To have an independent portfolio of work is advantageous and a boon for any freelancer. However, along with it comes the added cautiousness of legal compliances, of which, most of us are completely oblivious to. The chord is struck only when you receive dreadful notices of tax penalties from Tax Authorities. Have you received any such notices as of yet?

Let’s bust some myths and have a closer look to know when GST is attracted, and what all

we measures we should take.

Are freelancers required to obtain registration under the GST Act?

GST Registration is required only when there is:

- Services are delivered outside India

- Gross Receipts (Without deduction of expenses) for services provided are greater than Rs.20 Lakh (Rs.10 Lakhs for Special Category States).

- Every person who is registered under an earlier Service Tax law needs to register under GST, too.

- Those paying tax under the reverse charge mechanism

- Person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered taxable person.

- a non resident person who is making any kind of taxable supply in the taxable territory then he has to take compulsory registration

- when he make taxable supply of services on behalf of other taxable persons whether as an agent or otherwise

Also Read- Compulsory Registration under GST

What are the applicable tax rates for freelancers?

A GST rate of 18% is applicable in most freelancing services. For example, Vaishali designs a campaign for Veet, for which she charges Rs.10,00,000. In this case, she shall issue an invoice for Rs.11,80,000 (18%*10,00,000 + 10,00,000)

What is Input Tax Credit and can a freelancer avail it?

We shall understand the concept of Input Tax Credit with the following example:

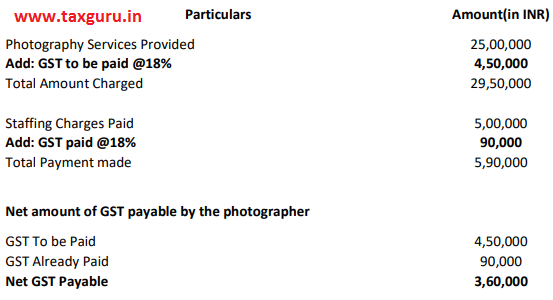

Suppose a freelancer photographer charges Rs.25,00,000 for the services carried, had hired a staff for which he had born expenses to tune of Rs.5,00,000.

In this case, the net GST payable shall be computed as follows:

The above case relates to a freelancer that has been providing services only in India. What happens in case he offers such services outside India? Such services fall under the category of ‘zero rated supply of goods’ in which the following facilities available:

- One can deliver services by filing a bond or a Letter of Undertaking where he does not does not pay any tax. However, he can claim a refund of taxes paid on expenses incurred earlier.

- One may provide services and pay tax accordingly and claim refund on such tax paid. The same can be differentiated by an example below:

| paying Tax Liability as per the Act and taking a

Refund |

Signing a Letter of Undertaking | ||

| Particulars | Amount(in INR) | Particulars | Amount(in INR) |

| Photography Services Provided Outside India | 25,00,000

|

Photography Services Provided Outside India | 25,00,000 |

| Add: GST to be paid @18% | 4,50,000 | Total Amount Charged | 25,00,000 |

| Total Amount Charged | 25,50,000

|

||

| Refund of GST Availed | 4,50,000 | Staffing Charges Paid | 5,00,000 |

How should a GST Invoice generated by a freelancer look like?

A basic invoice generated by a freelancer must cover the following elements:

√ Name, Business Address, GST Number

√Invoice Serial Number

√ Date

√ Client’s Name, Address and GST Number (if applicable)

√ The particulars, value and total amount charged for the services offered

√ The applicable tax rate

√ Signature

Is a freelancer required to file GST Returns?

Every registered person is required to file GST Returns. A summary of such forms have been represented in the table below:

| Return Form | Eligibility | Contents of the Return | Frequency |

| GSTR-1

|

Where Annual Turnover* is up to Rs.1.5 crore | A detailed return of all the sales/

services made.

|

Quarterly |

| GSTR-1

|

Where Annual Turnover* is greater than Rs.1.5 crore | Monthly | |

| GSTR-3B | All Service Providers | It is a summary of all services provided, GST paid, Input Tax Credit Availed against such payments. | Monthly

|

| GSTR-9 | All Service Providers | Annual Return | Annual |

*Gross Receipts (Without deduction of any expenses)

GST is predominantly a new concept. Most people are tensed with the changes that have been brought with the introduction of GST. Do you have doubts which are still unanswered? Don’t worry, we’re there at your beck and call to resolve all your queries. You can contact Sakshi Jain at sakshijain.1995@outlook.com.

freelancer is working on upwork which is US registered company and provide all payment in USD for all work whether from indian client or foreign client. if freelancer is having receipt of morethan Rs.20 lakhs GST registration is required? and whether all payment received in USD considered as export of services?

Hi Everyone, Just saw that the content of the tables is not complete in the published article. In case you have any doubts, request you all to mail me. TIA

Please recheck…as per one notification of GST 10/2017 dated 13.10.2017 , there is no need to get registration when turnover of the service provider is below Rs. 20 lacs and he is doing interstate/export of supply of services.