If you are an employee and contributing every month to Employees Provident Fund then you should read this. If you withdraw money from your PF account, the same can be taxable or non-taxable depending on the circumstances of the withdrawal like the period of service, reasons for the withdrawal or the Type of provident fund you are contributing to.

As a general rule, PF withdrawal before completion of 5 years of continuous service is taxable. However, in some cases withdrawal from the PF account even before completion of 5 years of service will not be taxable.

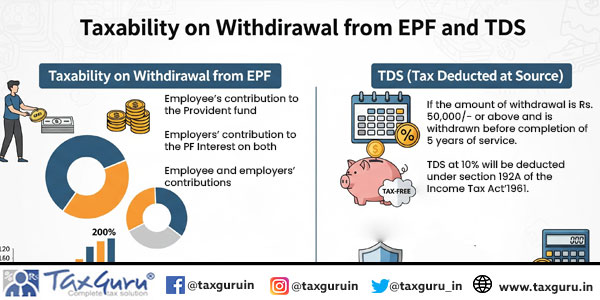

Withdrawal from your Provident fund account consists of three components:

- Employee’s contribution to the Provident fund

- Employers’ contribution to the PF

- Interest on both employee and employers’ contributions

The Taxability of these are as follows:

- Employee contribution being your own contribution to the PF is generally not taxable since you are withdrawing money contributed by your own self to the fund. However, if you have taken benefit of deduction u/s 80C on your contributions to the PF, then you have already saved taxes on your contribution and now the withdrawal of the same will be taxable in your hands.

- Interest on employee contribution is the Interest earned on your contribution to PF and the same will be taxable like any other interest income i.e under the head ‘Income from other sources’.

- Employers’ contribution is the amount contributed by the employer to the employees’ PF account. This amount when withdrawn before completion of 5 years of service will be taxable in the hands of the employee under the ‘Income from Salaries.’

- Interest on employers’ contribution is also taxable on withdrawal in the hands of the employee under the head ‘Income from Salaries’.

TDS on PF withdrawal:

- If the amount of withdrawal is Rs. 50,000/- or above and is withdrawn before completion of 5 years of service.

- TDS at 10% will be deducted under section 192A of the Income Tax Act’1961. However, if PAN is not furnished then TDS @20% will be deducted.

- TDS on withdrawal amount of Employer’s Contribution to PF and interest on the same will be deducted u/s 192 since these incomes are shown under the head salaries. This TDS will be deducted at the tax rate applicable to the employee i.e as per applicable tax slab.

- TDS will be deducted at the time of payment.

- If the employee is a member of an unrecognized PF then withdrawals are taxable and TDS will be deducted irrespective of the period of service.

TDS on EPF withdrawal will not be deducted in the following cases:

- If the amount is withdrawn after completion of 5 years of service (In calculating period of service of 5 years, tenure with previous employer will also be included).

- If the amount of withdrawal is less than Rs. 50,000/-.

- Transfer of PF funds from one account to another i.e. one employer to another.

- Termination of service due to a employees’ illness or discontinuation of business by the employer, the conclusion of a project, or any other reason beyond the employee’s control.

- TDS will also not be deducted if the employee withdraws an amount equal to or more than Rs. 50,000/- with less than 5 years of service but submits form 15G/15H along with PAN.

Below is the summary of Tax and TDS on withdrawal from EPF:

| S. No | Amount Withdrawn from EPF (In Rs.) | Period of Continuous Service | Reason for Withdrawal from PF | Taxability and TDS |

| 1. | < 50,000 | Less than 5 years | – | No TDS but amount withdrawn is taxable and must be shown in the ITR as income. |

| 2. | > 50,000 | Less than 5 years | – | TDS applicable. Also, the amount is taxable and shall be offered for taxation in ITR. |

| 3. | < 50,000 | Less than 5 years | Termination of employment due to ill health of employee/ discontinuation of business of employer/ reasons beyond the control of employee | No TDS and No taxability as amount withdrawn is exempt from Tax. |

| 4. | > 50,000 | Less than 5 years | Termination of employment due to ill health of employee/ discontinuation of business of employer/ reasons beyond the control of employee | No TDS and No taxability as amount withdrawn is exempt from Tax. |

| 5. | < 50,000 | 5 years or more of continuous service | – | No TDS and amount withdrawn is exempt from Tax |

| 6. | > 50,000 | 5 years or more of continuous service | – | No TDS and amount withdrawn is exempt from Tax |

| 7. | – | – | Transfer of PF balance from one employer to another due to job change | No TDS and Taxability as there is no withdrawal from PF just transfer of balance to another account. |

(The author is a Chartered Accountant and can be contacted at info@youronlinefilings.in or capratikanand@gmail.com or Mobile: +91-9953199493)

Author Bio