Case Law Details

Kisankraft Machine Tools Private Limited Vs Commissioner of Customs (CESTAT Chennai)

CESTAT Chennai held that imported goods being handheld machines popularly known as brush cutter is classifiable under CTH 84672900 and parts of brush cutter is classifiable under CTH 84679900.

Facts- The assessee imported certain goods describing them as “Agricultural Reaper” of different models and parts thereof, and filed Bills-of-Entry by classifying the same under Customs Tariff Heading (CTH) 8433 9000, which were assessed at the rate of BCD as applicable, exemption for CVD was claimed under Notification No. 21/2012 (Sl. No. 2).

Revenue having observed that the imported goods being portable machines having self-contained internal combustion engine mounted on a light metal frame and equipped with cutting devices, felt that the goods were classifiable under CTH 8467 2900, which attracted CVD at the rate of 12.5%. After due process the original authority having considered the case of the importer, proceeded to confirm the proposals made by him in the Show Cause Notice classifying the goods under CTH 8467.

Commissioner (Appeals) too has upheld the classification. Being aggrieved, the present appeal is filed.

Conclusion- The goods from their description, weight, common use understanding, pictures given in the Order in Original and appeal booklet etc. goes to show that the impugned goods are tools for working in the hand. They are primarily advertised for and used to remove unwanted growths like weeds, small cultivations, thick grasses, and hardy hedge plants and not for harvesting crop. They are trimming or cutting machines rather than reaping, crop-lifting, gathering, picking, threshing, binding or bundling machines. They are hence classifiable under CTH 8467.

Held that since the classification of the goods is found to be falling under CTH 8467, hence in terms of Note 2(b) of Section XVI, parts of ‘brush cutter’ will be classifiable under CTH 84679900.

FULL TEXT OF THE CESTAT CHENNAI ORDER

The details of the present appeals filed by the assessee are as under: –

|

Sl. |

Appeal No. | Appellant | Bill-of-Entry No. &

Dt. |

Impugned order No. & Dt. |

Duty /

Penalty / Fine |

| (1) | (2) | (3) | (4) | (5) | (6) |

| 1. | C/41118/2014 | Kisankraft Machine Tools Pvt. Ltd. |

4802478/30.09.2011,

4673148/17.09.2011 |

Order-in-Appeal C.Cus. No. 434/2014 dtd. 10.03.2014 | Duty short-paid Rs.2,22,180/-(No penalty) |

| 2. | C/41907/2015 | Kisankraft Machine Tools Pvt. Ltd. | 3559187/20.05.2011, 3559189/20.05.2011, 3782822/14.06.2011, 4088758/15.07.2011, 4164371/25.07.2011, 4176057/26.07.2011 | Order-in-Appeal C.Cus. II No. 548/2015 dtd. 29.05.2015 | Differential duty demand of Rs. 28,25,739/-Penalty Rs.50,000/- u/s 112(a) of the Customs Act, 1962 |

| 3. | C/41715/2017 | Kisankraft Machine Tools Pvt. Ltd. | 7678255/16.08.2012, 8322952/26.10.2012, 7162275/20.06.2012, 6727767/03.05.2012 | Order-in-Appeal C. Cus. II Nos. 348 to 350/2017 dtd. 24.04.2017 | Differential duty demand of Rs. 31,80,608/ plus equal penalty u/s 114A of the Customs Act, 1962 |

| 4. | C/41716/2017 | Kisankraft Machine Tools Pvt. Ltd. | 5323114/20.11.2011, 6078000/23.02.2012 | Differential duty demand of Rs.4,17,777/- plus equal penalty u/s 114A of the Customs Act, 1962 | |

| 5. | C/41717/2017 | Kisankraft Machine Tools Pvt. Ltd. | 9678154/25.03.2013, 9473984/04.03.2011, 9251108/07.02.2012, 9349291/08.02.2013 | Differential duty demand of Rs.11,56,756/- plus equal penalty u/s 114A of the Customs Act, 1962 | |

| 6. | C/40178/2020 | Kisankraft Ltd. [Formerly ‘Kisankraft Machine Tools Pvt. Ltd.’] | 4941445/18.04.2016, 5283424/17.05.2016, 5700976/20.06.2016, 5835755/01.07.2016, 6235451/04.08.2016, 7161272/20.12.2016, 5714977/21.06.2016, 5808074/29.06.216, 5807690/29.06.2016, 5979078/14.07.2016, 4850192/09.04.2016, 5330861/20.05.2016 | Order-in-Original No. 73345/2020 dtd. 24.01.2020 | Differential Duty demand Rs.67,15,462/- With equal penalty u/s 114A of the Customs Act, 1962 |

2.0 Brief facts which are common to all the appeals are that the assessee imported certain goods describing them as “Agricultural Reaper” of different models (some of which are listed at para 14 of the impugned order C/40178/2020) and parts thereof, and filed Bills-of-Entry by classifying the same under Customs Tariff Heading (CTH) 8433 9000, which were assessed at the rate of BCD as applicable, exemption for CVD was claimed under Notification No. 21/2012 (Sl. No. 2).

2.1 Revenue having observed that the imported goods being portable machines having self-contained internal combustion engine mounted on a light metal frame and equipped with cutting devices, felt that the goods were classifiable under CTH 8467 2900, which attracted CVD at the rate of 12.5%. After due process the original authority having considered the case of the importer, proceeded to confirm the proposals made by him in the Show Cause Notice classifying the goods under CTH 8467. Similarly, in the case of earlier orders, the Commissioner (Appeals) too has upheld the classification as confirmed in the respective Orders in Original.

2.2. It is against the orders listed at column 5 of the Table at para 1. above that appeals have been filed before us. The dispute is whether the impugned goods declared as “Agriculture Reaper” and “Spare parts of Reaper” are classifiable under CTH 84672900 and 84679900 respectively (Revenue) or under CTH 84331190 and 84339000 respectively (Appellant).

2.3 No cross objections have been filed by Revenue.

3.Heard Shri G. Shiva Kumar, Ld. Chartered Accountant for the appellant and Shri M. Ambe, Ld. Deputy Commissioner for the Revenue. Their submissions and the points stated in the appeal are as below.

Department’s View:

4. The following points have been made by Revenue:

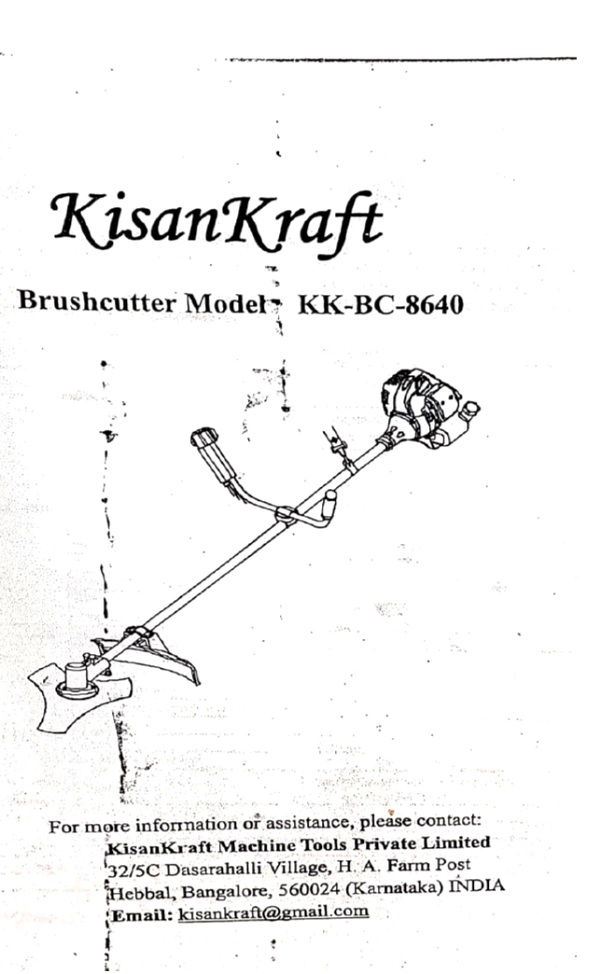

(i) The goods as seen from the Appellants website and literature are marketed as “Brush Cutters” to cut or trim bushes, hedges, weeds, plants and grass.

(ii) Brush cutters are primarily used for trimming or cutting rather than reaping, croplifting, gathering, picking, threshing, binding or bundling. Their primarily use is to remove unwanted growths like weeds, small cultivations, thick grasses, and hardy hedge plants.

(iii) As per the advertisement, supply orders to Govt programs and other selective material given by the appellant the impugned goods are known as ‘brush cutters’ or ‘weed cutters’ and have been purchased for use in agricultural and horticultural fields.

(iv) Weight of the majority of machines varies from 10-12 Kgs and are designed to be handled by a single operator and carried in hand.

(v) Explanatory Notes to heading 8467 at Sl no 19 gives exact specifications of machines included in the heading and includes portable brush-cutters with a self-contained motor, a drive shaft (rigid or flexible) and a tool holder.

(vi) In terms of the Explanatory Notes to HSN the machines of CTH 8433 are used in place of hand tools for agricultural operations. The machines for working in hand are thus excluded from the CTH 8433.

(vii) In terms of Note 2(b) of Section XVI, parts of brush cutter will be classifiable under CTH 84679900.

Appellant’s Averments

5. The following pleadings have been made by the Appellant:

(i) In terms of HSN Explanatory Notes to Chapter 84, (B) General Arrangement of the Chapter, Sl. No. 3, items falling under Headings 84.25 to 84.78 would cover machines which are classifiable by reference to the field of industry in which they are used, regardless of their particular functions.

(ii) CTH 8433 covers harvesting and post harvesting agricultural machinery and also includes machinery used in Lawns, Sports ground, and parks.

(iii) The List in HSN Explanatory HSN provides list of items that may fall in 8467 and excludes items by their weight or size which cannot be used in hand. The impugned goods cannot be used “in” hand.

(iv) Without prejudice, even assuming, without admitting, for the sake of argument that Sl. No. 19 covers the present items also, then unlike Sl. No 18 (which is excluded from 8433), Sl. No 19 is not excluded from 8433 in the Explanatory Notes. Thus, the item will fall both under 8433 and 8467. HSN Explanatory Note (D) to Chapter 84 states that in case machines fall under two or more headings – principal use of the machine. Since the principal use is established as Agricultural, the goods will fall under 8433.

5.1 The impugned goods as given by them in their appeal booklet is reproduced for easy reference:-

6. We have gone through the appeal papers and have heard the rival parties carefully. Being a matter of classification of goods the burden of proof is on Revenue to show that the particular case or item in question is taxable in the manner claimed by them. The correct manner of classifying imported goods under the Customs Tariff, is by interpreting the headings and notes etc. as per the Rules for the Interpretation of the Schedule to the Customs Tariff Act, 1985. According to Rule 1 titles of sections and chapters in the Schedule are provided for ease of reference only. But for legal purposes, classification ‘shall be determined according to the terms of the headings and any relevant section or chapter notes’. If neither the heading nor the notes suffice to clarify the scope of a heading, then it must be construed according to the provisions contained in the Rules. Rule 1 gives primacy to the section and chapter notes along with terms of the headings. They should be first applied. The need to refer to the HSN and resort to any interpretative process arises only where the meaning is not manifest. If the words are plain and clear and directly convey the meaning, there is no need for any interpretation.

7. It is not dispute that the Schedule to the Customs Tariff in itself does not contain a specific heading for “Agricultural Reaper” and its parts. There is also no dispute that though different models of goods have been imported all are sought to be classified under one heading. Finally, it is also not disputed that the impugned goods are marketed and known in the trade as “brush cutters” as also seen from the product literature and the tender notices etc. enclosed with the appeal.

8. In M/s Indo International Industries v. Commissioner of Sales Tax, Uttar Pradesh, [1981 (2) SCC 528], it has been held by the Apex Court that “if any term or expression has been defined in the enactment then it must be understood in the sense in which it is defined but in the absence of any definition being given in the enactment the meaning of the term in common parlance or commercial parlance has to be adopted“. In Plasmac Machine Manufacturing Co. Pvt. Ltd. v. Collector of Central Excise, Bombay [1991 (51) E.L.T. 161 (SC) = 1991 Suppl (1) S.C.C. 57], it was held by the Apex Court :

“It is an accepted principle of classification that the goods should be classified according to their popular meaning or as they are understood in their commercial sense and not as per the scientific or technical meaning. Indo International Industries v. CST [1981 (2) SCC 528] and Dunlop India Ltd. v. Union of India [1976 (2) SCC 241] have settled this proposition. How is the product identified by the class or section of people dealing with or using the product is also a test when the statute itself does not contain any definition and commercial parlance would assume importance when the goods are marketable as was held in Atul Glass Industrial (Pvt.) Ltd. v. CCE [1986 (3) SCC 480] and Indian Aluminium Cables Ltd. v. Union of India [1985 (3) SCC 284]. In Asian Paints India Ltd. v. CCE [1988 (2) SCC 470] which was a case of emulsion paint, at para 8, it was said:

“It is well settled that the commercial meaning has to be given to the expressions in tariff items. Where definition of a word has not been given, it must be construed in its popular sense. Popular sense means that sense which people conversant with the subject matter with which the statute is dealing, would attribute to it.”

(emphasis added)

Further in Commissioner of Customs and Central Excise, Amritsar (Punjab) Vs. D.L. Steels etc [2022 SCC OnLine SC 863] the Hon’ble Apex Court stated that the Harmonised System of Nomenclature, developed by the World Customs Organisation, has been adopted in India by way of the Customs Tariff Act, 1975, though there are certain entries in the Schedules to this Act which have not been assigned HSN codes. In the present times, given the widespread adoption of the Harmonised System by over 200 countries, it would be extremely difficult to deal with an international trade issue involving commodities, without adverting to the Harmonised System. The Code is the bedrock of custom controls and procedures.

9. We hence proceed to examine the classification of the impugned goods as finalized in the impugned orders and which in popular / trade parlance are known as “brush cutters’. The CTH 8467 preferred by Revenue pertains to ‘TOOLS FOR WORKING IN THE HAND, PNEUMATIC, HYDRAULIC OR WITH SELF-CONTAINED ELECTRIC OR NON-ELECTRIC MOTOR’, whereas CTH 8433 which reflects the Appellants choice covers ‘HARVESTING OR THRESHING MACHINERY, INCLUDING STRAW OR FODDER BALERS; GRASS OR HAY MOWERS; MACHINES FOR CLEANING, SORTING OR GRADING EGGS, FRUIT OR OTHER AGRICULTURAL PRODUCE, OTHER THAN MACHINERY OF HEADING 8437’. The impugned goods which are handheld machines, would at first sight and by its popular name as ‘brush cutter’, be more suitable to be classified under CTH 8467. However, the goods due to the dispute in their classification needs to be examined with support from the HSN.

10. As per Explanatory Notes to heading 8467 the tools included under the heading are shown in a list and include at Sl. No. 19, portable brush-cutters with a self-contained motor, a drive shaft (rigid or flexible) and a tool holder, presented together with various inter changeable cutting tools for mounting in the tool holder. Whereas portable machines for trimming lawns, cutting grass in corners, along wall, borders or under bushes which have a self-contained motor in a light metal frame and a cutting device usually consisting of a thin nylon thread are included at Sl. No. 18 of the said list. Revenue feels that the description at Sl. No. 19 fits the impugned goods perfectly and hence CTH heading 8467 holds good for classifying the impugned goods. The Appellant states that even in this worst-case scenario Sl. No 19 is not excluded from 8433 in the Explanatory Notes. Thus, the item would fall both under CTH 8433 and 8467. HSN Explanatory Note (D) to Chapter 84 states that in case machines fall under two or more headings – principal use of the machine. Since the principal use is established as Agricultural, the goods will fall under 8433. We do not find much substance in this argument by the Appellant as portable brush-cutter are specifically covered under CTH 8467 and as per the rule of construction a general description if at all must yield to those of a special one.

11. The impugned order states that the said goods weigh 10-12 Kgs and are portable machines designed to be handled by a single operator and carried in hand. In terms of the Explanatory Notes to HSN the machines of CTH 8433 are used in place of hand tools for agricultural operations. The machines for working in hand are thus excluded from CTH 8433. CTH 8467 specifically deals with tools for working in the hand. The Appellant during oral arguments, on the other hand, avers that the impugned goods cannot be used “in” hand in the sense of ‘in the palm of the hand’.

11.1 The usage of the phrase “in hand” is very much idiomatic and has to be understood very broadly. No hard and fast meaning can be attributed to it. So, there will be a limit as to how far one can “rationalise” it with any particular meaning. Metaphorically ‘in hand’ in one of its meanings is understood as an extension of a grasping hand with something (like a tool or machine for instance) in it. It has different meanings when spoken in Britian and in America. “In hand” can;

1) literally refer to something that someone is holding

2) be used to describe a situation, synonymous with “under control”

3) refer to something that is possessed in excess or

4) refer to a situation that is currently being dealt with.

The last three ways are much more common in British English than in American English. American English uses “at hand” instead of “in hand” and so forth.

11.2 This goes to show that language is an imperfect vehicle of thought and the ability of the written language to precisely convey technical information and description of products as done by mathematical symbols and formula, especially in the case of legal matters, enactment or notifications, may not at all times be achieved. As said “It is difficult to expect the Legislature carving out a classification which may be scientifically perfect or logically complete or which may satisfy the expectations of all concerned”. The inability of words to achieve precision at times makes it necessary, as discussed above, to understand the legislative intent by the one principle which is fairly well settled by a catena of judgments by the Supreme Court, that words and expressions describing goods in a taxing statute should be construed in the sense in which they are understood in the trade, by the dealer and the consumer. The reason is that it is they who are concerned with it and it is the sense in which they understood it which constitutes the definitive index of the legislative intention. This perhaps reflects the Constitutional Court’s thinking on the inability of the English language to convey complex technical information with a high degree of legal certitude in the classification of goods and services. The goods from their description, weight, common use understanding, pictures given in the Order in Original and appeal booklet etc. goes to show that the impugned goods are tools for working in the hand. They are primarily advertised for and used to remove unwanted growths like weeds, small cultivations, thick grasses, and hardy hedge plants and not for harvesting crop. They are trimming or cutting machines rather than reaping, crop-lifting, gathering, picking, threshing, binding or bundling machines. They are hence classifiable under CTH 8467.

12. The Appellant has stated that as per Note 4 to Section XVI, which covers chapter 84, for machines with a clearly defined function by one of the headings in Chapter 84 or 85, the whole falls to be classified in the heading appropriate to that function. We find that both the disputed heading fall under chapter 84 and as per the discussions have been found to have a clearly defined function covered by CTH 8467. Revenue has thus been able to discharge its burden and the impugned orders merit to be upheld.

13. Since the classification of the goods is found to be falling under CTH 8467, hence in terms of Note 2(b) of Section XVI, parts of ‘brush cutter’ will be classifiable under CTH 84679900.

14. The Appellant is also aggrieved by the imposition of penalty under Section 114A of the Customs Act. The matter, they say, has been in dispute since 2012. They have pointed out that as recorded in the SCN they had paid tax ‘under protest’ under CTH 8467 and that it was the Department which directed the Appellant to switch back to the Classification of CTH 8433. The impugned order on the other hand has stressed on the willful misstatement of the CTH of the goods which were described as ’brush cutters’ on their website and pamphlet but as ‘agricultural reapers’ in the Bills of Entry.

The findings in this regard are recorded at para 17 and are reproduced below:

“The Show Cause Notice has alleged short-levy of duty on impugned goods due to mis-classification. The importer have mentioned in their reply that the department has been raising the issue of mis-classification of Brush Cutters since 2012. Based on audit findings, the demands of short-levied duties have been confirmed by adjudicating authorities in past several cases and upheld by appellate Commissioners and most of the cases are pending before Hon’ble CESTAT. Thus, the entire issue and rival CTH were known to importer as well. In addition, it is also pertinent to mention here that immediately on receipt of audit findings, the importer was issued a letter vide F. No. TA/116085/2017 Gr. 5 dated 20.11.2017 for effecting payment of short-levied duty in this case, within the ambit of two years from the relevant date. The importer has also submitted written submissions dated 24.1.2018 to the aforesaid letter. Therefore, the importer cannot take refuge under the allegation that demand is time-barred and deviate from the main issue of mis-classification which resulted in short-levy of duty. . . . . In this case, it is not alleged in SCN that this is a case of suppression of facts alone but SCN has emphasized on mis-classification of impugned goods despite the fact that importer was aware of the issue and on several occasions, classification have already been decided by department by the way of issuance of several Order in Originals since 2012. The importer have themselves stated that they started classifying the goods under CTH 8467 and paid the duty under protest for some period. However, on gaining AEO status in 2016, the importer reverted to previous CTH 8433. Further, there is no documentary evidence on record wherein the issue of classification of Brush Cutters has been settled during the period of subject imports. Many cases were still pending before Hon’ble Tribunal for decision where importer had filed appeal. The importer has mainly contended that the impugned gods are used for agricultural purposes and specifically mentioned under heading 8433, which appears wrongly conceived idea in view of relevant chapter notes and HSN explanatory notes which act as guiding factor in deciding classification. Several agricultural tools are explicitly classified under various other heading such as 8201, 8208, 8424, 8428 and so on. The use of any machinery / tools for agriculture purpose alone cannot be assumed to be the sole criteria to determine classification.”

(emphasis added)

15. The learned Adjudicating Authority went on to impose a penalty under section 114A of the Customs Act 1962 for the blame worthy act. The relevant portion of the Section reads as under;

“114A. Penalty for short-levy or non-levy of duty in certain cases.:- Where the duty has not been levied or has been short-levied or the interest has not been charged or paid or has been part paid or the duty or interest has been erroneously refunded by reason of collusion or any willful mis-statement or suppression of facts, the person who is liable to pay the duty or interest, as the case may be, as determined under sub-section (2) of section 28 shall also be liable to pay a penalty equal to the duty or interest so determined: . . . .

The Appellant has submitted that when the demand is itself not sustainable the penalty is also liable to be dropped. Further they have stated that a penalty under section 114A ibid can be imposed only if there is a willful suppression with an intention to evade payment of duty. We find that as far as the description of the goods, quantity, classification etc. are concerned, the importer is bound to state the truth in the Bill of Entry. As per section 46(4) of the Customs Act, 1962, the importer while presenting the Bill of Entry shall make and subscribe to a declaration as to the truth of such Bill of Entry. Further, Section 114A does not incorporate ‘intention to evade payment of duty’. This is because while mens rea is an essential or sine qua non for criminal offence it is not an essential element for imposing penalty for breach of civil obligations or liabilities, unless specifically stated so in the statute. Similarly, the importer is required to make a true declaration of the description and quantity of goods etc which have actually been imported and not just the goods as declared in the import documents. Thus, if the goods actually imported are more in number or the actual description or CTH as determined by an order under the Act is different from what is declared in the Bill of Entry, the importer would have made a mis-declaration. If this is done knowingly it’s a willful misstatement.

16. In Associated Cement Companies Ltd. Versus Commissioner Of Customs [2001 (128) ELT 21 (S.C.)], the Apex Court observed;

”52.Though it was sought to be contended that Section 28 of the Customs Act is in pari materia with Section 11A of the Excise Act, we find there is one material difference in the language of the two provisions and that is the words “with intent to evade payment of duty” occurring in proviso to Section 11A of the Excise Act are missing in Section 28(1) of the Customs Act and the proviso in particular.”

“with intent to evade payment of duty” hence is not an essential condition for evoking the extended time limit, if the statute so provides. The term statement has come to be used in a variety of formal narratives of facts, required by law, one such is a declaration of fact. Misstatement implies making of an incorrect statement or declaration with the knowledge that it was not correct, like in this case of declaring an incorrect CTH of the goods. The object behind enactment of Section 114A is to provide for a deterrent. It is meant to ensure payment of tax correctly and is a remedy for loss of revenue by a wilful breach of legal provisions especially in an era of self-assessment.

17. The ‘Self-Assessment’ procedure has been introduced in respect of Customs clearance of imported goods under Section 17 of Customs Act,1962, with effect from 08.04.2011. It is a provision resting on utmost good faith. Section 17(1) read as under at the relevant time:

Section 17. Assessment of duty. – (1) An importer entering any imported goods under section 46, or an exporter entering any export goods under section 50, shall, save as otherwise provided in section 85, self-assess the duty, if any, leviable on such goods.

Assessment means determination of the tax liability as set out by the legislature, in the Act provided for the same. The Customs assessment process includes determining the import permissibility in terms of the EXIM policy and any other laws regulating imports/exports, determining the classification, valuation and duties leviable on the goods to arrive at the duty liability, which is required to be paid by the importer – (Basic, Additional, Anti-dumping, Safeguards etc.) Assessment is hence the procedure whereby the duty leviable on the imported goods can be ascertained. Classification of goods is an important step in this process. Under the self-assessment procedure, it is the responsibility of the importer, to declare the correct facts in regard to the imported goods. Classify them under appropriate CTH and self-assess the goods correctly. Failure to do so could invite action as provided for under the Act.

18. The Appellant has referred to the following judgments in support of their stand that subsequent notices cannot be issued by alleging suppression or misstatement invoking the extended period of limitation.

a) P and B Pharmaceuticals Pvt. Ltd. v. Collector — 2003 (153) E.L.T. 14 (S.C.): The facts of the case are that a show cause notice was issued to the assessee proposing to demand duty on the basis of the price at which its distributor sold the goods in the course of whole sale trade on the ground that the said distributor was a related person. The assessee contended that so far as the demand of duty on the basis of the distributor being a related person is concerned, there has been no suppression of fact and all these facts were before the concerned authorities and part of earlier show cause notices, therefore, it was not open to the Central Excise authorities to invoke proviso to Section 11A of the Act for making a demand of duty for the extended period. The Hon’ble Supreme Court held that the necessary facts had been brought to the notice of the authorities at different intervals from 1985 to 1988 and further, they had dropped the proceedings accepting that the distributor was not a related person. It has been held that in such circumstances, it could not be said that there was any willful suppression or misstatement and that therefore, the extended period under Section 11A could not be invoked.

b) ECE Industries Ltd. v. Commissioner — 2004 (164) E.L.T. 236 (S.C.): The facts of the case are that a Show Cause Notice was issued to the assessee in 1991. It was for the period from July, 1987 to February, 1988. It appears that earlier in 1988 also a Show Cause Notice had been issued making a demand on a similar issue and for an identical amount. The Collector has given a categoric finding that the earlier Show Cause Notice raised a demand on a similar issue and for an identical amount. The Hon’ble Supreme Court held that once the earlier Show Cause Notice, on similar issue has been dropped, it can no longer be said that there is any suppression.

c) Nizam Sugar Factory v. Collector — 2006 (197) E.L.T. 465 (S.C.): The facts of the case was that the Department had issued a Show Cause Notice to the assessee demanding duty for the period 1978 to 1982 alleging that the assessee had cleared carbon dioxide without payment of duty to another unit in contravention of the Central Excise Rules, 1944 and without obtaining licence for manufacture of carbon dioxide in their factory; without filing Classification/Price List and without maintaining accounts. Assessee contended that impure carbon dioxide was not exigible to duty. The case was heard and thereafter no further action was taken in the matter. Subsequently the assessee was served with a second SCN alleging that the appellant was supplying carbon dioxide to another unit; that they had not taken necessary licence; had not followed the procedure prescribed under the rules; and had not discharged duty liability. The Hon’ble Supreme Court held that the allegation of suppression of facts against the appellant cannot be sustained, since when the first SCN was issued all the relevant facts were in the knowledge of the authorities. Later on, while issuing the second and third show cause notices the same/similar facts could not be taken as suppression of facts on the part of the assessee as these facts were already in the knowledge of the authorities.

19 A decision is a precedent on its own facts. Each case presents its own features. It has been held by the Apex Court in its judgment in the case of Collector of Central Excise, Calcutta v. M/s. Alnoori Tobacco Products and Anr. [Civil Appeal Nos.4502-4503 of 1998 decided on 21.07.2004], that circumstantial flexibility, one additional or different fact may make a world of difference between conclusions in two cases. It cited the following words of Lord Denning with approval:

“Each case depends on its own facts and a close similarity between one case and another is not enough because even a single significant detail may alter the entire aspect, in deciding such cases, one should avoid the temptation to decide cases (as said by Cordozo) by matching the colour of one case against the colour of another. To decide therefore, on which side of the line a case falls, the broad resemblance to another case is not at all decisive.”

We hence need to look into the matter in a little more detail. The fact of this case is that although there was a dispute in the classification of imported goods, the same came to be finalised by the Department. The procedure culminated in the issue of a speaking order determining the classification of the impugned goods under the Customs Act. Once a classification of imported goods is decided in a particular manner by an order of the proper officer passed under the Act it has to be honored till it is upset in appeal proceedings. If not it will create an impossible situation in which orders get disregarded and the department perpetually issue notice to the importer whose classification has been settled but who continues to knowingly mis-state / mis-classify the goods, thus deliberately assessing the goods in a manner that duty is short paid which is an undesirable situation.

19.1 Thus the issue of subsequent SCN’s in this case was necessitated only because the Appellant knowing the classification of goods as finalised by the proper officer, chose to misclassify it deliberately. It helped them wrongly get a financial advantage and bleed the exchequer by evading payment of tax. This distinguishes the matter from the facts in the case laws relied upon by the Appellant. In those cases, it was the department who dithered in finalizing the matter after issue of the first Show Cause Notice or after having done so in a particular manner chose to change the decision reopening the matter on the plea of suppression of facts. Here the cause of action in evoking section 114A is the deliberate misclassification resorted to by the Appellant in the Bill of Entry in spite of an order classifying the goods which is contrary to law and the self-declaration given in the Bill of Entry and are hence distinguished. A Division Bench of the Rajasthan High Court in Lalji Moolji Transport Company v. State of Rajasthan, [DBCWP No. 324/2002., dated: 10.4.2002 / [2002] 127 STC 365], after considering the judgments of the Hon’ble Supreme Court in R.S. Joshi v. Ajeet Mills, [AIR 1977 SC 2279], and State of Rajasthan v. D.P. Metal, 2001 (124) STC 611 (SC) has gone to the extent of stating that it would not be correct to protect a tax evader saying that there was absence of mens rea. The Court further held as under: –

“The requirement of law is meant to be strictly construed, particularly in areas of evasion of tax. We cannot lose sight of the fact that of the there are attempts to avoid statutory obligation or requirement for oblique reason. An undue indulgence and leniency in favour of the tax-evaders on technical or misplaced sympathetic grounds leads to serious consequence’s affecting the revenue, and as such, development and security of the State. We are not oblivious of the fact that the penalty provisions cannot be used as a revenue-yielding provision. The object to the penalty provision is to ensure compliance in the larger public interest.”

In this case willful misstatement of the CTH is evident.

19.2 Even if a matter is under appeal it does not mean that the legal stand of the importer which has been defeated in quasi-judicial proceeding can continue to be recognized as legitimate and duty short paid. A valid order determining the CTH of the imported goods and a statutory document filed for the same goods knowingly misstating the CTH cannot coexist legally and be recognised in law to be valid. It cannot be said that ordinary prudence has been exercised by the importer-appellant according to the standards of a compliant tax payer or even a reasonable person. It violates the undertaking given as mandated by section 46(4) of the Customs Act, 1962 in the Bill of Entry by the appellant which forms the foundation for the trust based self-assessment envisaged by the Act. The undertaking is meant to carry out the intent of the statute and accomplish the reasonable objectives for which it was passed and thus cannot be brushed off as being merely procedural.

19.3 We find from the series of appeals being considered in this order that the classification of ‘brush cutters’ was reclassified from CTH 84339000 to CTH 84672900 vide Order in Original No. 21310/2013 dated 17.7.2013 which has been upheld by the Commissioner (Appeals) vide Order in Appeal C. Cus. No. 434/2014 dated 10.3.2014. The appellant has however continued to classify ‘brush cutters’ under CTH 8433 9000. A seven judge Constitutional Bench of the Supreme Court in Smt. Ujjam Bai v. State of Uttar Pradesh, [1962 AIR 1621/ 1963 SCR (1) 778/ 1961 1 SCR 778] had an occasion to examine the binding force of a decision which is arrived at by a taxing authority. It held as under;

“..A taxing authority, which has the power to make a decision on matters falling within the purview of the law under which it is functioning is undoubtedly under an obligation to arrive at a right decision. But the liability of a tribunal to err is an accepted phenomenon. The binding force of a decision which is arrived at by a taxing authority acting within the limits of the jurisdiction conferred upon it by law cannot be made dependent upon the question whether its decision is correct or erroneous. For, that would create an impossible situation. Therefore, though erroneous, its decision must bind the assessee. Further, if the taxing law is a valid restriction the liability to be bound by the decision of the taxing authority is a burden imposed upon a person’s right to carry on trade or business. This burden is not lessened or lifted merely because the decision proceeds upon a misconstruction of a provision of the law, which the taxing authority has to construe. Therefore, it makes no difference whether the decision is right or wrong so long as the error does not pertain to jurisdiction.” (emphasis added)

Hence if an order or judgment has been passed on a lis between the department and an assessee, he is bound to follow that order, until it is upset in appeal by a higher judicial forum. The responsibility is more when the tax is self-assessed. This is not a mere failure to pay duty. It is something more. The Appellant has deliberately sought to defeat the provisions of law. Thereby contravening the provisions of Section 46(4) ibid. Further there is nothing in the section to mean that because there is knowledge by the Department of the earlier mis-classification of the goods by the Appellant the willful misstatement in the Bill of Entry subsequently which stands established disappears.

20. In Hardeep Singh v. State of Punjab, reported in 2014 (3) SCC 92, at Paragraphs 43, the Hon’ble Supreme Court held as follows:

“43. The court cannot proceed with an assumption that the legislature enacting the statute has committed a mistake and where the language of the statute is plain and unambiguous, the court cannot go behind the language of the statute so as to add or subtract a word playing the role of a political reformer or of a wise counsel to the legislature. The court has to proceed on the footing that the legislature intended what it has said and even if there is some defect in the phraseology etc., it is for others than the court to rectify that defect. The statute requires to be interpreted without doing any violence to the language used therein. The court cannot re-write, recast or reframe the legislation for the reason that it has no power to legislate.

21. The Hon’ble High Court of Madras in King Bell Apparels v. Commissioner of Central Excise, Salem [2019 (365) E.L.T. 681 (Mad.)] held that the contention that once knowledge has been acquired by the department, there is no suppression and the ordinary statutory period of limitation would be applicable was rejected as a fallacious argument inasmuch as once the suppression is established, merely because the department acquires knowledge of the irregularity, the suppression would not be obliterated. A statutory penalty flows from a disregard of statutory provisions. With relaxation in procedure in the clearance of goods comes greater responsibility on the part of importers. This responsibility has not been discharged and the impugned order hence merits to be upheld on this score.

22. Further it is seen that interest is necessarily linked to the duty payable, such liability arises automatically by operation of law. As per the Hon’ble Supreme Court’s judgment in Commissioner of Central Excise, Pune Vs M/s SKF India [2009-TIOL-82-SC-CX] interest is leviable on delayed or deferred payment of duty for whatever reasons.

23. Based on the discussions above we uphold the impugned orders as listed at column 5 of the Table at para 1 above. The appeals are disposed of on the said terms.

(Order pronounced in open court on 22.03.2024)