1. Rule 138 of CGST Rules and respective SGST Rules of the different States requires every registered person who causes movement of goods of consignment value exceeding Rs. 50,000 in relation to a supply; for reasons other than supply; or due to inward supply from an unregistered person to generate e-way bill for the movement of goods.

2. E-way bill is required to be generated for the movement of goods where the consignment value of such goods exceed Rs. 50,000.

3. Consignment value: It is defined as the transaction value of the goods being transported which is declared in an invoice, a bill of supply or a delivery challan, as the case may be, issued in respect of the said consignment including the CGST, SGST or UTGST, IGST and GST compensation cess charged in the document.

4. The value of exempt supply of goods where the invoice is issued in respect of both exempt and taxable supply of goods should be excluded. However, in the following cases, e-way bill is required to be generated even if the consignment value of the goods does not exceed Rs. 50,000:

a. Movement of goods for job work by a principal located in one State or Union Territory to a job worker located in another State or Union Territory;

b. Movement of handicraft goods from one State or Union territory to another State or Union territory by a person who has been exempted from the requirement of obtaining registration.

5. We would discuss who is responsible for generating e-way bill? The person who causes the movement of goods is required to generate e-way bill.

6. When is e-way bill required to be generated? E-way bill is required to be generated for the movement of goods irrespective of whether the movement is being made for supply of goods or not. For example, in the cases of movement of goods for the purposes of job work, weighment, warehousing, there is no supply of goods being made. However, e-way bill is required to be generated as there is a movement of goods.

7. It is important to note that where the goods are being transported up to a distance of twenty kilometers from the place of the business of the consignor to a weighbridge for weighment or from the weighbridge back to the place of the business of the said consignor subject to the condition that the movement of goods is accompanied by a delivery challan issued in accordance with rule 55.

8. Invoice for the sale of goods: Section 31(1) of CGST Act states that a registered person supplying taxable goods is required to issue a tax invoice, before or at the time of, —

a. removal of goods for supply to the recipient, where the supply involves movement of goods; or

b. delivery of goods or making available thereof to the recipient, in any other case, showing the description, quantity and value of goods, the tax charged thereon and such other particulars as prescribed in Rule 46 of CGST Rules, 2017.

9. Delivery challan for the movement of goods: Rule 55 of CGST Rules, 2017 [Transportation of goods without issue of invoice] states that in the cases of transportation of goods for reasons other than by way of supply, the consignor would be required to issue a delivery challan in lieu of invoice at the time of removal of goods for transportation.

10. Therefore, where the transaction is in the nature of supply and where the consignment value exceeds INR 50,000 in such a case E-Way bill has be generated on the basis of Invoice. In case, where the transaction is for reasons other than supply and where the consignment value exceeds INR 50,000 in such a case E-Way bill has be generated on the basis of Delivery Challan.

11. During the first lockdown (Mar-Apr’20), CBIC had issued a series of Notification extending the time limit for compliances. One of extensions was also in regard to EWB. Notification stated that “Where validity of an e-way bill expires during the period 20th day of March, 2020 to 15th day of April, 2020, the validity period of such e-way bill shall be deemed to have been extended till the 30th day of April, 2020”. However, in the period of second lockdown, Notification in this regard has not been issued yet by CBIC. Therefore, we have come up with possible issues as well as solutions which are explained below:

Case 1: In case EWB is about to get expired when the vehicle is still in the movement

12. Extension of e-way bill by the transporter:Proviso to Rule 138(10) of CGST Rules states that under circumstances of an exceptional nature, including trans-shipment, where the goods cannot be transported within the validity period of the e-way bill, the transporter may extend the validity period after updating the details in Part B of FORM GST EWB-01, if required. The validity of the e-way bill may be extended within 8 hours from the time of its expiry.

13. Procedure for extension of e-way bill:The transporter would be required to follow the below-given procedure for extending the validity of e-way bill.

a. Select “Extend validity” option in the E-way bill field in the dashboard.

b. The Form for Extension of Validity of E-way bill appears. Enter the E-way bill number whose validity is to be extended and Select “Go”.

c. The relevant e-way bill is displayed on the portal with a question “Do you wish to get Extension for this EWB?”- Select “Yes”.

d. Once the “Yes” option is selected, the transporter has to fill the following details:

1. Reason for Extension;

2. Remarks- Provide the exact reason for extension in simple words;

3. Transportation details- Current place, pin code and State where the goods are presently located;

4. Approximate Distance [in KM]- Approximate remaining distance which is auto calculated and could be changed as discussed previously;

5. Consignment is- “In Movement” or “In Transit”;

6. Mode- Road, Rail, Air of Ship;

7. Vehicle Type- Regular or Over Dimensional Cargo;

8. Vehicle number; and

9. Transporter Doc. No & Date.

e. Click “Submit” and then the validity of the e-way bill would be extended after validation of the details given. The validity would be extended based on the remaining distance to be moved as discussed above.

Case 2: Where the EWB has been expired and goods are nowhere near the destination.

14. It was held in the case of Ram Charitra Ram Harihar Prasad Vs. State of Bihar- 2020(34) G.S.T.L. 151 (Pat.)that there is no bar in Rules that on expiry of old E-way Bill, a fresh E-way Bill cannot be issued. However, practically re-generating of EWB on the same Invoice is not possible. Practically portal does not accept the same.

15. Therefore, in such scenario, it is suggested to generate an EWB by mentioning the invoice number by mentioning an additional ‘DOT’ in the invoice. However, it is also suggested to intimate the same by RPAD letter to the department the valid reasons for re-generating EWB on the same Invoice number.

16. New EWB has been generated in the following manner:

| PART-A | ||

| 1 | Supply type | Outward |

| 2 | Sub type | Supply |

| 3 | Document type | Document type: Invoice

Document no: Invoice no. Document date: Invoice date |

| 4 | Transaction type | Regular |

| 5 | Bill from | Name, GSTIN and State of Supplier |

| 6 | Dispatch from | Address, place and pin code of the current location of the vehicle from where goods are dispatched. |

| 7 | Bill to | Name, State and GSTN of the customer |

| 8 | Ship to | Address, place and pin code of the Hub where the goods are to be delivered. |

| 9 | Item details | Product name, Description, HSN, Qty, unit, Value, Tax rate |

| PART-B | ||

| 10 | Transporter ID | Transporter ID/ TRANSIN |

| 11 | Approximate Distance | Mention KM in distance from the place of the current location of the vehicle to the place where the goods are delivered. |

| 12 | Mode | Road |

| 13 | Vehicle Type | Regular |

| 14 | Vehicle no | Vehicle number |

| 15 | Transporter Doc no & Date | LR number and LR date. |

17. In case, if the goods and the conveyance are verified during transit, the department cannot seize or detain such goods only on the grounds that there is “Error in one or two digits of the document number mentioned in the e-way bill”. The department could collect a penalty of Rs. 1,000 [Rs. 500- CGST+ Rs. 500- SGST or Rs. 1,000- IGST], in terms of Circular no. 64/38/2018-GST dt. 14thSeptember 2018.

Case 3: Where the EWB has been expired and goods are near the destination.

18. It is suggested to follow the same procedure as given in case 2 above.

Case 4: Where the goods have reached the destination in time, but EWB would be expired at the time of unloading such goods.

19. Extension of e-way bill by the transporter:Proviso to Rule 138(10) of CGST Rules states that under circumstances of an exceptional nature, including trans-shipment, where the goods cannot be transported within the validity period of the e-way bill, the transporter may extend the validity period after updating the details in Part B of FORM GST EWB-01, if required. The validity of the e-way bill may be extended within 8 hours from the time of its expiry.

20. The FAQ issued on the e-way bill portal provides as under.

“My goods are in warehouse, and the e-waybill validity is expiring. Can I extend the e-waybill ?

Yes. You can use the Extend Validity option before 8 hours or after 8 hours from the validity date. Select the E-waybill extension option. Specify the Consignment is in Transit, enter the details of the warehouse such as Pin code and address. The system will extend the validity for the remaining distance.”

Note: The time limit for extending the validity of e-way bill has been amended which is within 8 hours from the time of expiry of the e-way bill.

21. The FAQ issued on the e-way bill portal also provides as under.

“Who can extend the validity of the e-way bill?

The transporter, who is carrying the consignment as per the e-way bill system at the time of expiry of validity period, can extend the validity period.”

Case 5: How is validity of EWB computed?

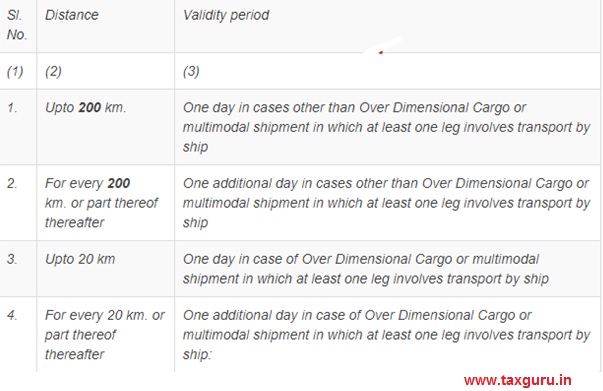

22. In terms of Rule 138(10) of CGST Act 2017, An e-way bill or a consolidated e-way bill generated under this rule shall be valid for the period as mentioned in column (3) of the Table below from the relevant date, for the distance, within the country, the goods have to be transported, as mentioned in column (2) of the said Table: –

23. As per Rule 138, the”relevant date” shall mean the date on which the e-way bill has been generated and the period of validity shall be counted from the time at which the e-way bill has been generated and each day shall be counted as the period expiring at midnight of the day immediately following the date of generation of e-way bill.

24. For Example:

a. Suppose an e-way bill is generated at 00:04 hrs. on 14th March. Then first day would end on 12:00 midnight of 15 -16 March. Second day will end on 12:00 midnight of 16 -17 March and so on.

b. Suppose an e-way bill is generated at 23:58 hrs. on 14th March. Then first day would end on 12:00 midnight of 15 -16 March. Second day will end on 12:00 midnight of 16 -17 March and so on. The same was clarified in FAQ’s released by CBIC.

Case 6: How many times can Part-B or Vehicle number be updated for an EWB?

25. The user can update Part-B (Vehicle details) for each change in the vehicle or mode of transport used in the course of movement of consignment up to the destination point. However, the updating should be done within overall validity period of EWB. There is no upper cap on the number of updation of vehicle in Part B.

Special thanks to CA Roopa Nayak as well as CA Mayank Jain for vetting this article and valuable suggestions.

For any further clarifications reach at Mail – rakesh@hiregange.com

Author Bio

Sir whether SEZ units has to issue e way bill for movement of goods from Port to sez factory and sez factory to port .