CA Ashu Dalmia

Uploading of invoices and filing of returns has remained challenge since beginning of GST regime. GSTR 1,2 and 3 could not be implemented. Now the The government has released new return forms that businesses will have to file for paying goods and services tax from the next financial year 2019-20.

GST Council on 4th May, 2018 in its 27th meeting approved principles for filing of new return design based on the recommendations of the Group of Ministers on IT simplification. GST Council in its 28th meeting held on 21st of July 2018 in New Delhi, approved the new return formats and associated changes in law.

The new GST returns would be implemented on a pilot basis from April 1, and will be made mandatory from July 1, according to a decision by the GST Council. Option to file quarterly return is optional and need to be exercised at the beginning of Year. The periodicity of the return filing will remain unchanged during the next financial year unless changed before filing the first return of that year.

This article discusses about main features of new Normal monthly/quarterly return. Three returns have been put in public domain and available for download on https://www.gst.gov.in/.

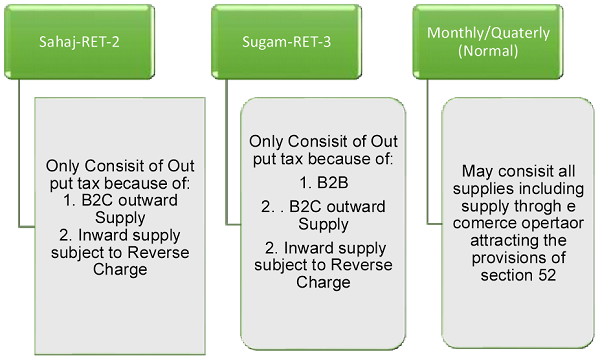

Businesses that have an annual turnover of up to Rs 5 crore have the option to file one of the three quarterly returns—Sahaj, Sugam and Normal. Tax in all cases will be paid on monthly basis. Following is the summary of returns proposed:

Limitations applicable to Shahaj and Sugam Returns:

- Cannot do supply through Ecommerce operator attracting provisions of section 52

- Can not take credit of missing Invoices

- Can do Nil Rated, Exempted or Non-GST supply, but not to be reported in these forms.

Normal Monthly/Quarterly return is most comprehensive return and has following structure:

Brief About Structure of Monthly/Quarterly (Normal GST Return) and Challan

| S. No. | Particulars | Description |

| 1. | Profile | Intimation of option for return periodicity and type of quarterly return |

| 2. | FORM GST ANX-1 | Annexure containing profile, questionnaire and 4 points with tables 3A to 3L and table 4 for details of outward supplies, imports and inward supplies attracting reverse charge. |

| 3. | FORM GST ANX-2 | Annexure auto populated for inward supplies containing tables 3A to 3C for inward supply, table 4 for summary of credits and table 5 for ISD credits. |

| 4. | FORM GST RET-1 | This is return containing details based on ANX-1, ANX-2, details not covered in said annexures, details of TDS, TCS, Interest, late fees, Payment of Taxes, Refund of cash ledger. |

| 5. | FORM GST ANX- 1A | Amendment to FORM GST ANX-1. |

| 6. | FORM GST RET1A | Amendment to FORM GST RET-1. |

| 7. | FORM GST PMT08 | Payment of self-assessed tax |

Profile

This is to choose periodicity (Monthly/quarterly) and type of return

(Sahaj/Sugam/quarterly-Normal) return. It consists of following questions:

- Was your aggregate turnover during the preceding financial year upto Rs. 00 Cr.?

- If reply is ‘Yes’ at Sr. No. 1, do you intend to file return on quarterly basis?

- If reply is ‘Yes´ at Sr. No. 2, choose your return –

√ Sahaj

√ Sugam

√ Quarterly (Normal)

GST ANX-1

This Annexure contains details of supplies creating output tax liability. It consists of outward supplies, Imports and inward supplies attracting reverse charge.

Before filing this annexure there are profiles in PART A and PARTB. Part B is required to be filled first time and will be required to file in subsequent periods only when there is some change in information filed in first/earlier Part B of profile. Information in Profile to be answered either Yes or No. Following are the information asked in Profile:

PART A:

√ I understand that the amount of tax specified in the outward supplies for which the details are being uploaded by me in this annexure shall be deemed to be the tax payable by me under the provisions of the Act.

√ Would you like to change the reply to the questions regarding nature of supplies as filled in the questionnaire of the return of the last tax period, if already filled in?

PART B:

| S.No. | Question | Relevant Table of GST ANX-I |

| 1. | Have you made B2C supply? | 3A |

| 2. | Have you made B2B supply? | 3B |

| 3. | Have you made exports with payment of tax? | 3C |

| 4. | Have you made exports without payment of tax | 3D |

| 5. | Have you made supply to SEZ units / developers with payment of tax? | 3E |

| 6. | Have you made supply to SEZ units / developers without payment of tax? | 3F |

| 7. | Have you made any supply which is treated as deemed exports? | 3G |

| 8. | Have you received inward supplies attracting reverse charge? | 3H |

| 9. | Have you made import of services? | 3I |

| 10. | Have you made import of goods? | 3J |

| 11. | Have you imported goods from SEZ units / developer on Bill of Entry? | 3K |

| 12. | Has your supplier not uploaded invoices on which you have claimed input tax credit (i.e. credit on missing invoices) two tax periods ago (for monthly) or previous tax period (for quarterly)? | 3L |

| 13. | Have you made any supply through e-commerce operators on which tax was required to be collected under section 52? | 4 |

Information in FORM GST ANX 1 can be filed real time basis (Subject to two limitations), however recipient will get credit during a tax period on the basis of information uploaded by supplier up to 1 0th of month/quarter following the month/quarter for which recipient is filing return. This will be available irrespective of filing of frequency of return by the supplier.

Following are the limitation when information in GST ANX 1 cannot be filed:

√ Time limitation provided in proviso of section 39 of the CGST Act. As per proviso of section 39 of the Act no rectification of any omission or incorrect particulars shall be allowed after the due date for furnishing of return for the month of September or second quarter following the end of the financial year, or the actual date of furnishing of relevant annual return, whichever is earlier.

√ Another restriction is that information cannot be filed in GST ANX I:

# Between 1 8th to 20th of the month following the tax period in case of monthly return

# Between 23rd to 25th of the month following the quarter in case of quarterly return filing.

Information pertaining to current system of returns (GSTR1 and 3B) if not reported in earlier period will be reported in new return subject to time limits of proviso to section 39 of the CGST/SGST Act. Following are the various possible scenarios:

# Document has not been reported in FORM GSTR-1 and tax has also not been accounted for in FORM GSTR-3B – In this case, document shall be uploaded, and tax shall also be paid along with applicable interest except in case of issuance of credit notes.

# Document has not been reported in FORM GSTR-1 but tax has been accounted for in FORM GSTR-3B– In this case, document shall be uploaded and adjustment of tax accounted for shall be made in of FORM GST RET-1.

# Document has been reported in FORM GSTR-1 but tax has not been accounted for in FORM GSTR-3B – In this case, uploading of the document shall not be required but adjustment of tax shall be made in table FORM GST RET-1

GST ANX-2

This Annexure will be auto populated containing details of inward supplies. This annexure will contain details of credit in following categories:

# Supplies received from registered persons including services received from SEZ units (other than those attracting reverse charge)-Table 3A

# Import of goods from SEZ units / developers on Bill of Entry-Table 3B

# Import of goods from overseas on Bill of Entry-Table 3C

# ISD Credits-Table 5

Table 4 contains summary of credits in Table 3A,3B and 3C with following bifurcation:

# Credit on all documents which have been rejected (net of debit /credit notes)

# Credit on all documents which have been kept pending (net of debit /credit notes)

# Credit on all documents which have been accepted (including deemed accepted) (net of debit/credit notes

Recipient can accept or reset / unlocked upto the 10th of the month following the month in which such documents have been uploaded by the supplier. After that take one of the following three actions can be taken by the recipient in GST ANX 2 on the basis of information uploaded by the supplier:

Accept: Accepted documents can not be amended by the supplier through Form GST ANX-I.

Reject: Rejected documents shall be conveyed to the supplier only after filing of the return by the recipient and edit can be done before filing any subsequent return for any month or quarter by the supplier. However, credit in respect of the document so edited or uploaded shall be made available through the next open FORM GST ANX-2 for the recipient.

Pending: These invoices will not available for amendment and would be rolled over to Form GST ANX-2 of the next tax period.

Status of return filing (not filed, filed) by the supplier will also be made known to the recipient in FORM GST ANX-2 of the tax period after the due date of return filing is over.

If there is no data in both ANX-1 and ANX-2 Nil return can be filed by choosing the option of NIL Return.

GST RET-1

GST RET 1 will contain all details of ANX-1 and ANX-2. Other details like Advances, Supplies with No GST liability, Reversal of Credits, TDS, TCS, Interest, late fees, Payment of taxes and Refund from electronic cash ledger will be filled manually. Following is the summary of information in GST RET-1:

| Table No. | Table no | Description |

| 1. | GSTN | |

| 2. | Legal Name, Trade Name, ARN, Date of ARN | |

| 3. | Summary of Outward Supply and Supplies containing Output Tax | |

| 3A | Details of Outward Supplies containing 8 tables for various transactions and 9th table for subtotal of table 1 to 8. | |

| 3B | Details of Inward supply containing two tables for transaction details and 3rd table for subtotal. | |

| 3C | Details of Debit Notes, Credit Notes, Advances Received, Adjusted and reduction in output liability in 5 tables and 6th table for subtotal. | |

| 3D | Details of Exempt, Nil rated, Outward Supply subject to reverse charge and Supply of goods from SEZ to DTA on Bill of entry containing 4 tables and 5th table for subtotal. | |

| 4. | Detail of inward supply and ITC | |

| 4A | Details of ITC based upon ANX -2, provisional credits and adjustment due to credit notes in 11 tables and I table for subtotal. | |

| 4B | Reversal of ITC in 5 tables and 1 table for subtotal. | |

| 4C | Net ITC based upon 4A and 4B | |

| 5. | Details of TDS and TCS available in cash ledger in 2 tables and I table for total. | |

| 6. | Interest and late fees payable in 5 tables and I table for total. | |

| 7. | Details of payment of taxes by cash and credit in 4 tables and one table for total. | |

| 8. | Refund claimed from cash ledger in 4 tables and one table of total. | |

After 8 tables as explained above last 9th point in the form is for verification by authorised person.

FORM GST ANX-IA will be used for amendment in FORM GST ANX-I and FORM GST RET-1A will be used for amendment in GST RET-1.

(Author is associated with Ashu Dalmia & Associates, Chartered Accountants and can be reached at ashu.dalmia@ada.org.in)