Extension of due dates under Income Tax, GST & FTP

Recently Central Government has issued Income Tax Notification No. 35/2020 and Notification No. 48/2020-Central Tax to Notification No. 54/2020-Central Tax on 24th June 2020 which relates to extension of Due dates under GST, Law, Income Tax Law and other Laws. In Addition to that Government has enhanced due dates related to FTP-2015-20 vide various notifications issued from time to time. Article analyses all such extension of due dates in recent past-

Page Contents

- Income Tax Due Dates Extension

- GST Due Date Extensions

- N 51 & 52/2020-CT dated 24th June 2020 Relief from Interest & Penalty for Late furnishing of GSTR 3B

- N 52/2020-CT dated 24th June 2020 One Time from Late Fees for non furnishing of GSTR 3B

- N 54/2020-CT dated 24th June 2020 Last Date of GSTR 3B for August 2020 Extended

- N 53/2020-CT dated 24th June 2020 Relief from Late Fees for non furnishing of GSTR 1

- Real Estate Developers paying Differential Tax Inst 3/2/2020

- N No 50/2020 – CT dated 24th June 2020 Sec 10(2A) read with Rule 7

- Extensions in FTP

Income Tax Due Dates Extension

| Section | Compliance | Fresh Due Date |

| 139 | Last Date for Original & Revised IT

Return for FY 18-19 Comments – – However the Fees u/s 234F For belated return will apply\ – Interest u/s 234 A, B & C shall apply subject to below |

31st July 2020 |

| 139 | ITR for FY 2019-20

Comments – – It applies to all whether Original due date is 31st July or 31st October – Int u/s 234B & C shall be levied in all cases – Int u/s 234A shall apply subject to below – No penalty or fees upto reised due date |

30th November 2020 |

| Any

|

Last date of furnishing audit report for FY 2019-20

Comments – – For FY 18-19, the penalty u/s 271B @0.5% of Turnover or Rs.1.5 Lakhs whichever is higher, shall apply – For FY 19-20, no penalty |

31st October 2020 |

| 234A | Date for payment of self-assessment tax in the case of a taxpayer whose self-assessment tax liability is upto Rs. 1 lakh for FY 2019-20.

Comment – Say Tax Liability for FY 19-20 is Rs.1.1 Lakhs and out of which TDS Credit/Adv Tax/Other relief is Rs.0.2L. In this case the said extension APPLIES as the present liability is less than Rs.1 Lakh. However, one has to assesses the due amt. and pay the differential Advance Tax by the Original due date of Return. |

30th November 2020 |

| 200 & 206C | Last Date of furnishing of TDS/TCS returns for Q4 of 2019-20 or Feb’20 & Mar’20 | 31st July 2020 |

| 203

|

Last date of issuing TDS certificates for FY 19-20 | 15th August 2020 |

| No Extension of Due date of payment of TDS for June 2020. It still remains 7th July 2020 | ||

| Interest on Delayed payment of TDS, TCS, Advance Tax and FA | 9% upto 30th June 2020

12%/18% thereafter |

|

| 54/ 54GB | For making investment/ construction/ purchase for claiming roll over benefit/ deduction in respect of capital gains under sections 54 or 54GB of the IT Act | 30th September, 2020 |

| 10AA | Date for commencement of operation for the SEZ units for claiming deduction under section 10AA of the IT Act has also been further extended for the units which received necessary approval by 31st March, 2020. | 30th September, 2020 |

| Date for passing of order or issuance of notice by the authorities and various compliances under various Direct Taxes & Benami Law which are required to be passed/ issued/ made by 31st December, 2020 has been extended | 31st March, 2021 | |

| Date for linking of Aadhaar with PAN | 31st March, 2021 | |

| Vivaad Se Vishwas Scheme – Declaration, Passing of Order, etc | 31st Dec 2020 | |

| 10(23C)/12AA/ 35/80G | New procedure for Approval/ Registration | 30th September 2020 |

| Chp. VIA | Last date for investments under Chapter VI-A i.e. 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) etc. for the FY 2019-20 | 31st July 2020 |

GST Due Date Extensions

N 51 & 52/2020-CT dated 24th June 2020 Relief from Interest & Penalty for Late furnishing of GSTR 3B

| Period of Return | Dealers | interest | Late Fee | Condition/ Eg |

| Feb 2020 to April 2020 | Having PAN India turnover above ₹ 5 Crore | – Lower rate of interest of NIL for first 15 days after the due date of filing return in FORM GSTR-3B

– @ 9% thereafter till 24th June 2020 – 18% thereafter |

NIL – till 24th June 2020

Rs.100 per day (CT) – from initial Date if the above dates are violated |

E.g. GSTR 3B for Feb 2020, Int is as follows –

1. Till 4th April –NIL 2. 5th Apr – 24th Jun – 9% 3. From 25th Jun 18% |

| Feb 2020 to April 2020 | Having PAN India turnover of ₹ 0 – ₹ 5 Crore

(For Simplicity Conservative dates have been taken for all states) |

NIL – Till 30th June

2020 (For Feb 2020 3B) – Till 3rd July 2020 (For Mar’20 3B) – Till 6th July 2020 (For Apr’20 3B) 9% – From above dates till 30th Sep 2020 |

NIL – Till 30th June 2020 (For Feb 2020 3B)

Till 3rd July 2020 (For Mar’20 3B) Till 6th July 2020 (For Apr’20 3B) Rs.100 per day (CT) – from initial Date if the above dates are violated |

E.g. GSTR 3B for Feb 2020, Interest is as follows –

1. Till 3rd July – NIL 2. 3rd July – 30th Sep – 9% 3. From 1st Oct – 18% |

| May 2020 to July 2020 | Having PAN India turnover of ₹ 0 – ₹ 5 Crore

(For Simplicity Conservative dates have been taken for all states) |

NIL – Till 12th Sep 2020 (For May’20 3B)

– Till 23rd Sep 2020 (For Jun’20 3B) – Till 27th Sep 2020 (For Jul’20 3B) 9% – From above dates till 30th Sep 2020 |

NIL – Till 12th Sep 2020 (For May’20 3B)

– Till 23rd Sep 2020 (For Jun’20 3B) – Till 27th Sep 2020 (For Jul’20 3B) Rs.100 per day (CT) – from initial Date if the above dates are violated |

E.g. GSTR 3B for May 2020, Interest is as follows –

1. Till 12th Sep – NIL 2. 13th Sep – 30th Sep – 9% 3. From 1st Oct – 18% |

N 52/2020-CT dated 24th June 2020 One Time from Late Fees for non furnishing of GSTR 3B

| Taxpayer Category | Late Fee | Condition/ Eg |

| GSTR 3B Not Filed between July, 2017 to January, 2020 – With SOME Central Tax Payable | Rs.250/ – CT per month | The return should be filed between July, 2020 to September, 2020 |

| GSTR 3B Not Filed between July, 2017 to January, 2020 – With NO Central Tax Payable | NIL |

N 54/2020-CT dated 24th June 2020 Last Date of GSTR 3B for August 2020 Extended

| Period of Return | Dealers | Last Date | Late Fee & Interest |

| August 2020 | Having PAN India turnover of ₹ 0 – ₹ 5 Crore | 1st October 2020 for Some States &

3rd October 2020 for Some States |

NIL |

N 53/2020-CT dated 24th June 2020 Relief from Late Fees for non furnishing of GSTR 1

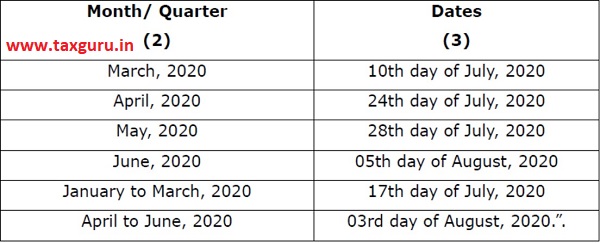

Due Dates of GSTR 1 for All Taxpayers WITHOUT LATE FEES

Real Estate Developers paying Differential Tax Inst 3/2/2020

Use Form DRC-03 for making the payment of tax by promoter/developer required to pay tax in accordance with the N no. 11/2017- CT (R) & N no. 3/2019- CT (R) ) on the shortfall from threshold requirement of procuring input and input services (below 80%) from registered person

N No 50/2020 – CT dated 24th June 2020 Sec 10(2A) read with Rule 7

From 1st April 2020, even Service Providers within a Turnover of Rs.50 Lakhs and as per conditions u/s 10(2A) read wit Rule 7 may opt for Composition Scheme and pay Tax @6%

Extensions in FTP

Extentions

– Duty Credit Scrips issued between 01.03.2018 and 30.06.2018 shall be valid till 30.09.2020

– AEO License expiring between 1st March & 31st May 2020 – Till 30th June 2020

– In MEIS applications which attracted a late cut as on 01.03.2020, the period between 01.03.2020 and 30.06.2020 shall not be counted and the last date for submission of various categories of applications attracting that late cut and the applicable cuts will be accordingly suitable re-determined.

– For SEIS applications

a. For the services rendered in FY 2016-17, the last date of application with 10% late cut would be 30.06.2020 and after that date it would become time barred.

b. For the services rendered in the FY 2017-18, 5% late cut as was applicable on 31.03.2020, shall continue to be applicable for applications submitted till 30.06.2020, and thereafter 10% late cut would be applicable for applications submitted till 31.03.2021.

Extension of RCMC

Extension of validity of Registration cum Membership Certificate (RCMC) beyond 31st March, 2020 –

– It has been decided that Regional Authorities (RAs) of DGFT will not insist on valid RCMC (in cases where the same has expired on or before 31 March, 2020) from the applicants for any incentive/authorizations till 30 September, 2020.

– EPCs will collect the applicable fees for the year 2020-21 on restoration of normalcy

FTP – 2015-20

1. Extension of Scheme of Rebate of State and Central Taxes and Levies on Export of Garments and Made-ups (RoSCTL)

2. It is clarified, without prejudice and subject to changes that may be deemed necessary in public interest from time to time, that:

a) Benefits under MEIS for any item/tariff line /HS Code currently listed in Appendix 3B, Table 2 (MEIS Schedule) will be available only up to 31.12.2020;

b) Prior to 31.12.2020, as and when an item/tariff line/HS code is notified to be covered under RoDTEP Scheme, it would at the same time be removed from coverage under MEIS;

Author Bio