Acquisition of Ambuja Cements and its subsidiary ACC by the Adani Group from a Swiss building material major – Holcim, has been the talk of the industry since a while. While addressing to the investors, the Holcim CEO Jan Jenisch stated that, “According to our analysis, it is a tax-free transaction.” Since then the industry has been much anxious about the design and structure of this tax-free acquisition worth USD 6.38 billion nailed by Adani Group. Through this article, we aim to uncover the probable rationale and takeaways from this acquisition, for which we need to first understand the ownership structure of both the groups – Holcim and Adani.

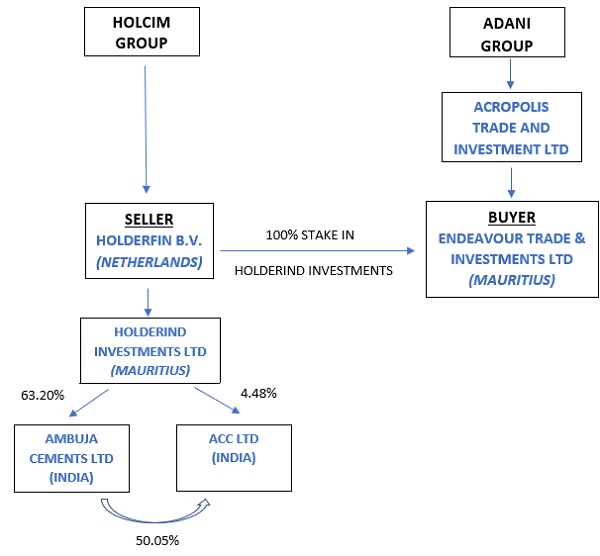

Thus, this transaction involves sale of a Mauritius Company (Holderind Investments Ltd) holding shares of Indian Listed Companies (Ambuja & ACC), by a Netherlands based Company (Holderfin B.V.) to another Mauritius Company (Endeavour trade & Investments Ltd). The shares of Mauritius based Company – Holderind Investments Ltd substantially derive their value from Indian assets i.e. shares of Ambuja & ACC. The change in the ownership of the holding company of Ambuja and ACC (being Holderind Investments Ltd) also indirectly tantamounts to transfer of ownership of these Indian Companies to another Mauritius based company – Endeavour Trade & Investments Ltd. Such an indirect transfer of shares of an Indian Company is taxable vide Explanation 5 to section 9(1)(i) of the Income-tax Act, 1961.

Addressing the taxability under the Tax Avoidance Treaties, it will be pertinent to analyze as to which treaty will be applicable here. The income of the Netherlands Seller (Holderfin B.V.) shall be taxable under the Indian Domestic Laws and hence, by virtue of it being a Netherlands resident, it can avail the benefits of India-Netherlands Double Tax Avoidance (DTAA). As per section 90(2) of the Act and various Apex Court judgements, it is very settled that, the beneficial provisions of the DTAA override the provisions of domestic laws. Article 13 of this DTAA addresses the taxing rights of both countries in context of income in the nature of capital gains. To be precise, paragraph 5 of Article 13 of the India – Netherlands DTAA is applicable to the transaction in hand. The said Article 13(5) reads as under –

“5. Gains from the alienation of any property other than that referred to in paragraphs 1, 2, 3 and 4 shall be taxable only in the State of which the alienator is a resident.

However, gains from the alienation of shares issued by a company resident in the other State which shares form part of at least a 10 per cent interest in the capital stock of that company, may be taxed in that other State if the alienation takes place to a resident of that other State. However, such gains shall remain taxable only in the State of which the alienator is a resident if such gains are realised in the course of a corporate organisation, reorganization, amalgamation, division or similar transaction, and the buyer or the seller owns at least 10 per cent of the capital of the other.”

Properties referred to in paragraphs 1 to 4 are – Immovable property, movable property forming a part of a PE, ships or aircrafts and unlisted shares of India or Netherlands who derives its value in principal from immovable property in that other state. The property involved in this case does not falls under any of these categories.

Probable rationale behind selling through a Netherlands entity –

1. Hence, by referring to Article 13(5) we can conclude that the right to tax is with the state where the seller is a resident i.e. Netherlands in our case. Speaking about the domestic tax laws of Netherlands, Netherlands levies no tax on capital gains which results in a net zero tax transaction because of the beneficial provision of India – Netherlands DTAA.

2. Had the sale been taken place through a Mauritius entity, India – Mauritius DTAA would have been applicable. Paragraph 3A of Article 13 of India – Mauritius DTAA gives taxing rights to that country, where the company whose shares are being sold is a resident i.e. India (Ambuja & ACC are Indian tax residents). Hence, India – Mauritius DTAA would have resulted in transaction being taxed under the purview of the Indian Income-tax Act.

Probable rationale behind buying through a Mauritius entity –

1. However, Article 13(5) further mentions an exception that, if the shares of an Indian Company (where shares sold are >10%) are being sold to an Indian resident, the taxing rights are given to India. Since the buyer here is Endeavour Trade & Investments Ltd, a Mauritius based Company, this exception is also not applicable. This is how, this buyer and seller structure resulted in a tax-free acquisition.

Implications under the India – Netherlands MLI –

The entire ground for claiming the transaction as tax-free revolves around the India – Netherlands DTAA. Therefore, the seller might be required to establish its eligibility to claim the benefits granted in the India – Netherlands DTAA in light of the fact that India and Netherlands have also signed a Multi-Lateral Instrument to prevent treaty abuse. Articles of the MLI mentioned in the ensuing paragraphs might act as a roadblock for this tax-free structure –

1. Article 6: Amends the preamble to India – Netherlands DTAA to clarify that the intent of the DTAA is to eliminate double taxation without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance (including through treaty-shopping arrangements aimed at obtaining reliefs provided in the Convention for the indirect benefit of residents of third jurisdictions).

2. Article 7: As per the principle purpose test, the benefit of DTAA shall not be available where having regard to all relevant facts and circumstances, it is reasonable to conclude that obtaining that benefit of the DTAA was one of the principal purposes of any arrangement or transaction that resulted directly or indirectly in that benefit unless it is established that granting that benefit in these circumstances would be in accordance with the object and purpose of the relevant provisions of the DTAA.

Holderfin B.V may accordingly be required to demonstrate before the Indian Tax Authorities that the case is not that of Treaty shopping and that the grant of treaty benefit in the present case is in accordance with the object and purpose of the India-Netherland DTAA.

Authors –

1. Priyanka Hotchandani – priyankahtn26@gmail.com

2. Chintan Rachh – chintanrachh02@gmail.com