Introduction

The Securities Exchange Board of India (SEBI) has introduced a Small Medium Real Estate Investment Trust (hereinafter referred to as “SM REITs[1]“) by a recent amendment to the Real Estate Investment Trust, 2014 (hereinafter referred to as “REITs), thereby paving the way to make real estate investment more accessible to a wider set of investors. REIT is defined under the Regulation 2(1)(zm)[2], a person who pools INR 50 crores or more for the purpose of issuing the units to at least two hundred investors to acquire and manage real estate assets. Those who can’t afford a high-ticket property under REITs can now participate in SM REITs. Prior to the introduction of SM REITs, all real estate investment was governed through fractional ownership platforms (FOPs), where a pool of investors invested their money into real estate assets such as buildings and office spaces, including warehouses, shopping centres, conference centres, etc. To put it simply, FOPs provide an opportunity for a group of people to pool money and jointly purchase real estate assets. Over the years, the fractional ownership platform has gained momentum, and SEBI has been constantly keeping an eye on the Indian market. As a result, SEBI decided to govern the FOPs under small medium real estate investment trust, or SM REITs, to safeguard investors against fraud of any kind. The aim of the introduction of SM REITs by SEBI to foster a broader range of real estate investments while ensuring transparency, control, and credibility for investors, which are favourable to individual investors who can invest money without incurring risks, was an exposure to the rise in investing on fractional platforms.

This article aims to highlight the structure of SM REITs, their main features, and real estate investment through fractional ownership platforms. The author also looked into the comparatively study of SM REITs and REITs and the way forward for SM REITs.

Page Contents

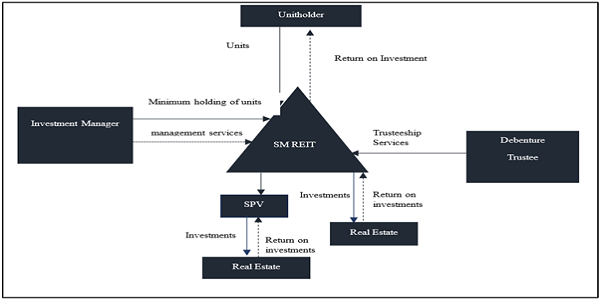

Structure of SM REITs:

Real Estate Investment through Fractional Ownership Platform (FOP) and SEBI’s take on FOP:

The real estate market in India has witnessed a notable increase in investment in the past few years. These investments have included buildings, offices, shopping malls, and other real estate assets in exchange for a portion of the ownership. Fractional Ownership Platforms, or FOPs, is a new buzzword in the Indian real estate industry. It is a commercial real estate notion where investors could buy a portion of real estate on these platforms for between INR 10 lakhs and INR 20 lakhs. To say it a different way, FOPs provide a group of people an avenue to pool their resources and purchase real estate jointly. In the post-Covid-19 world, investors remain on the lookout for different avenues for investment. Apart from gold, stocks, and government bonds, real estate is a consistent Favourite for people to invest money. In India, there were not any platforms available for retail investors to invest their money in fractions in the real estate sector. REITs do not work out here because of requirements such as minimum asset size of INR 500 crore, minimum public issue size of INR 250 crore, and investment manager net worth. So, FOP was the only option available to retail investors to invest their money in real estate. The strategy generally adopted by these FOPs is that the investors subscribe to the securities of a special purpose vehicle (SPV) established by the FOPs, which in turn purchases the actual real estate asset.

Let us understand this with an example: A group of investors is managing a commercial property worth Rs. 25 crores. They invite retail investors to invest a minimum of Rs. 10 lakh and earn fixed returns in proportion to their investments.

Over the past few years, there has been a significant rise in retail investor investment in fractional ownership platforms, as observed by SEBI, acting as a watchdog. As FOPs gained popularity over time, investors money was at risk because these platforms were not regulated by SEBI controls. The FOPs may violate the Companies Act of 2013, the Prevention of Money Laundering Act of 2022, and other laws, therefore SEBI decided to regulate these platforms by introducing a new chapter on small and medium real estate investment trusts under REIT Regulation 2014. There were numerous issues with the FOPs, which need to be regulated for the sake of investor protection. The above reasons provided by SEBI hinge on assumptions that might not be in breach of the law. However, as every healthcare professional is accustomed to cautioning patients that “prevention is better than cure,” here SEBI is acting as a healthcare professional, which assumes the above-cited laws for the safeguard of investors. Outlined below are the principal reasons given by SEBI for overseeing FOPs:

In contrast to more constructed vehicles like mutual funds and real estate investment trusts, which have been around for decades, the fractional ownership platform from the commercial real estate concept is entirely new, and as a result, people are oblivious of and have limited knowledge about investing in FOPs. Retail investors use these platforms to make investments, but co-ownership is another problem with fractional real estate. Because there was no hierarchy structure exist on these platforms, it implies who would make the decisions about investments and who would have authority over the property. As a result, investors were hesitant to make investments in fractional estate.

The lack of exit mechanisms is another issue with fractional investment. Retail investors invested money on these platforms, but as these FOPs players manage the secondary market, which can cause liquidity delays, they have no way to get their money out of the platform and invest it elsewhere. The main issue with fractional investments is that they are not regulated by SEBI, so the rules and regulations of SEBI do not apply to these platforms, so the managers of these platforms invest the investor’s money of their own choice without following the regulations of SEBI. Due to a lack of openness and disclosure of essential information, investors may experience losses as a consequence of misselling, and ultimately, they may incur losses as a result of the manager’s negligent management. Thus, SEBI chose to regulate these platforms in order to protect investors.

Small and Medium Real Estate Investment Trust or SM REITs

The Securities and Exchange Board of India (“SEBI”) objective in setting up SM REITs is to facilitate a broader group of investors to participate in fractional ownership because of the reduced asset base value (INR 50 crores compared to INR 500 crores in the current REITs regime) and the possibility of utilising special purpose vehicle (or “SPV[3]“) structures to leverage distinct holding schemes. These SM REITs seek to promote a wider variety of real estate investments while guaranteeing investors’ confidence, transparency, and control, with a lowered minimum asset size of INR 50 crore. Retail investors are made accessible while still keeping a certain level of expertise with the minimum ticket size investment threshold of INR 10 lakh. According to the regulation, the investment manager must file a trust deed registered under the Indian Registration Act, 1908, with SEBI in order to apply for the issue of a certificate of registration. The investment manager’s net worth shall not be less than INR 20 crores. Furthermore, it is proposed that the investment manager possess a minimum of two years of real estate industry expertise or at least employ two key managerial professionals who have at least five years of real estate industry experience. The current FOPs that are investing in real estate will need to register with SEBI as SM REITs in accordance with the recently introduced regulations for SM REITs and meet all requirements set forth by the regulators. In this instance, FOPs operations will be halted upon failure to fulfil the specified requirements.

This article is about small and medium real estate investment, but the author also looked into the comparative analysis of REITs and SM REITs and the notable changes brought by SEBI in SM REITs that were not in the REITs. The net worth requirements of SM REITs and REITs are similar in both regulations, but the mandatory unitholding of 15% for three years by the sponsors of SM REITs can be a positive step because this will not only reassure the investors but also work for the betterment of the scheme and the trust of the investors. Additionally, the number of minimum investors in REITs is brought down to 20 in SM REITs by SEBI. At last, but not least, the distribution of income in REITs is required to distribute 90% of their net distributable cash flows, but in SM REITs, at least 95% of the SPV’s net cash flow must be distributed.

Way Forward for SM REITs

Every coin has two sides, one of which has a positive impact and the other a negative one. The emergence of SM REITs is no different. Under the REITs Regulation 2014, SEBI introduced SM REITs, which will have both positive and negative effects. FOPs, which are governed by SM REITs, are a smart move on the side of SEBI to promote investment through small and medium-sized investors. This will address grievance redressal methods in along with offering investors stability. It permits risk management, fair pricing, liquidity, and exit opportunities in addition to giving investors transparency and disclosure obligations. In the existing FOPs, the presence of multiple fractional owners is also an issue because the presence of multiple owners in a place will not only affect the decision regarding the investment but will also suppress the investors who have a small investment on these platforms. In REITs, the investment manager can only invest in commercial properties, but under the new regime of SM REITs, the investment can be made in both commercial and residential areas. The minimum net worth of a sponsor or investment manager can act as a barrier for the major players who want to purchase such products as either sponsors or investment managers. According to the author, the introduction of SM REITs has a more positive impact and renders investments accessible to many players who were previously unable to do so because of the REITs minimum net asset value. Additionally, it gives investors transparency; previously, FOPs absence of exit mechanisms had negatively impacted investors. However, as many players are prevented from rendering these products by the minimum net worth requirement for sponsors or investment managers, SEBI ought to look into this issue. Additionally, it is essential to review and reevaluate the proposed regulatory framework in order to ensure merited investment discipline heading ahead.

Notes

[1] Small and Medium REIT” or “SM REIT” means a REIT that pools money from investors under one or more schemes in accordance with sub-regulation (2) of regulation 26P.

[2] SBEI Real Estate Investment Trust Regulations, 2014

[3] Special purpose vehicle” or “SPV” means any company which is a wholly owned subsidiary of the scheme of the SM REIT and the SPV shall not have any other capital or ownership interest in it.

Mr. Ankit Singh is a 4th Year B.A., LL.B student at Dr D.Y. Patil College of law (Mumbai University), Navi Mumbai. The author can be reached at ankitchauhan9821@gmail.com

Mr. Ankit Singh is a 4th Year B.A., LL.B student at Dr D.Y. Patil College of law (Mumbai University), Navi Mumbai. The author can be reached at ankitchauhan9821@gmail.com