Residency Rule

√ Generally residential status can be of two types:

1. Resident

⇒ ROR

⇒ NROR

2. Non resident

Note: Condition of ROR and RNOR applies only to Individual and HUF

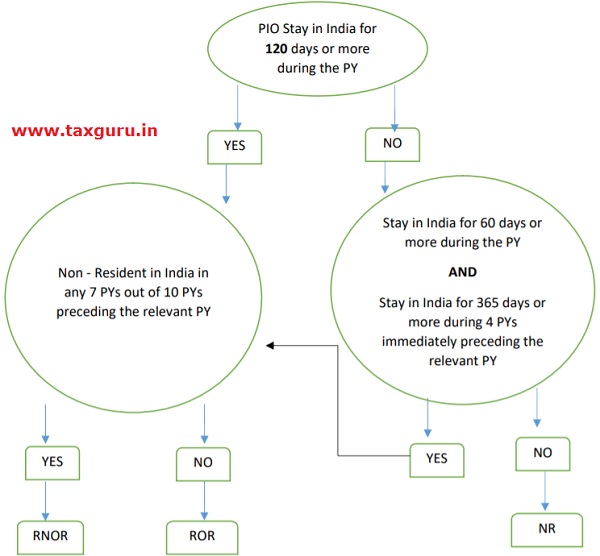

Residential Status of an individual

*NOTE: Here PIO =Person of Indian Origin

PY = Previous Year

ROR = Resident and Ordinary Resident

RNOR= Resident but Not Ordinary Resident

NR = Non Resident

AND = here AND means if any of one is NO – u have to go further in the line of NO.

Person of Indian Origin refers to Overseas Indians, officially known as Non-resident Indians (NRI/NRIs) .

Now as per Income tax act a person shall be deemed to be of Indian origin if he or either of his parents or any of his grandparents was born in undivided India. Example: if a person is born in New York City but his parents were born in INDIA then he will be POI.

Residential Status of an HUF/Firm/ AOP

√ CRITERIAS TO BE VERIFIED

It’s Control of Management Wholly OR Partly in INDIA

⇒ Yes ⇒ RESIDENT

⇒ NO ⇒ NR

Hence whether HUF is ROR or RNOR will be determined with the individual residential Status of KARTA of HUF.

If Karta is ROR then HUF is ROR and if Karta is NROR then HUF is NROR.

Residential Status of a Company

√ CRITERIAS TO BE VERIFIED

Is it Indian Company?

⇒ Yes ⇒ RESIDENT

⇒ NO ⇒ Whether It’s Control of Management Wholly OR Partly in INDIA ⇒ Yes ⇒ RESIDENT

⇒ NO ⇒ NR

Further it is to be noted that Non-resident shall not be required to file return of income if his or its total income consists of only dividend or interest income or royalty or FTS income (i.e. Fees from Technical Services) and TDS on such income has been deducted.

SCOPE OF TOTAL INCOME

| RESIDENTIAL STATUS | ROR | RNOR | NR |

| Income received in India | YES | YES | YES |

| Income deemed to be received in India | YES | YES | YES |

| Income accruing or arise in India | YES | YES | YES |

| Income deemed to accrue and arise in India | YES | YES | YES |

| Income received/accrued outside India from a business in India | YES | YES | NO |

| Income received/accrued outside India from a business controlled outside India | YES | NO | NO |

Author Bio