Exposure Draft of Standard on Auditing 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report

Introduction

Scope of this SA

1. This Standard on Auditing (SA) deals with additional communication in the auditor’s report when the auditor considers it necessary to:

(a) Draw users’ attention to a matter or matters presented or disclosed in the financial statements that are of such importance that they are fundamental to users’ understanding of the financial statements; or

(b) Draw users’ attention to any matter or matters other than those presented or disclosed in the financial statements that are relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report.

2. SA 7011 establishes requirements and provides guidance when the auditor determines key audit matters and communicates them in the auditor’s report. When the auditor includes a Key Audit Matters section in the auditor’s report, this SA addresses the relationship between key audit matters and any additional communication in the auditor’s report in accordance with this SA. (Ref: Para. A1– A3)

3. SA 570(Revised)2 and SA 720(Revised)3 establish requirements and provide guidance about communication in the auditor’s report relating to going concern and other information, respectively.

4. Appendices 1 and 2 identify SAs that contain specific requirements for the auditor to include Emphasis of Matter paragraphs or Other Matter paragraphs in the auditor’s In those circumstances, the requirements in this SA regarding the form of such paragraphs apply. (Ref: Para. A4)

Page Contents

- Effective Date

- Objective

- Definitions

- Requirements

- Emphasis of Matter Paragraphs in the Auditor’s Report

- Other Matter Paragraphs in the Auditor’s Report

- Communication with Those Charged with Governance

- Application and Other Explanatory Material

- The Relationship between Emphasis of Matter Paragraphs and Key Audit Matters in the Auditor’s Report (Ref: Para. 2, 8(b))

- Circumstances in Which an Emphasis of Matter Paragraph May Be Necessary (Ref: Para. 4, 8)

- Including an Emphasis of Matter Paragraph in the Auditor’s Report (Ref: Para. 9)

- Other Matter Paragraphs in the Auditor’s Report (Ref: Para. 10–11)

- Placement of Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Auditor’s Report (Ref: Para. 9, 11)

- Communication with Those Charged with Governance (Ref. Para. 12)

- List of SAs Containing Requirements for Emphasis of Matter Paragraphs

- List of SAs Containing Requirements for Other Matter Paragraphs

- Appendix 313

- Report on Other Legal and Regulatory Requirements18

- Report on Other Legal and Regulatory Requirements26

Effective Date

5. This SA is effective for audits of financial statements for periods beginning on or after …….

Objective

6. The objective of the auditor, having formed an opinion on the financial statements, is to draw users’ attention, when in the auditor’s judgment it is necessary to do so, by way of clear additional communication in the auditor’s report, to:

(a) A matter, although appropriately presented or disclosed in the financial statements, that is of such importance that it is fundamental to users’ understanding of the financial statements; or

(b) As appropriate, any other matter that is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report.

Definitions

7. For purposes of the SAs, the following terms have the meanings attributed below:

(a) Emphasis of Matter paragraph – A paragraph included in the auditor’s report that refers to a matter appropriately presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements.

(b) Other Matter paragraph – A paragraph included in the auditor’s report that refers to a matter other than those presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report.

Requirements

Emphasis of Matter Paragraphs in the Auditor’s Report

8. If the auditor considers it necessary to draw users’ attention to a matter presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements, the auditor shall include an Emphasis of Matter paragraph in the auditor’s report provided: (Ref: A5–A6)

(a) The auditor would not be required to modify the opinion in accordance with SA 705 (Revised)4 as a result of the matter; and

(b) When SA 701 applies, the matter has not been determined to be a key audit matter to be communicated in the auditor’s (Ref: Para. A1–A3)

9. When the auditor includes an Emphasis of Matter paragraph in the auditor’s report, the auditor shall:

(a) Include the paragraph within a separate section of the auditor’s report with an appropriate heading that includes the term “Emphasis of Matter”;

(b) Include in the paragraph a clear reference to the matter being emphasized and to where relevant disclosures that fully describe the matter can be found in the financial statements. The paragraph shall refer only to information presented or disclosed in the financial statements; and

(c) Indicate that the auditor’s opinion is not modified in respect of the matter (Ref: Para. A7–A8, A16–A17)

Other Matter Paragraphs in the Auditor’s Report

10. If the auditor considers it necessary to communicate a matter other than those that are presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report, the auditor shall include an Other Matter paragraph in the auditor’s report, provided:

(a) This is not prohibited by law or regulation; and

(b) When SA 701 applies, the matter has not been determined to be a key audit matter to be communicated in the auditor’s report. (Ref: Para. A9– A14)

11. When the auditor includes an Other Matter paragraph in the auditor’s report, the auditor shall include the paragraph within a separate section with the heading “Other Matter,” or other appropriate (Ref: Para. A15–A17)

Communication with Those Charged with Governance

12. If the auditor expects to include an Emphasis of Matter or an Other Matter paragraph in the auditor’s report, the auditor shall communicate with those charged with governance regarding this expectation and the wording of this (Ref: Para. A18)

***

Application and Other Explanatory Material

The Relationship between Emphasis of Matter Paragraphs and Key Audit Matters in the Auditor’s Report (Ref: Para. 2, 8(b))

A1. Key audit matters are defined in SA 701 as those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period. Key audit matters are selected from matters communicated with those charged with governance, which include significant findings from the audit of the financial statements of the current period.5 Communicating key audit matters provides additional information to intended users of the financial statements to assist them in understanding those matters that, in the auditor’s professional judgment, were of most significance in the audit and may also assist them in understanding the entity and areas of significant management judgment in the audited financial statements. When SA 701 applies, the use of Emphasis of Matter paragraphs is not a substitute for a description of individual key audit matters.

A2. Matters that are determined to be key audit matters in accordance with SA 701 may also be, in the auditor’s judgment, fundamental to users’ understanding of the financial statements. In such cases, in communicating the matter as a key audit matter in accordance with SA 701, the auditor may wish to highlight or draw further attention to its relative importance. The auditor may do so by presenting the matter more prominently than other matters in the Key Audit Matters section (e.g., as the first matter) or by including additional information in the description of the key audit matter to indicate the importance of the matter to users’ understanding of the financial statements.

A3. There may be a matter that is not determined to be a key audit matter in accordance with SA 701 (i.e., because it did not require significant auditor attention), but which, in the auditor’s judgment, is fundamental to users’ understanding of the financial statements (e.g., a subsequent event). If the auditor considers it necessary to draw users’ attention to such a matter, the matter is included in an Emphasis of Matter paragraph in the auditor’s report in accordance with this SA.

Circumstances in Which an Emphasis of Matter Paragraph May Be Necessary (Ref: Para. 4, 8)

A4. Appendix 1 identifies SAs that contain specific requirements for the auditor to include Emphasis of Matter paragraphs in the auditor’s report in certain circumstances. These circumstances include:

- When a financial reporting framework prescribed by law or regulation would be unacceptable but for the fact that it is prescribed by law or regulation.

- To alert users that the financial statements are prepared in accordance with a special purpose framework.

- When facts become known to the auditor after the date of the auditor’s report and the auditor provides a new or amended auditor’s report (i.e., subsequent events).6

A5. Examples of circumstances where the auditor may consider it necessary to include an Emphasis of Matter paragraph are:

- An uncertainty relating to the future outcome of exceptional litigation or regulatory action.

- A significant subsequent event that occurs between the date of the financial statements and the date of the auditor’s 7

- Early application (where permitted) of a new accounting standard that has a material effect on the financial statements.

- A major catastrophe that has had, or continues to have, a significant effect on the entity’s financial position.

A6. However, a widespread use of Emphasis of Matter paragraphs may diminish the effectiveness of the auditor’s communication about such matters.

Including an Emphasis of Matter Paragraph in the Auditor’s Report (Ref: Para. 9)

A7. The inclusion of an Emphasis of Matter paragraph in the auditor’s report does not affect the auditor’s opinion. An Emphasis of Matter paragraph is not a substitute for:

(a) A modified opinion in accordance with SA 705 (Revised) when required by the circumstances of a specific audit engagement;

(b) Disclosures in the financial statements that the applicable financial reporting framework requires management to make, or that are otherwise necessary to achieve fair presentation; or

(c) Reporting in accordance with SA 570 (Revised)8 when a material uncertainty exists relating to events or conditions that may cast significant doubt on an entity’s ability to continue as a going concern.

A8. Paragraphs A16–A17 provide further guidance on the placement of Emphasis of Matter paragraphs in particular circumstances.

Other Matter Paragraphs in the Auditor’s Report (Ref: Para. 10–11)

Circumstances in Which an Other Matter Paragraph May Be Necessary Relevant to Users’ Understanding of the Audit

A9. SA 260 (Revised) requires the auditor to communicate with those charged with governance about the planned scope and timing of the audit, which includes communication about the significant risks identified by the auditor.9 Although matters relating to significant risks may be determined to be key audit matters, other planning and scoping matters (e.g., the planned scope of the audit, or the application of materiality in the context of the audit) are unlikely to be key audit matters because of how key audit matters are defined in SA 701. However, law or regulation may require the auditor to communicate about planning and scoping matters in the auditor’s report, or the auditor may consider it necessary to communicate about such matters in an Other Matter paragraph.

A10. In the rare circumstance where the auditor is unable to withdraw from an engagement even though the possible effect of an inability to obtain sufficient appropriate audit evidence due to a limitation on the scope of the audit imposed by management is pervasive,10 the auditor may consider it necessary to include an Other Matter paragraph in the auditor’s report to explain why it is not possible for the auditor to withdraw from the engagement.

Relevant to Users’ Understanding of the Auditor’s Responsibilities or the Auditor’s Report

A11. Law, regulation or generally accepted practice may require or permit the auditor to elaborate on matters that provide further explanation of the auditor’s responsibilities in the audit of the financial statements or of the auditor’s report thereon. When the Other Matter section includes more than one matter that, in the auditor’s judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report, it may be helpful to use different sub-headings for each matter.

A12. An Other Matter paragraph does not deal with circumstances where the auditor has other reporting responsibilities that are in addition to the auditor’s responsibility under the SAs (see Other Reporting Responsibilities section in SA 700 (Revised)11), or where the auditor has been asked to perform and report on additional specified procedures, or to express an opinion on specific matters.

Reporting on more than one set of financial statements

A13. An entity may prepare one set of financial statements in accordance with a general purpose framework (e.g., the national framework) and another set of financial statements in accordance with another general purpose framework (e.g., International Financial Reporting Standards), and engage the auditor to report on both sets of financial statements. If the auditor has determined that the frameworks are acceptable in the respective circumstances, the auditor may include an Other Matter paragraph in the auditor’s report, referring to the fact that another set of financial statements has been prepared by the same entity in accordance with another general purpose framework and that the auditor has issued a report on those financial statements.

Restriction on distribution or use of the auditor’s report

A14. Financial statements prepared for a specific purpose may be prepared in accordance with a general purpose framework because the intended users have determined that such general purpose financial statements meet their financial information needs. Since the auditor’s report is intended for specific users, the auditor may consider it necessary in the circumstances to include an Other Matter paragraph, stating that the auditor’s report is intended solely for the intended users, and should not be distributed to or used by other parties.

Including an Other Matter Paragraph in the Auditor’s Report

A15. The content of an Other Matter paragraph reflects clearly that such other matter is not required to be presented and disclosed in the financial statements. An Other Matter paragraph does not include information that the auditor is prohibited from providing by law, regulation or other professional standards, for example, ethical standards relating to confidentiality of information. An Other Matter paragraph also does not include information that is required to be provided by management.

Placement of Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Auditor’s Report (Ref: Para. 9, 11)

A16. The placement of an Emphasis of Matter paragraph or Other Matter paragraph in the auditor’s report depends on the nature of the information to be communicated, and the auditor’s judgment as to the relative significance of such information to intended users compared to other elements required to be reported in accordance with SA 700 (Revised). For example:

Emphasis of Matter Paragraphs

- When the Emphasis of Matter paragraph relates to the applicable financial reporting framework, including circumstances where the auditor determines that the financial reporting framework prescribed by law or regulation would otherwise be unacceptable,12 the auditor may consider it necessary to place the paragraph immediately following the Basis for Opinion section to provide appropriate context to the auditor’s opinion.

- When a Key Audit Matters section is presented in the auditor’s report, an Emphasis of Matter paragraph may be presented either directly before or after the Key Audit Matters section, based on the auditor’s judgment as to the relative significance of the information included in the Emphasis of Matter paragraph. The auditor may also add further context to the heading “Emphasis of Matter”, such as “Emphasis of Matter – Subsequent Event”, to differentiate the Emphasis of Matter paragraph from the individual matters described in the Key Audit Matters section.

Other Matter Paragraphs

- When a Key Audit Matters section is presented in the auditor’s report and an Other Matter paragraph is also considered necessary, the auditor may add further context to the heading “Other Matter”, such as “Other Matter – Scope of the Audit”, to differentiate the Other Matter paragraph from the individual matters described in the Key Audit Matters section.

- When an Other Matter paragraph is included to draw users’ attention to a matter relating to Other Reporting Responsibilities addressed in the auditor’s report, the paragraph may be included in the Report on Other Legal and Regulatory Requirements section.

- When relevant to all the auditor’s responsibilities or users’ understanding of the auditor’s report, the Other Matter paragraph may be included as a separate section following the Report on the Audit of the Financial Statements and the Report on Other Legal and Regulatory Requirements.

A17. Appendix 3 is an illustration of the interaction between the Key Audit Matters section, an Emphasis of Matter paragraph and an Other Matter paragraph when all are presented in the auditor’s report. The illustrative report in Appendix 4 includes an Emphasis of Matter paragraph in an auditor’s report for an entity other than a listed entity that contains a qualified opinion and for which key audit matters have not been communicated.

Communication with Those Charged with Governance (Ref. Para. 12)

A18. The communication required by paragraph 12 enables those charged with governance to be made aware of the nature of any specific matters that the auditor intends to highlight in the auditor’s report, and provides them with an opportunity to obtain further clarification from the auditor where necessary. Where the inclusion of an Other Matter paragraph on a particular matter in the auditor’s report recurs on each successive engagement, the auditor may determine that it is unnecessary to repeat the communication on each engagement, unless otherwise required to do so by law or regulation.

Appendix 1

(Ref: Para. 4, A4)

List of SAs Containing Requirements for Emphasis of Matter Paragraphs

This appendix identifies paragraphs in other SAs that require the auditor to include an Emphasis of Matter paragraph in the auditor’s report in certain circumstances. The list is not a substitute for considering the requirements and related application and other explanatory material in SAs.

- SA 210, Agreeing the Terms of Audit Engagements – paragraph 19(b).

- SA 560, Subsequent Events – paragraphs 12(b) and 16.

- SA 800(Revised), Special Considerations—Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks – paragraph 14.

Appendix 2

(Ref: Para. 4)

List of SAs Containing Requirements for Other Matter Paragraphs

This appendix identifies paragraphs in other SAs that require the auditor to include an Other Matter paragraph in the auditor’s report in certain circumstances. The list is not a substitute for considering the requirements and related application and other explanatory material in SAs.

- SA 560, Subsequent Events – paragraphs 12(b) and 16.

- SA 710, Comparative Information—Corresponding Figures and Comparative Financial Statements – paragraphs 13–14, 16–17 and 19.

Appendix 313

(Ref: Para. A17)

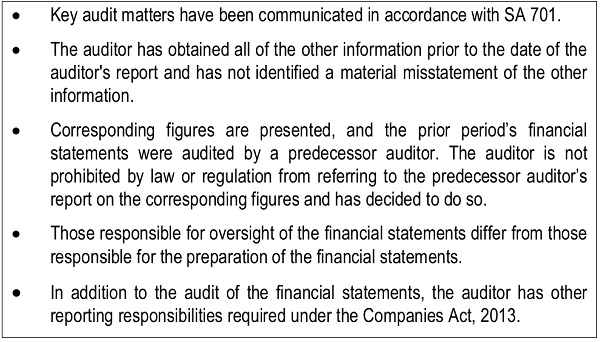

Illustration of an Auditor’s Report that Includes a Key Audit Matters Section, an Emphasis of Matter Paragraph, and an Other Matter Paragraph

–

INDEPENDENT AUDITOR’S REPORT

To the Members of ABC Company Limited

Report on the Audit of the Standalone Financial Statements

Opinion

We have audited the standalone financial statements of ABC Company Limited (“the Company”), which comprise the balance sheet as at March 31, 20X1, and the statement of Profit & Loss, (statement of changes in equity)14 and the statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (in which are included the Returns for the year ended on that date audited by the branch auditors of the Company’s branches located at (location of branches))15.

In our opinion, and to the best of our information and according to the explanations given to us the aforesaid financial statements, give the information required by the Companies Act, 2013 in the manner so required, and give a true and fair view, in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at March 31st, 20X1 and its profit/loss, (changes in equity16) and its cash flows for the year ended on that date.

Basis for Opinion

We conducted our audit in accordance with the Standards on Auditing (SAs) specified under Section 143(10) of the Companies Act, 2013. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the financial statements as per the ICAI’s Code of Ethics and the provisions of the Companies Act, 2013, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Emphasis of Matter17

We draw attention to Note X of the financial statements, which describes the effects of a fire in the Company’s production facilities. Our opinion is not modified in respect of this matter.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

[Description of each key audit matter in accordance with SA 701.]

Other Matter

The financial statements of ABC Company Limited for the year ended March 31, 20X0, were audited by another auditor who expressed an unmodified opinion on those statements on June 15, 20X0.

Other Information [or another title if appropriate such as “Information Other than the Financial Statements and Auditor’s Report Thereon”]

[Reporting in accordance with the reporting requirements in SA 720 (Revised) – see Illustration 1 in Appendix 2 of SA 720 (Revised).]

Responsibilities of Management and Those Charged with Governance for the Financial Statements

[Reporting in accordance with SA 700 (Revised) – see Illustration 1 in SA 700 (Revised).]

Auditor’s Responsibilities for the Audit of the Financial Statements

[Reporting in accordance with SA 700 (Revised) – see Illustration 1 in SA 700 (Revised).]

Report on Other Legal and Regulatory Requirements18

[Reporting in accordance with SA 700 (Revised) – see Illustration 1 in SA 700 (Revised).]

While reporting under Section 143(3) of the Companies Act, 2013, the auditor is required to suitably reword the wordings given in the Illustration in SA 700(Revised) to meet the circumstances of the audit.

For XYZ &

Co Chartered Accountants

(Firm’s Registration No.)

Signature

(Name of the Member signing the Auditor’s Report)

(Designation19)

(Membership No.)

UDIN

Place of Signature:

Date:

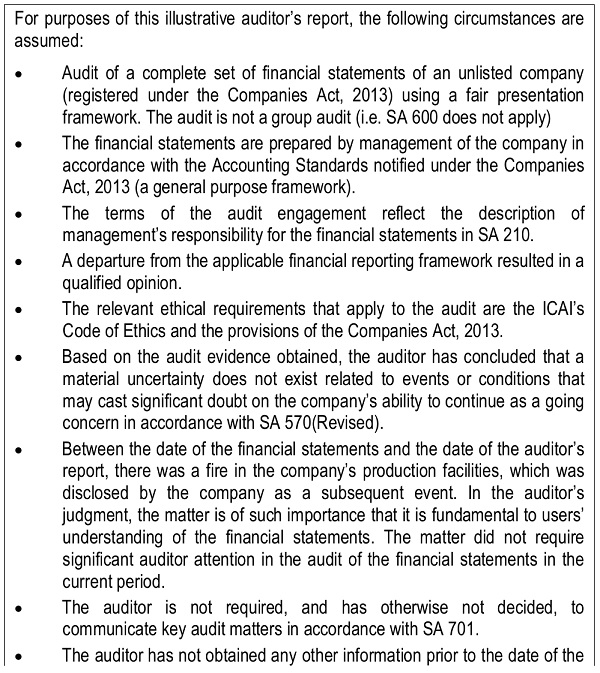

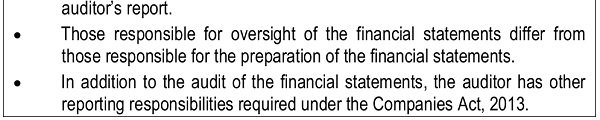

Appendix 420

(Ref: Para. A17)

Illustration of an Auditor’s Report Containing a Qualified Opinion Due to a Departure from the Applicable Financial Reporting Framework and that Includes an Emphasis of Matter Paragraph

–

INDEPENDENT AUDITOR’S REPORT

To the Members of ABC Company Limited

Report on the Audit of the Standalone Financial Statements

Qualified Opinion

We have audited the standalone financial statements of ABC Company Limited (“the Company”), which comprise the balance sheet as at March 31st, 20X1, and the statement of Profit and Loss, (statement of changes in equity)21 and the statement of cash flows22 for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (in which are included the Returns for the year ended on that date audited by the branch auditors of the Company’s branches located at (location of branches))23.

In our opinion and to the best of our information and according to the explanations given to us, except for the effects of the matter described in the Basis for Qualified Opinion section of our report, the aforesaid financial statements give the information required by the Companies Act, 2013 in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India of the state of affairs of the Company as at March 31st, 20X1 and its profit/loss, (changes in equity24) and its cash flows25 for the year ended on that date.

Basis for Qualified Opinion

The Company’s short-term marketable securities are carried in the balance sheet at Rs. xxx. Management has not marked these securities to market but has instead stated them at cost, which constitutes a departure from the Accounting Standards notified under the Companies Act, 2013. The Company’s records indicate that had management marked the marketable securities to market, the Company would have recognized an unrealized loss of Rs. xxx in the statement of profit and loss for the year. The carrying amount of the securities in the balance sheet would have been reduced by the same amount at March 31, 20X1, and income tax, net income and shareholders’ equity would have been reduced by Rs. xxx, Rs. xxx and Rs. xxx, respectively.

We conducted our audit in accordance with the Standards on Auditing (SAs) specified under Section 143(10) of the Companies Act 2013. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the financial statements as per the Code of Ethics issued by ICAI and under the provisions of the Companies Act, 2013, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the ICAI’s Code of Ethics. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified opinion.

Emphasis of Matter – Effects of a Fire

We draw attention to Note X of the financial statements, which describes the effects of a fire in the Company’s production facilities. Our opinion is not modified in respect of this matter.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

[Reporting in accordance with SA 700(Revised)–see Illustration 3 in SA 700(Revised).]

Auditor’s Responsibilities for the Audit of the Financial Statements

[Reporting in accordance with SA 700(Revised – see Illustration 3 in SA 700(Revised).]

Report on Other Legal and Regulatory Requirements26

[Reporting in accordance with SA 700 (Revised) – see Illustration 3 in SA 700 (Revised).]

While reporting under Section 143(3) of the Companies Act, 2013, the auditor is required to suitably reword the wordings given in the Illustration in SA 700(Revised) to meet the circumstances of the audit.

For XYZ &

Co Chartered Accountants

(Firm’s Registration No.)

Signature

(Name of the Member signing the Auditor’s Report)

(Designation27)

(Membership No.)

UDIN

Place of Signature:

Date:

Notes:

1 SA 701, Communicating Key Audit Matters in the Independent Auditor’s Report.

2 SA 570 (Revised), Going Concern.

3 SA 720 (Revised), The Auditor’s Responsibilities Relating to Other Information.

4 SA 705 (Revised), Modifications to the Opinion in the Independent Auditor’s Report.

5 SA 260 (Revised), Communication with Those Charged with Governance, paragraph 16.

6 SA 560, Subsequent Events, paragraphs 12(b) and 16.

7 SA 560, paragraph 6.

8 SA 570 (Revised), paragraphs 22–23.

9 SA 260 (Revised), paragraph 15.

10 See paragraph 13(b)(ii) of SA 705 (Revised) for a discussion of this circumstance.

11 SA 700(Revised), Forming an Opinion and Reporting on Financial Statements, paragraphs 43- 45.

12 For example, as required by SA 210, Agreeing the Terms of Audit Engagements, paragraph 19 and SA 800(Revised), Special Considerations—Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks, paragraph 14.

13 It may be noted that auditor’s report formats are illustrative in nature and necessary changes may be made as per the facts and circumstances of the audit for example due to changes in applicable financial reporting framework, applicable laws and regulations, pronouncements issued by ICAI.

14 Where applicable.

15 Where applicable.

16 Where applicable.

17 As noted in paragraph A16, an Emphasis of Matter paragraph may be presented either directly before or after the Key Audit Matters section based on the auditor’s judgment as to the relative significance of the information included in the Emphasis of Matter paragraph.

18 Auditor should also include, wherever applicable, reporting on Section 197(16) of the Companies Act 2013, reporting on Section 143(3)(f), Section 143(3)(h) of the Companies Act, 2013, reporting on new reporting requirements under Rule 11 of the Companies (Audit and Auditors) Rules, 2014 prescribed by the Companies (Audit and Auditors) Amendment Rules dated 24th March 2021 and other reporting requirements as may be prescribed from time to time under the provisions of the Companies Act, 2013 and Rules thereunder.

19 Partner or Proprietor, as the case may be

20 It may be noted that auditor’s report formats are illustrative in nature and necessary changes may be made as per the facts and circumstances of the audit for example due to changes in applicable financial reporting framework, applicable laws and regulations, pronouncements issued by ICAI.

21 Where applicable.

22 Where applicable.

23 Where applicable.

24 Where applicable.

25 Where applicable.

26 Auditor should also include, wherever applicable, reporting on Section 197(16) of the Companies Act 2013, reporting on Section 143(3)(f), Section 143(3)(h) of the Companies Act, 2013, reporting on new reporting requirements under Rule 11 of the Companies (Audit and Auditors) Rules, 2014 prescribed by the Companies (Audit and Auditors) Amendment Rules dated 24th March 2021 and other reporting requirements as may be prescribed from time to time under the provisions of the Companies Act, 2013 and Rules thereunder.

27 Partner or Proprietor, as the case may be.