CIT Vs Diamond Tree (Delhi High Court); ITA 275/2025; 06/08/2025

The treatment of Common Area Maintenance (CAM) charges has been a matter of debate under the Income Tax Act, 1961, particularly with reference to deduction of tax at source (TDS). The issue revolves around whether CAM charges, paid by tenants or showroom owners in malls and commercial complexes, should be treated as part of “rent” under Section 194I or as contractual payments under Section 194C.

The Delhi High Court, in a recent decision, has provided much-needed clarity. In Commissioner of Income Tax (TDS)-1 v. Diamond Tree, the Court held that CAM charges are not rent and, therefore, are not liable to TDS under Section 194I. Instead, such charges fall within the purview of Section 194C, which governs TDS on payments made under contractual arrangements.

The Statutory Framework

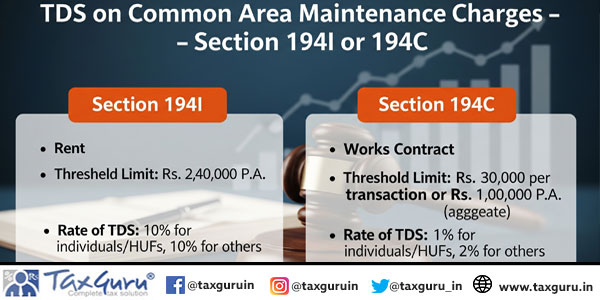

Section 194I requires deduction of TDS on rent paid for the use of land, buildings, furniture, fittings, or equipment, provided the total amount in a financial year exceeds the prescribed limit. The expression “rent” is interpreted widely to cover payments under lease, tenancy, sub-lease, or arrangement for use of assets.

In contrast, Section 194C applies to payments made to contractors and sub-contractors for carrying out any work, including supply of labour, under a contract. The rate of deduction under this section is generally lower than that under Section 194I.

The rate of deduction under Section 194I is generally 10% (for use of land or building), whereas under Section 194C it is 2% for payments to contractors (other than individuals/HUF) and 1% for individuals/HUF contractors.

CBDT Clarifications

The Central Board of Direct Taxes (CBDT) has, from time to time, issued circulars clarifying the scope of “rent” under Section 194I and distinguishing it from contractual payments:

1. CBDT Circular No. 715, dated 8 August 1995

- In the form of FAQs, the Board clarified that where composite payments are made, the nature of the payment should be determined with reference to the agreement.

- Importantly, it clarified that payments for routine maintenance services (such as repairs, servicing, and facilities management) are covered under Section 194C and not Section 194I.

2. CBDT Circular No. 718, dated 22 August 1995

The Board further clarified that “rent” under Section 194I applies only to payments for the use of land, building, plant, machinery, etc., and not to payments for separate contractual services, even if such services are provided in connection with leased premises.

3. CBDT Circular No. 5/2002, dated 30 July 2002

Specifically dealt with “passenger service fees” collected at airports and clarified that such charges are not rent but contractual payments falling under Section 194C.

- Though the context was aviation, the principle—charges for services linked to premises are not rent—has wider application, including to CAM charges.

These circulars lend statutory support to the interpretation later adopted by the courts, that CAM charges, being contractual in nature, do not fall within Section 194I.

This difference in scope has often led to disputes regarding payments that are incidental to lease agreements but not directly for the use of the premises—such as CAM charges.

The Case and Court’s Findings

In the Diamond Tree case, the assessee was a showroom owner in Ambience Mall, New Delhi. While the assessee duly deducted TDS on rent paid to the landlord, it did not deduct TDS on CAM charges under Section 194I. The Income Tax Department contended that CAM charges formed an integral part of the rent and, therefore, should attract TDS under Section 194I.

The matter reached the Delhi High Court, which rejected the Revenue’s argument. The division bench of Justice V. Kameswar Rao and Justice Vinod Kumar observed that CAM charges are not payments for the use of premises, but rather for availing facilities such as security, cleaning, electricity for common areas, and general maintenance of shared spaces. These services may be provided by the landlord or outsourced to third-party agencies, but in either case, the payment is contractual in nature.

The Court relied on its earlier ruling in Commissioner of Income Tax (TDS)-1 v. Liberty Retail Revolutions Limited, where it was held that CAM charges are distinct from rental payments and fall squarely under Section 194C. The Court emphasized that the scope of Section 194I is limited to payments for use of premises or equipment and cannot be extended to cover maintenance services.

Accordingly, the Court dismissed the Revenue’s appeal and affirmed that CAM charges attract TDS under Section 194C and not Section 194I.

Practical Implications

The ruling provides significant clarity for businesses operating from leased commercial premises. Many malls, office complexes, and industrial parks levy CAM charges, often under a separate head in the lease agreement. Tenants frequently face uncertainty on whether to deduct TDS under Section 194I or Section 194C.

The High Court’s ruling confirms that:

Rent payments must be subjected to TDS under Section 194I.

CAM charges must be subjected to TDS under Section 194C, being contractual payments for services.

Even if rent and CAM charges are billed together, they should be bifurcated to ensure proper compliance.

This approach not only ensures adherence to law but also prevents unnecessary disputes and demands from the tax department.

Conclusion

The Delhi High Court’s judgment in CIT (TDS)-1 v. Diamond Tree reinforces the distinction between rent and service charges in the context of TDS obligations. While rent clearly falls under Section 194I, CAM charges are contractual payments that attract TDS under Section 194C.

This ruling aligns taxation with the true nature of the transaction and provides certainty for taxpayers dealing with complex lease and maintenance structures in commercial real estate. Businesses should carefully review their lease agreements and ensure that rent and maintenance charges are appropriately segregated and subjected to TDS under the correct provisions of law.

****

Disclaimer: This article is intended for informational purposes only and does not constitute legal or tax advice. Readers are advised to consult their professional advisors before taking any decision based on the contents of this article. The views expressed are based on judicial precedents available at the time of writing and may be subject to change with future developments in law.

Author Bio