The Chartered Accountants Act of 1949 serves as a guiding document, ensuring the integrity and professionalism within the accounting community. Embedded within this framework is Section 21A, which empowers the formation of the Board of Discipline. Under this jurisdiction, the recent case of CA. Rajesh Kumar Chandak, as deliberated under Rule 14(9) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, has reached its conclusion.

The matter, presented before the Board of Discipline, involved serious allegations against CA. Rajesh Kumar Chandak, pertaining to his involvement in various corporate entities beyond the purview of his role as a Chartered Accountant. The Complainant, Sh. Vikram Singh Chopra, brought forth compelling evidence indicating Chandak’s active participation in the administrative functions of these entities, including signing financial statements and directors’ reports. Despite his pivotal role, Chandak allegedly failed to disclose these involvements to the Institute of Chartered Accountants of India (ICAI), thereby violating established regulations.

Following a thorough examination of facts, submissions, and documents, the Board of Discipline, chaired by CA. Prasanna Kumar D., and consisting of Mrs. Rani Nair (IRS, Retd.) as the government nominee, arrived at several key observations and findings.

Firstly, the Board addressed procedural concerns raised by Chandak’s counsel, affirming the validity of the proceedings and dismissing claims of impropriety. It was emphasized that the composition of the Board remained unchanged, and ample opportunities were provided for both parties to present their cases.

Secondly, the Board refuted Chandak’s assertion of the complaint being time-barred, asserting that the delay did not impede his ability to mount a defense adequately.

Moreover, the Board dismissed the argument questioning the locus standi of the complainant, reaffirming its mandate to investigate allegations against any member of the Institute.

In adjudicating the matter, the Board delineated the distinction between criminal proceedings and disciplinary inquiries, emphasizing the standard of proof required—a preponderance of probabilities rather than proof beyond a reasonable doubt.

Crucially, the Board analyzed Chandak’s role in the subject companies vis-à-vis the provisions of the Companies Act and the Chartered Accountants Regulations. Despite Chandak’s claims of acting as a Director Simplicitor, the evidence presented suggested a more involved role inconsistent with this designation. Financial statements were signed, and responsibilities beyond mere attendance at board meetings were assumed, contravening regulatory mandates.

Furthermore, Chandak’s receipt of director fees and other incomes from these entities, as evidenced by his income tax returns and Form 26AS, underscored his active engagement beyond permissible limits.

Lastly, the Board scrutinized the Articles of Association of the implicated companies, affirming that Chandak’s role transcended that of a Director Simplicitor, as envisaged by the regulations.

In light of these findings, the Board concluded that CA. Rajesh Kumar Chandak was guilty of professional misconduct, as defined under Item (11) of Part I of the First Schedule to the Chartered Accountants Act, 1949.

[PR-188/2017-DD/247/2017/BO D/582/2020]

BOARD OF DISCIPLINE

Constituted under Section 21A of the Chartered Accountants Act 1949

Findings under Rule 14(9) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007

File No.: PR-188/2017-DD/247/2017/BOD/582/2020

QUORUM:

CA. Prasanna Kumar D., Presiding Officer

Mrs. Rani Nair (IRS, Retd.), Government Nominee

(Attended Physically)

(Through Video Conferencing)

In the matter of:

Sh. Vikram Singh Chopra,

…………………..Complainant

-Vs.-

CA. Rajesh Kumar Chandak

DATE OF FINAL HEARING : 3rd January, 2022

PLACE OF HEARING : New Delhi/ Through video conferencing

PARTIES PRESENT : (Through video conferencing)

Counsel for Complainant : CA. A. P. Singh

Respondent : CA. Rajesh Kumar Chandak

Counsel for Respondent : CA. Ashish Makhija alongwith his assistant Ms. Richa Singh

Findings:

Charge alleged :

1. The Respondent was involved and engaged as Director in various body corporates. In one of such body corporate, he along with one of the partner in his CA firm, were the only Directors, where the Company had business activities, in which the Respondent along with his partner participated and played an active role in its administration. The Respondent signed the directors’ report, financial statements and various other Forms of the bodies corporate which clearly prove that he was engaged in the business operations of those companies. The Respondent also signed the Forms for investments made by the companies in which he was a director. That is by no stretch of imagination the role of a Director Simplicitor. The Respondent did not make full and fair disclosures to ICAI and did not seek the appropriate permission to be involved in the overall activities of the Companies.

The Complainant submitted the name of following 8 companies and alleged

that the various documents in those companies were signed by the Respondent and also submitted other in Formation in relation to each of the following company:

I. M/s Hare Krishna Properties Pvt Ltd

ii. M/s Kuldeepak Vanijya Pvt Ltd

iii. M/s Rachit Vanijya Pvt Ltd

iv. M/s High Value Investments Pvt Ltd

v. M/s High Value Securities Pvt Ltd

vi. M/s Sigma Services Pvt Ltd

vii. M/s Sushwani Info Systems Pvt Ltd

viii. M/s High Value Management Consultants Pvt Ltd.

The Respondent was the arbitrator in the family settlement of CA Raj Singh Chopra, partner in his CA firm and was aware that his partner was wholly involved in his family business and firms. Despite this knowledge, the Respondent continued to remain in partnership with CA. Raj Singh Chopra and thus gave false declarations and in Formation to ICAI and brought disrepute to the profession and contravened the provision contained in the regulations and guidelines issued by CAI.

The Director (Discipline) in his Prima Facie Opinion dated 16th June, 2020 held the Respondent Prima Facie Guilty in respect of the Charge specified at pars 1 above and the Board of Discipline concurred with the said Opinion of the Director (Discipline) holding the Respondent Prima Facie Guilty of ‘Professional Misconduct’ falling within the meaning of Item (11) of Part I of the First Schedule to the Chartered Accountants Act, 1949. Accordingly. the Respondent had been examined in respect of the said Charge during inquiry.

The Board also noted that the Complainant has filed another complaint against one of the partner of the Respondent Firm, CA. Raj Singh Chopra and the said case is dealt with separately in case reference no. PR-189/2017-DD/248/2017/ BOD/597/2021.

Brief of Proceedings held:

2. At the time of hearing held in the case on 29th December, 2021, the Complainant and the Respondent alongwith their respective Counsels were present before the Board through video conferencing. They confirmed that they have read and understood the contents of the modalities and protocols of e-hearing and follow them. The Complainant and the Respondent were put on oath. The charges alleged against the Respondent were taken as read with the consent of parties present. On being asked by the Board as to whether the Respondent pleaded guilty in respect of the charges alleged against him, he replied in negative. Thereafter, the Counsel for the Complainant and the Respondent made their respective detailed oral submissions before the Board. The Respondent was examined by the Board. To counter the submissions of the Counsel for the Respondent, the Counsel for the Complainant needed some time and requested for adjournment of the hearing as he had to catch the flight. Looking into the request of the Counsel for the Complainant, the Board decided to adjourn the hearing in the case with the direction to the Respondent to provide the signatory details of the companies under question.

3. Thereafter. at the hearing held in the case on 3rd January, 2022, the Counsel for the Complainant and the Respondent alongwith his Counsel were present before the Board through video conferencing. Further to the hearing held in the case on 29th December 2021, the Counsel for the Complainant made his detailed oral submissions before the Board. The Counsel for the Respondent also made his submissions before the Board. On consideration of the documents and submissions on record, the Board decided to conclude the proceedings in the case.

4. After the conclusion of hearing in the case, the Respondent has filed further submissions dated 141h January. 2022 before the Board and the same were also considered by the Board while arriving at its Findings in the case.

Brief submissions of the Respondent:

5. The Board noted that the Respondent, in his defence, inter-alia, submitted as under:-

a. The Respondent signed MBP-1 and submitted that the said Form is required to be signed by the individual director himself. Further, there is no exceptions for Director Simplicitor for any statutory compliance violations and as compliance with the requirement of law cannot be construed as involvement in day to day activities, when the same is done on exigencies in the capacity of Director Simplicitor. There is no bar on Director Simplicitor to sign the documents, required by law.

b. The use of digital signature for uploading the Forms required by the Statutes is for complying with requirements of law and in no circumstances can be construed that the person whose DSC has been used, occasionally, in uploading the Forms, is involved in day-to-day activities.

c. Interest income on loan given to a Company for purchase of property, has been considered as receipt of remuneration.

d. There is a difference between Director Fees and Director Remuneration. Director Fees are paid for attending Board meetings whereas in case of Director Remuneration, there is a relation of employer and employee. The Respondent has received Director Fees for attending Board meetings which has been considered as receipt of remuneration. Even, Director Fees received for attending Board Meetings of M/s. JJ Exporters Ltd and M/s. JJ Spectrum Silks Ltd (both listed Companies) was considered as receipt of remuneration.

e. The ROC Form certification charges received from M/s Highvalue Management and Consultants P Ltd. for certifying various Forms uploaded at ROC has been considered as receipt of remuneration and an activity which requires specific permission from the Council.

f. Regarding the submissions that Respondent had never received any remuneration from any of the Companies, the Respondent reiterated that from his accounts submitted for FY 2006-07 to FY 2015-16, it is clear that Respondent has not received any remuneration from any of the Companies other than Director sitting fees for attending Board Meetings. Interest on Loan and Fees for certifying ROC Forms in the capacity of a practising Chartered Accountant.

g. Regarding Form MGT-7 the Respondent submitted that the said Form requires -“Details of Directors and Key Managerial Personnel as on the closure of financial year”. The details of Directors given in Section VIII of the Form MGT-7 are treated as details of “Key Managerial Persons”.

Part VIII of Form MGT-7 deals with “DETAILS OF DIRECTORS AND KEY MANAGERIAL PERSONNEL”, wherein;

Section “A” requires Composition of Board of Directors, segregating between numbers of executive & Non-Executive Directors.

The preface of Section B, requires, – “Number of Directors and Key Managerial Personnel as on the financial year end date” — meaning that details of Directors as well as KMP needs to be given.

Section B (i), requires details of Directors & Key Managerial Personnel as on the closure of financial year. The various options for designations in drop down facility in the Form MGT-7 are

a) Director

b) Manager

c) Managing Director

d) Company Secretary

e) Alternate Director

f) Additional Director

g) Director appointed in Casual Vacancy

h) Nominee Director

i) Whole Time Director

j) CEO

k) CFO

As per Section 2(51) of the Companies Act 2013, the KMP has been defined to be a CEO or MD or Company Secretary or WTD or CFO.

If wrong nomenclature in respect to designation is given, then the Form is liable to fail the pre scrutiny test by MCA 21 and will not be allowed to be uploaded.

Section B(ii) requires – Particulars of Change in director(s) and Key Managerial Persons.

It has been deliberately ignored that, in the multiple MGT-7 annexed & referred to by the Complainant:

in the Section “A” dealing with Composition of Directors. the directors are stated as “Non-Executive” directors except for one Company where there is one Executive Director (Who is not the Respondent).

The Preface of Section B requires Number of Directors Key Managerial personnel as on the financial year end date – meaning that the details of all the Directors as well as Key Managerial persons (As given in page 3 under requirement of Section B (i)) detailing the options available in are to be given in Section (B)(i)

In the options available in Form MGT-7 requiring designation of the person, “Director” is the only designation which is the nearest resembling designation that of Director Simplicitor.

The Respondent has not been designated as any other Designations for which options are available in Form MGT 7, Part VIII B. In the list of options available and in absence of option for Director Simplicitor, the nearest resembling option is that of “Director” and as such the Respondent has been shown as “Director”, though being Director Simplicitor.

The number as inserted in Box for providing -“Number of Directors and Key Managerial Personnel as on the financial year end date” is the total number of Directors (Executive & non-executive) + Key Managerial Person, as mentioned in Section VIII (A)- Composition of Directors & Key Managerial Persons.

h. Signing of various documents in relation to Harekrishna Properties P Ltd, Kuldeepak Vaniiva P Ltd, Rachit Vaniiva P Ltd, Hiqhvalue Investments P Ltd, Hiqhvalue Securities P Ltd, Sushwani Infosystems P Ltd, Highvalue Management & Consultants P Ltd and Sigma Services P Ltd. :

a) All the above-mentioned Entities are Body Corporates governed by the Companies Act and are Board Managed Companies. There are certain compliances which are required to be done, every year, with ROC, Income Tax and other statutory bodies. Default in these compliances, leads to Prosecutions and other penalties and all the Directors are individually and collectively held responsible for non-compliance.

b) The Respondent signed on the purported documents only in extreme exigencies like non availability of the other signatory at the then point of time/ non availability of the DSC of other Director etc. Merely signing of Compliance related documents does not mean that he is not a director Simplicitor or that he is a full time Director involved in day to day activities of the Companies, ignoring the fact that neither he was a Whole time Director or Managing Director or Key Managerial Person.

c) None of the above-mentioned Companies have Managing Director or Whole time Director. In many Companies there were only two Directors. The Directors Report and the financial statements were signed by the available two Directors, as per requirement of the law and in case of Highvalue Investments P ltd., one of the signatories was Executive Director.

d) Even the other Documents mentioned as signed by the Respondent were occasionally signed by him in the Capacity of Director Simplicitor, as the same were required for statutory filing purposes and does not imply his involvement as a working Director of the Company.The same were sometimes signed by him, when the other directors were not available.

e) All the Companies mentioned by the Complainant, where the Respondent was a Director’ Simplicitor, are engaged in the activity of Investments in Shares & Properties. Both these activities cannot be categorized as Business activity and are permitted to be carried on by a Practicing Chartered Accountant.

Some of the Companies, in which the Respondent was a director Simplicitor, were family-owned Companies and were Formed/purchased as a “SPV” to deploy funds of the family. The Respondent was inducted, by virtue of being a family member, to be a Director Simplicitor, so that his interest in the family assets was protected and ensure smooth transition.

The Companies do not have any business. The Activity of the Companies are Investments in Shares, Securities and Property.

If the Corporate veil is lifted, the fact will emerge that the Companies are of SPV nature for investing in Shares and Properties and for ensuring protection of stakeholders and his involvement as only the beneficiary. In a family, no person will like to lose control over his assets during his life time and also like to plan heritance through smooth transition and as such the route of Corporate entities have been adopted.

A Director Simplicitor is also a Director and the duties and Rights of the Directors are defined in the Companies Act. A Director is duty bound to act in a fiduciary capacity and no such acts done by any person in a fiduciary capacity can be termed as illegal or termed as Professional misconduct.

i. MOA and AOA are the charter of the Company entailing what is to be done and how it is to be done i.e. how the Company will function. Moreover, the AOA are taken, as is, from the standard table as detailed/given in the Schedule to Companies Act.The content of MOA and AOA does not define the function of the Director Simplicitor. These documents are incorporating document of the company and only defines what is to be done and how it is to be done as prescribed by the Companies Act (as amended from time to time). It is sole decision of the Board Members among themselves to delegate the duties which is done after the incorporation of the Company. Contents of MOA and AOA cannot be taken as evidencing document that whatever mentioned therein also fall within the duty of “Director Simplicitor”. It is the Board which defines the duties of Director.

j. How can it be presumed that statutory documents of a company will be governed by a definition of a post (Director Simplicitor) which exists only for the members of !CAI. These documents are filed as per law of the land and for the benefit of its’ shareholders. There is no designation in Companies Act as “Director Simplicitor.

k. Company wise issues raised are dealt in the paragraphs below: I. Harekrishna Properties P Ltd

The Company was formed by practicing professionals to Purchase office Property and is a Board Managed Company.

a) There were 3 directors on the Board as on the date of EGM, all of whom were practicing professionals. In such case, extract of Minutes of EGM for ROC filing is required to be signed by at least one Director, certifying the authenticity of the extracts, and therefore the same was signed by the Respondent, in the capacity of Director Simplicitor. Attending EGM is in the fiduciary capacity of a Director Simplicitor, is permissible as per guidelines for practicing Chartered Accountant, not requiring any specific permission (in view of Clause 2.14.1.11 (iv)(b) of the Code of ethics) and consequently, it also covers certifying the extract of resolution passed at EGM attended by the Respondent.

b) Regarding declaration u/s 33(1) signed on Formation of the Company signed by the Respondent as promoter Director:

Clause 2.14.1 .1 1 (iv)(b) of the Code of Ethics, Volume II (Revised 2020) states ” There is no bar for a member to be a Promotor/Signatory to the Memorandum and Articles of Association of any Company. There is also no bar for such a Promoter/Signatory to be a Director Simplicitor of that Company irrespective of whether the objects of the Company include areas which fall within the scope of the profession of Chartered Accountants. Therefore, members are not required to obtain specific permission of the Council in such cases. It must be clarified that under Section 25 of the Chartered Accountants Act, no Company can practise as a Chartered Accountant.”

The declaration is required to be signed by a promoter Director, declaring the fulfillment of requirement of Companies Act, 1956 and It was signed by the Respondent for incorporation of the Harekrishna Properties P Ltd and has been conveniently considered in day-to-day activity of a Company which was not in existence (Under incorporation) on the date of signing the declaration.

c) The Form 32 filed alongwith incorporation documents and Formalities of Forming the company, as referred to, needs to be signed by the prospective promoter director .The Respondent, as one of the promoter director, to comply with the requirement of the Companies Act, 1956 for Formation of the Company has digitally signed Form 32. This is well within the permission as per Clause 2.14.1.1 1 (iv)(h) of the Code of Ethics, Volume 11 (Revised 2020).

It has been deliberately ignored that the Form was for Formation of a new Company, as stated in point 1 of Form 32. Again, a document of a nonexistent company (Under incorporation) on the date of signing the Form 32 and has been conveniently considered in day-to-day activity of a Company which was not in existence (Under incorporation) on the date of signing the Form.

II. Kuldeepak Vanijya P Ltd

The Company is owned by 1Mr. Sanjay Mundra. The Respondent was appointed as a simple non-executive Director, to comply with the requirement of minimum directors in a private limited Company, as prescribed by the Companies Act, 1956. The Activities of the Company is investments and are carried out in Mumbai, by the other Director Mr. Sanjay Mundra. Evidence for the same are attached vide Annexure D (which includes Proof of residence of Mr. Sanjay Mundra, Address of Depositary, Evidence of Bank account in Mumbai. Resolution for opening Bank Account).

The Company is a NBFC Company regulated under Guidelines issued by the Reserve Bank of India and had only two Directors, namely Mr. Sanjay Mundra and the Respondent. Any addition of Director needs prior approval of the Reserve Bank of India. Application for appointment of another Director is pending with the RBI under NBFC Regulations.

a) As no Managing Director was appointed by the Company, the Respondent was one of the two directors who signed the Directors report in the capacity of Director Simplicitor.

b) The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by the only two directors of the Company i.e the Respondent (in the capacity of Director Simplicitor) and the other director.

c) The MOA of the Company was signed as certified to be true copy for Compliance with ROC, Kolkata.

It is to be noted that the Registered Office of the Company is in Kolkata. As the other Director is based in Mumbai and therefore in the absence of the other director in Kolkata, the MOA was signed by the Respondent to certify it to be true, which is allowed as per Clause 2.14.1.11(iv)(b) of the Code of ethics, Volume II.

d) The Respondent has been stated as a non-executive director in MGT-7 which has been deliberately ignored while framing allegations against him.

e) No such appointment of KMP has been made by the Company.

III. Rachit Vanijya P Ltd

a) In the said case, as no Managing Director was appointed by the Company, the Respondent was one of the two directors who signed the Directors report in the capacity of Director Simplicitor.

b) The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by the then available Director i.e the Respondent (as Director Simplicitor) and the other director.

However, another Director has been appointed on 30.4.2018 and thereafter all financial statements have been signed by Mrs. Anjana Chopra and Mr. Subhash Sharma .

a) The declaration in MGT -7 clearly establishes Respondent as Non-Executive Director.

b) It has been alleged that “Copy of resolution adopted by the Board of Director of Rachit Vanijya P Ltd” on 30th August 2008 to authorize the Respondent to make investments on behalf of the Company and to sign all necessary documents in this regard and signed by the Respondent”.

(i) The resolution attached for the Board Meeting states that the Board Meeting was held at 4pm on 30.8.2008, whereas the meeting was held at I Iam,(Copy of Minutes of the meeting held on 30.8.2008 attached vide Annexure “E” 2 thereby raising a question on the authenticity of the document attached.

(ii) Authenticity of the document attached in the Complaint needs verification in light of the facts detailed herein below dealing with opening of Bank account with forged documents & false signature.

(iii) Name of Mr. Subhash Sharma, director being authorized, has been deliberately suppressed. Copies of Application Forms of the investments made by Rachit Vanijya P Ltd can be produced, if required, as an evidence that the Forms were not signed by the Respondent.

(iv) The Copy of minutes attached vide Annexure “E” clearly states that no such resolution was passed in the said meeting. Mr. Subhash Sharma, Director was authorized in earlier meeting for making investments and signing Application Forms, thereafter no resolution was passed to supersede the resolution authorizing Mr. Subhash Sharma for making investments.

(v) The allegation implies that the Respondent has self-authorized himself in a Board Managed Company, to deal with the transactions of the Company and the investee Company has accepted the ” void ab initio Form”.

This further strengthen the fact that this is a forged document.

(vi) Even if such type of document exists, they are null and void, ab initio, as Respondent was never authorized by the Board for the said purpose.

IV. Highvalue Investments P Ltd

a) The Directors of the Company were Late Ramanlal Chandak —Respondent’s Father, Respondent and Mrs, Rashmi Chandak. Respondent’s Father, who expired on 24.1.2018, was suffering from Parkinson Disease since 2004 and as such he was not in a position of signing the financial statements and related papers. As such, the Respondent had no option but to get the Board Report signed by the other 2 directors including him.

Mr. Harsh Chandak, who became major on 10.11.2014, was appointed Director of the Company on 1.3.2018, on completion of 21 years of age and obtaining approval from the RBI under NBFC Regulations, and all the accounts thereafter has been signed by Mr. Harsh Chandak and Mrs. Rashmi Chandak.

b) In the said case, as no Managing Director was appointed by the Company. the Respondent was one of the two directors who signed the Directors report in the capacity of Director Simplicitor.

c) As regarding the Board Report wherein, it has been mentioned that “the Company does not have any key managerial person other than present Directors”, the Respondent stated that the disclosure in the Director Report has been misinterpreted, as in practice, a standard Format of Board Report with specific applicability pertaining to respective companies are adopted. However, the said clause in respect to KMP is not applicable to a private limited Company.

This reporting disclosure is void, is also corroborated by the MGT-7, Part VIII (B)(i) wherein the designation of the persons has been mentioned as “Director” and not MD/WTD/CEO/CFO/Company Secretary, Manager etc

However, from subsequent years onward, the said clause has been suitable amended as per requirement of law.

d) Only Mrs. Rashmi Chandak was an executive Director.

Certain compliance needs to be done by the Company to designate a person to be KMP. As the Company does not have any key managerial person, there was no need to making, such compliances.

e) The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by the then available Director i.e the Respondent (as Director Simplicitor) and the other one being executive director.

However, another Director has been appointed on 1.3.2017 and thereafter all financial statements are signed by Mrs. Rashmi Chandak, Executive Director and Mr. Harsh Chandak.

f) “Extract of Minutes of the BOD meeting required for uploading Form 2 for allotment of shares was signed by the Respondent, for compliance of the statutory regulations”.

As per Companies (Issue of Share Certificate) Rules, 1960 specifies that Every share certificate shall be signed by two directors and one authorized signatory and shall be issued under the seal of the Company.

Both the Directors, the Respondent and Mrs. Rashmi Chandak were authorized to do all such acts relating to allotment of shares. Probably, the Complainant has intentionally not mentioned the name of Mrs. Rashmi Chandak.

As already explained about the illness of the 3rd director namely Late Raman Lal Chandak and his inability to sign due to shivering of hands pursuant to Parkinson Disease, the names of the remaining two directors were mentioned in the resolution.

Further increasing of Share Capital cannot be termed and included in day-to-day activities.

g) The declaration in MGT-7 clearly establishes Respondent as Non-Executive Director.

h) In order to comply with the statutory requirements in time, the Form was digitally signed by the Respondent due to unavailability of Digital Signature of the other Director.

i) AOC-4 is, a compliance related filing and has been digitally signed under Respondent’s signature, as the other director were not having active digital signature. This was one of the events and subsequently all such Forms are signed generally by other Directors.

j) Copy of application Forms for investments in equity shares of other Bodies Corporate and signed by the Respondent:The Copies of Forms attached were not the Forms through which investments were made in Freya Shipping Agencies P Ltd. They appear to be forged documents.The Complainant has stated in one of his affidavits before the High Court at Calcutta that all the Documents of M/s Freya Shipping Agencies P. Ltd are not with him but are in possession of his brother Mr. Raj Singh Chopra. Copy of Affidavit attached. The Complainant vide letter dated 10.3.2017, attached vide Annexure ” F-24 & F25″ addressed to Mr. Raj Singh Chopra has affirmed that ” The allegation with regard to possession of statutory records and accounting records are completely false and all the documents of the company have always been in your possession.” That is, Complainant stating that the Statutory & Accounting documents of the Freya Shipping Agencies P Ltd were not in his possession.

As the Complainant is in litigation with his brother Mr. Raj Singh Chopra and he has stated under OATH before the High Court Calcutta that he had no access to the documents of Freya Shipping Agencies P Ltd and therefore authenticity of the Forms attached is doubtful and needs verification. Under the said facts, either the affidavit given by the Complainant before the High Court at Calcutta is false or the Form attached is forged. Therefore. no reliance can be made on any such document, the authenticity of which is questionable. This matter ought to be reported to High Court. Calcutta, as making a false statement under oath is a contempt of the Court.

k) The Respondent was never authorized by the Board to make decision regarding making investments or sign the application Forms for investments on behalf of the Company.Mr. Ramanlal Chandak, Director of the Company was authorized to make investments. as per resolution passed in the meeting of Board of Directors held on 30.6.1993. Subsequently, Mrs. Rashmi Chandak, Director of the Company was also authorized to make investments, as per resolution passed in the meeting of Board of Directors held on 30.3.1999.The Company has made many investments since Incorporation and the papers have been signed by other Director. Few of the Application’ Forms (Including the true copy of the application Forms for making investments in Freya Shipping Agencies P Ltd) are attached as evidence.

Even. if at all, there is an existence of such a Form, it is a dummy Form and is void “ab-initio” owing to the fact that the Board never authorised Respondent to make decision regarding making investments or sign the application Forms for investments. Any such Form, even if in existence, would have been immediately rectified before the investee Company processed the application. The Complainant, with a mala-fide intention has intentionally misstated the facts.

V. Hiqhvalue Securities P Ltd

a) Both the promoter Directors were the Practising Chartered Accountants. There were only two directors of the Company and the Company was a Board Managed Company. For Increase in Capital. Form 2 was required to be signed by one of the Directors and accordingly Form 2 was signed, by Respondent as Director Simplicitor.

However, subsequently, another Director was inducted on the Board. w.e.f 29.9.2017.

b) The declaration in MGT -7 clearly establishes Respondent as Non-Executive Director.

) As a matter of Practice and as per requirement of Companies Act, 2013 Directors need to Sign the financial Statements and as the Company had only 2 Director, both of them signed.

The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by both the two Directors as Director Simplicitor.However, another Director has been appointed 29.9.2017 and thereafter all accounts are signed by Mrs. Anjana Chopra & another Director.

VI. Sushwani Infosystems P Ltd

The Company was Formed on 27.5.2011 to Purchase Office/ Property by Mr. Sajan Surana and Mr. Subir Jain. Subsequent to purchase of the property by Respondent’s family, the Company got transferred to Respondent’s family and Respondent, Mrs Rashmi Chandak and Mr. Harsh Chandak were inducted as Director on 5.5.2015.

a) As no Managing Director was appointed by the Company, Respondent was one of the two directors who signed the Directors report in the capacity of Director Simplicitor. The erstwhile owners, the other Directors, logically did not sign the same.

As regarding the Board Report wherein, it has been mentioned that “the Company does not have any key managerial person other than present Directors”, the Respondent stated that the disclosure in the Director Report has been misinterpreted, as in practice, a standard Format of Board Report with specific applicability pertaining to respective companies are adopted. However, the said clause in respect to KMP is not applicable to a private limited Company. This reporting disclosure is void, is also corroborated by the MGT-7, Part VIII (B)(i) wherein the designation of the persons has been mentioned as “Director” and not MDNVTD/CEO/CFO/ Company Secretary, Manager etc.

However, from subsequent years onward, the said clause has been suitable amended as per requirement of law. Directors report for year ending March 2017 to March 20, copies of which are enclosed for reference.

Certain compliance needs to be done by the Company to designate a person to be KMP. As the Company does not have any key managerial person, there was no need to making such compliances.

b) Financial Statements for year ending March 2016, were signed by the Respondent as a Director Simplictor. This was the first year after acquisition, for abundance precautions, the same was signed by the Respondent (As Director Simplicitor) and Mr Harsh Chandak. Thereafter the financial statements were signed by Mr. Harsh Chandak & Mrs Rashmi Chandak .

The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by the then available Director i.e Respondent (as Director Simplicitor) and the other director. The erstwhile owners, Mr. Sajan Surana and Mr. Subir Jain, the other Directors, logically did not sign the same.

c) Form MBP-1 deals with “Notice of Interest by Director” and as such the Respondent has informed the Company of his interest in other Companies pursuant to Section 184(1) of the Companies Act and Rule 9(1). The notice has to be given by the individual and accordingly, the Respondent has signed the Form as it is a declaration to be given in his individual capacity.

d) It has been alleged that the name of Respondent has been shown as “Director and key Managerial Person” in MGT-7 filed for the year ended 31st March 2016.The declaration in MGT -7 clearly establishes Respondent as Non-Executive Director.

VII. Highvalue Management & Consultants P Ltd

This Company is the owner of the office property located at 402 Bentinck Chambers, 37A Bentinck Street, Kolkata 700069, which was taken on rent by M/S R K Chandak 8 Co, as its office since 2002 to 2019. R K Chandak & Co, is a Partnership firm and a Chartered Accountant firm.

a) The Respondent and his father were the promoter director of the Company. Pursuant to his father’s illness, another director, his wife was inducted as Director in the Company on 17.11.2003 and since then the Respondent and his wife both are signing the documents, as required by law. Accordingly, Director’s report, Financial statements were signed by him and his wife. Subsequently, Harsh Chandak, Respondent’s son was appointed as director in the Company on 28.05.2018 on completion of 21 years of age and since then Rashmi Chandak & Harsh Chandak are signing all documents.

As no Managing Director was appointed by the Company, Respondent was one of the two directors who signed the Directors report in the capacity of Director Simplicitor.

As regarding the Board Report wherein, it has been mentioned that “the Company does not have any key managerial person other than present Directors”, the Respondent stated that the disclosure in the Director Report has been misinterpreted, as in practice, a standard Format of Board Report with specific applicability pertaining to respective companies are adopted.

However,’ the said clause in respect to KMP is not applicable to a private limited Company.

This reporting disclosure is void, is also corroborated by the MGT-7, Part VIII (B)(i) wherein the designation of the persons has been mentioned as “Director” and not MD/ VVTD/ CEO/ CFO/ Company Secretary, Manager etc. However, from subsequent years onward, the said clause has been suitable amended as per requirement of law. Directors report for year ending March 2017 to March 20, copies of which are enclosed for reference.

Certain compliance needs to be done by the Company to designate a person to be KMP. As the Company does not have any key managerial person, there was no need to making such compliances.

b) The Company being a private Company, has not appointed any Managing Director and hence the financial statements were signed by the then available Director i.e the Respondent (as Director Simplicitor) and the other director. For subsequent years, the financial statements were not signed by the Respondent but were signed by Mr. Harsh Chandak & Mrs. Rashmi Chandak.

c) As regarding MGT -7 & AOC-4, which is again statutory compliance, digital signature is essential for filing of the Forms, Respondent’s DSC was used in absence of availability of DSC of other Directors. Subsequently, all such Forms are signed by other Directors.

d) The Respondent relinquished the post of Director w.e.f 1.10.2019. VIII. Sigma Services P Ltd

It has been alleged that the name of Respondent has been shown as “Director and key Managerial Person” in MGT-7 filed for the year ended 3151 March 2016.The declaration in MGT -7 clearly establishes Respondent as Non-Executive Director.

Signing documents in the capacity of Director Simplicitor. which are compulsorily to be signed by a Director, does not tantamount to Professional Misconduct and construing Respondent as Director involved in day to day activities.

I. The complaint is barred by !aches and delay — the complaint contains allegations relating to 2004 onwards and the present complaint has been filed in 2017. The genuineness of the Complaint is under grave doubt in as much as the Complainant was aware of all these facts since 2004 and did not choose to file the complaint till 2017. It also goes on to demonstrate that the present complaint is mischievous and has been filed merely to harass the Respondent. The first complaint was filed on 17.11.2016 vide case no. PR-282/2016-DD/08/2017 and the present complaint with case no. PR 188/2017/DD/247/2017 has been filed on 19.06.2017.

m. The Respondent was one of the Arbitrator in the family dispute of the Complainant. It was only after the award was passed, which was not to the liking of the Complainant, that the Complainant filed this complaint. The Respondent was nominated as an Arbitrator by the father of the Complainant. In this sense, the present complaint is a clear case of counter blast. The complainant is a habitual litigant having filed frivolous complaints in various quorums.

n. The Complainant has no locus standi to file the present complaint in relation to the companies in which the Respondent is the director and has not rendered any professional services to the Complainant. Such a practice of filing frivolous complaints with no locus are to be discouraged by the Institute of Chartered Accountants of India. The Respondent has been in practice as a Chartered Accountant since 1989 and no complaint was ever filed against him except by the Complainant herein and that too after passing of the Family Award by the Respondent, which was not in favor of the Complainant.

o. A Chartered Accountant is entitled to become a director of a company for which no permission of the Institute of Chartered Accountant of India (ICAI) is required. The only restriction is that the Chartered Accountant cannot hold the position as a Managing Director or Wholetime Director of any company. A further restriction is for a Chartered Accountant from becoming a director of a company if he or any of his partners in a Chartered Accountant Firm are the auditors of such a company. The Council of the ICAI considered the question of permitting members in practice to become a director, Managing Director, full time/executive director and referred to Para 2.14.1.11 (iv) on Page 86-87 of Code of Ethics Vol-II (Revised 2020). Further, the ICAI requires obtaining of the specific and prior approval of the council in case a member of the Institute in practice is being appointed to the office of the Managing Director or a whole-time director of a body corporate. This is clearly stated in Appendix No. (9) attached to The Chartered Accountant’s Regulations, 1988 (CA Regulations).

p. The Chartered Accountants in practice are permitted to become a director of the company, besides being permitted to be named as director, promoter, promoter/director or subscriber to the Memorandum and Articles of Association of any company. The only bar is to become a Managing Director or Wholetime director of a company. The other condition that must be fulfilled is that the Member in practice who is a director, promoter, promoter/director or subscriber should not receive any remuneration except for attending meetings of the Board of directors or any of its committees of which he is a member. In the present case, the Respondent was a Director Simplicitor in a few companies and was neither a Managing Director nor a Whole-time director of any such company. It is also pertinent to state that the Respondent did not receive any remuneration from any of these companies except sitting fees for attending the Board/Committee meetings.

q. The Respondent further referred to the judgment of Division Bench Hon’ble Delhi High Court in Yogeshwari Kumari vs The Institute of Chartered Accountants of India & Anr, (20101160 CompCas11(Delhi) dated 13.09.2010 LPA 455 of 2010, wherein Clause (11) was considered by the Hon’ble Delhi High Court and it was held as under:

“9. On a perusal of Clause (11), it is quite vivid that the RespondentNo.2 was not a whole-time director of LSPH; he was not engaged in any business or occupation and, therefore, the First part of the Clause does not get attracted to his case. As far as the proviso is concerned, a Chartered Accountant is not disentitled from becoming a director of a company. The only rider is that he should not be interested in such company as an auditor. The terms which have been laid emphasis upon and correctly so are “such company” and the RespondentNo.2 is not the auditor of LSPH. He is the auditor of LPHM which is a separate corporate entity. Regard being had to the concept of different furls entity and keeping in view the concept of disqualification which has to be strictly construed, we are of the considered opinion that the analysis made by the learned Single Judge is absolutely impeccable.”

r. Mere signatures on the Director’s Report, Financial Statements and other forms do not change the status of the Respondent as Director Simplicitor. Though the Respondent has signed Financial Statements, Directors’ report in pursuance of the provisions of Companies Act, 2013, yet it cannot be construed that the Respondent was engaged in managing the affairs of such companies. By affixing his signatures as per the statutory provisions, the Respondent was primarily complying with the statutory provisions. Signing of the Forms, Financial Statements and Directors’ report is a ministerial act which tags along with the position of a Director. It does not tantamount to the Respondent managing the affairs of the company. This was done by the Respondent merely to make annual mandatory compliances. It may also be noted that there is a difference between annual compliances as per the legal requirement and carrying on day to day business operations. Under no circumstances, annual compliances of law can be considered as carrying on day to day business operations.

s. The Respondent further referred to Para 100.3 of Code of Ethics Volume (Revise 2019) and submitted that as one of the directors of the company, the Respondent was under an obligation to ensure compliance with the provisions of the Companies Act, 2013. Merely complying with the provisions of the Companies Act cannot be considered as managing the operations of the company. It is a regular practice in the companies to get the signatures of the Directors including independent directors on the Financial Statements, Directors Report and other documents. Mere signing of such statutory papers or other documents which are signed in terms of the authority given by the Board of Directors does not amount to managing the company.

t. All the information relating to his Income Tax returns for Assessment Year 2006-07 to 2016-17 along with Form 26AS have been furnished by the Respondent to the Disciplinary Directorate. All these documents clearly indicate that the Respondent has not received any income from these companies except the sitting fees.

u. The Director (Discipline) has erred by relying upon several clauses of the Articles of Association of Highvalue Management and Consultants Private Limited and Sushwani Infosystems Private Limited.

v. The Respondent was not key managerial personnel of any of the companies mentioned in the complaint.

w. The Disciplinary enquiry cases relating to professional misconduct are quasi criminal in nature in as much as member of the profession can have penal consequences which affects his right to practice the profession as also his honour.

x. The Respondent brought on record the copy of the appointment letters issued by the respective Companies, appointing CA Rajesh Kumar Chandak as Simple Director and the minutes of the meeting of Board of Directors of those Companies.

y. No remuneration was received by the respondent in any of the companies — the Respondent has received only the sitting fees for attending the board meetings/committee meetings from these companies as reflected in Income Tax Returns for Assessment years 2006-07 to 2012-13. The Director (Discipline) has pointed out that the Respondent has received certification charges for certification of ROC Forms from High Value Management and Consultants Pvt Ltd. in three Assessment years from 2013-14 to 2015-16. The reply by the Respondent that these amounts were received by the Respondent in his professional capacity for certifying the ROC Forms of the clients of High Value Management and Consultants Pvt Ltd. The Companies Act, 2013 does not bar payment of professional fee to the directors and such payment is not considered as remuneration of the directors. In this connection, the attention of Board of Discipline is drawn to section 197(4) First Proviso which clearly states that if the services rendered by a director are of a professional nature, the same shall not be considered as remuneration. Hence, receipt of professional fees by the Respondent cannot partake the character of remuneration. In addition to the above, the Respondent has also received interest on the loans given to Sushwani Infosystems Pvt Ltd. The payment of interest is also not remuneration.

z. Harerishna Properties P Ltd and Kuldeepak Vanijya P Ltd. were not involved in any business. As regards, Highvalue Securities Pvt Ltd. it is stated that the company has only 2 directors and both are practicing Chartered Accountants. None of the director is a managing or a whole-time director or KMP of the Company. In that sense, the company is a board managed company. The following points merit consideration: –

i. As explained that the Company belonged to Chopra Family

ii. CA Rajesh Chandak was holding only 100 shares out of 120,200 shares issued by the Company. These 100 shares were allotted to him, as being the Subscriber to the MOA & AOA.

iii. The management of the whole of companies belonging to Chopra family was managed by the Chopra Family headed by Mr. Jagat Singh Chopra, the staff of operating Companies of Chopra Family and Professionals.

iv. The issue of Trading of Sarees was carried out in almost all the Companies belonging to Chopra Family including in those Companies in which neither CA Rajesh or CA Raj Singh were Director and were managed by Mr. Jagat Singh Chopra, being the head of Chopra Family. No salary was paid in private investment companies of Chopra Family, which were looked after by the family and the staff of operation Companies. The Companies with no salary also includes the companies in which the Complainant & his father are the only Directors. For reference the total salaries/service charges/professional charges etc in companies of Chopra family were as follows:

| Financial Year | Amount (Rs.) |

| 2010-11 | 18I 52I 436 |

| 2011-12 | 23.10,994 |

| 2012-13 | 62.07,885 |

| 2013-14 | 86,51,354 |

| 2014-15 | 91,27,031 |

| 2015-16 | 99,87344 |

Once the Company was handed over to CA Raj Singh Chopra, as per family settlement, there were no trading transactions.

Submissions of the Complainant:

6. The Board noted that the Counsel for the Complainant stated before the Board during the hearing that the involvement of the Respondent was in 8 Private Ltd. Companies. There are certain companies in which no salary payment is there to any employee. He also pointed out the Director’s Report of a few private companies wherein it was categorically stated that the Respondent was one of the directors of the company and the company did not had any Key Managerial person other than them. The Respondent has openly admitted in a number of instances in his own Rejoinder that he has not signed the Financial Statements/Director’s report of certain companies regularly. He has signed the Financial Statements/Director’s report of certain companies when other directors were not available and then he says that from 2018 onwards he is not signing them. From the various documents brought on record. it is evident that he is signing various documents and then he says that he is not involved in the administration of that particular company which is totally not maintainable.

Observations and Findings of the Board:

7. The Board, upon overall examination of the facts of the case, submissions and documents on record observed as under:-.

7.1 . At the outset, the Board noted that after the conclusion of the hearing on 3rd January 2022, the Counsel of the Respondent made a passing observation that at the time of last hearing held in the case on 29th December, 2021, the three member bench heard his case whereas today, it was heard by a two member bench In this regard, the Board observed that Rule 13(2) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007 provides as under:

“The quorum for any meeting of the Board of Discipline shall be two members.”.

Further, there had been no change in the composition of the Board. Thus, the Board held that it had been validly constituted and was well within its powers to conduct and conclude the Disciplinary proceedings. The Board also observed that adequate opportunities were provided to both the parties to the case to represent their case and raising of such plea on the conclusion of the proceedings by the Respondent seemed to be an effort to divert the attention of the Board from the merits of the case.

7.2 As regards the plea of the Respondent that the extant complaint is not barred by principle of laches and delay, the Board held that Rule 12 of CA Rules 2007 is attracted in a situation/circumstances where on account of time lag, the Respondent faces any difficulty in securing proper evidence for his/her defence and it does not ipso facto render the complaint / information as not maintainable. However, in the instant matter, the Respondent has not expressed any difficulty to lead evidence. Therefore, this plea of the Respondent is not sustainable.

7.3 As regards the plea that the Complainant has no locus standi to file the complaint in relation to the companies in which the Respondent is the director and has not rendered any professional services to the Complainant. the Board observed that in the instant case, it is the conduct of the Respondent that has to be examined based on the documents and submissions on record and the Director(Discipline) is duly empowered to investigate any complaint/ information received against any Member of the Institute in terms of the provisions of the Chartered Accountants Act, 1949 read with CA Rules, 2007.The locus standi of the Complainant is not germane to the examination of the conduct of the Respondent.

7.4 The Board further opined that proceedings before it are quasi-judicial in nature where the misconduct can be proved by preponderance of probabilities having regard to the conduct of the Respondent which is distinct from Criminal proceedings where the misconduct has to be proved beyond reasonable doubt. While coming to the said view, the Board took into consideration the decision of the Hon’ble Supreme Court in the matter of “Ajit Kumar Nag —vs-General Manager (PJ) Indian Oil Corporation Limited-AIR 2005 SC ‘4217 wherein the Hon’ble Apex Court held as under:-

‘The degree of proof which is necessary to order a conviction is different from the degree of proof necessary to record the commission of delinquency. The rules relating to appreciation of evidence in the two proceedings is also not similar. In criminal law, burden of proof is on the prosecution and unless the prosecution is able to prove the guilt of the accused ‘beyond reasonable doubt he cannot be convicted by a Court of law. In a departmental enquiry penalty can be imposed on the delinquent Officer on a finding recorded on the basis of ‘preponderance of probability’.”

Similarly, in the matter of Capt. M Paul Anthony —vs- Bharat Gold Mines Limited – AIR….1999 SC 1416 the Hon’ble Supreme Court held as under:-

“In Departmental proceedings, factors prevailing in the mind of the Disciplinary authority may be many, such as enforcement of discipline of to investigate level of integrity of delinquent or other staff. The standard of proof required in those proceedings is also different from that required in a criminal case. While in Departmental proceeding’s, the standard of proof is one of preponderance of probabilities, in a criminal case, the Charge has to be proved by the prosecution beyond reasonable doubt.”

7.5 Thus, the Board viewed that the plea raised by the Respondent is not sustainable. Accordingly, the case was dealt with on its merits by the Board of Discipline, keeping in view, the submissions and documents on record.

8. As regards the charge that the Respondent was engaged in any business or occupation other than the profession of Chartered Accountant unless permitted by the Council, the Board observed that the intent behind having the restrain provided under Item (11) of part I of the First Schedule as stated hereunder has been expressly provided in the Code of Ethics:

“The objective is to restrain members from carrying on any other business in conjunction with the profession of accountancy and combining such work with any business which is not in keeping with the dignity of the profession. Another reason for the introduction of such prohibition is that a Chartered Accountant, if permitted to enter into all kinds of business, would be able to advertise for his other business and thereby secure an unfair advantage in his professional practice.”

Thereafter, the Board took into view Regulation 190A of Chartered Accountants Regulations, 1988, which deals with the provision for Chartered Accountants in practice not to engage in any other business or occupation, and the same reads as below:

“A Chartered Accountant in practice shall not engage in any business or occupation other than the profession of accountancy, except with the permission granted in accordance with a resolution of the Council’.

The permissible categories of engagements approved by the Council under . Regulation 190A, are available in Appendix No. 9 to the Chartered Accountants Regulations, 1988. Further, a member in practice shall be permitted to be a Director (Director Simplicitor), Promoter/Promoter Director, Subscriber to the Memorandum and Articles of Association of any company including a Board Managed Company. Further, the expression ‘Director Simplicitor’ shall be used for an ordinary/simple Director, who fulfills the following conditions :

(a) he is required to attend the Board meetings only.(emphasis provided)

(b) He will not be paid any remuneration except the sitting fees for attending the Board meetings; and

(c) He will be devoting his time for the company only to attend Board meetings and not for any other purpose. (emphasis provided)

A Member in practice is permitted generally to be a Director Simplicitor in any Company including a Board-Managed Company and as such he is not required to obtain any specific permission of the Council in this behalf irrespective of whether he and/or his relatives hold substantial interest in that Company. Further, there is no bar for a member to be a Promoter/Signatory to the Memorandum and Articles of Association of any Company. There is also no bar for such a promoter/signatory to be a Director Simplicitor of that Company irrespective of whether the objects of the Company include areas which fall within the scope of the profession of Chartered Accountancy. Therefore, members are not required to obtain specific permission of the Council in such cases.

9. On perusal of the copies of various documents / evidences in relation to alleged companies, brought on record by the Complainant it is noted that the following documents were signed by the Respondent as its Director:

i Copy of extract of the minutes of EGM of ‘Hare Krishna Properties Pvt Ltd’ held on 28th Feb 2014.

ii. Copy of declaration submitted u/s 33(1) and (2) of Companies Act 1956 in respect of ‘Hare Krishna Properties Pvt Ltd’ .

iii. Copy of Form 32 regarding particulars of appointment of directors of ‘Hare Krishna Properties Pvt Ltd’ (digitally signed).

iv. Copy of directors’ report of ‘Kuldeepak Vanijya Pvt Ltd’ for the year ended on 31st March 2016.

v. Copy of financial statements of ‘Kuldeepak Vanijya Pvt Ltd’ for the year ended on 31st March 2016.

vi. Copy of Memorandum of Association of ‘Kuldeepak Vanijya Pvt Ltd’ filed with ROC on 21st March 1995.

vii. Copy of directors’ report of ‘Rachit Vanijya Pvt Ltd’ for the year ended on 31st March 2016.

viii. Copy of financial statements of ‘Rachit Vanijya Pvt Ltd’ for the year ended on 31st March 2016.

ix. Copy of the resolution adopted by the Board of Directors of `Rachit Vanijya Pvt Ltd’ on 30th August 2008 to authorize the Respondent to make investments on behalf of the Company and to sign all necessary documents in this regard .

x. Copy of directors’ report of ‘High Value Investments Pvt Ltd’ for the year ended on 31st March 2016. The said report also includes the name of the Respondent as ‘Director and Key managerial Personnel’. The Directors report also mentions that the Company does not have any key managerial person other than the present directors.

xi. Copy of financial statements of ‘High Value Investments Pvt Ltd’ for the year ended on 31st March 2016 .

xii. Copy of extract of the minutes of board meeting of ‘High Value Investments Pvt Ltd’ held on 21st August 2017 was signed by the Respondent where the said minutes authorized the Respondent to do all acts as may be required in collection of allotment of equity shares, sign the share certificates and affix the common seal.

xiii. Copy of Form AOC-4 in relation to ‘High Value Investments Pvt Ltd’ for the year ended 31st March 2016(digitally signed).

xiv. Copy of application Forms for investments in equity shares of other bodies corporate and signed by the Respondent.

xv. Copy of Form 2 for allotment of shares in relation to ‘High Value Securities Pvt Ltd’ for allotment on 28th March 2009 and 31st March 2010(digitally signed )

xvi. Copy of financial statements of ‘High Value Securities Pvt Ltd’ for the year ended on 31st March 2016.

xvii. Copy of directors’ report of ‘Sushwani Info Systems Pvt Ltd’ for the year ended on 31st March 2016. The said report also includes the name of the Respondent as ‘Director and Key managerial Personnel’.

xviii. Copy of financial statements of ‘Sushwani Info Systems Pvt Ltd’ for the year ended on 31st March 2016.

xix Copy of directors’ report of ‘High Value Management & Consultants Pvt Ltd’ for the year ended on 31st March 2016. The said report also includes the name of the Respondent as ‘Director and Key managerial Personnel’.

xx. Copy of financial statements of ‘High Value Management & Consultants Pvt Ltd’ for the year ended on 31st March 2016.

xxi. Copy of Form AOC-4 for the year ended on 31st March 2016 in relation to ‘High Value Management & Consultants Pvt Ltd’ (digitally signed).

10. From the above documents, it is noted that the Respondent signed various documents including directors’ report and financial statements of aforesaid 8 companies being the Director of those companies. It is also noted that the Respondent in his defence stated that the activities carried on by the Companies had no bearing or bar on him being appointed as Director Simplicitor where he was neither a Managing Director nor Whole time director in any of the Companies. Further. he had not been entrusted to look after wholly or substantially, the whole of the management of the affairs of the Companies as mentioned in the Complaint and had never received any remuneration from any of the Companies as mentioned in the Complaint for the post of Director Simplicitor. The Respondent also mentioned that the papers / documents signed by him in respect to various companies were only of procedural nature for meeting the compliance of law and all documents were signed by him as Director Simplicitor since at some times, he was the only available director at that point of time. The Board noted that Section 134(1), (6) and (7) of Companies Act, 2013 provides as under:

134. Financial statement, Board’s report, etc

(1) The financial statement, including consolidated financial statement, if any, shall be approved by the Board of Directors before they are signed on behalf of the Board at least by the chairperson of the company where he is authorised by the Board or by two directors out of which one shall be managing director and the Chief Executive Officer, if he is a director in the company, the Chief Financial Officer and the company secretary of the company, wherever they are appointed, or in the case of a One Person Company, only by one director, for submission to the auditor for his report thereon (emphasis added).

(6) The Board’s report and any annexures thereto under sub-section (3) shall be signed by its chairperson of the company if he is authorised by the Board and where he is not so authorised, shall be signed by at least two directors, one of whom shall be a managing director, or by the director where there is one director.

(7) A signed copy of every financial statement, Including consolidated financial statement, if any, shall be issued, circulated or published along with a copy each of—

(a) any notes annexed to or Forming part of such financial statement;

(b) the auditor’s report; and

(c) the Board’s report referred to in sub-section (3).

11. From the above, it is clear that in case of company having more than one director, the financial statement shall be signed by:

— Chairperson of the Company (if authorised by the board of directors) or

— Two Directors (out of which one shall be Managing Director) and

— Chief Executive Officer / Company Secretary / Chief Financial Officer (if they are appointed in the Company)

However, in case of alleged companies, the financial statements were signed by the directors of the Companies including the Respondent. But the Respondent has failed to submit any evidence / document on record that the financial statements were signed by him only as the Director of the Companies and by the other signing director as the Managing Director of the Companies.

12. The Board further noted that there were no salary payments in the company Kuldeep Vanijyak Pvt. Ltd. as per the audited Financial Statements of the company for the F.Y. 2015-16. the Director’s Report for the company Kuldeep Vanijyak Pvt. Ltd. for the F.Y. 2015-16 specifically provided as under:

“Directors & Key Managerial Personnel

During the year, Mr. Sanjay Gopalal Mundra and Mr. Rajesh Kumar Chandak were the Directors of the Company. There was no appointment or resignation of directors or key managerial personnel during the year and the company does not have any key managerial person other than present directors.”

The Director’s Report for the company Highvalue Investments Pvt. Ltd. for the F.Y. 2015-16 specifically provided as under:

“Directors & Key Managerial Personnel

During the year, Mr. Rajesh Kumar Chandak, Mr. Ramanlal Chandak and Mrs. Rashmi Chandak were the Directors of the Company. There was no appointment or resignation of directors or key managerial personnel during the year and the company does not have any key managerial person other than present directors.”

Similar disclosures were there with respect to the Director’s Report ‘Sushwani Info Systems Pvt Ltd’ for the year ended on 31st March 2016. The Board further noted that there were no salary payments in the company Sushwani Info Systems Pvt Ltd’ as per the audited Financial Statements of the company for the F.Y. 2015-16.

Thus, the Board observed that the role of the Respondent in the aforesaid companies was clearly beyond that of the Director Simplicitor.

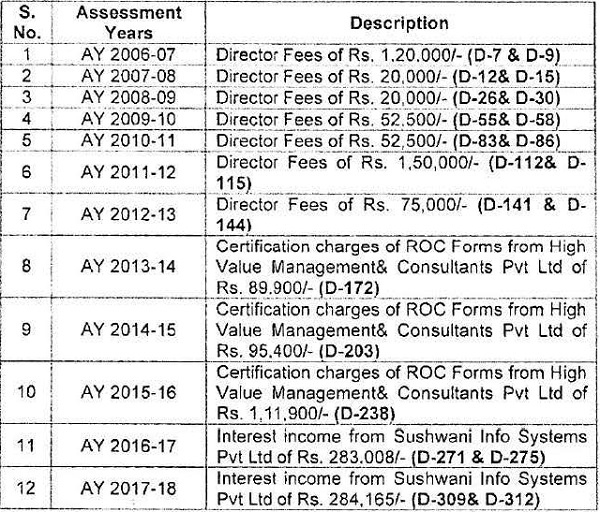

13. Further, from the copy of Income Tax returns submitted by the Respondent, it is noted that the Respondent had disclosed the various income / receipts in specific years in his ITRs, computation sheets and Income & Expenditure account annexed with ITRs which are mentioned as under:

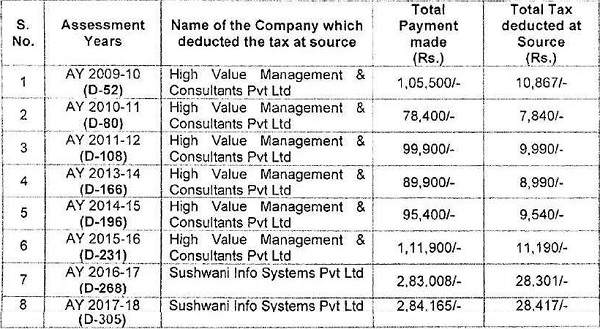

14. Further, from the copy of Form 26AS for the various financial / assessment years submitted by the Respondent, it is noted that the tax had been deducted at Source by the alleged Companies before making payment to the Respondent in different years. the details of which are mentioned as under:

15. Thus, from the copy of Income Tax Returns and Form 2GAS submitted by the Respondent, it is amply clear that the Respondent had received the director fees and other incomes from the Companies i.e. High Value Management & Consultants Pvt Ltd and Sushwani Info Systems Pvt Ltd.

16. The Board also perused the various provisions of the Articles of Association of those two companies in relation to the role and powers of the directors of the Companies. From the copy of Articles of Association of High Value Management & Consultants Pvt Ltd and Sushwani Info Systems Pvt Ltd, the Board noted that the Respondent was appointed as the first director of High Value Management & Consultants Pvt Ltd along with one other director in the Company. Further, the other relevant paragraphs of the Articles of Association of both Companies read as under:

“14. The Board of Directors may meet together for the despatch of the business or may adjourn or otherwise regulate their meeting in such manner as they think fair subject to the provisions of Section 285 of the companies Act, 1956. Each director may receive out of the funds of the Company the sitting fee for each and every meeting attended by him as may be decided by the Board and further sums as the Company in General Meeting may from time to time determine. The Directors will also receive out of the funds of the company such sum per month as remuneration as will be decided by the Board of Directors subject however, to the rectification of the members in the Annual General Meeting held immediately after such fixation or any change or any change in the amount of remuneration payable (emphasis added).

15. Subject to the provisions of the Act, the control of the Company shall be vested in the Board of Directors and the business of the company shall be managed by the Board of Directors who in addition to the powers of the authorities by these presents or otherwise expressly confirmed upon them, may be exercised or done by the company. The Board of Directors, if they like, may enter into a contract with any person or business expert to advise them in any or all matters on such terms and conditions and for such period as may be determined by the Board of Directors for the benefit of the Company (emphasis added).

16. The powers and responsibilities of the Directors of the Company shall he as in the Companies act, 1956 and the table ‘A’ thereof excepting so far as they stand modified by the provisions of the Articles.

17. The Director shall have the powers, jointly and severally, of engagement and dismissal of the staff and of general direction and of management and superintendence of the business of the company with full powers to do all acts, matters and things deemed necessary, proper and expedient for carrying on the business of the company with full powers to do all acts, matters and things deemed necessary, proper and expedient for carrying on the business of the company and to make and to draw, accept, endorse and negotiate on behalf of the company in General Meeting. All such powers of the directors shall be subject to Supervision and control of the Boards, which may entrust powers of specific nature to a particular director or employee of the company (emphasis added)

18.(a) To purchase or otherwise acquire for the company and property rights or privileges which the company as authority to acquire at such price and on such terms and conditions as they think fit and to sell let, lease, exchange or otherwise dispose of absolutely or conditionally any part of the property, privileges and undertaking of the company upon such terms and conditions and for such consideration as they may think fit (emphasis added).

(b) Subject to the provisions of the Act, to invest and deal with any money of the company, not immediately required for the purpose thereof upon such securities, shares (not being shares in thins company) deposits or loans in such manner as they think fit and from time to time vary or realise such investment (emphasis added)

19. The Board of Directors may from time to time raise or borrow any sums of money for and on behalf of the company from the members or other persons, companies or banks or they may themselves advance money to the company on such terms and conditions as may be approved by the Board of Directors (emphasis added).

20. The Board of Directors may from time to time secure the payment of such money in such manner and upon such terms and conditions in all respects as they think fit and in particular by issue of debentures or bonds of the Company or by mortgaging or charging of all or any part of the Company’s property and of the uncalled capital for the time being (emphasis added).

21. Subject to the provisions of the Companies Act, any debentures, bonds or other securities may be issued at discount, premium of otherwise and with special privileges as to the redemption surrender, drawing and otherwise as the Board thinks fit (emphasis added)

22. The Board shall cause proper books of accounts to be kept in accordance with section 209 of the Company Act, 1956.”

17. . From the above points in the Articles of Association of the aforesaid two Companies, it is amply clear that role and powers entrusted to the Respondent being the director of the Companies by the Articles of Association, was far away from the role of Director Simplicitor. The Respondent being the director of the Companies was entrusted with the various duties and powers relating to day to day affairs of the Companies.

18. As regards the plea that the Respondent is Director Simplicitor and only involved in annual compliances as per Companies Act, the Board observed as under:-

a. As per Companies Act, private limited companies are opened and operated by atleast two directors.

b. As per submissions of the Respondent, both the directors in the alleged private limited companies were non-executive Independent Directors and none amongst them were involved in the executive functions of those companies.

c. The concept of independent directors was evolved to regulate the public limited and listed companies as the stake of general public and stakeholders in those companies were generally at inherent risk. There is no such requirement for private limited companies.

The Board examined the Respondent in this respect that how the said companies were being run by non-executive directors when there is none who holds managerial position and also sought explanation/ clarifications with respect to employee details employed with such alleged companies, how the day to day operations were carried out, the exact details of operations of said companies and mode of execution of banking operations of said companies. However, the Board observed that the Respondent was unable to provide any justifiable clarifications/ explanations with respect to the same.

19. Considering the attendant circumstances, the evidence put forth during the proceedings and the submissions on record, the Board, viewed that it is conclusively proved that the role of the Respondent in the alleged companies clearly exceeded beyond that of the Director Simplicitor and he ought to have sought the prior permission of the Council before engaging himself in any business or occupation other than profession of Chartered Accountant. Accordingly, the Respondent is held Guilty in respect of the Charge alleged.

CONCLUSION:

20. The Board of Discipline, in view of the above, is of the considered view that the Respondent is Guilty of Professional Misconduct falling within the meaning of Item (11) of Part I of First Schedule to the Chartered Accountants Act 1949.

This is issued pursuant to the Order dated 29th April 2024 passed by Hon’ble High Court of Delhi in W.P.(C) 5247/2024 namely [CAI Vs R. Vinod Kumar & others.

Sd/-

CA. PRASANNA KUMAR D

(PRESIDING OFFICER)

Sd/-

MRS. RANI NAIR (IRS, RETD.)

(GOVERNMENT NOMINEE)

good decison for young professional acadmic