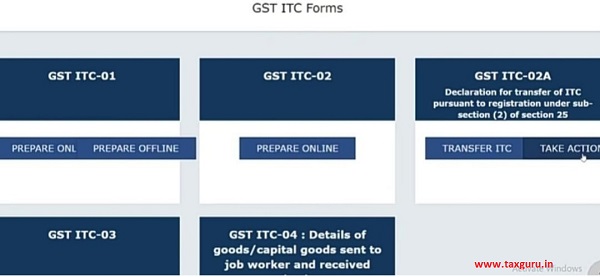

GST portal has now enabled filling of GST ITC-02A.

GST ITC-02A is a declaration of untilized ITC transferred for obtaining a separate registration within the same state or union territory.

Rule 41A deals with Transfer of credit on obtaining separate registration for multiple places of business within a state or UT-

(1) A registered person who has obtained separate registration for multiple places of business in accordance with the provisions of Rule 11 and who intends to transfer, either wholly or partly, the untilized input tax credit lying in his electronic credit ledger to any or all of the newly registered places of business, shall furnish within 30 days from obtaining such separate registration, the details in Form GST ITC-02A electronically on the common portal either directly or through a facilitation center notified on this behalf by the commissioner.

Provided that the input tax credit shall be transferred to the newly registered entities in the ratio of value of assets held by them at the time of registration.

Explanation– For the purposes of this sub rule,it is hereby clarified that the value of asset means the value of entire assets of the business whether or not input tax credit has been availed thereon.

(2) Newly registered person (Transferee) shall on the common portal, accept the details so furnish ed by the registered person ( Transferor) and upon such acceptance the untilized input tax credit specified in Form GST ITC-02A shall be credited in his electronic credit ledger.

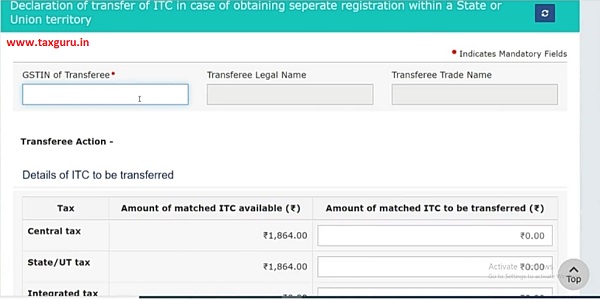

Details to be furnished in GST ITC-02A are as follows:

Go to login: fill your credentials like Userid and password.

Dashboard_ Returns_ ITC Forms:

1) GSTIN of Transferee: Newly registered person to whom you want to transfer ITC. This will auto populate Transferee’s legal name and trade name.

2) Amount of matched ITC to be transferred: Amount available in electronics credit ledger of which amount to be transferred needs to mentioned according to head of tax Central tax, State/UT tax, Integrated Tax.

3) Save the above details and submit with DSC/ EVC.

Next Transferee needs to login to common portal and click on take action to accept credits transferred.

Example:

ABC Ltd has operations in Maharashtra with GSTIN:27AAxxxxxxxX1ZP (MH1)having credits in electronics ledger available is as follows CGST: Rs.10,000,SGST: Rs.10,000,IGST Rs.50,000. A new registration taken in the same state for different segment of business on 24 May 20 with GSTIN:27AAxxxxxxxX1ZQ (MH2) wanted to utilize credit available with MH1 to file GSTR-3B. MH1 should file GST-ITC-02A within 30 days of 24th May 2020 by 23 June 2020. MH2 should accept by clicking on Take Action. MH1 has a option to transfer all or partly based on value of asset by company on the date of registration. Hence asset with MH1 is Rs.10,00,000 and MH2 is Rs.10,00,000 on 24 May 2020 so ratio is 1:1. Available ITC will be divided equally between MH1 and MH2.

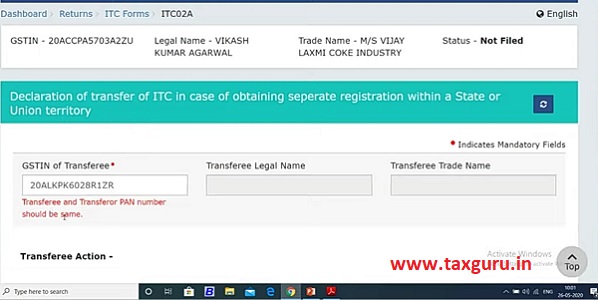

Key Note: Make sure PAN are same for both transferor and transferee.

Author’s Comment: GST ITC-02A will enable easy flow of credit within the same organisation.

Author Bio

@CA Karishma Mota

Is this one-time declaration or we can file it more than one time???