The approach of the government towards the NGO sector used to be lenient but today the position is changing as the government is tightening the laws and regulatory controls over NGOs every other day. It has to be appreciated that NGOs play an important role in the society and the income of these institutions is fully exempt from taxation subject to fulfilment of certain conditions.

There are many registered and unregistered NGOs in India working for the welfare of society. NGOs have multiple options to select the form of constitution, refer my blog on ‘Formation of NGO in India’. Post formation, NGOs are required to get registered under section 12A/12AA or obtain approval under section 10(23) and 80G to claim exemptions under the Income Tax Act, 1961 (‘the Act’).

The Finance Act 2020 has brought in major changes for NGOs by introducing new section 12AB replacing section 12AA and bringing in similar amendments in section 10(23C) and Section 80G. These changes shall be applicable with effect from 1st June 2020.

It is a welcome step that the process of registration and approvals of NGOs shall be completely electronic under which a unique registration number (URN) shall be issued to all new and existing charity institutions. This database shall help in bringing the exact size of NGO sector in India as it has always remained unregulated as compared to the corporate sector.

New requirements of registration for NGOs under the Act are discussed below:

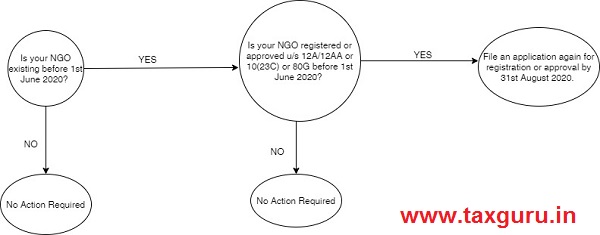

1. Renewal of Existing Registration and Approvals

The trusts or institutions which have been granted perpetuity of registration under section 12A/12AA or approval under section 10(23C) or 80G are required to make an application again under the new section 12AB or amended provisions of section of 10(23C) or 80G.

1.1 Requirement to file Application

If your NGO is existing on 1st June 2020 and already registered under Section 12A/12AA or approved under Section 10(23C) or Section 80G, then you will be required to make an application again, as per amendment by the Finance Act 2020.

1.2 Timeline to file Application

The application for approval in all such cases has to be made within 3 months from the date on which the new provisions shall come into force i.e. application has to be filed on or before 31st August 2020.

1.3 Passing of Order

The application has to be made to Principal Commissioner or Commissioner. On receipt of application, registration or approval in all such cases shall be granted under new law without any enquiries by the concerned officer.

The concerned officer has to pass an order to grant registration or approval in all such cases within 3 months calculated from the end of the month in which the application is received.

1.4 Validity of Approval

The registration or approval shall be granted for 5 years. These entities which were granted perpetuity of registration under earlier law shall now be required to renew their registration after every 5 years.

Example, A charitable trust already registered under section 12AA makes an application on 23rd July 2020. In such case, the order has to be passed by commissioner on or before 31st October 2020 granting registration under section 12AB for the period of 5 years without any enquiries.

2. Renewal after every 5 years

NGOs granted registration under new section 12AB or approved under section 10(23C) or 80G shall be required to make an application after every 5 years once the period of registration is due to expire.

2.1 Timeline to file Application

The application has to be made at least 6 months before the expiry of the period of 5 years of registration.

2.2 Procedure on Receipt of Application

Commissioner, on receipt of application, may call for the documents and information as he thinks necessary in order to satisfy himself about the genuineness of activities of trust or institution and the compliance of such requirements of any other law for the time being in force by it as are material for the purpose of achieving its objects.

2.3 Passing of Order

After satisfying himself about the objects and the genuineness of its activities and compliance of the requirements, the commissioner shall pass an order in writing granting registration to such NGO. However, if he is not so satisfied, he shall afford an opportunity of being heard and subsequently, pass an order in writing rejecting such application and also cancelling its registration.

The order shall be passed before expiry of the period of 6 months calculated from the end of the month in which the application is received by the commissioner.

2.4 Validity of Approval

The approval shall be granted for 5 years. Before this amendment, the registration once granted shall remain valid until it is withdrawn or cancelled. Now, there will be an obligation on every NGO registered to apply for re-registration after every 5 years.

Example, A trust has been granted registration for a period of 5 years for the A.Y. 2021-22 to A.Y. 2025-26. It has to make a fresh application at least 6 months prior to 31st March 2025 i.e. by 30th September 2024. The registration shall be granted by commissioner for period of 5 years after satisfaction of genuineness of activities and compliance of other laws. If he is not so satisfied, he shall afford an opportunity of being heard and subsequently, pass an order in writing rejecting such application and also cancelling its registration.

3. Provisional Registration or Approval

There has always been litigation between the income tax department and NGOs seeking registration, before the commencement of activities. The Finance Act 2020 introduced the concept of provisional registration for new charity institutions which are yet to start their charitable activities.

3.1 Timeline to file Application

The application for provisional registration has to be filed at least 1 month before the commencement of the previous year relevant to the assessment year from which the registration is sought.

3.2 Passing of Order

The registration under section 12AB or approval under section 10(23C) or 80G shall be granted for 3 years without any enquiries.

The order of registration shall be passed by the commissioner within 1 month from the end of the month in which the application for registration was received.

3.3 Conversion into Normal Registration

NGOs provisionally registered under section 12AB or approved under section 10(23C) or 80G shall be required to convert their provisional registration into normal registration at least 6 months before the expiry of the period of the provisional registration or within 6 months of commencement of its activities, whichever is earlier.

Example, A new charitable trust is seeking provisional registration for the Assessment Year 2022-2023. It is required to make an application for registration by 28 February 2021 i.e. 1 month before the commencement of the previous year relevant to the assessment year from which registration is sought. The registration shall be granted for 3 years without any enquiries by commissioner.

Author Bio

In view of the unprecedented economic crisis emanating due to the COVID-19 situation, CBDT has deferred the implementation of new procedure for approval/registration/notification of certain entities u/s 10(23C),12AA, 35 & 80G of IT Act,1961 from 1st June,2020 to 1st October,2020.