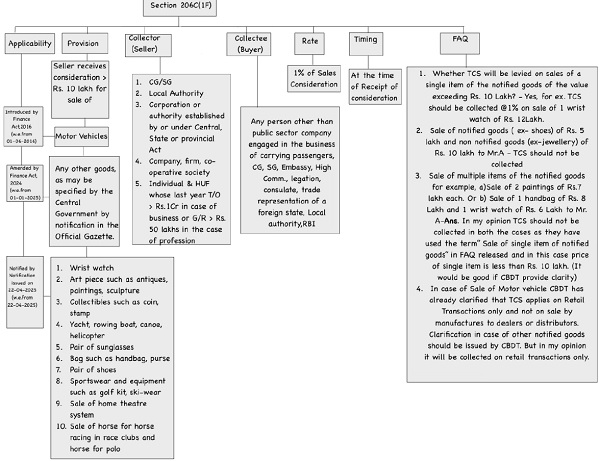

Introduction: The amended provisions extend the applicability of TCS at the rate of 1%, effective from 1st January 2025 to any other goods that may be notified by the Central Government, provided the value exceeds Rs. 10 lakh. As of now, 10 goods have been notified by the government on which TCS at 1% is to be collected (w.e.f. from 22-04-2025).

Bare Act Provision (Post Amendment) is as follows:

Following sub-section (1F) shall be substituted for the existing sub-section (1F) of section 206C by the Finance

(No. 2) Act, 2024, w.e.f. 1-1-2025:

(1F) Every person, being a seller, who receives any amount as consideration for sale of—

- a motor vehicle; or

- any other goods, as may be specified by the Central Government by notification in the Official Gazette, of the value exceeding ten lakh rupees, shall, at the time of receipt of such amount, collect from the buyer, a sum equal to one per cent of the sale consideration as income-tax.

(source: https://incometaxindia.gov.in/Pages/acts/income-tax-act.aspx )

Chart Prepared by the Author

Key Points:

Applicability: Applicability of this section is as follows

| Motor Vehicles | With effect from 01-06-2016 |

| 10 Notified Luxury Goods | With effect from 22-04-2025 |

Provision: TCS should be collected by the seller, when he receives any amount of consideration exceeding Rs. 10 Lakh for sale of :

a. Motor Vehicle

b. any other goods, as may be specified by the Central Government by notification in the Official

Gazette:

The Notification notifies the following ten goods of the value exceeding Rs. 10 Lakh for TCS @ 1%:

a. any wristwatch

b. any art piece such as antiques, painting, sculpture

c. any collectibles such as coin, stamp

d. any yacht, rowing boat, canoe, helicopter

e. any pair of sunglasses

f. any bag such as handbag, purse

g. any pair of shoes

h. any sportswear and equipment such as golf kit, skiwear

i. any home theatre system

j. any horse for horse racing in race clubs and horse for polo

Collector (Seller):

“seller” with respect to sub-section (1) and sub-section (1F) means:

- the Central Government,

- a State Government or

- any local authority or corporation or authority established by or under a Central, State or Provincial Act, or

- any company or firm or co-operative society, or

- an individual or a Hindu undivided family whose total sales, gross receipts or turnover from the business or profession carried on by him exceed one crore rupees in case of business or fifty lakh rupees in case of profession during the financial year immediately preceding the financial year in which the goods of the nature specified are sold.

Collectee (Buyer): means a person who obtains in any sale, goods of the nature specified in the said subsection, but does not include,—

- the Central Government, a State Government and an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State; or

- a local authority as defined in Explanation to clause (20) of section 10; or

- a public sector company which is engaged in the business of carrying passengers.

Rate: TCS @1% of sales consideration. (Inclusive of GST & other charges).

(Failure to furnish Aadhar-linked PAN by buyer attracts higher TCS at 5%)

Timing: TCS should be collected at the time of receipt of consideration.

FAQ:

1. Will TCS be levied on the sale of a single item of the notified goods, if the value exceeds Rs. 10 lakh? – Yes. For example, TCS at the rate of 1% should be collected on the sale of a wristwatch priced at Rs. 12,00,000.

2. Whether TCS will be levied in the following examples?

Example 1: Sale of notified goods (e.g., shoes) worth Rs. 5 lakh and non-notified goods (e.g., jewellery) worth Rs.10 lakh to Mr. A.

Answer: No, TCS should not be collected, as the value of the single item of notified goods does not exceed Rs. 10 lakh.

Example 2: Sale of multiple items of notified goods—e.g., two paintings worth Rs.7 lakh each (same class of goods)—to Mr. A.

Answer: In my opinion, TCS should not be collected, as per the FAQs released by the CBDT. TCS is applicable on the sale of a single item of notified goods exceeding Rs. 10 lakh. In this example, the value of each individual item does not exceed Rs. 10 lakh. (Note: This aspect has not been specifically clarified by the CBDT. It would be helpful if the CBDT provides explicit clarification.)

Example 3: Sale of multiple items of different notified goods—e.g., one painting worth Rs. 7 lakh and one wrist watch worth Rs.5 lakh—to Mr. A.

Answer: In my opinion, TCS should not be collected, as none of the individual items exceeds the ₹10 lakh threshold. (Note: This scenario also remains unclarified by the CBDT. A clarification on this point would provide better compliance certainty.)

3. Whether TCS will apply to all transactions, including sales by manufacturers to dealers/distributors, or only to retail sales, similar to the provisions applicable to motor vehicles? Answer: In my opinion, TCS should be applicable only to retail sales transactions in the case of notified goods. This interpretation aligns with the treatment under motor vehicle sales. However, it would be helpful if the CBDT issues a clarification to this effect to avoid any ambiguity in implementation.

4. In the case of notified goods, only broad descriptions have been provided, along with illustrative examples — for instance, “any art piece such as antiques, paintings, sculptures, etc. Greater clarity is required regarding the definition of terms such as “art piece” and “collectible.” As these terms are open to interpretation, a clear and comprehensive definition from the CBDT would help ensure uniform understanding and implementation of the TCS provisions.

Conclusion: The recent amendment to Section 206C(1F) significantly broadens the scope of TCS by extending its applicability to notified luxury goods. This measure is aimed at enabling better tracking of high-value transactions. It will also contribute to enhancing the accuracy and comprehensiveness of the Annual Information Statement (AIS). Sellers dealing in such high-value luxury items must ensure strict compliance. This includes obtaining a Tax Collection Account Number (TAN), timely deposit of TCS, filing of quarterly TCS statements, and issuance of TCS certificates to buyers. Proper adherence to these requirements will not only help in regulatory compliance but also support the broader objective of expanding and deepening the tax base.

Disclaimer: The examples and interpretations shared in this article reflect my personal understanding and experience.