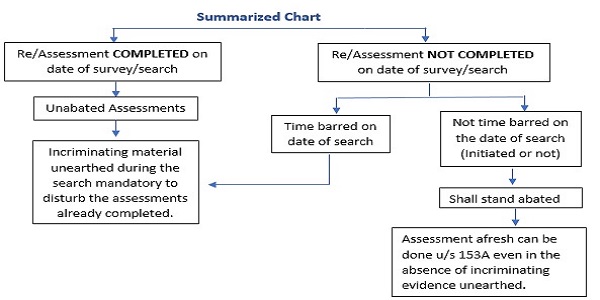

On the conclusion of search/survey, the assessment of preceding 6 years is reopened u/s 153A. As per the plain reading of 153A, the assessments earlier made in respect of these years stand abated i.e. shall stand nullified and new proceedings afresh would be done u/s 153A again. However, it is only the assessment / reassessment proceedings that are pending on the date of conducting search u/s 132 shall stand abated and all the proceedings carried out by the AO in respect to that incomplete assessments/reassessments shall stand nullified in the midway itself. The unabated proceedings are the ones which have attained finality i.e. either assessment / reassessment order have been passed or the proceedings have become time barred. Once it is held that the assessment has attained finality, then the Assessing Officer while passing the independent assessment order under section 153A could not have disturbed the assessment / reassessment order which has attained finality, unless the materials gathered in the course of the proceedings under section 153A establish that the reliefs granted under the finalised assessment / reassessment were contrary to the facts unearthed during the course of 153A proceedings. If there is no incriminating evidence on record to suggest that any material was unearthed during the search or during the 153A proceedings, the AO while passing order under section 153A read with section 143(3) cannot disturb the assessment order. This legal principle was established by landmark judgements of Hon’ble Bombay High Court in CIT v. Continental Warehousing Corporation (Nhava Sheva) Ltd. [2015] 58 taxmann.com 78 and CIT v. Murli Agro Products Ltd. [2014] 49 taxmann.com 172.

Therefore it would be of immense importance to determine as to what all is included in the scope of incriminating material. It would be highly illogical to presume that any premises would not be found with any document or material. Documents and materials related to business operations in the ordinary course are bound to be present. And hence, every document seized in search cannot be termed as incriminating. A document seized partakes the nature of incriminating material relevant for making assessment u/s 153A only when it is established that the transaction is undisclosed or unexplained and the income earned out of such transaction has escaped the scope of taxation while it should have been assessed to tax had it been disclosed in the right manner. Incriminating material need not necessarily be something tangible. It not only includes any assets, documents, entry in books of accounts, etc, but also any information stored in electronic form or any confession by a person relating to escapement of income. There are a number of case laws establishing the meaning and scope of incriminating material.

1. A Statement recorded u/s 132(4): A statement recorded u/s 132(4) has evidentiary value but cannot justify the additions in the absence of corroborative material. The statement also cannot, on a standalone basis, constitute ‘incriminating material’ so as to empower the AO to frame a block assessment u/s 153A. [PCIT v. Anand Kumar Jain (HUF)[2021] 432 ITR 384 (Delhi HC)]

2. Loose papers without date and narration: During search, certain loose papers containing bifurcation of the consideration payable for the flat purchased by the assessee in cash and cheque. The Tribunal held that since the impugned seized papers are undated, have no acceptable narration and do not bear the signature of the assessee or any other party, they are in the nature of dumb documents having no evidentiary value and cannot be taken as a sole basis for determination of undisclosed income of the assessee. When dumb documents like the present loose sheets of papers are recovered and the Revenue wants to make use of it, the onus rests on the Revenue to collect cogent evidence to corroborate the noting therein. Further, no circumstantial evidence in the form of any unaccounted cash, jewellery or investments outside the books of account was found in course of search in the case of assessee. Thus, the impugned addition was made by the AO on grossly inadequate material or rather no material at all and as such, deserves to be deleted. [ITO Vs Kranti Impex Pvt. Ltd. ITA No. 1229/Mum/2013 (Mum ITAT)]

3. Material found in 1st search for framing assessment under 2nd search: The seized or incriminating documents found during the 1st search could have only used for the purpose of assessment and reassessment u/s 153A for the stipulated 6 assessment years; and if not then its fate ends there. If the department has not made an assessment in pursuance to the first search, material found during the course of the said first search cannot be used in respect of the assessment years relating to and in consequence of the ‘second’ search. [ACIT v. Prakash Industries Ltd. ITA No. 4039/Delhi/2017 (Delhi ITAT)]

4. Regular Books of Accounts & Audit Report of the Assessee: By no stretch of imagination can the Revenue treat the regular books of accounts like cash and bank book, ledgers, audit report, TALLY accounting software found during the search as incriminating material. The AO had thoroughly examined the books of accounts during the assessment u/s 143(2). [PCIT v. Param Diary Ltd. ITA No. 37/2021 (Delhi HC)]

5. Documents relating to transactions duly recorded in books: Purchases of land reflected in the seized sale deeds duly recorded in the regular books of account, documents seized relating to same during the course of search cannot be considered as incriminating material, enabling AO to proceed under section 153A. [Lord Krishna Dwellers P. Ltd. v. DCIT ITA No. 5294/Del/2013 (Delhi ITAT)]

6. Assessee’s confession about undisclosed income later retracted: The partner of the Assessee firm in his sworn statement during the survey confessed about the undisclosed income, but later retracted from his statement saying that the he was new to the management of the Assessee firm and hence wasn’t yet fully acquainted. The Apex Court held that, statement obtained under survey would not automatically bind upon the assessee and addition made solely on the basis of such statement is unsustainable. [CIT v. S. Khader Khan Son 352 ITR 480 (SC)]

Well explained!!

Thanks!