RBI keeps key interest rates unchanged

Per transaction limit of IMPS transactions increased to Rs 5 lakhs

Real GDP projected to grow at 9.5% (FY 2021-22)

Measures to support small businesses, unorganized sectors, digital payments in remote areas announced

RBI has kept the key lending rate – Repo Rate unchanged at 4 per cent for the 8th time in a row. The Reverse Repo Rate also remains unchanged at 3.35 per cent. Announcing the decisions of the six-member Monetary Policy Committee, RBI Governor Shaktikanta Das said the GDP forecast for FY 2021-22 is 9.5 per cent.

Governor Das further said “the MPC has also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and to continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target”.

The Governor also shared various measures taken by the RBI since the onset of pandemic to support the growth and recovery of the economy. He informed that the RBI has injected Rs. 2.37 Lakh Crore liquidity into the financial system through Open Market Operations, in the first 6 months of FY 2021-22. This is against the Rs. 3.1 lakh crore injected during the full financial year 2020-21.

Shri Shaktikanta Das announced additional measures to support small businesses and unorganized sectors. They include:

1. Increasing IMPS (Immediate Payment Service Transaction) per transaction limit from Rs. 2 lakhs to Rs. 5 lakhs, to enhance customer convenience, enabling instant domestic fund transfer 24 x 7.

2. Extension of Rs. 10,000 crore On-Tap Special Liquidity Long Term Repo Operations (SLTRO) for small finance banks, till December 31, 2021

3. Introduction of pan-India Framework for Retail Digital Payment Solutions in offline mode, for areas with little or scarce internet access

4. IMPS Transaction Limit to be increased from Rs. 2 Lakh to Rs. 5 Lakh

5. Geo-tagging of all existing and new payment system touchpoints, to expand reach of payments acceptance infrastructure

6. New fraud prevention cohort in RBI’s Regulatory sandbox, to provide further impetus to fintech ecosystem

7. Continuation of Enhanced Ways and Means Advance Limits and liberalized overdraft measures for states, till March 31, 2022

8. Continuation of classifying bank lending to NBFCs as priority sector lending, till March 31, 2022

9. Internal Ombudsman Scheme for NBFCs with higher customer interface, to strengthen internal grievance redress mechanism

The Governor assured that the additional measures announced today will support small businesses and unorganized sector entities, will be helpful in remote areas with little or no internet connectivity, will expand reach of digital payments, will provide further impetus to fintech ecosystem and ensure continuous innovation in fintech.

As a relief to the States and UTs, RBI has also extended the interim enhancement of Ways and Means Advance (WMA) limits of Rs. 51,560 Crore up to March 31, 2022. “This is to help states/UTs manage cashflow amidst continued uncertainties on account of the pandemic,” he remarked.

“Consumer Price Index (CPI) inflation is moderating,” said the Governor, noting that the measures taken by the government are helping to contain volatility in vegetable prices.

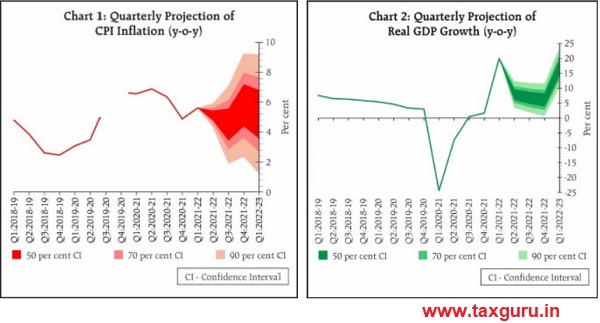

CPI inflation for 2021-22 projected at 5.3%

Q2 – 5.1%

Q3 – 4.5%

Q4 – 5.8%

Q1 (of 2022-23) – 5.2%

Real GDP projected to grow at 9.5% for FY 2021-22

Q2 – 7.9%

Q3 – 6.8%

Q4 – 6.1%

Q1 (of 2022-23) – 17.2%

The Governor also gave confidence in being able to meet our export target of $ 400 Billion during FY 2021-22 as exports have remained above $ 30 US Billion in September 2021, for the seventh consecutive month.

The Governor said that the conduct of Monetary Policy in India will continue to be oriented to the domestic circumstances. “We must not rest in the glory of what has been achieved, but work tirelessly on what remains to be done”. The Governor called for combined efforts of all sectors in order to support the economy. “Overall, aggregate demand is improving but slack still remains; output is still below pre-pandemic level and the recovery remains uneven and dependent upon continued policy support”, he observed.

The full text of the Governor’s statement can be found here. Watch the address here. The monetary policy statement of the Monetary Policy Committee can be found here.

******

Reserve Bank of India

Date : Oct 08, 2021

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) liquidity measures; (ii) payment and settlement systems; (iii) debt management; and (iv) financial Inclusion and customer protection.

I. Liquidity Measures

1. On Tap Special Long-Term Repo Operations (SLTRO) for Small Finance Banks (SFBs) Small Finance Banks (SFBs) have been playing a prominent role in providing last mile credit to individuals and small businesses. A three-year special long-term repo operations (SLTRO) facility of ₹10,000 crore at the repo rate was made available to them in May 2021 to be deployed for fresh lending of up to ₹10 lakh per borrower. This facility was made available till October 31, 2021. Recognising the persisting uneven impact of the pandemic on small business units, micro and small industries, and other unorganised sector entities, it has been decided to extend this facility till December 31, 2021. Further, this will now be available on tap to ensure extended support to these entities.

II. Payment and Settlement Systems

2. Introduction of Digital Payment Solutions in Offline Mode

The Statement on Developmental and Regulatory Policies dated August 06, 2020 had announced a scheme to conduct pilot tests of innovative technology that enables retail digital payments even in situations where internet connectivity is low / not available (offline mode). Three pilots were successfully conducted under the Scheme in different parts of the country during the period from September 2020 to June 2021 involving small-value transactions covering a volume of 2.41 lakh for value ₹1.16 crore. The learnings indicate that there is a scope to introduce such solutions, especially in remote areas. Given the experience gained from the pilots and the encouraging feedback, it is proposed to introduce a framework for carrying out retail digital payments in offline mode across the country. Detailed guidelines will be issued in due course.

3. Enhancing Transaction Limit in IMPS to ₹5 lakh

Immediate Payment Service (IMPS) of National Payments Corporation of India (NPCI) is an important payment system providing 24×7 instant domestic funds transfer facility and is accessible through various channels like internet banking, mobile banking apps, bank branches, ATMs, SMS and IVRS. The per-transaction limit in IMPS, effective from January 2014, is currently capped at ₹2 lakh for channels other than SMS and IVRS. The per-transaction limit for SMS and IVRS channels is ₹5000. With RTGS now operational round the clock, there has been a corresponding increase in settlement cycles of IMPS, thereby reducing the credit and settlement risks. In view of the importance of the IMPS system in processing of domestic payment transactions, it is proposed to increase the per-transaction limit from ₹2 lakh to ₹5 lakh for channels other than SMS and IVRS. This will lead to further increase in digital payments and will provide an additional facility to customers for making digital payments beyond ₹2 lakh. Necessary instructions in this regard would be issued separately.

4. Geo-tagging of Payment System Touch Points

Deepening digital payments penetration across the country is a priority area for financial inclusion. The setting up of Payments Infrastructure Development Fund (PIDF) to encourage deployment of acceptance infrastructure and create additional touch points is a step in this direction. To ensure a balanced spread of acceptance infrastructure across the length and breadth of the country, it is essential to ascertain location information of existing payment acceptance infrastructure. In this regard, geo-tagging technology, by providing location information on an ongoing basis, can be useful in targeting areas with deficient infrastructure for focussed policy action. Accordingly, it is proposed to lay down a framework for geo-tagging (capturing geographical coordinates -, viz., latitude and longitude) of physical payment acceptance infrastructure, viz., Point of Sale (PoS) terminals, Quick Response (QR) codes, etc., used by merchants. This would complement the PIDF framework by better deployment of acceptance infrastructure and wider access to digital payments. Necessary instructions will be issued separately.

5. Regulatory Sandbox – Announcement of the Theme for a New Cohort and On Tap Application for Earlier Themes

The Reserve Bank’s Regulatory Sandbox (RS) has so far introduced three cohorts. Six entities have successfully exited the First Cohort on ‘Retail Payments’ while under the Second Cohort on ‘Cross Border Payments’ eight entities are undertaking Tests. The application window for the Third Cohort of ‘MSME Lending’ is currently open.

With a view to preparing the fintech eco-system, it is proposed that the topic for the Fourth Cohort would be ‘Prevention and Mitigation of Financial Frauds’. The focus would be on using technology to reduce the lag between the occurrence and detection of frauds, strengthening the fraud governance structure and minimising response time to frauds. The application window for this cohort would be opened in due course.

In addition, based on the experience gained and the feedback received from stakeholders, it is proposed to facilitate ‘On Tap’ application for themes of cohorts earlier closed. This measure is expected to ensure continuous innovation and engagement with industry to enable a proactive response to the rapidly evolving FinTech scenario. The modified framework will be released today.

III. Debt Management

6. Review of Ways and Means Advances (WMA) Limits and Relaxation in Overdraft (OD) Facility for the State Governments/UTs

As recommended by the Advisory Committee (Chairman: Shri Sudhir Shrivastava) to review the Ways and Means Advances (WMA) limits for State Governments/UTs, the enhanced interim WMA limits totalling ₹51,560 crore were extended by the Reserve Bank up to September 30, 2021 to help States/UTs to tide over the difficulties faced by them during the pandemic. Considering the uncertainties related to the ongoing pandemic, it has been decided to continue with the enhanced WMA limits up to March 31, 2022.

It has also been decided to continue with the liberalized measures introduced to deal with the pandemic, viz., enhancement of maximum number of days of OD in a quarter from 36 to 50 days and the number of consecutive days of OD from 14 to 21 days, up to March 31, 2022. The above measures are expected to help States/UTs to manage their cash flows better. The details in this regard will be issued separately.

IV. Financial Inclusion and Customer Protection

7. Priority Sector Lending – Permitting Banks to On-lend through NBFCs – Continuation of Facility

With a view to increase the credit flow to certain priority sectors of the economy which contribute significantly to growth and employment, and recognizing the role played by NBFCs in providing credit to these sectors, bank lending to registered NBFCs (other than MFIs) for on lending to Agriculture (investment credit), Micro and Small enterprises and housing (with an increased limit) was permitted to be classified as priority sector lending up to certain limits in August 2019, which was last extended on April 07, 2021 and was valid up to September 30, 2021.

Considering the increased traction observed in delivering credit to the underserved/unserved segments of the economy, it has been decided to extend this facility till March 31, 2022. A circular in this regard will be issued shortly.

8. Internal Ombudsman for NBFCs

Non-Banking Financial Companies (NBFCs) have played an important role in extending finance to niche sectors such as MSME, microfinance, housing, vehicle finance and have effectively complemented the efforts of banks through last mile financial intermediation. Several NBFCs have also successfully adopted digital modes to support the delivery of their financial products and services to a wide spectrum of customers.

The increased significance, strength and reach of NBFCs across the country has necessitated having in place better customer experience including grievance redress practices. Over the last few years, RBI has initiated various measures for consumer protection and grievance redress for customers of NBFCs, which include requiring NBFCs to appoint Nodal Officers for grievance redress (2013) and the launch of the Ombudsman Scheme for NBFCs (2018).

With a view to further strengthen the internal grievance redress mechanism of NBFCs, it has been decided to introduce the Internal Ombudsman Scheme (IOS) for certain categories of NBFCs which have higher customer interface. The IOS for NBFCs, which will be on the lines of IOS for banks and non-bank payment system participants, will require select NBFCs to appoint an Internal Ombudsman (IO) at the top of their internal grievance redress mechanism to examine customer complaints which are in the nature of deficiency in service and are partly or wholly rejected by the NBFCs. Detailed instructions in this regard will be issued separately.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/1003

*************

Reserve Bank of India

Date : Oct 08, 2021

Monetary Policy Statement, 2021-22 Resolution of the Monetary Policy Committee (MPC) October 6-8, 2021

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (October 8, 2021) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

The reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

- The MPC also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. Since the MPC’s meeting during August 4-6, 2021, the momentum of the global recovery has ebbed across geographies with the rapid spread of the delta variant of COVID-19, including in some countries with relatively high vaccination rates. After sliding to a seven-month low in August, the global purchasing managers’ index (PMI) rose marginally in September. World merchandise trade volumes remained resilient in Q2:2021, but more recently there has been a loss of momentum with the persistence of supply and logistics bottlenecks.

3. Commodity prices remain elevated, and consequently, inflationary pressures have accentuated in most advanced economies (AEs) and emerging market economies (EMEs), prompting monetary tightening by a few central banks in the former group and several in the latter. Change in monetary policy stances, in conjunction with a likely tapering of bond purchases in major advanced economies later this year, is beginning to strain the international financial markets with a sharp rise in bond yields in major AEs and EMEs after remaining range-bound in August. The US dollar has strengthened sharply, while the EME currencies have weakened since early-September with capital outflows in recent weeks.

Domestic Economy

4. On the domestic front, real gross domestic product (GDP) expanded by 20.1 per cent year-on-year (y-o-y) during Q1:2021-22 on a large favourable base; however, its momentum was dragged down by the second wave of the pandemic. The level of real GDP in Q1:2021-22 was 9.2 per cent below its pre-pandemic level two years ago. On the demand side, almost all the constituents of GDP posted robust y-o-y growth. On the supply side, real gross value added (GVA) increased by 18.8 per cent y-o-y during Q1:2021-22.

5. The rebound in economic activity gained traction in August-September, facilitated by the ebbing of infections, easing of restrictions and a sharp pick-up in the pace of vaccination. The south-west monsoon, after a lull in August, picked up in September, narrowing the deficit in the cumulative seasonal rainfall to 0.7 per cent below the long period average and kharif sowing exceeded the previous year’s level. Record kharif foodgrains production of 150.5 million tonnes as per the first advance estimates augurs well for the overall agricultural sector. By end-September, reservoir levels at 80 per cent of the full reservoir level were above the decadal average, which is expected to boost rabi production prospects.

6. After a prolonged slowdown, industrial production posted a high y-o-y growth for the fifth consecutive month in July. The manufacturing PMI at 53.7 in September remained in positive territory. Services activity gained ground with support from the pent-up demand for contact-intensive activities. The services PMI continued in expansion zone in September at 55.2, although some sub-components moderated. High-frequency indicators for August-September – railway freight traffic; cement production; electricity demand; port cargo; e-way bills; GST and toll collections – suggest progress in the normalisation of economic activity relative to pre-pandemic levels; however, indicators such as domestic air traffic, two-wheeler sales and steel consumption continue to lag. Non-oil export growth remained strong on buoyant external demand.

7. Headline CPI inflation at 5.3 per cent in August softened for the second consecutive month, declining by one percentage point from the recent peak in May-June 2021. This was primarily driven by an easing in food inflation. Fuel inflation edged up to a new high in August. Core inflation, i.e. inflation excluding food and fuel, remained elevated and sticky at 5.8 per cent in July-August 2021.

8. System liquidity remained in large surplus in August-September, with daily absorptions rising from an average of ₹7.7 lakh crore in July-August to ₹9.0 lakh crore during September and ₹9.5 lakh crore during October (up to October 6) through the fixed rate reverse repo, the 14-day variable rate reverse repo (VRRR) and fine-tuning operations under the liquidity adjustment facility (LAF). Auctions of ₹1.2 lakh crore under the secondary market government securities acquisition programme (G-SAP 2.0) during Q2:2021-22 provided liquidity across the term structure. As on October 1, 2021, reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 8.3 per cent (y-o-y); money supply (M3) and bank credit grew by 9.3 per cent and 6.7 per cent, respectively, as on September 24, 2021. India’s foreign exchange reserves increased by US$ 60.5 billion in 2021-22 (up to October 1) to US$ 637.5 billion, partly reflecting the allocation of special drawing rights (SDRs), and were close to 14 months of projected imports for 2021-22.

Outlook

9. Going forward, the inflation trajectory is set to edge down during Q3:2021-22, drawing comfort from the recent catch-up in kharif sowing and likely record production. Along with adequate buffer stock of foodgrains, these factors should help to keep cereal prices range bound. Vegetable prices, a major source of inflation volatility, have remained contained in the year so far and are likely to remain soft, assuming no disruption due to unseasonal rains. Supply side interventions by the Government in the case of pulses and edible oils are helping to bridge the demand supply gap; the situation is expected to improve with kharif harvest arrivals. The resurgence of edible oils prices in the recent period, however, is a cause of concern. On the other hand, pressures persist from crude oil prices which remain volatile over uncertainties on the global supply and demand conditions. Domestic pump prices remain at very high levels. Rising metals and energy prices, acute shortage of key industrial components and high logistics costs are adding to input cost pressures. Weak demand conditions, however, are tempering the pass-through to output prices. The CPI headline momentum is moderating with the easing of food prices which, combined with favourable base effects, could bring about a substantial softening in inflation in the near-term. Taking into consideration all these factors, CPI inflation is projected at 5.3 per cent for 2021-22; 5.1 per cent in Q2, 4.5 per cent in Q3; 5.8 per cent in Q4 of 2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.2 per cent (Chart 1).

10. Domestic economic activity is gaining traction with the ebbing of the second wave. Going forward, rural demand is likely to maintain its buoyancy, given the above normal kharif sowing while rabi prospects are bright. The substantial acceleration in the pace of vaccination, the sustained lowering of new infections and the coming festival season should support a rebound in the pent-up demand for contact intensive services, strengthen the demand for non-contact intensive services, and bolster urban demand. Monetary and financial conditions remain easy and supportive of growth. Capacity utilisation is improving, while the business outlook and consumer confidence are reviving. The broad-based reforms by the government focusing on infrastructure development, asset monetisation, taxation, telecom sector and banking sector should boost investor confidence, enhance capacity expansion and facilitate crowding in of private investment. The production-linked incentive (PLI) scheme augurs well for domestic manufacturing and exports. Global semiconductor shortages, elevated commodity prices and input costs, and potential global financial market volatility are key downside risks to domestic growth prospects, along with uncertainty around the future COVID-19 trajectory. Taking all these factors into consideration, projection for real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 7.9 per cent in Q2; 6.8 per cent in Q3; and 6.1 per cent in Q4 of 2021-22. Real GDP growth for Q1:2022-23 is projected at 17.2 per cent (Chart 2).

11. Inflation prints in July-August were lower than anticipated. With core inflation persisting at an elevated level, measures to further ameliorate supply side and cost pressures, including through calibrated cuts in indirect taxes on petrol and diesel by both Centre and States, would contribute to a more durable reduction in inflation and anchoring of inflation expectations. The outlook for aggregate demand is progressively improving but the slack is large: output is still below pre-COVID level and the recovery is uneven and critically dependent upon policy support. Compared to pre-pandemic levels, contact intensive services, which contribute around two-fifth of economic activity in India, still lag considerably. Capacity utilisation in the manufacturing sector is below its pre-pandemic levels and an early recovery to its long-run average is critical for a sustained rebound in investment demand. Even as the domestic economy is showing signs of mending, the external environment is turning more uncertain and challenging, with headwinds from slowing growth in some major Asian and advanced economies, steep jump in natural gas prices in the recent weeks and concerns emanating from normalisation of monetary policy in some major advanced economies. Against this backdrop, the ongoing domestic recovery needs to be nurtured assiduously through all policy channels. The MPC will remain watchful given the uncertainties surrounding the outlook for growth and inflation. Accordingly, keeping in mind the evolving situation, the MPC decided to keep the policy repo rate unchanged at 4 per cent and continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

12. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent.

13. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

14. The minutes of the MPC’s meeting will be published on October 22, 2021.

15. The next meeting of the MPC is scheduled during December 6 to 8, 2021.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/1002

********

Reserve Bank of India

Date : Oct 08, 2021

Governor’s Statement : October 08, 2021

This is my twelfth statement since the onset of the pandemic. Of these, two statements were outside the Monetary Policy Committee (MPC) cycle – one in April 2020 at the outbreak of the COVID-19 crisis and the other in May 2021 at the peak of the second wave. Further, on two occasions – March and May 2020 – the MPC meeting had to be advanced to take pre-emptive action to safeguard the economy from the ravages of the pandemic. Over this period, the Reserve Bank has taken more than 100 measures to proactively and decisively respond to the unprecedented crisis. While doing so, we have not been a prisoner of any rulebook. We have not hesitated to take new and unconventional measures to keep the financial markets functioning and the market sentiments positive; provide liquidity to targeted sectors and institutions; and leverage on digital technologies to reach out to individuals and businesses. Thus, although the pandemic protocols do us part, technology ties us together.

2. In this backdrop, the MPC met on 6th, 7th and 8th October, 2021. Based on an assessment of the evolving macroeconomic and financial conditions and the outlook, the MPC voted unanimously to maintain status quo with regard to the policy repo rate and by a majority of 5 to 1 to retain the accommodative policy stance. Consequently, the policy repo rate remains unchanged at 4 per cent; and the stance remains accommodative as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. The marginal standing facility (MSF) rate and the bank rate remain unchanged at 4.25 per cent. The reverse repo rate also remains unchanged at 3.35 per cent.

3. With the worst of the second wave behind us and substantial pick-up in COVID-19 vaccination giving greater confidence to open up and normalise economic activity, the recovery of the Indian economy is gaining traction. While vaccine reach is the real fault line in the current global recovery, India is in a much better place today than at the time of the last MPC meeting. Growth impulses seem to be strengthening and we derive comfort from the fact that the inflation trajectory is turning out to be more favourable than anticipated. In spite of global headwinds, we hope to emerge from the storm and sail towards normal times, steered by the underlying resilience of the macro-economic fundamentals of the Indian economy.

4. Let me now give a brief overview of the MPC’s rationale for the pause on the policy rate and the accommodative stance. The MPC noted that economic activity over the past two months has broadly evolved in consonance with the MPC’s August assessment and outlook; and CPI inflation during July-August has turned out to be lower than anticipated. The actual outturn of real GDP growth in Q1:2021-22 at 20.1 per cent was close to, albeit a little below the MPC’s forecast of 21.4 per cent. High-frequency indicators for Q2:2021-22 suggest that economic recovery has gained momentum, supported by ebbing of infections, the robust pace of vaccination, expected record kharif foodgrains production, government’s focus on capital expenditure, benign monetary and financial conditions, and buoyant external demand.

5. Consumer price inflation softened during July-August, moving back into the tolerance band with an easing of food inflation, corroborating the MPC’s assessment of the spike in inflation in May as transitory. Improvement in monsoon in September, the expected higher kharif production, adequate buffer stock of foodgrains and lower seasonal pickup in vegetable prices are likely to keep food price pressures muted. Core inflation, however, remains sticky. Elevated global crude oil and other commodity prices, combined with acute shortage of key industrial components and high logistics costs, are adding to input cost pressures. Pass-through to output prices has, however, been restrained by weak demand conditions. The evolving situation requires close vigilance.

6. Overall, aggregate demand is improving but slack still remains; output is still below pre-pandemic level and the recovery remains uneven and dependent upon continued policy support. Contact intensive services, which contribute about 40 per cent of economic activity in India, are still lagging. Supply side and cost push pressures are impinging upon inflation and these are expected to ameliorate with the ongoing normalisation of supply chains. Efforts to contain cost-push pressures through a calibrated reversal of the indirect taxes on fuel could contribute to a more sustained lowering of inflation and an anchoring of inflation expectations. Against this backdrop, the MPC decided to retain the prevailing repo rate at 4 per cent and continue with the accommodative stance, as stated in the last MPC statement.

Assessment of Growth and Inflation

Growth

7. According to the release of National Statistical Office on August 31, real GDP growth for Q1:2021-22 at 20.1 per cent exhibited resilience of the economy in the face of the destructive second wave of COVID-19. Almost all components of GDP registered y-o-y growth, despite a sharp loss of momentum due to the second wave.

8. Recovery in aggregate demand gathered pace in August-September. This is reflected in high-frequency indicators – railway freight traffic; port cargo; cement production; electricity demand; e-way bills; GST and toll collections. The ebbing of infections, together with improving consumer confidence, has been supporting private consumption. The pent-up demand and the festival season should give further fillip to urban demand in the second half of the financial year. Rural demand is expected to get impetus from continued resilience of the agricultural sector and record production of kharif foodgrains in 2021-22 as per the first advance estimates. The improved level in reservoirs and early announcement of the minimum support prices for rabi crops boost the prospects for rabi production. The support to aggregate demand from government consumption is also gathering pace.

9. Improvement in government capex, together with congenial financial conditions, could bring about an upturn in the much-awaited virtuous investment cycle. Pick up in import of capital goods and cement production point towards some revival in investment activity. According to our survey results, capacity utilisation (CU) in the manufacturing sector, which declined sharply in Q1:2021-22 under the second wave, is assessed to have recovered in Q2 and further improvement is expected in the ensuing quarters.

10. Critical support to aggregate demand also came from exports, which remained in excess of US$ 30 billion for the seventh consecutive month in September 2021 reflecting strong global demand and policy support. This augurs well for meeting our export target of US$ 400 billion during 2021-22.

11. Recovery in the services sector is also gaining traction. Gradual pickup in contact-intensive services, together with strong performance of technology driven sectors, are likely to support the momentum.

12. Impact of elevated input costs on profit margins, potential global financial and commodity markets volatility and a resurgence in COVID-19 infections, however, impart downside risks to the growth outlook. Taking all these factors into consideration, the projection for real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 7.9 per cent in Q2; 6.8 per cent in Q3; and 6.1 per cent in Q4 of 2021-22. Real GDP growth for Q1:2022-23 is projected at 17.2 per cent.

Inflation

13. Headline CPI inflation at 5.3 per cent in August registered a moderation for the second consecutive month and a decline of one percentage point from its level in June 2021. The key driver of the disinflation has been the moderation in food inflation even as fuel inflation edged up and CPI inflation excluding food and fuel inflation (core inflation) remained elevated. Headline inflation continues to be significantly influenced by very high inflation in select items such as edible oils, petrol and diesel, LPG and medicines. On the other hand, a very low seasonal build-up in vegetable prices, declining cereal prices, a sharp deflation in gold prices and muted housing inflation have helped to contain inflationary pressures.

14. Going forward, several evolving factors provide comfort on the food price front. Its momentum is expected to remain muted in the near term. Cereal prices are expected to remain soft due to likely record kharif foodgrains production and adequate buffer stocks. Vegetable prices, a major source of inflation volatility, have remained contained in the year so far with record production and supply side measures by the Government. Unseasonal rains and adverse weather-related events – if any, in the coming months – are, however, upside risks to vegetable prices. Supply side measure by the Government for edible oils and pulses are helping to temper price pressures; however, an uptick in prices of edible oils is seen in the recent period.

15. Overall, the CPI headline momentum is moderating which, combined with favourable base effects in the coming months, could bring about a substantial softening in inflation in the near-term. Taking into consideration all these factors, CPI inflation is projected at 5.3 per cent for 2021-22: 5.1 per cent in Q2, 4.5 per cent in Q3; 5.8 per cent in Q4 of 2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.2 per cent. We are watchful of the evolving inflation situation and remain committed to bring it closer to the target in a gradual and non-disruptive manner.

Liquidity and Financial Market Conditions

16. At the current juncture, central banks across the world find themselves at crossroads. Diverging monetary policy stances are not being dictated by country groupings but by country circumstances. Among EMEs, some are tightening monetary policy, others are undertaking further monetary stimulus, while a few are on a resolute pause. The countries that are tightening monetary policy are those which are facing inflation much above their upper tolerance bands and are also registering a strong rebound in growth above pre-pandemic levels, boosted mainly by commodity export earnings and positive spillovers from improvement in macroeconomic conditions in some advanced economies. Countries that are easing monetary policy through non-rate actions are the rare few which have low consumer price inflation. And finally, countries which are on a resolute pause have inflation in the elevated zone but poor growth prospects or nascent recoveries that need nurturing. In India, the MPC has maintained a pause and given time and state contingent forward guidance from time to time on maintaining accommodation. The conduct of monetary policy in India will continue to be oriented to our domestic circumstances and our assessment.

17. Since the onset of the pandemic, the Reserve Bank has maintained ample surplus liquidity to support a speedy and durable economic recovery. The level of surplus liquidity in the banking system increased further during September 2021, with absorption under fixed rate reverse repo, variable rate reverse repo (VRRR) of 14 days and fine-tuning operations under the liquidity adjustment facility (LAF) averaging ₹9.0 lakh crore per day as against ₹7.0 lakh crore during June to August 2021. The surplus liquidity rose even further to a daily average of ₹9.5 lakh crore in October so far (up to October 6). The potential liquidity overhang amounts to more than ₹13.0 lakh crore.

18. As the economy shows signs of emerging from the COVID-19 inflicted ravages, a near consensus view emerging among market participants and policy makers is that the liquidity conditions emanating from the exceptional measures instituted during the crisis would need to evolve in sync with the macroeconomic developments to preserve financial stability. This process has to be gradual, calibrated and non-disruptive, while remaining supportive of the economic recovery.

19. The Reserve Bank’s secondary market G-Sec Acquisition Programme (G-SAP) has been successful in addressing market concerns and anchoring yield expectations in the context of the large borrowing programme of the Government. Coupled with other liquidity measures, it facilitated congenial and orderly financing conditions and a conducive environment for the recovery. The total liquidity injected into the system during the first six months of the current financial year through open market operations (OMOs), including G-SAP, was ₹2.37 lakh crore, as against an injection of ₹3.1 lakh crore over the full financial year 2020-21. Given the existing liquidity overhang, the absence of a need for additional borrowing for GST compensation and the expected expansion of liquidity in the system as Government spending increases in line with budget estimates, the need for undertaking further G-SAP operations at this juncture does not arise. The Reserve Bank, however, would remain in readiness to undertake G-SAP as and when warranted by liquidity conditions and also continue to flexibly conduct other liquidity management operations including Operation Twist (OT) and regular open market operations (OMOs).

20. With the resumption of normal liquidity operations since mid-January 2021, 14-day variable rate reverse repo (VRRR) auctions have been deployed as the main instrument under the liquidity management framework. Market appetite for VRRRs has been enthusiastic. Moreover, the higher remuneration which VRRR offers vis-à-vis the fixed rate reverse repo is also rendering the former relatively attractive. Keeping in view the market feedback, it is proposed to undertake the 14-day VRRR auctions on a fortnightly basis in the following manner: ₹4.0 lakh crore today as already notified; ₹4.5 lakh crore on October 22; ₹5.0 lakh crore on November 3; ₹5.5 lakh crore on November 18; and ₹6.0 lakh crore on December 3. Further, depending upon the evolving liquidity conditions – especially the quantum of capital flows, pace of government expenditure and credit offtake – the RBI may also consider complementing the 14-day VRRR auctions with 28-day VRRR auctions in a similar calibrated fashion. The RBI also retains the flexibility to conduct fine-tuning operations of varying amounts as and when required. Even with all these operations, the liquidity absorbed under the fixed rate reverse repo would still be around ₹2 to 3 lakh crore in the first week of December 2021.

21. Let me reiterate and reemphasise that the VRRR auctions are primarily a tool for rebalancing liquidity as part of our liquidity management operations and should not be interpreted as a reversal of the accommodative policy stance. The RBI will ensure that there is adequate liquidity to support the process of economic recovery. The Reserve Bank will continue to support the market in ensuring an orderly completion of the borrowing programme of the Government. Further, our focus on orderly evolution of the yield curve as a public good also continues.

Additional Measures

22. Against this backdrop and based on our continuing assessment of the macroeconomic situation and financial market conditions, certain additional measures are also being announced today. The details of these measures are set out in the statement on developmental and regulatory policies (Part-B) of the Monetary Policy Statement. The additional measures are as follows.

On Tap Special Long-Term Repo Operations (SLTRO) for Small Finance Banks (SFBs)

23. A special three-year long-term repo operation (SLTRO) of ₹10,000 crore at the repo rate was introduced for Small Finance Banks (SFBs) in May 2021. This facility is currently available till October 31, 2021. Recognising the need for continued support to small business units, micro and small industries, and other unorganised sector entities, it has been decided to extend this facility till December 31, 2021 and make it available On Tap.

Introduction of Retail Digital Payment Solutions in Offline Mode

24. A scheme to test technologies that enable digital payments even in remote places where internet connectivity is either absent or barely available was announced in August 2020. Given the encouraging experience gained from the pilot tests, it is proposed to introduce a framework for retail digital payments in offline mode across the country. This will further expand the reach of digital payments and open up new opportunities for individuals and businesses.

Enhancing Transaction Limit in IMPS to ₹5 lakh

25. Immediate Payment Service (IMPS) offers instant domestic funds transfer facility 24×7 through various channels. In view of the importance of the IMPS system and for enhanced consumer convenience, it is proposed to increase the per-transaction limit from ₹2 lakh to ₹5 lakh.

Geo-Tagging of Payment System Touch Points

26. Ensuring wider availability of payments acceptance (PA) infrastructure throughout the country has been one of the priority areas for financial inclusion. To target areas with deficient PA infrastructure, it is proposed to introduce a framework for leveraging geo-tagging technology for capturing exact location information on all existing and new PA infrastructure viz., Point of Sale (PoS) terminals, Quick Response (QR) Codes, etc. This would complement the Payment Infrastructure Development Fund (PIDF) framework of the Reserve Bank in ensuring wider geographical deployment of PA infrastructure.

Regulatory Sandbox – Announcement of the Theme for a New Cohort and On Tap Application for Earlier Themes

27. The Reserve Bank’s Regulatory Sandbox (RS) has so far introduced three cohorts on ‘Retail Payments’; ‘Cross Border Payments’; and ‘MSME Lending’. With a view to provide further impetus to the fintech eco-system, a fourth cohort on ‘Prevention and Mitigation of financial frauds’ is being announced. In addition, based on the experience gained and the feedback received from stakeholders, it is proposed to facilitate ‘On Tap’ application for earlier themes for participating in the Regulatory Sandbox. This measure is expected to ensure continuous innovation in the fintech ecosystem of our country.

Review of Ways and Means Advances (WMA) Limits and Relaxation in Overdraft (OD) Facility for the State Governments / UTs

28. To help States/UTs to manage their cash flows amidst continued uncertainties on account of the pandemic, it has been decided to continue with the interim enhanced WMA limits of ₹51,560 crore for States/UTs for a further period of six months up to March 31, 2022. It has also been decided to continue with the liberalised measures, viz, enhancement of maximum number of days of overdraft (OD) in a quarter from 36 to 50 days and the number of consecutive days of OD from 14 to 21 days, up to March 31, 2022.

Priority Sector Lending – Permitting Banks to On-lend through NBFCs – Continuation of Facility

29. Considering the increased traction observed in delivery of credit by NBFCs to the underserved/unserved segments of the economy, bank lending to registered NBFCs (other than MFIs) for on-lending to Agriculture, MSME and Housing was permitted to be classified as Priority Sector lending (PSL). This facility, which was available from August 13, 2019 till September 30, 2021 is being further extended for another six months up to March 31, 2022.

Internal Ombudsman for NBFCs

30. The increased strength and reach of NBFCs across the country has necessitated various measures by the Reserve Bank for protection of customers of NBFCs. With a view to further strengthening the internal grievance redress mechanism of NBFCs, it has been decided to introduce the Internal Ombudsman Scheme (IOS) for certain categories of NBFCs having higher customer interface.

Concluding Remarks

31. If there is anything that the most trying and difficult past eighteen months have taught us, it is to never doubt the indomitable human spirit which always rises to face mighty challenges. With our resilience and resolute commitment, we have learnt to adapt, innovate and turn challenges into opportunities. As we further accelerate the pace of economic recovery, it is important not to rest in the glory of what has been achieved but work tirelessly on what remains to be done. As Mahatma Gandhi, whose birth anniversary we celebrated last week, had said: “to lose patience is to lose the battle”1.

Thank you. Stay safe. Stay well. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/1001

Source

1. https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52368

2. https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52366

3. https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52367