During the week of June 2nd to 8th, 2025, several regulatory bodies issued significant notifications and circulars. The Income Tax Department formalized data sharing with Maharashtra for the ‘Mazi Ladki Bahin Yojana’ to identify eligible beneficiaries, and a Delhi High Court ruling allowed Section 54F exemption for different floors of a single residential house. In GST, advisories were issued regarding non-editable auto-populated GSTR-3B liabilities from July 2025, necessitating amendments via GSTR-1A, and a three-year time limit for filing GST returns was announced to be implemented from July 2025. Custom duties saw the imposition of anti-dumping duties on Insoluble Sulphur and Vitamin-A Palmitate from specified countries, alongside the removal of port restrictions and testing requirements for certain leather exports. SEBI updated investor charters for Research Analysts and Investment Advisers, streamlined margin obligations for client securities, extended compliance relaxations for Non-Convertible Debts, and issued a framework for ESG Debt Securities. The RBI reduced the policy repo rate, adjusted related rates, revised qualifying asset criteria for NBFC-MFIs, and issued comprehensive directions for lending against gold and silver collateral. Additionally, IBBI cancelled a valuer’s registration for suppressing criminal charges, and a Delhi High Court judgment affirmed that liquidated damages require proof of actual loss.

Notifications & Circulars issued during week (2nd – 8th June 2025)

A. Income Tax

Income Tax Dept to share data with Maharashtra for ‘Mazi Ladki Bahin Yojana’: The notification specifies ‘Secretary to the Government of Maharashtra, Women and Child Development’ for the purposes of sharing of information regarding Income-tax payers’ for identifying eligible beneficiaries under the Mukhyamantri Mazi Ladki Bahin Yojana. Section 138(1)(a)(ii) allows the CBDT or other specified income tax authorities to furnish information received or obtained by them in the performance of their duties under the Income-tax Act. Such information can be shared with an officer, authority, or body performing functions under any other law, provided the Central Government specifies the entity via an official notification.

(Link: Income Tax Notification 54/2025 Dated 03/06/2025)

CBDT Facilitates Income Tax Data Sharing for Maharashtra Scheme: The CBDT order designate the Director General of Income-tax (Systems), New Delhi, as the authority to share information with the Secretary to the Government of Maharashtra, Women and Child Development. This information exchange pertains to identifying eligible beneficiaries for the “Mukhyamantri Mazi Ladki Bahin Yojana” by checking income tax payer status.

(Link: Income Tax CBDT Order Dated 06/06/2025)

HC, Section 54F exemption granted for different floors of single residential house: Case of PCIT vs Lata Goel, HC Delhi Judgement Dated 30th April 2025. High Court held that exemption under section 54F of the Income Tax Act is allowed towards different floors of a house considering it as single residential house. Accordingly, appeal of the revenue dismissed.

Advisory regarding non-editable of auto-populated liability in GSTR-3B: GST Portal provides a pre-filled GSTR-3B, where the tax liability gets auto-populated based on the outward supplies declared in GSTR-1/ GSTR-1A/ IFF. As of now taxpayers can edit such auto populated values in form GSTR 3B itself.

— With introduction of form GSTR 1A, taxpayer now has a facility to amend their incorrectly declared outward supplies in GSTR-1/IFF through GSTR-1A, allowing them an opportunity to correct their liabilities before filing their GSTR-3B in the same return period. In view of the same, from July 2025 tax period, such auto populated liability will become non editable and taxpayers will be allowed to amend their auto populated liability by making amendments through form GSTR 1A.

(Link: GSTN Advisory Dated 07/06/2025)

Advisory, Barring of GST Return on expiry of three years: As per the provisions, the taxpayers shall not be allowed file their GST returns after the expiry of a period of three years from the due date of furnishing the said return under Section 37 ( Outward Supply), Section 39 (payment of liability), Section 44 ( Annual Return) and Section 52 (Tax Collected at Source). These Sections cover GSTR-1, GSTR 3B, GSTR-4, GSTR-5, GSTR-5A, GSTR-6, GSTR 7, GSTR 8 and GSTR 9. The said restriction will be implemented on the GST portal from July 2025 Tax period. Hence, the taxpayers are once again advised to reconcile their records and file their GST Returns as soon as possible if not filed till now.

(Link: GSTN Advisory Dated 07/06/2025)

HC, Sets aside GST refund rejection under Budgetary Support Scheme: Case of Shiva Industries vs Union of India, HC J&K Judgement Dated 4th April 2025. HC ruled in favour of petitioner and directed to release the full amount of budgetary support claimed by the company. The court found that the partial rejection of refund claims by the respondent was contrary to the clear provisions of the Government of India’s notification dated 5th October 2017, concerning budgetary support under GST provisions.

HC, Awaits SC verdict on GST deadline challenge: Case of Engineers India Limited vs Union of India, HC Delhi Judgement Dated 23rd April 2025. HC decided to defer its judgment on a petition challenging an adjudication order and specific GST notifications that extended tax- related deadlines. The court decision is contingent upon a forthcoming ruling by the Supreme Court, which is currently examining the validity of similar notifications due to a divergence of opinions among various High Courts across the country. The central point of contention revolves around the procedural requirement for issuing such extensions. Section 168A of the GST Act mandates a prior recommendation from the GST Council before any deadlines can be extended.

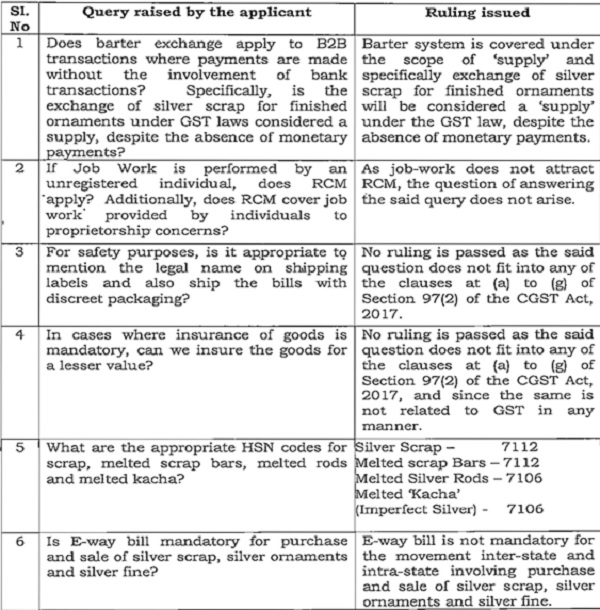

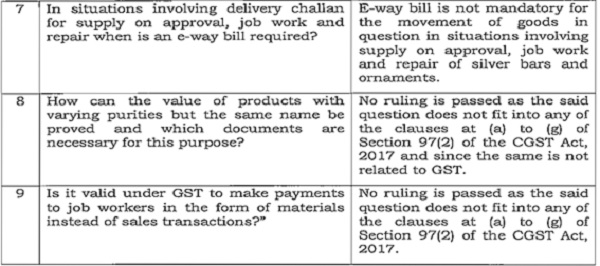

AAR, Silver trade, ruling on Barter, RCM & E-Way Bill: Case of Paaragiri Balaraman Nagarajeshwaran, AAR Tamil Nadu Ruling Dated 9th May 2025.

–

C. Central Excise

No Notifications/ Circular during the week.

D. Custom Duty

Anti-dumping Duty on Insoluble Sulphur originating in or exported from China and Japan: Anti-dumping Duty has been imposed on imports of Insoluble Sulphur originating in or exported from China and Japan and imported into India. The anti-dumping duty shall be effective for a period of five years.

(Link: Custom Notification 13/2025 (ADD) Dated 06/06/2025)

Anti-dumping Duty on Vitamin-A Palmitate originating in or exported from China, European Union and Switzerland: Anti-dumping Duty has been imposed on imports of Vitamin-A Palmitate originating in or exported from China, European Union and Switzerland, and imported into India. The anti-dumping duty shall be effective for a period of five years.

(Link: Custom Notification 14/2025 (ADD) Dated 06/06/2025)

Removal of Port Restrictions and Testing Requirements for Export of Finished Leather, Wet Blue Leather, El Tanned Leather and Crust Leather: DGFT has removed the port restriction and testing requirement for Export of Finished Leather, Wet Blue Leather, El Tanned Leather and Crust Leather. Thus the following export conditions stands revoked i.e. Port restrictions and Requirement for Testing and certification by Central Leather Research Institute (CLRI) for Finished Leather, Wet Blue Leather, Crust Leather and El tanned leather. The officers under your jurisdiction be sensitized regarding the said matter.

(Link: Custom Instructions 13/2025 Dated 02/06/2025)

Implementation of Agreement signed between FSSAI, Ministry of Health and Family Welfare, Government of India and Bhutan Food and Drug Authority (BFDA): FSSAI has shared the updated list of 117 approved establishment of Bhutan with scope of approval. It may be noted that there is no change in the format of the Health Certificate or in the list of authorized signatories previously communicated. All other compliance requirements remain unchanged. The officers under your jurisdiction be sensitized regarding the said matter.

(Link: Custom Instructions 14/2025 Dated 02/06/2025)

E. Directorate General of Foreign Trade (DGFT)

Import of Yellow Peas Free without MIP & port restriction till March 2026: The notification has extended the import policy for yellow peas (ITC HS Code 07131010) until March 31, 2026, thus continuing the “Free” import status for yellow peas, and imports are allowed without Minimum Import Price (MIP) conditions or port restrictions.

(Link: DGFT Notification 16/2025 Dated 31/05/2025)

F. Securities and Exchange Board of India (SEBI)

Investor Charter for Research Analysts (RAs) updated: The updated charter outlines the vision and mission for investors, detailing the business transactions and services provided by (RAs). It mandates RAs to offer independent, unbiased research reports with transparent disclosure of financial interests and conflicts. RAs are also required to conduct annual audits, adhere to advertisement codes, maintain records of client interactions, and respect client data privacy. It specifies a grievance redressal mechanism, allowing investors to complain directly to the RA, via SCORES 2.0, or through the RA Administration and Supervisory Body (RAASB), with an option for online conciliation or arbitration if dissatisfaction persists.

(Link: SEBI Circular Dated 02/06/2025)

Investor Charter for Investment Advisers (IAs) updated: The updated Investor Charter outlines IAs responsibilities, including unbiased risk profiling, annual audits, and clear disclosures on fees, conflicts of interest, and the use of AI tools. It details investor rights, such as privacy, fair treatment, and access to suitable financial products. For grievance redressal, investors can now approach the IA directly (21-day resolution), use SCORES 2.0 for a two-level review (IAASB and SEBI), email the IAASB, or utilize the SMARTODR platform for online conciliation/arbitration. Additionally, IAs must prominently display the charter on their websites and mobile apps, provide it during client onboarding, and monthly disclose complaint data.

(Link: SEBI Circular Dated 02/06/2025)

Margin obligations to be given by way of Pledge/Re-pledge in the Depository System: SEBI has issued a circular to streamline the process of handling client securities pledged as margin by brokers. Previously, the brokers were required to accept collateral from clients only through margin pledges. However, issues arose with unsold invoked shares accumulating in brokers’ demat accounts, and operational difficulties occurred when clients sold pledged securities. To address these concerns, while protecting investor interests, SEBI has automated the invocation and sale process.

— New provisions allow for a single instruction, “Pledge release for early pay in,” when clients sell pledged securities, enabling immediate pledge release and early pay- in blocking. For invoked margin-pledged securities, including funded stock, they will be blocked for early pay-in in the client’s demat account, with a trail maintained in the broker’s margin pledge account. For invoked mutual fund units not traded on exchanges, a single “invocation cum redemption” functionality will be provided. If a client’s trading account is frozen, invoked securities will go to the broker’s demat account for sale under their proprietary code, with a mandate for same-day pay-in to prevent accumulation.

(Link: SEBI Circular Dated 03/06/2025)

Relaxation from compliance for Non-Convertible Debts with certain provisions of LODR Regulations: Previously, the regulation 58(1)(b) of LODR Regulations, mandated sending physical copies of financial statements and related documents to holders of non-convertible securities who had not registered their email addresses. MCA had extended relaxations till 5th June 2025, for sending physical copies of financial statements to shareholders, now extended till 30th September 2025. The issuers who did not send hard copies of these documents will not face penalties. However, the entities must disclose a web-link to the statement containing the salient features of all documents, as specified in Section 136 of the Companies Act, within their advertisement as per regulation 52(8) of the LODR Regulations.

(Link: SEBI Circular Dated 05/06/2025)

Framework for Environment, Social and Governance (ESG) Debt Securities: The circular provides a framework for the issuance and listing of Environment, Social, and Governance (ESG) debt securities (excluding green debt securities). This includes social bonds, sustainability bonds, and sustainability-linked bonds. The framework mandates that funds raised be used for projects aligned with internationally recognized standards such as the ICMA Principles, Climate Bonds Standard, ASEAN Standards, or EU Standards. Issuers must also comply with SEBI’s NCS and LODR Regulations. For sustainability-linked bonds, target setting must rely on a combination of benchmarking approaches including historical issuer performance (with a recommended minimum of 3 years of data), comparison with industry peers or sectoral standards, and alignment with science-based targets like the Paris Agreement or Sustainable Development Goals.

(Link: SEBI Circular Dated 06/06/2025)

Extension of timeline of additional liquidation period for VCFs migrating to AIF Regulations: The circular extends the additional liquidation period granted to VCFs that are in the process of migrating to the SEBI (Alternative Investment Funds) Regulations, 2012. A prior SEBI circular, dated 19th August 2024, established the framework for such migration, particularly for VCF schemes that had not yet been wound up post their original liquidation period. That circular had initially provided an additional liquidation period until 19th July 2025, now extended to 19th July 2026.

(Link: SEBI Circular Dated 06/06/2025)

Amendments to SEBI Alternative Investment Funds Regulations: As per the amended regulation 17, Category II AIFs are now permitted to invest in investee companies or in the units of Category I or other Category II AIFs, as long as these investments are disclosed in their Placement Memorandum. The explanation further clarifies that Category II AIFs are expected to invest primarily in unlisted securities and/or listed debt securities with a credit rating of ‘A’ or below from a SEBI-registered credit rating agency. This can be done either directly or through investments in units of other Alternative Investment Funds, in a manner specified by SEBI.

(Link: SEBI Notification Dated 21/05/2025)

SEBI warns against Fake Notices and Communications: SEBI has issued a public caution regarding fraudulent communications falsely claiming to be from SEBI. These messages, sometimes shared through social media, use forged SEBI letterheads, logos, and seals to mislead individuals. Incidents include fake notices demanding fines to avoid alleged SEBI action, counterfeit sale certificates of PACL properties, and fabricated certificates authorizing the use of third- party vendor accounts.

— SEBI advises the public to verify the authenticity of such communications using the SEBI website. All official SEBI communications, including notices and summons, contain a unique Document Identification Number (UDIN) that can be authenticated under the “Authenticate Document Number Issued by SEBI” section. SEBI urges the public and investors to remain vigilant, verify any suspicious communication through its official channels, and refrain from responding to fraudulent demands for payments or information.

(Link: SEBI Press Release Dated 04/06/2025)

G. Ministry of Corporate Affairs (MCA)

No Notifications/ Circulars during the week.

H. Insolvency and Bankruptcy Board of India (IBBI)

IBBI Cancels Valuer Registration for suppressing pending criminal charges: IBBI has cancelled the registration of Mr. Shreegopal Govindram Mundhra as a valuer for the asset class of Land and Building, following a complaint that he had suppressed information regarding a chargesheet filed against him in the CBI Special Court in 2013. The charges included serious offenses under the Indian Penal Code and the Prevention of Corruption Act, which were pending at the time of his application for valuer registration. The IBBI determined that Mr. Mundhra intentionally concealed material information, violating rules pertaining to eligibility, conditions of registration, and the code of conduct for registered valuers.

IBBI not obligated for Non-Disclosure of Chairperson visitor information under RTI: The appellant had sought the procedure to secure an appointment with the IBBI Chairperson and details of appointments given to others. The CPIO provided a phone number, which was incorrect, and stated that appointment details were unavailable. The First Appellate Authority noted the incorrect phone number and advised the CPIO to be more careful, while also affirming that the IBBI is not obligated to create information not already held, and that personal appointment details are exempt under Section 8(1)(j) of the RTI Act.

(Link: IBBI FAA Order Dated 02/06/2025)

I. Reserve Bank of India (RBI)

Liquidity Adjustment Facility- Change in rates: It has been decided by the Monetary Policy Committee (MPC) to reduce the policy repo rate under the Liquidity Adjustment Facility (LAF) by 50 basis points from 6.00 per cent to 5.50 per cent with immediate effect. Consequently, the standing deposit facility (SDF) rate and marginal standing facility (MSF) rate stand adjusted to 5.25 per cent and 5.75 per cent respectively, with immediate effect.

(Link: RBI Notification 42/2025 Dated 06/06/2025)

Standing Liquidity Facility for Primary Dealers: The Standing Liquidity Facility provided to Primary Dealers (PDs) (collateralised liquidity support) from the Reserve Bank would be available at the revised repo rate of 5.50 per cent with immediate effect.

(Link: RBI Notification 43/2025 Dated 06/06/2025)

Review of Qualifying Assets Criteria: Paragraph 8.1 of the Master Direction on Regulatory Framework for Microfinance Loans prescribes Qualifying Assets Criteria for Non-Banking Financial Companies- Microfinance Institutions. It has been decided to revise the qualifying asset criteria. The definition of ‘qualifying assets’ of NBFC-MFIs has been aligned with the definition of ‘microfinance loans’ given at paragraph 3 above. Qualifying assets of NBFC-MFIs shall constitute a minimum of 60 percent of the total assets (netted off by intangible assets), on an ongoing basis. If an NBFC-MFI fails to maintain the qualifying assets as aforesaid for four consecutive quarters, it shall approach the Reserve Bank with a remediation plan for taking a view in the matter.

(Link: RBI Notification 44/2025 Dated 06/06/2025)

Penal Interest on shortfall in CRR and SLR requirements- Change in Bank Rate: All penal interest rates on shortfall in CRR and SLR requirements, which are specifically linked to the Bank Rate, stands revised. The existing rates (depending on duration of shortfall) Bank Rate plus 3.0 percentage points (9.25 per cent) or Bank Rate plus 5.0 percentage points (11.25 per cent) are revised to Bank Rate plus 3.0 percentage points (8.75 per cent) or Bank Rate plus 5.0 percentage points (10.75 per cent).

(Link: RBI Notification 45/2025 Dated 06/06/2025)

Maintenance of Cash Reserve Ratio (CRR): It has been decided to reduce the Cash Reserve Ratio (CRR) of all banks by 100 basis points in four equal tranches of 25 basis points each to 3.0 per cent of net demand and time Liabilities (NDTL). Accordingly, banks are required to maintain the CRR at 3.75 per cent, 3.5 per cent, 3.25 per cent and 3.0 per cent of their NDTL effective from the reporting fortnight beginning September 6, October 4, November 1 and November 29, 2025, respectively.

(Link: RBI Notification 46/2025 Dated 06/06/2025)

RBI Lending Against Gold and Silver Collateral Directions, 2025: RBI has issued comprehensive directions for lending against gold and silver collateral, to establish a harmonized regulatory framework across all regulated entities (REs) such as commercial banks, co- operative banks, and NBFCs. The key provisions include detailed credit assessment for loans above Rs 2.5 lakh, guidelines for loan renewals and top-ups, and strict restrictions on lending against primary gold/silver or re-pledging collateral. The policy outlines maximum loan- to-value (LTV) ratios, varying from 85% for loans up to Rs 2.5 lakh to 75% for loans exceeding Rs 5 lakh, which must be maintained throughout the loan tenor. Other important aspects covered are the standardization of assaying and valuation procedures, transparency in auction processes, and compensation mechanisms for borrowers in cases of collateral loss or damage.

(Link: RBI Notification 47/2025 Dated 06/06/2025)

RBI Amends Government Securities STRIPS Regulations: The guidelines for Separate Trading of Registered Interest and Principal of Securities (STRIPS) of government securities has been amended. The key changes include the substitution of ‘PDO-NDS (Negotiated Dealing System)’ with ‘RBI Core Banking Solution (e-Kuber System)’ in section II, clause (1) for operational purposes. Now, all fixed coupon securities issued by the Government of India are eligible, regardless of maturity year. For State Government/Union Territory fixed coupon securities, eligibility is granted if they have a residual maturity of up to 14 years and a minimum outstanding value of ₹1,000 crore on the day of stripping. A condition for all eligible government securities is that they must qualify as eligible investments for Statutory Liquidity Ratio (SLR) and be transferable.

(Link: RBI Notification Dated 29/05/2025)

J. Miscellaneous

HC, Mere occurrence of breach doesn’t entitle claim for Liquidated Damages, Actual loss to be proved: Case of J&K Economic Reconstruction Agency vs Simples Projects Limited, HC Delhi Judgement dated 19th May 2025. High Court held that the Liquidated Damages clause does not entitle a party to claim the whole Liquidated Damages sum automatically upon the occurrence of breach. Liquidated Damages can be claimed subject to proving the actual loss suffered. The court observed that it may be noted that as per law of damages evolved by courts in India, unlike UK, the Indian law does not recognise penalties as a measure of damages. The courts have therefore held that LD stipulated in contracts must not be in the nature of penalty but must be in the nature of a genuine pre- estimate of damages made by the parties.

(Link: HC Delhi Judgement Dated 19/05/2025)

*****

Compiled by CMA Yash Paul Bhola, MBA, FCMA, and former Director (Finance) of National Fertilizers Limited.

Disclaimer: The contents of this article are for informational purposes only. The user may refer to the relevant notification/ circular/ decisions issued by the respective authorities for specific interpretation and compliances related to a particular subject matter)