Guidance Note For Forensic Accounting And Investigation Standard No. 110 On Nature Of Engagement outlines the manner in which the Professional obtains clarity on the nature and purpose of the Forensic Accounting and Investigation (FAI) engagement for the purpose of implementing the Standard.

Digital Accounting Assurance Board

The Institute of Chartered Accountants of India

1st June, 2023

GUIDANCE NOTE FOR FORENSIC ACCOUNTING AND INVESTIGATION STANDARD NO. 110 ON NATURE OF ENGAGEMENT

EXPOSURE DRAFT Approved by DAAB (On 1 June’23)

This Guidance Note provides technical clarifications and implementation guidance on how to prepare for and conduct work procedures on Forensic Accounting and Investigation Standard Number 110, on “Nature of Engagement,” issued by the Institute of Chartered Accountants of India (ICAI) and should be read in conjunction with all the Standards relevant to the topic. The contents of this Guidance Note are recommendatory in nature and do not represent the official position of the ICAI. The reader is advised to apply his best Professional judgement in the application of this Guidance Note considering the relevant context and prevailing circumstances.

Page Contents

1.0 Introduction

1.1 FAIS 110 on “Nature of Engagement” expects the Professional to understand the nature of an engagement. It presents three options:

(a) a Forensic Accounting engagement,

(b) an Investigation; or

(c) a Litigation Support engagement.

It also states how these three are distinct from an audit engagement, and this distinction is particularly important since these Standards would not apply in those engagements.

1.2 The Standard expects the Professional to understand the nature of the engagement by understanding the mandate received from the primary stakeholder. The requirements of the Standard are expected to be implemented through an understanding of the various unique features which define the requirements in the mandate. These unique features cover various elements like objective, approach, focus, required skill set and also the expected outcomes, etc.

2.0 Objectives

2.1 This Guidance Note (GN) outlines the manner in which the Professional obtains clarity on the nature and purpose of the Forensic Accounting and Investigation (FAI) engagement for the purpose of implementing the Standard.

2.1 The objective of the GN is to assist the Professional establish the nature of

the engagement by:

(a) Understanding the concepts which determine the nature of the

(b) Obtaining the engagement mandate, what it requires, as well as what the deliverables are.

(c) Defining the appropriate engagement scope and approach.

(d) Identifying if any specialised skills or resources would be required to execute the engagement.

2.2 The GN also provides examples and illustrations to help the Professional make a determination of the nature of the engagement.

3.0 Procedures

3.1 There are certain salient features of the engagement which make it either a Forensic Accounting engagement, or an Investigation or a Litigation Support engagement. The Professional uses these unique features to establish the nature of engagement. A snapshot of some of these indicative features can be summarised in the infographic presented below.

3.2 Indicative features of Forensic Accounting are presented here:

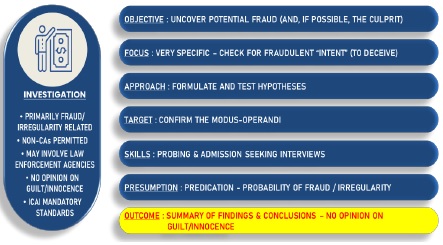

3.3 Indicative features of an Investigation are presented here:

3.4 For example, one of the features which defines the nature of the engagement is the “Objective” and if this objective is to gather evidence which may be admissible before a Competent Authority, then it may be a Forensic Accounting engagement. However, if the objective is to uncover a potential fraud, then it may be categorised as an Investigation.

3.5 The Professional can make a determination of the nature of the engagement by looking at the proposed mandate by the Primary Stakeholder (the party seeking Professional help and appointing the Professional).

(a) In most cases, the mandate does not specify any procedures which would immediately direct the Professional to decide the nature of In fact, the Primary Stakeholder may not know enough to help in this matter and would rely on the regular jargons like “Forensic Audit” or “Investigation” without even knowing enough about the distinction between the two.

(b) The mandate received from the Primary Stakeholders mostly define the purpose of the engagement, which eventually will define its This mandate will rightly define the expected outcome. For example, the Professional is informed that the management suspects that there is inventory pilferage from the plant and unpacked finished product is probably being stolen. The purpose in calling the Professional is to seek help to confirm or deny this suspicion. This therefore becomes the mandate, which in most cases would point towards a Forensic Accounting engagement.

3.6 The Professional may consider asking some of the following indicative questions while determining the nature of the engagement:

(a) Does the engagement require gathering of evidence regarding alleged legal, ethical or contractual violations?

(b) Will the findings be reported to a Competent Authority to make a legal or contractual determination?

(c) Does the engagement require provision of testimony or assistance to arbitration, mediation or other alternative dispute resolution mechanisms on financial or non-financial matters?

3.7 The proposal, and ultimately the engagement deliverable, may state that the engagement is not an audit engagement, and therefore generally accepted auditing standards may not apply in such a situation. This could

help manage the client’s expectations and avoid any subsequent

misunderstandings or disputes.

3.8 If the Professional determines that the engagement falls under FAIS, it would be appropriate to discuss this during communication with the client or Primary Stakeholders and even as part of the proposal finalisation process. Compliance with the Standards do introduce the need to follow certain processes and protocols to help achieve engagement objectives and ensure quality is maintained.

4.0 Explanations with Examples

4.1 Information about nature of the engagement may be forthcoming from various sources, or obtained through discussions and material provided by the client as follows (indicative list):

(a) Request for Proposal and Terms of Reference issued by client.

(b) High-level meetings and discussions with the stakeholders.

(c) Whistleblowing complaints.

(d) Board of Director/Management suspicions.

(e) Identified red flags in statutory, internal or other audit reports.

(f) Identified business fraud risks as per the entity’s Enterprise Risk Management (ERM) framework.

(g) Board of Director/Management decision to implement, monitor or strengthen anti-fraud measures.

4.2 The Professional may also gather information about nature of the engagement from other sources as follows (indicative list):

(a) Applicable laws and regulations (see FAIS 130 on “Laws and Regulations”).

(b) Written orders of a regulatory authority, enforcement authority, court of law, arbitral tribunal or any other legal or quasi legal authority directing the engagement.

(c) Expected enforcement action by third parties (financial institutions, business partners etc.), regulators, enforcement agencies etc.

(d) Progress and current status of legal or contractual disputes.

5.0 Annexures

5.1 Examples of some mandate scenarios which may be proposed by the primary stakeholder and form the basis of making a determination of the nature of the engagement and considered to be an AUDIT – hence FAIS may NOT apply.

| Sr. No. | Proposed Mandate | Classification of the Nature |

| 1 | Review of financial statements to ensure that they comply with accounting standards and regulations and to express an audit opinion. | Statutory Audit |

| 2 | Evaluation of internal controls and strengthen processes and mitigate risks. | Internal Audit |

| 3 | Audit of information systems and technology used by an organisation to ensure that they are secure, reliable, and meet regulatory requirements. | Information Systems Audit |

| 4 | Review of financial statements and records of a not- for-profit organisation to ensure that they comply with accounting standards and regulations specific to not-for-profit organisations. | Not-for-Profit Audit |

| 5 | Evaluation of the efficiency and effectiveness of an organisation’s operations and to identify opportunities for improvement. | Internal/Performance Audit |

| 6 | Review of organisation’s financial records to ensure that they comply with legal and regulatory requirements. | Compliance Audit |

| 7 | Audit under section 44AB of Income Tax Act, 1961 | Tax Audit |

| 8 | Review of an organisation’s compliance with grant requirements and regulations. | Grant Audit |

| 9 | Express an opinion on the true and fair view of financial statements for a particular fiscal year. | Statutory Audit |

5.2 Examples of some mandate scenarios which may be proposed by the Primary Stakeholder and form the basis of making a determination of the nature of the engagement and considered to be a FORENSIC ACCOUNTING engagement – hence FAIS would apply.

| Sr. No. | Proposed Mandate |

| 1 | Review of books of accounts for quantification of fraudulent transactions. |

| 2 | To assist an entity to estimate business interruption claims resulting from natural disasters, accidents, or other events causing a financial loss. |

| 3 | To estimate the loss of inventory in a warehouse fire or theft to estimate the loss of profits in an insurance claim. |

| 4 | To analyse the production records indicating high wastage to confirm or deny the possibility of inventory pilferage. |

5.3 Examples of some mandate scenarios which may be proposed by the primary stakeholder and form the basis of making a determination of the nature of the engagement and considered to be an INVESTIGATION engagement – hence FAIS would apply.

| Sr. No. | Proposed Mandate |

| 1 | To examine suspicions of irregularity or fraud in the purchase of a particular raw material and to corroborate these with some unusual activity on the part of some staff members in the purchase department. |

| 2 | An enquiry into allegations of Sexual Harassment against a fellow employee. |

| 3 | A review into certain whistle-blower complaints against the Procurement Head in the nature of:

1) Procurement of raw materials at inflated prices; and 2) Payments of kickback for increased share of business. |

| 4 | Borrower defaults on loans and engagement is to determine whether there is any misutilisation of funds. |

5.4 Examples of some mandate scenarios which may be proposed by the Primary Stakeholder and form the basis of making a determination of the nature of the engagement and considered to be LITIGATION SUPPORT engagement – hence FAIS would apply.

| Sr. No. | Proposed Mandate |

| 1 | Professional is asked by an investigative agency or a Competent Authority to provide evidence in support of the observations made in an audit report. |

| 2 | To analyse financial records and provide testimony in a lawsuit involving a breach of contract. The analysis will be used to calculate damages resulting from the breach of contract and to help the plaintiff negotiate a settlement. |

| 3 | To review a concern that profits have been impacted due to incorrect capitalisation. The Professional is appointed to testify as to whether the capitalisation is in accordance with the prescribed accounting standards and international best practices. |

| 4 | An engagement to value a closely held business in a dispute between shareholders. The analysis may be used in the settlement negotiations. |