Last year ICAI had revised SA 700, in accordance with revision in ISA 700, by IFAC. Subsequently its effective date was changed to audit after 01/04/2018. The key change in revised SA 700 is Key Audit Matters.

Why Key Audit Matters?

Users of the financial statements have signaled that the auditor’s opinion on the financial statements is valued, many have called for the auditor’s report to be more informative and relevant. The auditor’s report is the key deliverable addressing the output of the audit process. The IAASB intends for its new and revised Auditor Reporting standards to result in an auditor’s report that increases the confidence in the audit and the financial statements, which is in the public interest.

The IAASB believes that in addition to the increased transparency and enhanced informational value of the auditor’s report, changes to auditor reporting will also have the benefit of:

• Enhanced communications between the auditor and investors as well as between auditors and those charged with governance;

• Increased attention by management and those charged with governance (e.g., the audit committee) to the disclosures in the financial statements to which reference is made in the auditor’s report; and

• Renewed focus of the auditor on matters to be reported, which could indirectly result in an increase in professional skepticism.

What is Key Audit Matters?

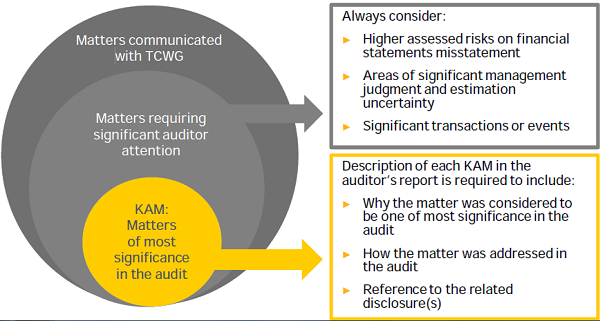

Key Audit Matters (KAM) are defined as “Those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period. Key audit matters are selected from matters communicated with those charged with governance.”

KAM are selected from matters communicated with TCWG

Are KAM forms to be a qualification in auditor’s report?

Stakeholders are used to the binary “pass/fail” opinion.With KAM reporting, the stakeholders might perceive it as a piecemeal qualification on matters determined to be KAMs. The description of auditor’s procedures contained in the KAM section of the auditor’s report might be misunderstood without proper context.

One very important message to be conveyed to the stakeholders is that KAMs are not an avenue for the auditor to express qualification on matters highlighted as KAMs. KAMs are addressed in the context of the audit of the financial statements as a whole, and the auditor does not provide a separate opinion on these matters.

Determination of Key Audit Matter (KAM)

When KAM’s are required to be reported?

As per paragraph 30 of SA 700 KAM is required to be reported in audits of listed entities.

As per paragraph 31 auditor may determine to communicate key audit matters in the auditor’s report, the auditor shall do so in accordance

Benefits of KAM

Illustrative list of benefits of KAM is enlisted below:

a. Increase transparency about the audit that was performed.

b. Focus investors and other users on areas in the financial statements that are subject to significant management judgment and significant auditor attention.

c. Provide users a basis to further engage with management and TCWG

d. Renew auditor focus on matters to be communicated, which could indirectly result in an increase in professional skepticism, among other contributors to audit quality.

KAM Description

Description of KAM will always include:

a. Why matter was considered to be a KAM

b. How the matter was addressed during the audit by auditor and management

c. Reference to related disclosures

Further, how matter was addressed in audit may include:

i. Aspects of auditor’s response or approach.

ii. Brief overview of procedures performed

iii. Indication of outcome of the auditor’s procedures

iv. Key observation with respect to matters.