OVER VIEW ON TDS:

TDS or Tax Deducted at Source is income tax reduced from the money paid at the time of making specified payments such as rent, commission, professional fees, salary, interest etc. by the persons making such payments. Usually, the person receiving income is liable to pay income tax. But the government with the help of Tax Deducted at Source provisions makes sure that income tax is deducted in advance from the payments being made by you. The recipient of income receives the net amount (after reducing TDS). The recipient will add the gross amount to his income and the amount of TDS is adjusted against his final tax liability. The recipient takes credit for the amount already deducted and paid on his behalf.

Example:

Shine Pvt Ltd make a payment for office rent of Rs 80,000 per month to the owner of the property. TDS is required to be deducted at 10%. Shine Pvt ltd must deduct TDS of Rs 8000 and pay the balance of Rs 72,000 to the owner of the property. Thus, the recipient of income i.e., the owner of the property in the above case receives the net amount of Rs 72,000 after deduction of tax at the source. He will add the gross amount i.e., Rs 80,000 to his income and can take credit of the amount already deducted i.e., Rs 8,000 by shine Pvt ltd against his final tax liability.

Purpose of TDS:

TDS or Tax Deducted at Source is a critical tool for the purpose of Income Tax collection. By means of it, the government collects tax from a person’s income at the time it is generated. The primary objective of TDS is to reduce incidences of tax evasion by ensuring it is deducted at the source of income generation rather than at a future date.

Major tax related proposals in Budget 2023-2024:

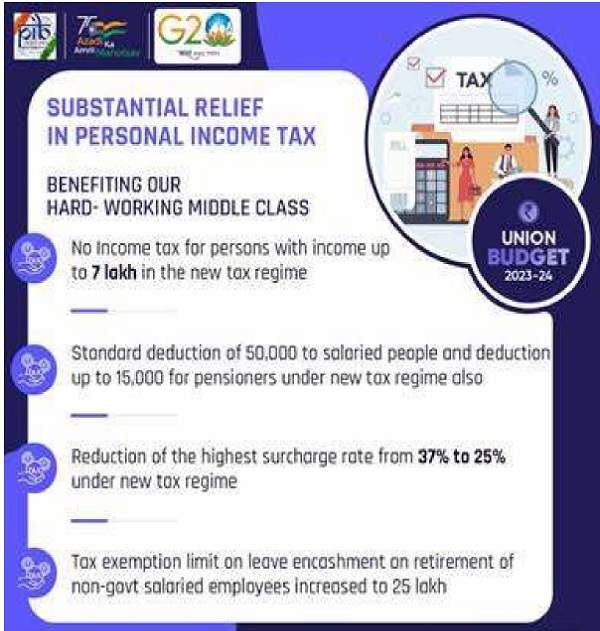

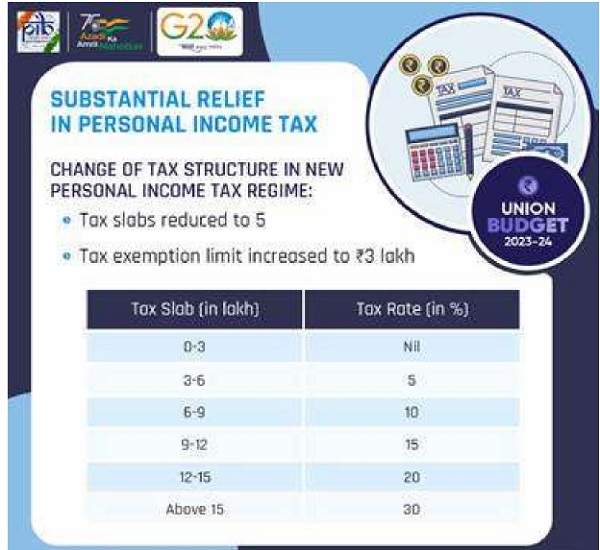

- There are five major announcements relating to the personal income tax. The rebate limit in the new tax regime has been increased to ₹ 7 lakh, meaning that peons in the new tax regime with income upto ₹ 7 lakh will not have to pay any tax. The tax structure in the new personal tax regime has been changed by reducing number of slabs to five and increasing the tax exemption limit to ₹ 3 lakh. This will provide major relief to all tax payers in the new regime.

Source: PIB

- The benefit of standard deduction has been extended to the salaried class and the pensioners including family pensioner under the new tax regime. Salaried individual will get standard deduction of ₹ 50,000 and pensioner ₹ 15,000 as per the proposal. Each salaried person with an income of ₹ 5 lakh or more will thus gain ₹ 52,500, from the above proposals.

- The highest surcharge rate in personal income tax has been reduced from 37% to 25% in the new tax regime for income above ₹2 crore. This would result in maximum tax rate of personal income tax come down to 39% which was earlier 42.74%.

- The limit of tax exemption on leave encashment on retirement of non-government salaried employees has been increased from ₹3 lakh to ₹25

- The new income tax regime has been made the default tax regime. However, the citizens will continue to have the option to avail the benefit of the old tax regime.

Source: PIB.

Budget 2023 and TDS:

- Section 194BA – Introduction of TDS on income from online gaming

- Section 196A – Starting April 1st, 2023, non-residents earning income from mutual funds in India can provide a Tax Residency Certificate to avail the benefit of TDS as per rate given in tax treaty, instead of 20%.

- Section 192A – TDS rate reduced to 20% from maximum marginal rate on PF withdrawal for employees who do not have PAN

- Section 193 – No exemption from TDS on interest from listed debentures. Therefore, tax has to be deducted on interest on such specified securities.

- Section 194N – TDS threshold has been increased on cash withdrawal by by co-operative societies. Starting April 1st, 2023, tax will be deducted on cash withdrawals by co-operative societies if the amount exceeds Rs 3 crore, instead of the previous limit of Rs 1 crore.

Budget 2022 and TDS:

- New Section 194S- A person is liable for Tax Deduction at Source (TDS) at 1% at the time of payment of the transfer of virtual digital assets.

- Sale of immovable property under Section 194-IA- It is proposed to amend the amount on which TDS should be deducted. The person buying the property should deduct tax at 1% on the sum paid/credited or the stamp duty value of such property, whichever is higher.

- New Section 194R- TDS at 10% should be deducted by any person who provides perks or benefits, whether convertible into money or not, to any resident for carrying out any business or profession by such resident.

Landmark Supreme Court rulings on TDS:

- Union of India vs. Tata Tea Co. Ltd. (1991): In this case, the Supreme Court held that TDS provisions apply only to payments made to residents and not to non-residents.

- Hindustan Coca-Cola Beverages Pvt. Ltd. vs. CIT (2007): The Supreme Court held that TDS cannot be levied on payments made to contractors for executing a works contract, as it does not fall under the category of “fees for technical services” or “professional services.”

- CIT vs. Bharat General Reinsurance Co. Ltd. (2007): The Supreme Court held that if tax is deducted at source, it has to be paid to the government within the prescribed time limit, regardless of whether the payee has actually received the payment or not.

- GE India Technology Centre Pvt. Ltd. vs. CIT (2010): In this case, the Supreme Court held that payments made by a resident to a non-resident for the use of software are not taxable as royalty under the Income Tax Act, and hence, TDS provisions do not apply.

- Commissioner of Income Tax vs. Vodafone Essar Gujarat Ltd. (2012): This is one of the most famous tax cases in India, in which the Supreme Court held that the transaction between Vodafone and Hutchison was not taxable in India, and hence, TDS provisions did not apply.

- Commissioner of Income Tax vs. Bharti Airtel Ltd. (2019): In this case, the Supreme Court held that TDS is not applicable on payments made by an assessee to a non-resident for the sale of pre-paid SIM cards and vouchers, as it does not fall under the category of “fees for technical services” or “professional services.”

CBDT Measures:

The Central Board of Direct Taxes (CBDT) has taken several measures in recent years to improve the Tax Deduction at Source (TDS) system in India. Here are some of the key measures:

1. TDS Reconciliation Analysis and Correction Enabling System (TRACES): The CBDT has developed TRACES, a web-based application to facilitate TDS compliance. It provides a platform for taxpayers to view their TDS status, file TDS returns, and verify TDS certificates.

2. Increased Penalty for Non-Compliance: The CBDT has increased the penalty for non-compliance with TDS provisions. Under the new rules, a penalty of up to Rs. 1 lakh can be levied for failure to deduct TDS or remit TDS to the government.

3. Rationalization of TDS Rates: The CBDT has rationalized the TDS rates for various payments. For example, in the 2021 budget, the TDS rate for non-filers of income tax returns was increased to 5%.

4. Use of Technology: The CBDT has encouraged the use of technology to improve TDS compliance. It has introduced a facility for e-filing of TDS returns, electronic payment of TDS, and electronic issuance of TDS certificates.

5. TDS Compliance Management Cell: The CBDT has set up a TDS Compliance Management Cell to monitor TDS compliance and take necessary action against defaulters.

These above measures of the Supreme court, CBDT, and the budget will improve the TDS system in India and boosts its economic growth.

How TDS promotes growth of Indian Economy:

The introduction of TDS has several benefits for the Indian economy, which are as follows:

1. Increased Tax Compliance: The implementation of TDS ensures that taxpayers are more compliant with the tax laws. The system provides a mechanism for the government to collect taxes on time and reduces the chances of tax evasion.

2. Steady Revenue Stream: The TDS system ensures that the government has a steady revenue stream throughout the year, which helps in planning and executing various projects and schemes.

3. Reduction in Black Money: The implementation of TDS helps in reducing the circulation of black money in the economy. The system ensures that tax is deducted at the source, which reduces the chances of unaccounted cash transactions.

4. Boosts Investment: The implementation of TDS promotes investment in the economy. It ensures that the government has a stable revenue stream, which enables it to undertake infrastructure projects, which in turn attracts more investment.

5. Encourages Formal Economy: TDS encourages the formal economy by promoting transparency and accountability in financial transactions. The system ensures that all financial transactions are recorded, and tax is deducted at the source, which promotes transparency and accountability.

6. Reduces Tax Evasion: TDS helps in reducing tax evasion by ensuring that the tax is deducted at the source. It acts as a deterrent to tax evaders who may otherwise try to underreport their income or avoid paying taxes altogether.

7. Helps Small Businesses: TDS can help small businesses as it provides a system for tax collection that is easy to understand and implement. It also helps in reducing the burden of tax compliance as the responsibility of deducting and remitting taxes is on the payer.

8. Reduces Tax Arrears: TDS ensures timely collection of taxes and reduces the chances of tax arrears. It also reduces the burden on taxpayers as they do not have to pay a lump sum amount at the end of the financial year.

9. Improves Credit Rating: The implementation of TDS can improve the credit rating of the country. It ensures that the government has a steady revenue stream, which helps in reducing the fiscal deficit and improving the credit rating.

10. Encourages Digital Payments: TDS promotes digital payments as it is easier to deduct and remit taxes electronically. This helps in reducing the circulation of cash and promotes transparency in financial transactions.

11. Provides Data for Policy Making: The TDS system provides valuable data for policy making. The data can be used to identify areas where tax compliance is low, and measures can be taken to improve compliance. The data can also be used to identify sectors that require policy interventions.

12. Promotes Fairness: TDS promotes fairness in taxation by ensuring that taxes are deducted at the source. It ensures that all taxpayers are treated equally, and the burden of tax compliance is shared among all taxpayers.

Why TDS is not so successful in India:

Reasons why TDS is not so successful in India:

1. Lack of Awareness: Many taxpayers, particularly small taxpayers, are not aware of the TDS provisions and how they apply to their income. As a result, they may not deduct or pay TDS even when required, leading to lower TDS collection.

2. Low Compliance: Some taxpayers who are aware of the TDS provisions may intentionally avoid or delay TDS deduction and payment to the government. This can be due to various reasons such as a lack of funds, poor cash flow, or a desire to avoid tax liabilities.

3. Complex Regulations: The TDS provisions in India are complex and involve a lot of paperwork and compliance requirements. This can be particularly challenging for small businesses and individuals who may not have the resources to comply with the regulations.

4. Low Penalty: The penalty for non-compliance with TDS provisions in India is relatively low compared to other countries. This can make it less of a deterrent for tax evaders to comply with the TDS provisions.

5. Limited Resources: The government agencies responsible for enforcing TDS regulations may not have enough resources, such as manpower and technology, to effectively monitor and enforce compliance.

6. High Exemptions: There are several exemptions available for TDS deductions, particularly for small taxpayers. This can reduce the number of taxpayers who are required to deduct TDS, leading to lower TDS collection.

7. Inadequate Systems: The existing systems for TDS collection, such as tax deduction and payment through banks, may not be adequate to handle the large volume of transactions in the Indian economy. This can lead to delays, errors, and other inefficiencies in TDS collection.

Comparison of Indian and Global TDS systems: Similarities between Indian TDS System and Global TDS System:

1. Purpose: The primary purpose of TDS is to ensure that tax is collected at the source of income. This is the same across the Indian TDS system and the global TDS system.

2. Coverage: TDS covers various types of income, including salaries, interest, dividends, rent, and royalty payments. This coverage is similar across the Indian TDS system and the global TDS system.

3. Compliance: TDS requires taxpayers to deduct tax from the payment they make to the recipient and deposit it with the government. This compliance requirement is similar across the Indian TDS system and the global TDS system.

Differences between Indian TDS System and Global TDS System:

1. Threshold Limits: The threshold limits for TDS deduction are different in India and other countries. In India, the threshold limit for TDS deduction is lower than most other countries, making it more burdensome for small

2. Exemptions: The exemptions for TDS deduction vary across different In India, there are several exemptions available, particularly for small taxpayers, which can reduce the number of taxpayers required to deduct TDS.

3. Rates: The TDS rates are different in India and other countries. In India, the TDS rates are generally higher than in other countries, making it more burdensome for taxpayers.

4. Penalty: The penalty for non-compliance with TDS regulations is different in India and other countries. In some countries, the penalty for non-compliance is much higher than in India, making it a more effective deterrent for tax evaders.

5. Procedures: The TDS procedures, including the documentation, filing, and payment requirements, are different in India and other countries. In some countries, the TDS procedures are simpler and more efficient, making it easier for taxpayers to comply with the regulations.

Way forward:

How to increase the TDS share in the total tax collections:

Ways to increase TDS collection in India:

1. Encourage Digital Payments: The government can promote digital payments by providing incentives such as cashback, discounts, and other rewards. This can encourage people to use digital payment modes, which will help in increasing TDS collection.

2. Increase Awareness: The government can increase awareness about TDS and its benefits through advertisements, seminars, and workshops. This will help in educating people about the importance of TDS and encourage them to comply with the tax laws.

3. Expand the Scope of TDS: The government can consider expanding the scope of TDS to include more sources of income such as capital gains, dividends, and royalties. This will help in increasing TDS collection and reducing tax evasion.

4. Reduce TDS Rates: The government can consider reducing TDS rates for certain types of income such as interest income for senior citizens or rental income for low-income households. This will encourage people to comply with the tax laws and increase TDS collection.

5. Introduce Penalty for Non-Compliance: The government can introduce penalties for non-compliance with TDS regulations. This will act as a deterrent to tax evaders and encourage people to comply with the tax

6. Use Data Analytics: The government can use data analytics to identify potential tax evaders and act against them. This will help in increasing TDS collection and reducing tax evasion.

7. Simplify TDS Procedures: The government can simplify TDS procedures to make it easier for taxpayers to comply with the tax laws. This will reduce the burden of tax compliance and encourage people to comply with the tax laws.

Conclusion:

In conclusion, The Indian government has set a target of achieving a 5 trillion-dollar economy by the year 2025. To achieve this target, it is essential to increase tax revenue, which can be done by strengthening the tax collection system, including the TDS system. TDS is a critical component of India’s tax system, and its importance will only increase as the country aims to achieve a 5 trillion-dollar economy. By strengthening the TDS system, the government can improve revenue collection, promote fiscal discipline, and encourage formalization of the economy, all of which will contribute to sustained economic growth.

****

The Author Can Be Reached At MAIL: swamyjustice@gmail.com

Author Bio