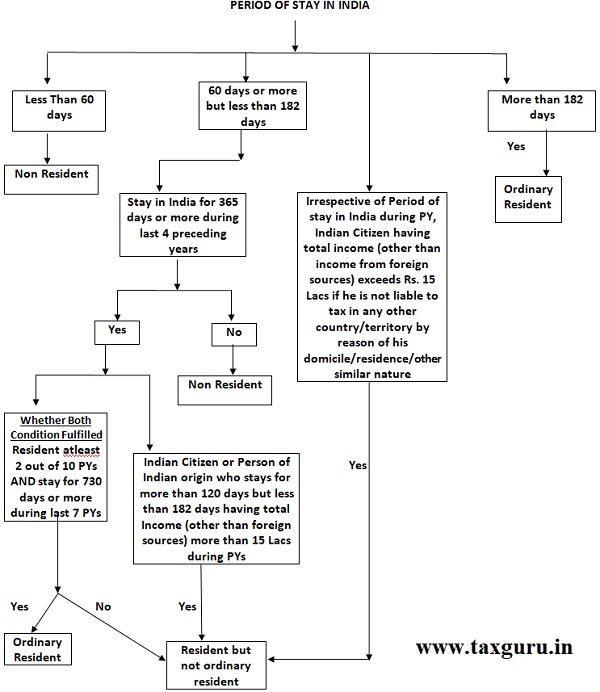

As per Section 6(1), an individual is said to be resident in India in any previous year, if he fulfils any one of the following conditions:

a) He is in India for total period of 182 days or more during the previous year OR

b) He had been in India for 365 days or more in aggregate during the 4 years preceding the previous years and he is in India for total period of 60 days or more during the previous year.

If any of the above condition gets fulfilled, then he is a resident for that previous year. If both conditions are not fulfilled then he is a non resident for that previous year.

5. Explanation 1 of Section 6(1) states as under:

The following person will be treated as resident only if their period of stay in India is fulfilled as mentioned below:

a) Indian Citizen who leaves India as a member of crew of an Indian Ship or for the purpose of employment outside India then their period of stay should be 182 days or more in aggregate during the previous year. [Ordinary Resident]

b) Indian Citizen or Person of Indian Origin within the meaning of Explanation to clause (e) of Section 115C who, being outside India, comes on visit to India then their period of stay should be 182 days or more in aggregate during the previous year. [Ordinary Resident]

c) Indian Citizen or Person of Indian Origin having total income, other than income from foreign sources, exceeding Rs 15 Lakh then their period of stay should be 120 days or more in aggregate during the previous year. (Inserted by Finance Act,2020) [Period of stay exceeds 120 days but does not exceeds 182 days then he is said to be “Resident but not ordinarily resident”. If period of stay exceeds 182 days then he is said to be “Ordinary Resident” for the relevant year.]

Explanation to Clause (e) of Section 115C

A person is said to be Indian origin if he or either of his parents or either of his grant parents were born in undivided India.

6. Explanation 2 of Section 6(1) states as under:

For the purposes of this clause, in the case of an individual, being a citizen of India and a member of the crew of a foreign bound ship leaving India, the period or periods of stay in India shall, in respect of such voyage, be determined in the manner and subject to such conditions as may be prescribed. This determination has been prescribed in Rule 126 of the Income Tax Rules,1962 which we will discussed later in Para 12.

7. We have discussed above regarding the determination of residential status of resident and non resident status of an Individual. Once we determine that an Individual is resident then we move on to next step to determine whether an individual is an ordinary resident or resident but not ordinary resident.

8. A resident status as determined above by fulfilment of conditions can either be:

a) Ordinary Resident or

b) Resident but not ordinary resident

9. As per Section 6(6), a person is said to be “Resident but not ordinarily resident” in India, if such person fulfils any of the one conditions:

a) An individual who has been Non resident in India in 9 out of 10 previous year preceding that year OR

b) An individual who has been in India for period of 729 days or less during the 7 previous years preceding that year.

To make the above interpretation simpler or in other words, we would like to state that an individual will become an ordinary resident, if both the following conditions are fulfilled:

i) He has been resident in India for at least 2 out of 10 previous years preceding that year AND

ii) He has stayed in India for at least 730 days during the 7 previous years preceding that year.

If one or none of the above conditions are not fulfilled then an individual is said to be “Resident but not ordinary resident” during the previous year.

10. To widen the scope of tax base, the Finance Act,2020 has introduced that the following person will be said to be “Resident but not ordinarily resident” in India in previous year, if such person is:

i) Indian Citizen or Person of Indian Origin, having total Income, other than the Income from foreign sources, exceeding Rs 15 Lakh during the previous year who has been in India for period exceeding 120 days or more but less than 182 days. [ If the said individual resides in India for more than 182 days then he will be treated as “Ordinary Resident for the relevant previous year]

ii) Indian Citizen having total Income, other than the Income from foreign sources, exceeding Rs 15 Lakh during the previous year who is deemed to be resident in India in that previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.

11. Non Resident

As per Section 2(30), “non-resident” means a person who is not a “resident”, and for the purposes of sections 92, 93 and 168, includes a person who is not ordinarily resident within the meaning of section 6(6).

12. Rule 126 of the Income Tax Rules,1962

[Computation of period of stay in India in certain cases.

126. (1) For the purposes of section 6(1), in case of an individual, being a citizen of India and a member of the crew of a ship, the period or periods of stay in India shall, in respect of an eligible voyage, not include the period computed in accordance with sub-rule (2).

(2) The period referred to in sub-rule (1) shall be the period beginning on the date entered into the Continuous Discharge Certificate in respect of joining the ship by the said individual for the eligible voyage and ending on the date entered into the Continuous Discharge Certificate in respect of signing off by that individual from the ship in respect of such voyage.

Explanation : For the purposes of this rule,—

a) “Continuous Discharge Certificate” shall have the meaning assigned to it in the Merchant Shipping (Continuous Discharge Certificate-cum-Seafarer’s Identity Document) Rules, 2001 made under the Merchant Shipping Act, 1958 (44 of 1958);

b) “eligible voyage” shall mean a voyage undertaken by a ship engaged in the carriage of passengers or freight in international traffic where-

i) For the voyage having originated from any port in India, has as its destination any port outside India; and

ii) For the voyage having originated from any port outside India, has as its destination any port in India.

For Better Understanding of Determination of Residential Status of an Individual in India, we have provided the above discussion in diagrammatic representation as below.

We would like to provide the various illustration which would give further clarification in concept to determine the residential status of an individual.

Illustration 1

Mr. A, resident of India, stays for more than 182 days in India then he will be treated as Ordinary Resident in India for the relevant previous year.

Illustration 2

Mr. A, New York Chess Player visits India for various days in every financial year since last 7 years. To determine the residential status for FY 2020-21

| Financial Year | No. of days in India | |

| Scenario I | Scenario II | |

| 2020-21 | 100 | 105 |

| 2019-20 | 95 | 95 |

| 2018-19 | 105 | 110 |

| 2017-18 | 85 | 105 |

| 2016-17 | 103 | 115 |

| 2015-16 | 98 | 100 |

| 2014-15 | 93 | 113 |

| 2013-14 | 109 | 97 |

First, we will check the basic conditions as per Section 6(1), which says that the person is said to be resident if it fulfils any of the below conditions:

i) An individual stay for more than 182 days or more OR

ii) An Individual has been for more than 365 days during the 4 preceding previous years and has stayed for more than 60 days during the previous year.

Scenario I

As we can observed that the first condition is not fulfilled as Mr. A has stayed for less than 182 days during the previous year. Then we will move to second condition wherein Mr. A has stayed for 388 days [95+105+85+103] during the 4 preceding previous years i.e from F.Y 2016-17 to F.Y 2019-20. Therefore, Mr. A satisfies one of the conditions under Section 6(1), he is resident for FY 2020-21.

Once he is resident in India, then we have to further identify whether he is ordinary resident or Resident but not ordinary resident.

As per Section 6(6), a person is said to be “Resident but not ordinarily resident” in India, if such person fulfils any of the one conditions:

a) An individual who has been Non resident in India in 9 out of 10 previous year preceding that year OR

b) An individual who has been in India for period of 729 days or less during the 7 previous years preceding that year.

In this case, Mr. A has stayed for 688 days during the 7 previous years preceding FY 2020-21. Since Mr. A satisfies condition (b), therefore, he is a resident but not ordinarily resident for FY 2020-21.

Scenario II

As we can observed that the first condition is not fulfilled as Mr. A has stayed for less than 182 days during the previous year. Then we will move to second condition wherein Mr. A has stayed for 425 days [95+110+105+115] during the 4 preceding previous years i.e from F.Y 2016-17 to F.Y 2019-20.Therefore, Mr. A satisfies one of the conditions under Section 6(1), he is resident for FY 2020-21.Once he is resident in India, then we have to further identify whether he is ordinary resident or Resident but not ordinary resident.

For the sake of brevity and to avoid repetition, we refer Section 6(6) as mentioned above. In the instant case Mr. A has stayed for 735 days during the 7 previous years preceding FY 2020-21. Since Mr. A does not satisfies any of the above mentioned conditions, therefore, he is a ordinary resident for FY 2020-21.

Illustration 3

Mr. A, being citizen of India, having total income, other than income from foreign sources, of Rs 20 Lakh which is accrue and arise in India and he has stayed in India for 121 days during AY 2021-22. Further, it is observed that Mr. A is not liable to tax this Rs 20 Lakh in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.

As per the concept explained above in Para 9, as Mr. A has stayed for more than 120 days in India, it is concluded that Mr. A will be treated as Resident but not ordinarily resident for AY 2021-22.

Illustration 4

Mr. A, being citizen of India, employed by an Indian ship and is on frequent foreign tour on the ship as member of crew of Indian ship. During FY 2021-22, he visited as under:

i) Ship left from Vishakhapatnam on 10.04.2021 for destination of Singapore. However, the ship first reached Kozhikode from Vishakhapatnam on 17.04.2021 to take passengers from there. Ship left from Kozhikode on 20.04.2021 and reached Singapore on 10.05.2021.

ii) Ship returned from Singapore on 20.05.2021 and came to Kozhikode on 15.06.2021. Ship then sailed to Vishakhapatnam on 24.06.2021.

For the above voyage, the Continuous Discharge Certificate shows the date of joining the voyage on 10.04.2021 and shows date of signing off from voyage on 24.06.2021.

Period from 10.04.2021 to 24.06.2021 comes to 76 days

Similar 2 more trips has been made by Mr. A during FY 2021-22 the period of which is as under:

i) Period from 08.07.2021 to 10.09.2021 comes to 65 days

ii) Period from 01.01.2022 to 25.03.2022 comes to 85 days

Mr. A total stay outside India is 226 days (76 + 65 + 85).

Mr. A stay in India is 139 days (365 – 226) which is less than 182 days, therefore, he is a non resident in India for FY 2021-22.

Here, if Mr. A, being citizen of India, has earned Rs 50 Lakh (other than income from foreign sources) and this Rs 50 Lakh is not taxable in any other country or territory by reason of his domicile or residence or any other reason. Therefore, Mr.A will be said to be “Resident but not ordinary resident for FY 2021-22.

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

(For any queries or feedback in the above mentioned article, the author can be contacted at cakaushikmakwana@gmail.com)

Author Bio