The submission of MSME-1 is not only a requirement of the Companies Act, but it also has implications on the Income Tax Act and affects the statutory auditor of the company.

As a statutory auditor, it is necessary to include a report in the financial statement regarding the delay in payment to MSME vendors, as well as the provisions of the loan.

Even if a Company Secretary who is certifying the MGT-7 of a Company should mention the failure to file or incorrect filing of MSME-1 in the MGT-7 as non-compliance.

BACKGROUND:

As per section 405(1) of the Companies Act, 2013 and as per para 3 of the Specified Companies (Furnishing of Information about payment to Micro and Small Enterprise Suppliers) Order, 2019, every company shall file a return as per MSME Form I:

- By 31st October for the period from April to September and

- By 30th April for the period from October to March

Non-compliance of Section 405(1) is liable with penalty u/s 405(4) i.e. such company shall be liable to a penalty of INR. 20,000 /- and every officer in default shall be liable to a penalty of INR. 20,000 in case of continuing failure, with further penalty of INR. 1,000/- for each day during which such failure continues, subject to a maximum of INR. 300,000/-.

Analysis of order File No. ROC(B)/Adj.Ord.454-405/Samsung R&D /Co.No.35309/2023/ Date: 15.11.2023

ADJUDICATION ORDER IN THE MATTER OF SAMSUNG R&D INSTITUTE-INDIA-BANGALORE PRIVATE LIMITED

I. FACTS OF THE CASE:

a. The company was required to file MSME-1 for the period April 2022 to September 2022 by October 31, 2022, and October 2022 to March 2023 by April 30, 2023, with ROC.

b. On July 25, 2023, the company filed both durations MSME-1 by making a default of 266 days and 85 days respectively.

c. Non-compliances of section 405 are calculated from November 01, 2022, to July 25, 2023 and May 01, 2023 to July 25, 2023 respectively for both delayed return filed.

II. ORDER:

Having considered the facts and circumstances of the case, and after taking into account the factors above, I hereby impose penalty as under

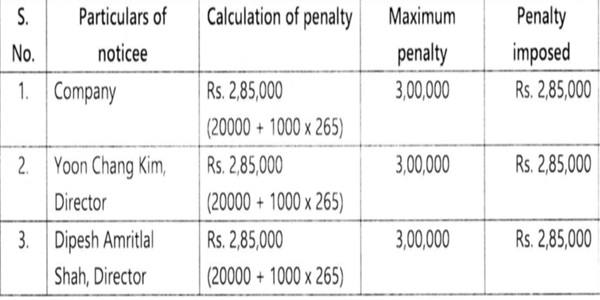

Default Instance I: November 01, 2022, to July 25, 2023 – Delay of 266 days.

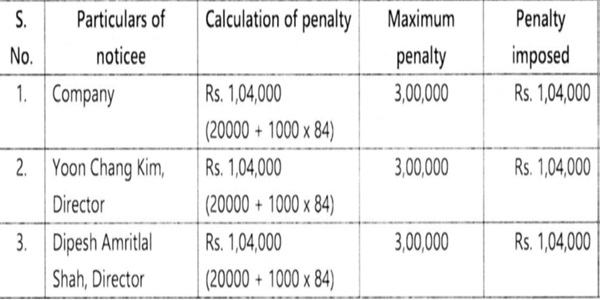

Default Instance II: May 01, 2023 to July 25, 2023-Delay of 85 days

CONCLUSION:

The ROC Karnataka made a commendable decision to take action against companies who deliberately fail to comply with Section 405 and do not take the requirements of the Companies Act seriously. We, as professionals from all the ROCs in the country, suggest that action be taken and notices of adjudication be issued against companies that are not adhering to the compliance requirements of the Companies Act.

****

Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com).

Author Bio