RECENT DEVELOPMENTS IN COMPANIES ACT, 2013

Amendment in Year 2019

Companies (Ordinance), 2019

Companies Amendment Act, 2019

Other Recent Amendments 2019

√ Dematerialization of Securities

√ Corporate Social Responsibility

√ National Financial Reporting Authority

√ Declaration of Commencement of business

√ Creation/ Modification of Charge

√ Significant Beneficial Owner

COMPANIES (AMENDMENT) act, 2019

Process for Approval of the Companies (Amendment) Act, 2019.

| Submission of Report by Committee of Government | August, 2018 |

| The Companies (Amendment) Ordinance, 2018 | 02nd November, 2018 |

| The Companies (Amendment) Ordinance, 2019 | 12th January, 2019 |

| The Companies (Amendment) Second Ordinance, 2019 | 21st February, 2019 |

| Approval of proposal to introduce Bill in Parliament by union cabinet | 17th July, 2019 |

| Placed before Lok Sabha | 25th July, 2019 |

| Passed by Lok Sabha | 26th July, 2019 |

| Passed by Rajya Sabha | 30th July, 2019 |

| Received Assent of President of India and become Act. | 31st July, 2019 |

IMPACT OF AMENDMENTS

√ Enlarging the jurisdiction of Regional Director.

√ Re-categorized of “Fine as Penalty”

√ De-clogging the NCLT

√ Corporate Governance relating Reforms.

PURPOSE OF AMENDMENTS

√ Simplification of Compliances and doing away with unnecessary procedures.

√ Lesser regulatory interference and greater self-Regulation

√ Clarity in the provisions of the Act.

√ Encouragement for Startups

√ Strengthen Corporate Governance Standard

√ Strict Action against defaulting Companies

√ Transparency

√ Investor Protection

A. Demat of Shares of Public Limited Companies:

The Ministry of Corporate Affairs in its drive to enhance transparency, investor protection and corporate governance, has notified Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2018 on 10th September 2018 effective from 02nd October, 2018.:-

Dematerialization:

-

- Dematerialization is the process of converting Physical Securities into electronic format.

- A Shareholder intending to dematerialize its securities needs to open a Demat account with Depository Participant.

- Investor Deface and surrenders his Physical Securities and in turn gets Electronic Shares in his Demat Account

Benefit of Dematerialization:

-

- Elimination of risk of duplication, theft, fraud and loss with respect to physical share certificates.

- Exemption from payment of stamp duty on transfer.

- Ease in transfer and pledge of securities.

Applicability:

Every unlisted public company with effect from 02nd October 2018 shall-

-

- Issue its securities only in dematerialized form; and

- Ensure dematerialization of all its existing securities

1Except:

This rule shall not apply to an unlisted public company which is:—

-

- A Nidhi;

- A Government company or

- A wholly owned subsidiary of public Company

Quick Bite:

Whether provision of Demat of securities applicable on Deemed Public Company also?

Major Impact on Company:

After 02.10.2018, Unlisted Public Company has to ensure that entire holding of securities of its Promoters, Directors, Key Managerial personnel is in dematerialized Form, otherwise company shall not be able to do followings:

- Issue of securities;

- Buy-back of securities;

- Issue of bonus shares; and

- Rights issue

After 02.10.2018, all new issue of securities or transfer of securities shall be only in Dematerialize form.

Impact on Security Holders (Transfer / subscription of Securities):

Rule 3 of the amendment specifies that every holder of Securities

- who intends to transfer securities or

- who intends to subscribe to any securities of an unlisted public company

has to make sure that all their existing Securities are held in dematerialized form before such transfer or subscription to the Securities;

Compliance Requirement by Public Company:

After amendment w.e.f. 02nd October, 2018, Public Companies must have to compliance with the following below mentioned compliances:

A. Make timely payment of Fees (admission as well as annual).

B. Maintenance of Security deposit of 2 years’ Fees, as per agreement executed with the followings:

-

- Depository;

- Registrar to an issue;

- Share Transfer Agent

C. Comply with the regulations, guidelines or circulars, if any issued by the Securities and Exchange Board or Depository from time to time.

Most Important Compliance Requirement:

Every unlisted public company governed by this rule shall submit Form PAS-6 to the Registrar with such fee as provided in Companies (Registration Offices and Fees) Rules, 2014 within sixty days from the conclusion of each half year duly certified by a company secretary in practice or chartered accountant in practice.

B. PROVISIONS IN RELATION TO CHARGES

(Creation/ Modification/ Satisfaction)

Creation/ modification of charge are one of crucial activity for Loan from Bank/ financial institutions etc. However, Companies (Amendment) Ordinance, 2018 have changed the period for Creation/ Modification of Charge with tighter time based norms:

Section Involved: Section 77 Duty to Register Charge

i. BEFORE ORDINANCE: As per Section 77 of Companies Act, 2013, Company has to create charge with the Registrar within 30 daysof creation of Charge.

Provided that the Registrar may, on an application by the company, allow such registration to be made within a period of Three Hundred Days of such creation on payment of such additional fees as prescribed:

Condonation: Provided further that if registration is not made within a period of three hundred days of such creation, “the company shall seek extension of time in accordance with section 87”

ii. AFTER AMENDMENT ACT, 2019: As per Section 77 of Companies Act, 2013, Company has to create charge with the Registrar within 30 daysof creation of Charge.

Provided that the Registrar may, on an application by the company, allow such registration to be made within a period of Sixty Days of such creation on payment of such additional fees as may be prescribed.

Additional Fees: For the charges created or modified on or after the 2nd November, 2018, the following additional fees or advalorem fees as the case may be, shall be payable with effect from 1st August, 2019

| S. No. | Period of delay | Small Companies and One Person Company | Other than Small Companies and One Person Company |

| 1. | Upto 30 days of Creation/ Modification of Charge | Normal Fees | Normal Fees |

| 2. | After 30 days up to 60 days | 3 times of normal fees | 6 times of normal fees |

Condonation replaced by Advalorem Fees: Provided further that if the registration is not made within the period specified—

The Registrar may, on an application, allow such registration to be made within a further period of further Sixty Days after payment of such ADVALOREM fees as may be prescribed

Additional Fees: For the charges created or modified on or after the 2nd November, 2018, the following additional fees or Advalorem Fees as the case may be, shall be payable with effect from 1st August, 2019

| S. No. | Period of delay | Small Companies and One Person Company | Other than Small Companies and One Person Company |

| 1. | More than 30 days and up to 120 days | 3 times of normal fees

PLUS An ad-valorem fee of 0.025 per cent. of the amount secured by the charge, subject to the maximum of one lakh rupees |

6 times of normal fees,

PLUS an advalorem fee of 0.05 per cent. of the amount secured by the charge, subject to the maximum of five lakh rupees”. |

Quick Bites:

If Charge is created after 02.11.2018 in such case

what shall be time period for filing of form for registration of charge with ROC.

If charge is created after 02.11.2018 in such case following shall be period for filing of charge form with ROC.

| STAGE | PARTICULAR | TIME PERIOD | Days | FEES |

| i. | Registration of Charge with ROC | Within 30 days of Creation | 0+30 | Normal Fees |

| ii. | If Fails to file with in 30, days | within a period of 60 days of such creation | 0+30+30

= 60 |

Normal Fees + 3 time Additional Fees |

| iii. | If Fails to file with in 60, days | Registrar may, on an application, allow such registration to be made within a further period of 60 days. i.e. 120 days of such creation | 0+30+30+60

= 120 |

Normal Fees + 3 time Additional Fees +Advalorem Fees |

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

if company fails to file form for creation/ modification of charge within 120 days of creation of charge. In such case whether company can file application for Condonation to Regional Director u/s 87.

As per Ordinance, 2018 there is modification in Section 87 of Companies Act, 2018.

| Before Ordinance | After Ordinance |

| The Central Government on being satisfied that—

(i) (a) the omission to file with the Registrar the particulars of any charge created by a company or any charge subject to which any property has been acquired by a company or any modification of such charge; or |

The Central Government on being satisfied that —

(a) the omission to give intimation to the Registrar of the payment or satisfaction of a charge, within the time required under this Chapter; or |

Note: After ordinance i.e. 02.11.2018 clause relating to Condonation of delay in creation/ modification of charge has been removed from Section 87.

Thus, one can opine that as per question no. II if company fails to file e-form CH-1 for creation / modification of charge within 120 from creation of charge then there is no way under Companies act for filing of such form with ROC.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

If Charge is satisfied before/ after 02.11.2018 in such case what shall be time period for filing of form for satisfaction of charge of charge with ROC.

If charge is satisfied even before or after 02.11.2018 in such case following shall be period for filing of e-form CHG-4 for satisfaction of charge with ROC.

| STAGE | PARTICULAR | TIME PERIOD | Days | FEES |

| i. | Satisfaction of Charge with ROC | Within 30 days of Satisfaction | 0+30

= 30 |

Normal Fees |

| ii. | If Fails to file with in 30, days | within a period of 300 days of such satisfaction | 0+30+270

= 300 |

Normal Fees + Additional Fees |

| iii. | If Fails to file with in 300, days | Filing of form with RD for satisfaction of Charge | 0+30+270+—-

= —— |

Normal Fees + Additional Fees +Condonation fees |

Note: Provisions for Condonation of delay in satisfaction of charge is still there in act even after ordinance.

C. Declaration of Commencement of Business

MCA has inserted New Section 10A after Section 10 by Companies (Amendment) Ordinance, 2018 Dated 02.11.2018 and same has been inserted in Companies (Amendment) Act, 2019.

As per 10A, a company having SHARE CAPITAL incorporated after ordinance i.e. 02.11.2018 shall not commence its business or exercise any borrowing powers unless,

- A declaration is filed by the directors in e-form Form No. INC-20A within 180 days from date of incorporation of company with ROC that ‘every subscriber to the MOA has paid the value of the shares agreed to be taken by him”.

Quick Bite:

a. Whether company incorporated without share capital need to file declaration in form INC- 20A?

As per Section 10A this declaration of commencement of business is required to file only by Companies having Share Capital. Therefore, Company not having share capital need not to file 20A.

b. A Company incorporates on or before 02.11.2018 whether needs to file e-form INC-20A with ROC?

Section 10A came into effect 02nd November, 2019 with prospective applicability.

Therefore, Companies incorporate before 02.11.2019 no need to file Declaration of Commencement of Business.

c. After filing of e-form INC-22A, whether ROC shall issue Certificate of Commencement of Business?

Let’s have some look on Background:

-

- There was section 149 in Companies Act, 1956 which required public Company to obtain certificate of commencement of business from ROC.

- In Companies Act, 2013 there was Section 11 which required every company to obtain certificate of Commencement of Business from ROC.

However, such section has been omitted w.e.f. 29th May, 2015 by Companies (Amendment) Act, 2015

-

- On 02.11.2018 Govt. has introduced Companies (Ordinance), 2018 and inserted section 10A “Declaration of Commencement of Business”.

Before 02.11.2018 there was sections for obtaining ‘Certificate of Commencement of Business” from ROC but section 10A states about “Declaration of Commencement of Business”.

Therefore, after filing of INC-20A Roc shall not issue any certificate of commencement of business. It is just an declaration from the Directors of Company.

d. Restriction before filing of e-form INC-20A?

-

- Company can’t Commence Business.

- Company Can’t exercise Borrowing Powers.

- Practically MCA system not allows filing any e-form with ROC.

e. What are the consequences if company fails to file form within 180 days?

Company can file such form INC-20A with Roc even after 180 days by paying additional fees as per fees rules. However, until unless form is not filed above mentioned restrictions shall be applicable on Company.

f. What are the consequences if company commences business without filing of INC-20A?

-

- Penalty on Company: the company shall be liable to a penalty of fifty thousand rupees.

- Penalty on Officer in Default: every officer who is in default shall be liable to a penalty of one thousand rupees for each day during which such default continues but not exceeding an amount of one lakh rupees

g. Whether subscription money can be received in cash from the subscribers of memorandum?

As per Companies Act, 2013 that subscription money must be received in Bank account of Company. Therefore, one can opine that Company can receive subscription money in cash also and book the same in books of accounts of Company.

Even as per section 269ST of Income Tax Act, a Company can accept maximum Rs. 200,000/- per day per person in cash.

h. What are the attachments of e-form INC-20A?

-

- In case of subscription money received in Bank Account, attachment shall be copy of Bank Statement.

- In case of subscription money received in cash, attachment shall be a declaration along with copy of books of account of Company.

i. What is the time period of issue of share certificate by the Company?

As per section 56, every company shall deliver the certificates of all securities allotted, transferred or transmitted within a period of two months from the date of incorporation, in the case of subscribers to the memorandum.

j. Section 10A allows company to receive subscription money within 180 days then how to comply with the provision of Section 56?

As per section 56: Company need to issue share certificate within 2 month of Incorporation of Company.

As per section 10A: Company can receive money within 180 days of incorporation of Company.

Note: In such case one can opine that whether subscription money received or not it is duty of Company to issue share certificates to subscribers of Memorandum of Association.

Maintenance of Registered office of Company

Addition of Sub – Section (9) after Section 12 Sub Section 8:

As per Section 12(1) A company shall, within thirty days of its incorporation and at all times thereafter, have a registered office capable of receiving and acknowledging all communications and notices as may be addressed to it.

By ordinance, 2018/ Amendment Act, 2019:

Registrar may do physical verification of the registered office of Company and if any default is found to be made in complying with provision of Section 12(1) (extract mentioned above). ROC may, initiate action for removal of name of Company (Strike off)

Compliance as per Section 12:

Every company shall—

(a) paint or affix its name, and the address of its registered office, in a conspicuous position, in legible letters, and

(b) if the characters employed therefore are not those of the language or of one of the languages in general use in that locality, also in the characters of that language or of one of those languages;

D. RE CATEGORIZED OF DEFAULT:

There is always confusion between “Fine and Penalties”. first see the meaning as per dictionary:

| Fine | Penalty |

| As per Oxford Dictionary

Fine is “a sum of money exacted as a penalty by a court of law or other authority?” |

As per Oxford Dictionary:

Penalty is “a punishment imposed for breaking a law, rule, or contract.” |

In General words, Fine imposed when any application/ petition filed with any court (like: NCLT, High Court) and penalty imposed when company made any non compliance and authority directly can impose penalty on them.

Quick Bites:

Many people having doubt whether ‘Additional Fees’ paid on filing of form is penalty or fine?

As per Rule 12 of The Companies (The Registered offices and Fees) Rules, 2014.

Additional fees are only a fees paid by Company for filing of form it is neither Fine nor Penalty.

Example: Section 92- Annual Return

Sub section 4: Every company shall file with the Registrar a copy of the annual return, within sixty days from the date on which the annual general meeting is held.

Sub Section 5: If any company fails to file its annual return under sub-section (4), before the expiry of the period specified therein, such company and its every officer who is in default shall be liable to a penalty of Rs. 50,000 and in case of continuing failure, with further penalty of Rs. 100 for each day during which such failure continues, subject to a maximum of five lakh rupees.

Therefore, one can observe that for one form Annual Return MGT-7 Company is paying additional fees and fine both in case company make any non compliance for filing of same.

Hence Proof, Additional fees are neither fine nor penalty.

The Companies (Amendment) Ordinance, 2018/ Amendment Act, 2019 has re categorized certain offence from Fine to Penalty. Thus, Registrar of Companies (ROC) and Regional Director (RD) can now impose penalties directly after issuing SCN, instead of going to judiciary for imposing fines or for following procedure for composition of offences.

There are as many as 16 sections amended via Ordinance, whereby the punishment for non-compliance to be levied under the Companies Act, 2013 is re-categorized from “FINE” to “PENALTY”

| S. No. | Section | Section Description |

| 1. | 53(3) | Prohibition of Issue of shares at a discount |

| 2. | 64(2) | Notice to be given to Registrar for alteration of share capital |

| 3. | 92(5) | Annual Return |

| 4. | 102(5) | Statement to be annexed to Notice |

| 5. | 105 | Proxies |

| 6. | 117(2) | Resolutions and Agreements to be filed |

| 7. | 121(3) | Report on annual general meeting |

| 8. | 137(3) | Copy of financial statement to be filed with Registrar |

| 9. | 140(3) | Removal, resignation of auditor and giving of special notice |

| 10. | 157(2) | Company to inform Director Identification Number to Registrar |

| 11. | 159 | Punishment for Contravention – in respect of DIN |

| 12. | 165(6) | Number of Directorships |

| 13. | 191(5) | Payment to Director for Loss of Office |

| 14. | 197(15) | Overall maximum managerial remuneration and managerial remuneration in case of absence or inadequacy of profits |

| 15. | 203(5) | Appointment of Key Managerial Personnel |

| 16. | 238(3) | Registration of the offer of scheme involving transfer of shares |

Example- Discussion on one of above section:

Section 117(2) – Resolutions and Agreements to be filed: As per this section Companies are required to file e-form MGT-14 with ROC for passing of resolutions mentioned u/s 117(3) within 30 days of passing of resolution.

| S. No. | Fine | Penalty |

| Company | Company shall be punishable with FINE which shall not be less than 5,00,000 rupees but which may extend to 25,00,000 rupees | Liable to PENALTY of 1,00,000 rupees and incase of continuing failure futher penalty of 500 rupees for each day upto maximum 25,00,000 rupees |

| Director | punishable with FINE which shall not be less than 1,00,000 rupees but which may extend to 5,00,000. | PENALTY of 50,000 and Incase of continuing failure with further penalty of 500 rupees for each day up to 5,00,000 |

Thus, before ordinance section 117(2) states about Fine and after ordinance section states about Penalty.

Therefore, before ordinance default can be make good by petition in NCLT by filing compounding application Suo Moto or after receipt of notice form ROC/ MCA.

And, After Ordinance ROC may start levying penalty by issuing ‘Show Cause Notice’ without any petition to NCLT or any other authorities.

E. CORPORATE SOCIAL RESPONSIBILITY:

Initially, the CSR provisions were codified and introduced by the Companies Act, 2013. CSR provisions as introduced imposed only a statutory obligation on the corporate to take social, environmental and economic initiatives for the society. The reporting of CSR being the only obligation.

I. Applicability to which CSR provisions applicable:

Following below mention companies are required to constitute CSR Committee, If Company having following during the immediately preceding financial year.

NET WORTH MEANING

As per Section 2(57), ‘NW’ = (Paid Up Share Capital + All Reserves Created Out of Profits + Securities Premium Account) – (Accumulated Losses + Deferred Expenditure and Miscellaneous Expenditure not Written Off).

II. CSR COMMITTEE

Constitutions of CSR Committee: Company to which CSR is mandatory should constitute a CSR Committee to undertake and monitor CSR activities:

The CSR Committee shall consist of 3 (Three) or more Director, out of which at least one director shall be an Independent Director.

-

- An Unlisted Public Company: This is covered under CSR provisions, but need not to have Independent Director on the CSR Committee.

- Private Limited Company: which is covered under CSR provisions

√ Need not have Independent director on the CSR Committee

√ Can have CSR committee with only Two Directors.

-

- In case of Foreign Company: The CSR committee should have at least Two person, out of which

- One person shall be specified under section 380(1)(d) of the 2013 Act and

- Another person nominated by the Foreign Company.

- In case of Foreign Company: The CSR committee should have at least Two person, out of which

III. NET PROFIT REQUIRE SPENDZING ON CSR ACTIVITY:

To ensure that at least 2% of average net profit of 3 immediately preceding financial years to be spent on CSR activities every year. Exp. For Financial Year 2019-20 Calculation: Average net profit of FY 2016-17, 2017-18 & 2018-19 needed to be considered.

Quick Bite:

a. Whether the average net profit criteria in section 135(5) is Net profit before tax or Net profit after tax?

The explanation to section 135(5) states that “average net profit” shall be calculated in accordance with section 198 of the Companies Act, 2013.

In terms of section 198(5)(a) in making computation of net profits, income-tax and super-tax payable by the company under the Income-tax Act, 1961 shall not be deducted. Therefore, the net profit criterion in section 135(5) is NET PROFIT BEFORE TAX.

b. If 3 years of incorporation not completed, whether provision of CSR can be applicable on Company?

Till now, there has been confusion about the amount of CSR expenditure to be incurred in cases where the company meets the CSR Criteria within 3 years of its incorporation. Now as per the amendments, if a company has not completed three financial years since incorporation, then also the company is obligated to spend 2% of the average net profit made during such immediately preceding financial years.

IV. ACTIVITY DOESN’T INCLUE IN CSR:

- Activities undertaken in normal course of business.

- Activity undertaken outside India.

- CSR projects or programs or activities that benefit only the employees of the company and their families shall not be considered as CSR activities.

- Contribution of any amount directly or indirectly to any political party under section 182 of the Act, shall not be considered as CSR activity.

- Activity not covered within schedule VII of the 2013 Act.

- One-off events such as marathons/ awards/ charitable contribution/ advertisement/ sponsorships of TV programmes etc. would not be qualified as part of CSR expenditure.

- Expenses incurred by companies for the fulfillment of any Act/ Statute of regulations (such as Labour Laws, Land Acquisition Act etc.) would not count as CSR expenditure under the Companies Act

V. IMPACT OF AMENDMENT ACT, 2019

- Addition of sub Section 6 in Section 135:

Till now, the company was not required to reserve the percentage of the CSR Expenditure in a separate account.

- Unspent amount relates to ongoing project: However, with the introduction of Sub-Section 6, the company is required to transfer the “unspent CSR expenditure pursuant to an ongoing CSR Policy project, to a special account within 30 days from the end of the financial year.”

√ Company shall open a special account called “Unspent Corporate Social Responsibility Account” in a scheduled bank.

√ Company need to spend such unspent amount within 3 financial years from the date of transfer.

√ Upon failure, to spend the amount the company will have to transfer such amount to a Fund specified in Schedule VII within 30 days from the date of completion of the third financial year.

Unspent amount doesn’t relates to any project: Then such amount is required to be directly transferred to a Fund specified in Schedule VII. The transfer is required to be done within 6 months of the expiry of that financial year.

VI. PENALTY:

Fine on Company: the company shall be punishable with fine which shall not be less than fifty thousand rupees but which may extend to twenty-five lakh rupees and

Fine on Officer in Default: every officer of such company who is in default shall be punishable with imprisonment for a term which may extend to three years or with fine which shall not be less than fifty thousand rupees but which may extend to five lakh rupees, or with both.

F. NATIONAL FINANCIAL REPORTING AUTHORITY (NFRA):

MCA vide its notification dated 13th November 2018 notified National Financial Reporting Authority (NFRA) Rules 2018.

A. Functions of NFRA:

- Recommend CG on formulation of AS and SA

- Monitor and enforce compliance of AS and SA

- Oversee quality of services rendered by professionals in context of above and suggest improvement measures

- It has also been given the power to investigate matters of professional misconduct by chartered accountants or CA firms, impose penalty and debar the CA or firm for up to 10 years.

The ICAI will continue to exercise these powers over small companies. The NFRA will have jurisdiction over listed companies and large, unlisted companies.

B. Companies cover under NFRA:

a) All Listed Companies/ Listed Body Corporate;

(in other words companies whose securities are listed on any stock exchange in India or outside India)

Body Corporate: body corporate” or “corporation” includes a company incorporated outside India,

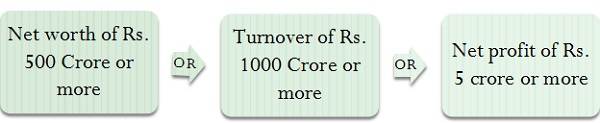

b) Unlisted Public Companieswith

– Paid up Capital or Loans > = INR 500 crores OR

– Turnover > = INR 1000 crores OR

– Outstanding Loan, Debentures and Deposit >= INR 500 crores

**Above Limits shall be check on as on the 31st March of immediately preceding financial year;

c) Following Companies

- Banking Companies

- Insurance

- Electricity Companies

- Special Act Companies

d) Body corporate; or Company; or Person on a reference made by CG in public interest.

e) Certain specific foreign Subsidiaries/Associates of Indian Companies

- A body corporate incorporated or registered outside India,

- which is a subsidiary or associate company of any company or body corporate incorporated or registered in India as referred to in clause (a) to (d),

- if the income or net worth of such subsidiary or associate company exceeds 20%, of the consolidated income or

- Consolidated net worth of such company or the body corporate, as the case may be, referred to in clause (a) to (d).

C. Companies Not cover under NFRA:

Considering the provisions of applicability of the Rules, following companies shall not be governed by the Authority:

1. Private Companies (unless referred by Central Government to the Authority in public interest); and

2. Unlisted public companies with paid-up capital or turnover or aggregate of loans, debentures and deposits below the limit stated under Rule 3(1)

D. Applicability of NFRA-1

1. It is not required to file by any Company.

2. It is not required to file by entities covered under 3(c) & (d)

3. However, if the Company “Which is listed above in pt (a) to (c)” has anybody corporate “Incorporated or registered outside India, which is a subsidiary or associate company of the Company and if income or networth of such subsidiary or associate company exceeds 20% of the consolidate income or consolidated net worth of such company or the body corporate then the form NFRA-1 is required to be filed by such existing body corporate

E. Compliance Requirements:

Existing body corporate: Initial One Time Disclosure

Every existing Body Corporate, other than a company, governed by these rules, shall inform the Authority within Thirty Days of the Commencement of These Rules, in Form NFRA-1, the particulars of the auditor as on the date of commencement of these rules.

- Everybody corporate formed in India and govern under these rules shall within 15 days of appointment of an auditor, inform the Authority about the particulars of the auditors appointed by the body corporate, inform NFRA-1;

Note: Indian Cos. are exempted from this requirement.

- Annual return – Every auditor referred to in rule 3 shall file a return with the Authority on or before 30th April every year in such form as may be specified by the Central Government

G. POWER OF COMPOUNDING:

1. COMPOUNDING OF OFFENCE– SECTION 441:

Before Amendment Act, where the maximum amount of fine which may be imposed for such offence does not exceed Five Lakh Rupees, compounding shall be done by the Regional Director (Power of RD to compound offence punishable upto Rs. 500,000/-) and if fine exceeds Rs. 500,000/- then compounding shall be done by NC LT.

By Amendment Act, 2019: where the maximum amount of fine which may be imposed for such offence does not exceed Twenty five lakh rupees, compounding shall be done by the Regional Director, (Power of RD to compound offence punishable increased upto Rs. 2,500,000/-) and if fine exceeds Rs. 2,500,000/- then compounding shall be done by NC LT.

| Power of RD | Power of NCLT | |

| Before Amendment Act | If offence punishable up to Rs. 500,000/- | If offence punishable more than Rs. 500,000/- |

| After Amendment Act | If offence punishable up to Rs. 2,500,000/- | If offence punishable more than Rs. 2, 500,000/- |

H. CONVERSION OF PUBLIC COMPANY INTO PRIVATE COMPANY:

After mandatory applicability of provision of Demat on Public Companies. Many closely held public Companies have started to get themselves convert into Private Limited Companies. Even Private Limited Company having many exemptions under Provision of Companies Act. (Exemption given by 2 circulars vide notification dated 05th June, 2015 and 13th June, 2017)

As per Section 14(1)- for conversion of Public Company into Private Limited Company approval of Tribunal is required.

4By Amendment Act, 2019: Power of Tribunal has been transferred to Central Government. Therefore, after notification of ordinance Public Company can be converting into Private Company with approval of Central Government.

Power of Central Government assigned to Regional Director for approval of conversion of public limited company into private limited company.

STEPS:

i. Hold Board Meeting of Directors

ii. Hold General Meeting of Shareholders

iii. Drafting of application for filing with Regional Director

iv. Declarations by KMP or Directors i.e.

- The Company limits the number of its members to 200, andthat no deposit has been accepted by the Company in violation of the

Act and rules. - There is no non-compliance of Section 73 to 76A, 177, 178, 185,186 and 188 of Act an rules made thereunder

- That, No resolution is pending to be filed in terms of Section 179(3) and

- that the company never listed on stock exchange and if listed complied with the relevant provisions

v. Details of Creditors: There shall be attached to the application, a List of Creditors and Debenture Holders, drawn up to the latest practicable date preceding the date of filing of petition by not more than 30 days.

vi. Publication of News Paper Advertisement: The company shall at least Twenty One days before the date of filing of application.

vii. Filing of Forms:

- E form MGT-14 for filing of Special Resolution with ROC within 30 days of passion of Special Resolution.

- Filing of GNL-1 with ROC

- Filing of RD-1 with Regional Director within 60 days of passing of Special Resolution

- Form required filing with Roc: File e-form INC-28 with ROC within 30 days of confirmation of conversion of company from public to Private.

I. CHANGE IN FINANCIAL YEAR OF COMAPNY:

Financial Year”,

- in relation to any company or body corporate, means the period ending on the 31st day of March every year, and

- where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year, in respect whereof financial statement of the company or body corporate is made up:

Provided that where a company or body corporate, which is a holding company or a subsidiary or associate company of a company incorporated outside India and is required to follow a different financial year for consolidation of its accounts outside India, the Central Government may, on an application made by that company or body corporate in such form and manner as may be prescribed, allow any period as its financial year, whether or not that period is a year:

Substitution of First Proviso of Section 2 Clause 41: “Financial Year”

As per Companies Act, in case of Indian company having Holding/ subsidiary/ Associate Company situated outside india, it is allowed the change the financial year as per such company with the approval of Tribunal.

5By Amendment Act, 2019: Power of Tribunal has been transferred to Central Government. Therefore, after notification of ordinance financial year of Company can be changed with approval of Central Government.

Power of Central Government has been transferred to “Regional Director”. Application to Regional Director shall be File in e-form RD-1.

STEPS:

i. Hold Board Meeting of Directors

ii. Hold General Meeting of Shareholders

iii. Drafting of application for filing with Regional Director

iv. Application shall be accompanied by following documents:

- Copy of articles of association with proposed alterations

- Copy of Minutes of General Meeting (mentioning details of votes cast in favour or against)

- Copy of Attendance Sheet of General Meeting

- Copy of Minutes of Board Meeting.

- Certified true copy of Board Resolution.

- Power of Attorney or Memorandum of Appearance

- Details of any previous application made within last five years for change in financial year and outcome thereof along with copy of order, if any.

v. Filing of Forms:

- E form MGT-14 for filing of Special Resolution with ROC within 30 days of passion of Special Resolution.

- Filing of GNL-1 with ROC

- File Form RD-1 with the Regional Director with all the above mentioned annexure like:

√ MOA & AOA

√ General Meeting Minutes and Attendance Sheet

√ Copy of Board Minutes along with CTC of Board Resolution

Form required filing with Roc: File e-form INC-28 with ROC within 30 days of confirmation of change in financial year from Regional Director.

J. REGISTERED VALUER:

The Ministry of Corporate Affairs by Notification Dated: 18th October, 2017 has notified that Section 247shall come into force w.e.f. 18.10.2017.

1st February, 2019 onwards, any person who will possess the prescribed qualifications and pass the valuation examination conducted by the Designated Agency, shall be allowed to act as the Registered Valuers.

Who is Valuer?

“valuer” means a person registered with the authority in accordance with these rules and the term “registered valuer” shall be construed accordingly.

Functions of a Valuer.─

A valuer shall conduct valuation required under the Act as per these rules and he may conduct valuation as per these rules if required under any other law or by any other regulatory authority.

As per this the Registered Valuer can do valuation under the following Acts/Regulations-

I. Companies Act, 2013

II. Insolvency Code, 2016 and

III. SEBI (REIT and InvIT) Regulations, 2016

Provisions under the Companies Act, 2013 which requires Valuation Report from a Registered Valuer:

| S. No. | Section | Particulars |

| 1. | 42 | Private Placement of Shares |

| 2. | 62(1)C | Valuation report for Preferential Allotment of Shares |

| 3. | 192(2) | Valuation of Assets Involved in Arrangement of Non cash transactions involving Directors |

| 4. | 230(2)(c)(v) | Valuation of shares, property and assets of the Company under a scheme of Corporate Debt Restructuring |

| 5. | 230(3) | Valuation report along with Notice of creditors/shareholders meeting –Under scheme of compromise/Arrangement. |

| 6. | 232(2(d) | The report of the expert with regard to valuation, if any, would be circulated for meeting of creditors/Members |

| 7. | 232(3)(h) | The Valuation report to be made by the tribunal for exit opportunity to the shareholders of transferor Company – Under the scheme of Compromise/Arrangement in case the Transferor company is Listed Company and the Transferee-company is an unlisted Company. |

| 8. | 236(2) | Valuation of equity shares held by the Minority Share Holders. |

| 9. | 260(2) (C) | Preparing valuation report in respect of shares and assets to arrive at the reserve price for company Administrator |

| 10. | 281(1) | Valuing assets for submission of report by liquidator |

QUICK BITE:

Who is eligible to do valuation of Securities under Companies Act or Income Tax Act ?”

To find out solution of above mentioned discussion, we have to go through following checks:

Check I: Mode of Allotment.

Check II: Whether Valuation required as per Company Law or Income Tax Act or Both.

Check III: If Valuation required, then who will do valuation as per Companies Act or Income Tax Act.

Allotment of securities can be done in following ways:-

1. Right Issue of Shares [Section 62(1)]

2. Preferential allotment of Share [Section 62(1)(c)]

3. Private Placement of Shares [Section 42)

A. Sections 62: RIGHT ISSUE OF SHARES

As per Section 62(1), A Company can issue and allot shares on Face Value irrespective of Net worth of Company. However, under Section 62 there is no requirement of Valuation of Shares. Therefore, one can opine that in case of right issue there is no need of Valuation Report.

Quick Bites:

I. In case of issue of shares on Premium under Right Issue of Shares, Whether Valuation report required?

-

- As per Companies Act

- As per Income Tax Act

Companies Act: There is no requirement of valuation report for right issue of shares under Companies Act, Irrespective of fact whether shares issue on Face Value or Premium.

Income Tax Act: As per Income Tax Act in case of right issue of shares, shares are issued to existing shareholders only in proportion to their shareholding. Therefore, no need of Valuation of Shares.

Therefore, one can opine that in case of right issue of shares whether on face value/ premium no need of Valuation Report as per Both Acts.

B. PREFERENTIAL ALLOTMENT OF SHARES:

As per Section 62(1)(c), for preferential allotment shares company have to follow rule 13 also. As per rule 13, “(g) the price of the shares or other securities to be issued on a preferential basis, either for cash or for consideration other than cash, shall be determined on the basis of valuation report of a registered value”

Therefore, one can opine that it is mandatory for preferential allotment of shares to obtain Report of Registered Valuer, irrespective of fact whether allotment made on Face Value/ Premium.

II. In case of issue of shares on Face Value/ Premium under Preferential Allotment Shares, Whether Valuation report required?

-

- As per Companies Act

- As per Income Tax Act

Companies Act: Irrespective of Fact shares allotted on Face Value or Premium. It is mandatory to obtain report of Registered Valuer for allotment of shares as preferential allotment.

Income Tax Act: As per Income Tax Act until unless shares are issued on premium there is no need of valuation certificate. However, if shares issued on premium then valuation report issued by registered Valuer shall be accepted here.

Therefore, one can opine that Valuation is mandatory for allotment of shares on preferential basis and report taken from registered valuer shall fulfill the purpose of both acts.

C. PRIVATE PLACEMENT OF SHARES:

As per Section 42, for preferential allotment Shares Company have to follow rule 14 also. As per section 42 price of security shall be determined by the report of Registered Valuer.

Therefore, one can opine that it is mandatory for Private Placement of shares to obtain Report of Registered Valuer, irrespective of fact whether allotment made on Face Value/ Premium.

III. In case of issue of shares on Face Value/ Premium under Private Placement of Shares, Whether Valuation report required?

-

- As per Companies Act

- As per Income Tax Act

Companies Act: Irrespective of Fact shares allotted on Face Value or Premium. It is mandatory to obtain report of Registered Valuer for allotment of shares as Private Placement.

Income Tax Act: As per Income Tax Act until unless shares are issued on premium there is no need of valuation certificate. However, if shares issued on premium then valuation report issued by registered Valuer shall be accepted here.

Therefore, one can opine that Valuation is mandatory for allotment of shares on Private Placement and report taken from registered valuer shall fulfill the purpose of both acts.

K. STRIKEOFF COMPANY – WITHOTU FILING ANNULA RETURN:

I. GROUNDS OF STRIKE OFF OF COMPANIES

-

- A company has failed to commence its business within one year of its incorporation.

OR

-

- A company is not carrying on any business or operation for a period of two immediately preceding financial years and has not made any application within such period for obtaining the status of a dormant company under section 455

II. BRIEF PROCESS OF STRIKE OFF

Application shall be made in eform STK-2 (fee Rs.10,000/-). Following below mentioned documents will be attached in the Form STK-2.

i. NOC from the appropriate concerned authority, if required (RBI, IRDA, Housing Finance, SEBI etc.)Rule 4(2)

ii. Indemnity Bond from Every Director in Form STK-3

iii. Statement of Accounts certified by CA. Statement should not be older than 30 days from the date of application.

iv. An Affidavit from every Director in Form STK-4

v. CTC of Special Resolution duly signed by each Director

vi. Statement regarding pending litigations, if any, involving Company. (Better to give in affidavit format)

QUICK BITE:

Many persons have query in mind that, where in Section 248 it is mandatory to file e-form AOC-4 and MGT-7 before filing of strike off?

There is amendment in rule 4 of Companies (Removal of Name of Companies) rules, 2016 w.e.f. 8th May, 2019 i.e “no application in Form No. STK-2 shall be filed by a company unless it has filed overdue returns in Form No. AOC-4 (Financial Statement) or AOC-4 XBRL, as the case may be, and Form No. MGT-7 (Annual Return), up to the end of the financial year in which the company ceased to carry its business operations”

Therefore, after amendment in Rule 4 w.e.f. 08th May, 2019 it is very clear that annual filing of AOC-4 and MGT-7 is mandatory up to the end of the financial year in which the company ceased to carry its business operations.

In other words, Company is required to file AOC-4 and MGT-7 up to financial year till company carries its business and operations.

L. DISQUALIFICATION OF DIRECTOR– SECTION 164:

Addition of clause (h) in Section 164(1)

As per Section 165, No person, after the commencement of this Act, shall hold office as a director, including any alternate directorship, in more than twenty companies at the same time.

By Amendment Act, 2019: If default made in Section 165, then director shall be considered as disqualified under Section 164. “Breach in Maximum no of Directorships to be a Ground for Disqualification.

Author Bio

Dear Sir,

I have one query:

Can we accept subscription amount in kind/asset. A valuation report can be provided as annexure.