Case Law Details

In re Alleima India Private Limited (AAR Gujarat)

In a significant ruling, the Authority for Advance Rulings (AAR) in Gujarat has provided clarity on the applicability of GST on nominal charges deducted by employers for canteen services provided to employees. The case in question, involving Alleima India Private Limited, examines whether the recovery of a nominal amount from employees’ salaries for canteen facilities constitutes a ‘supply of service’ under the CGST Act, 2017, and whether Input Tax Credit (ITC) is available for the GST paid by the company to the canteen service provider (CSP).

Background:

Alleima India Private Limited, engaged in manufacturing and selling seamless stainless steel pipes, tubes, and high resistance wires, operates a manufacturing facility in Gujarat. Employing over 300 employees, the company is mandated by the Factories Act, 1948, to provide canteen facilities. Consequently, they have engaged a CSP to prepare and supply food, deducting a nominal amount of Rs. 104 per month from each employee’s salary for this service.

Key Questions Raised:

1. Is the nominal amount deducted from employees’ salaries for canteen facilities considered a ‘supply of service’ under the CGST Act, 2017?

2. If yes, is GST applicable on this nominal amount?

3. Is ITC available to the applicant for the GST charged by the CSP?

Applicant’s Contentions:

- The applicant argued that the canteen facility, being part of the employment contract, should not be considered a supply of goods/services and hence, not subject to GST.

- The applicant cited several rulings and circulars, including Circular No. 172/04/2022-GST, which clarified that perquisites provided to employees as part of their employment contract are not subject to GST.

- The nominal amount deducted from employees’ salaries is merely a transaction in money and does not qualify as ‘consideration’ for a supply.

- The canteen facility is provided as a statutory obligation under the Factories Act, 1948, and the company does not profit from it.

AAR’s Findings:

The AAR Gujarat meticulously examined the provisions of the CGST Act, 2017, relevant circulars, and past rulings cited by the applicant.

1. Supply of Service:

- The definition of ‘supply’ under Section 7 of the CGST Act includes all forms of supply made for a consideration by a person in the course of furtherance of business.

- However, Circular No. 172/04/2022-GST clarifies that perquisites provided by an employer to an employee under an employment contract are not considered a supply of goods/services.

2. GST Applicability:

- The AAR noted that the canteen service is provided in compliance with the Factories Act and is part of the employment contract.

- Therefore, the nominal amount deducted from employees’ salaries for canteen facilities is not a consideration for the supply of services but a statutory obligation, and hence, not subject to GST.

3. Input Tax Credit:

- The AAR referred to Section 17(5) of the CGST Act, which restricts ITC on food and beverages unless it is obligatory for an employer to provide the same to employees under any law.

- Given that the Factories Act mandates the provision of canteen facilities, the applicant is eligible to claim ITC on the GST paid to the CSP for canteen services.

Rulings Cited:

- circular no. 172/04/2022-GST

- Tata Motors Limited [GUJ/GAAR/R/39/2021]

- M/s Amneal Pharmaceuticals Ltd [GURGAAR/R/50/2020]

- Posco India Pune Processing Center Pvt Ltd [GST-ARA-36/2018-19/B-110] – Maharashtra

Conclusion

The AAR Gujarat’s ruling in the case of Alleima India Private Limited provides critical clarity on the applicability of GST on canteen facilities provided to employees. By ruling that the nominal amount deducted from employees’ salaries does not constitute a ‘supply of service’ and is not subject to GST, and that ITC is available for the GST paid to the CSP, the AAR has reinforced the principle that statutory obligations under employment contracts do not fall within the ambit of GST.

FULL TEXT OF THE ORDER OF AUTHORITY FOR ADVANCE RULING, GUJARAT

M/s. Alleima India Private Limited, [for short—`applicant’] is a company incorporated under the Companies Act, 2013, having its registered office at Pune. There manufacturing facility in Gujarat, located at Survey No 2118, Ahmedabad Mehsana Highway, Opp. Kalapi Hotel, Village Rajpur, Taluka Kadi, Mahesana, Gujarat, 384440., is registered under GST and their GSTIN is 24ABBCS6573P1ZQ.

2. The applicant is engaged in the business of manufacturing and selling of seamless stainless steel pipes and tubes along with high resistance wires. They also render R & D services. The applicant states that they have employed more than 300 employees and are also registered under the Factories Act, 1948.

3. The applicant further states that they have engaged a canteen service provider [CST)] for preparing and supplying food to their employees. The applicant recovers Rs. 104/- on monthly basis from each employee in respect of the food being prepared and supplied by the CSP.

4. Further, the applicant states that in terms of section 46 of the Factories Act, 1948, since they have employed more than 300 employees, they are mandated to provide canteen for their employees; that they have ultimate control over the affairs of the factory & would be considered as an ‘occupier’, that they have set up a canteen facility having a separately demarcated area in the factory premises pursuant to & in compliance with the Factories Act; that the canteen facility has seating area with tables and chairs, cooking facility with utensils, refrigeration, storage rooms for keeping the cooked food, washrooms and wash basin, etc..

5. The applicant has attached a copy of agreement executed with the CSP and copy of sample invoice as Annexure 1 and Canteen Policy as Annexure 2 with their application.

6. The applicant has further contended as follows:

No GST on canteen facility

- that the detail of food consumed & details of employee is maintained by the applicant; that based on the record of food consumed, the CSP raises an invoice; that after termination of employment services, the employee is not allowed access to canteen facilities;

- that deduction of the nominal amount from employees would become taxable under GST only if such amount qualifies as ‘consideration’ towards supply as defined u/s 7 of the CGST Act, 2017;

- that in terms of Schedule-III, services by an employee to employer in the course of or in relation to his employment, is not treated as a supply of goods/services;

- that any consideration by the employer to the employee on account of the activities undertaken under the contract of employment is out of the scope of GST; that an activity undertaken in the course of an employment relationship would be outside the scope of GST;

- that in terms of circular no. 172/04/2022-GST dated 6.7.22, it is clarified that any perquisite provided to employees as part of employment contract is not subject to tax under GST;

- that the applicant provides canteen facility in terms of contractual agreement entered between the employer and employee; that the contractual agreement specifically provides for availment of benefits and allowances which includes canteen services to employees;

- that in terms of section 7, ibid, the below mentioned criteria plays a crucial role to determine GST implications viz

- that there should be a legal intention of both parties to supply & receive the goods;

- it should involve quid-pro-quo;

- the supply of goods or services or both shall be affected by a person in the course of furtherance of business;

- that deduction of employee’s salary towards food availed by employee would constitute a transaction in money between applicant & its employees & would not attain the character of `consideration’;

- that there is no reciprocity/quid-pro-quo between applicant and its employees;

- that the activity does not fall within the ambit of business as defined u/s 2(17) of CGST Act, 2017;

- that unless there is evidence that applicant had intention of undertaking business & earning profit in relation to provision of canteen facilities, it cannot be construed to be in the course of furtherance of business;

- that they would like to rely on the below mentioned rulings/circular which substantiate their averment that no GST is leviable;

- circular no. 172/04/2022-GST dated 6.7.22;

- M/s Tata Motors Limited [GUJ/GAAR/R/39/2021];

- Bai Mumbai Trust and Others vs. Suchitra and others reported at [2019-VIL-454 BOM];

- M/s. Amneal Pharmaceuticals Ltd [GURGAAR/R/50/2020 I;

- M/s. SRF Limited [GURGAAR/R/41/2022];

- Posco India Pune Processing Center Private Limited [GST-ARA-36/2018-19/B-110] – Maharashtra;

- M/s Jotun India Pvt Ltd [GST-ARA-19/2019-20/B-108]- Maharashtra;

- M/s. Cadila Pharmaceuticals Ltd [GURGAAR/R/2023/14];

- M/s. TATA Autocomp Systems Limited [GUJ/GAAR/ 2023/231;

- M/s. Emcure Pharmaceuticals Ltd [GST-ARA-119/2019-20/13-03 dated 4.1.221.

ITC of the GST paid by the applicant to CSP

- that credit of ITC charged on supply of services would only be allowed when such goods or services or both are used or intended to be used in the course of furtherance of business;

- that the CSP provides the services to the applicant in the preparation of food and maintenance of canteen premises, for the applicant’s employees; that such services are provided in pursuance of applicants obligation to provide such facilities to its employees in the capacity of an occupier of the factory under the Factories Act;

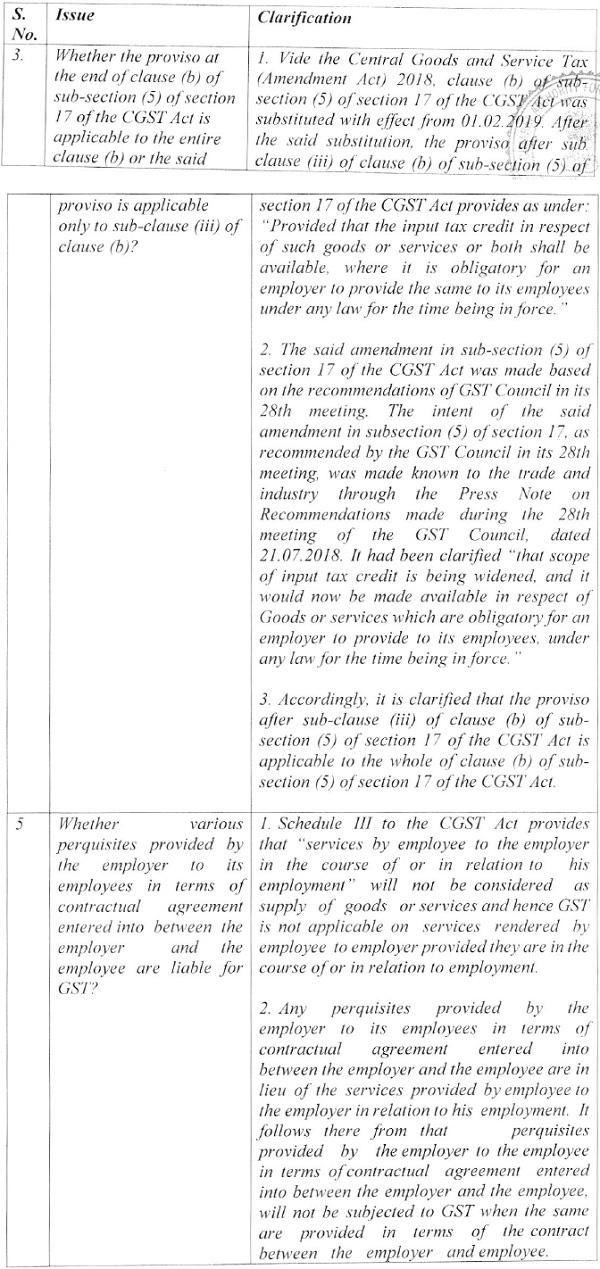

- that in terms of circular no. 172/04/2022-GST dated 6.7.22, it is clarified that the proviso at the end of clause (b) of section 17(5), ibid, is applicable to the entire clause 17(5)(b), ibid;

- the circular clarifies that ITC on food & beverages, etc., covered u/s 17(5), would not be restricted provided it is obligatory for an employer to provide the same to its employees under the law;

- that they would like to rely on the below mentioned rulings/circular which substantiate their averment that applicant is eligible to avail ITC on input service of canteen;

- circular no. 172/04/2022-GST dated 6.7.22;

- M/s Bharat Oman Refineries reported at 2021-TIOL-36-AAAR-GST;

- M/s Hindustan Coca Cola Beverages Pvt. Ltd. v/s CCE- Appeal No. E/89199/2013 & E/85728/2014;

- Cema Electric Lighting Products India Private Limited Vs. CCE, Appeal No. E/787/2012, reported in 2015 (37) STR 718 (Guj.);

- M/s Tata Motors Limited [GUJ/GAAR/R/39/2021];

- M/s. Cadila Pharmaceuticals Ltd [GURGAAR/R/2023/14];

- TATA Autocomp Systems Ltd [GURGAAR/R/2023/23]

7. In view of the foregoing, the applicant has filed this application, seeking advance ruling on the below mentioned questions viz

i. Whether the deduction of a nominal amount by the Applicant from the salary of the employees who are availing the facility of food provided in the factory premises would be considered as a “Supply of Service” by the Applicant under the provisions of Section 7 of Central Goods and Service Tax Act, 2017 and Gujarat Goods and Service Tax Act, 2017?

ii. In case answer to above is yes, whether GST is applicable on the nominal amount to he deducted from the salaries of employees?

iii. Whether ITC to the extent of cost borne by the applicant is available, to the Applicant on GST charged by the Canteen Service Provider for providing the catering services?

8. Personal hearing was granted on 28.5.2024 wherein Shri Mohit Airan, Shri Niraj Doshi, Shri Ahok Jani and Shri Nirav Shah, appeared and reiterated the facts as stated in the application.

Discussion and findings

9. At the outset, we would like to state that the provisions of both the CGST Act and the GGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provisions under the GGST Act.

10. We have considered the submissions made by the applicant in their application for advance ruling as well as the submissions made during the course of personal hearing. We have also considered the issue involved, the relevant facts & the applicant’s submission/interpretation of law in respect of question on which the advance ruling is sought.

11. Before adverting to the submissions made by the applicant, we would like 1.0 reproduce the relevant provisions/circular for ease of reference:

- Section 7. Scope of –

(1) For the purposes of this Act, the expression —

“supply” includes-

(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business;

[(aa) the activities or transactions, by a person, other than an individual, to its members or constituents or vice-versa, for cash, deferred payment or other valuable consideration.

Explanation .-For the purposes of this clause, it is hereby clarified that, notwithstanding anything contained in any other law for the time being in force or any judgment, decree or order of any Court, tribunal or authority, the person and its members or constituents shall be deemed to be Iwo separate persons and the supply of activities or transactions inter se shall be deemed to take place from one such person to another,]

(b) import of services for a consideration whether or not in the course or furtherance of business; 2[and]

(c) the activities specified in Schedule I, made or agreed to he made without a consideration; 3 [****]

(d) 4f* * * *

5 [(1A) where certain activities or transactions constitute a supply in accordance with the provisions of sub-section (1), they shall be treated either as supply of goods or supply of services as referred to in Schedule

(2) Notwithstanding anything contained in sub-section (1),-

(a) activities or transactions specified in Schedule III; or

(b) such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council. shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to the provisions of6[sub-sections (1), (IA) and (2)], the Government may, on the recommendations of the Council, specify, by notification, the transactions that are to be treated as –

(a) a supply of goods and not as a supply of services; or

(b) a supply of services and not as a supply of goods.

- Section 17. Apportionment of credit and blocked credits.- [relevant extracts]

5) Notwithstanding anything contained in sub-section (1) of section 16 and sub-section (1) of section 18, input tax credit shall not be available in respect of the following, namely:-

21(a)………;

(aa)………….;

(ab) ………..’

(b) 3[the following supply of goods or services or both-

(i) food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, leasing, renting or hiring of motor vehicles, vessels or aircraft referred to in clause (a) or clause (aa) except when used for the purposes specified therein, life insurance and health insurance:

Provided that the input tax credit in respect of such goods or services or both shall be available where an inward supply of such goods or services or both is used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply;

(ii) membership of a club, health and fitness centre; and

(iii) travel benefits extended to employees on vacation such as leave or home travel concession:

Provided that the input tax credit in respect of such goods or services or both shall be available, where it is obligatory for an employer to provide the same to its employees under any law for the time being in force.]

- CBIC’s press release dated 10.7.2017

Another issue is the taxation of perquisites. It is pertinent to point out here that the services by an employee to the employer in the course of or in relation to his employment is outside the scope of GST (neither supply of goods or supply of services). It .follows therefrom that supply by the employer to the employee in terms of contractual agreement entered into between the employer and the employee, will not be subjected to GST. Further, the input tax credit (ITC) scheme under GST does not allow ITC of membership of a club, health and fitness centre [section 17 (5) (b) (ii)]. It follows, therefore, that if such services are provided free of charge to all the employees by the employer then the same will not be subjected to GST, provided appropriate GST was paid when procured by the employer. The same would hold true for five housing to the employees, when the same is provided in terms of the contract between the employer and employee and is part and parcel of the cost-to-company (C2C).

12. The facts having been enumerated supra we do not intent to repeat the same for the sake of brevity.

13. The first issue to be decided is whether the deduction of a nominal amount made by the applicant from the salary of the employees who are availing the facility of food provided in the factory would be considered as a ‘supply’ of services by the applicant under the provisions of section 7 of the CGST Act, 2017. Now, in terms of Section 7 of the CGST Act, 2017, supply means all forms of ‘supply’ of goods/services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. The exception being Schedule-I, which includes the activities made or agreed to be made without a consideration and Schedule-III, which includes activities which shall be treated neither as a supply of goods or services. The applicant’s case is that they employ more than 300 employees who have been provided with canteen facility in terms of section 46 of the Factories Act, 1948. The applicant’s primary role is that he provides a demarcated space and that the amount is paid by him to the CSP [a part of which is collected from the employees] on behalf of the employees.

14. Now in terms of circular no. 172/04/2022-GST dated 6.7.22, it is clarified that perquisites provided by the ’employer’ to the ’employee’ in terms of contractual agreement entered into between the employer and the employee, will not be subjected to GST when the same are provided in terms of the contract between the employer and employee. We find that factually there is no dispute as far as [a] the canteen facility is provided by the applicant as mandated in section 46 of the Factories Act, 1948 is concerned; and [b] the applicant has provided copy of the HR policies for canteen facility to employees wherein it is stated as follows:

“Policy Highlights

a. This policy gives the guidelines for the canteen facilities provided to the employees of the company.

b. Subsidized canteen facility will be provided to all employees of the company as per this policy guidelines at Gujarat (Mehsana) location.

c. The cost of the canteen deduction is as per employee category.

d. The Canteen Committee will be the administrative in charge of the canteen who will have interactions with the Canteen Manager for the smooth functioning of the canteen service.

Canteen Facility Guidelines:

a. Canteen facilities will be provided to all employees of the company.

b. The menu for the week will be decided and communicated to the Canteen contractor by the Canteen Committee and the same will be displayed on the board for everyone’s knowledge.

c. This is a subsidized canteen facility and certain amount will he deducted, the salary every month .from all employees who are availing the facility.

d. There will be a monthly meeting on the canteen service with the Canteen contractor and Canteen committee. The communication of the meeting outcome will be communicated to the concerned by the committee.

e. Canteen contractor ensures the of the raw material and storage at the proper place with proper housekeeping and pest control measures. FIFO system should be adopted to ensure consumption of raw material in the right manner.

f. Canteen contractor and maintenance team should have common observation round in the canteen for the equipment’s and the facilities provided to the canteen contractor are used properly and maintained as per the guidelines.

g. The canteen committee and in-charge should ensure the medical check and hygiene of the canteen staff regularly.

h. The canteen timetable should be communicated and displayed at the proper location in the canteen.”

In view of the foregoing, we hold that the deduction of nominal amount made by the applicant from the salary of the employees who are availing the facility of food provided in the factory premises would not be considered as a ‘supply’ under the provisions of section 7 of the CGST Act, 2017.

15. Since the answer to the above is not in the affirmative, the ruling sought in respect of the second question is rendered infructuous.

Input Tax Credit

16. The next question on which the applicant has sought ruling is whether Input Tax Credit of GST charged by the CSP would be eligible for availment to the extent of cost borne by the applicant. In this connection, before proceeding further, certain factual aspects which we would like to mention, though at the cost of repetition are viz

- that they employ more than 300 employees at their factory;

- that section 17(5)(b) ibid, was amended on 1.2.2019, and is reproduced supra;

- that the applicant is mandated vide section 46 of the Factories Act, 1948 to provide canteen facility to its employees within the factory premises to provide canteen facility to its employees;

- that circular no. 172/04/2022-GST dated 6.7.22, clarifies that post substitution, effective from 1.2.2019, based on the recommendation of the GST council in its 28th meeting, the proviso after sub clause (iii) of clause (b) of section 17(5) of the CGST Act, 2017 is applicable to the whole of clause 17(5)(b),

17. In view of the foregoing, we hold that Input Tax Credit will be available to the applicant in respect of food and beverages as canteen facility is obligatorily to be provided under the Factories Act, 1948, read with Gujarat Factories Rules, 1963 as far as provision of canteen service employees working at the factory is concerned. It is further held that the ITC on GST charged by the canteen service provider be restricted to the extent of cost borne by the applicant only. Our substantiated by the Ruling of the Gujarat Appellate Authority for Advance Ruling order No. GUJ/GAAAR/Appeal/2022/23 dated 22.12.2022 in the case of M/s. Tata Motors Ltd, Ahmedabad.

18. In view of the foregoing, we hold that Input Tax Credit will be available to the appellant in respect of food and beverages as canteen facility is obligatorily to be provided under the Factories Act, 1948, read with Gujarat Factories Rules, 1963 as far as provision of canteen service for employees in factory is concerned.

19. In the light of the foregoing, we rule as under:

RULING

i. The deduction of nominal amount made by the applicant from the salary of the employees who are availing the facility of food provided in the factory premises would not be considered as a ‘supply’ under the provisions of section 7 of the CGST Act, 2017 and the GGST Act, 2017.

ii. Since the answer to the above is not in the affirmative, the ruling sought in respect of the second question is rendered infructuous.

iii. Input Tax Credit (ITC) will be available to the applicant on GST charged by the service provider in respect of canteen facility provided to its employees working in their factory, in view of the provisions of section 17(5) (b) as amended effective from 1.2.2019 and clarification issued by CBIC vide circular no. 172/04/2022-GST dated 6.7.2022 read with provisions of section 46 of the Factories Act, 1948 and read with provisions of Gujarat Factory Rules, 1963. ITC on the above is restricted to the extent of the cost borne by the applicant for providing canteen services to its permanent employees, but disallowing proportionate credit to the extent embedded in the cost of goods recovered from such employees.