Recently, My Father in law was hospitalised and had a surgery. Strangely, all visitors asked “Do you hold a Health Insurance? Expenses are covered nah?”

Listening to this I had decided that my next article had to be on Health Insurance. So in this ‘Thoughtful Thursday’ we are covering everything you want to know about health Insurance

Health Insurance

Health insurance is a type of insurance coverage that pays for medical and surgical expenses incurred by the insured. Health insurance can reimburse the insured for expenses incurred from illness or injury, or pay the care provider directly.

Need for Health Insurance

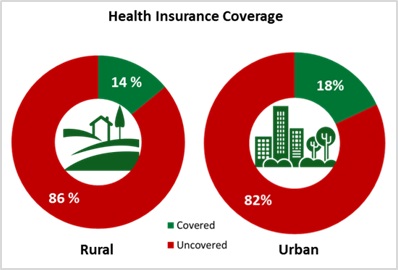

(Health Insurance Coverage in India:Stats from NSSO survey)

“Health is not valued till sickness comes”

Amidst the emotional turmoil and chaos, money flows like water. Firstly, the patient is suffering and secondly there is huge outflow of cash. At such times, one would want the patient be in a relaxed state of mind. However, this is not possible due to multiple stresses including emotional, physcial, financial, etc. One of the factor giving some relief to the patient is Health Insurance so that at least the financial burden is taken care of.

Actually the problem with Insurance is that you need it the most when you don’t have it.

Health Insurance or Mediclaim as it is referred to is available in various variants. Below is a quick summary of items to look at before buying a Health Insurance.

a) Amount of cover

Considering medical and hospitalisation costs I believe at the minimum Rs 20-25 lakhs of health insurance is required for a family of 2 adults and 2 children living in metro cities.

Myth – Some people believe that right now a Cover of Rs 5 lakhs is sufficient and later on we will increase it.

(In survey conducted by Nimit Wealth Management in our seminar, we found more than 50% have cover less than 5 lac and almost 35% people don’t have Health Insurance policy)

This is my personal experience, when my parents wanted to increase the Health Insurance cover the premium at their age was so high it was not financially feasible. Its my personal request and advise to each one reading this blog that keep a buffer at the beginning . If you believe Rs 5 – 10 lakhs is sufficient then you are overlooking the fact that inflation in medical industry is rising very fast.

Right now the additional premium of Rs 2,000 to 5,000 won’t matter but family will not suffer cash shortage at the time of Medical Emergencies.

b) Existing diseases

Myth – Some people believe that they are still young and medically fit and will not use the Health Insurance so they would purchase Health Insurance only when its required.

This is not true, we have heard of multiple events where young people were identified with some diseases out of the blue and what about accidents, it can cost you a bomb.

God forbid, if you are identified with some disease even as common as BP or Diabetes and then if you buy a Private Insurance those diseases will not be covered for the Gestation Period (generally, three years) and the Health Insurance Premium Amount will be higher.

We buy a protective case and cover for our Rs 20,000 mobile but we think twice before buying a Health Insurance for ourselves. Think Again..!

c) Employer provided Insurance

Myth – Some people believe that the Health Insurance provided by Employer is enough and they would not need any additional Health Insurance cover.

Well, that would be true ‘Only if’ you have decided that you are going to work for the same Employer for life!

Point to note is that (a) the amount of cover provided by Employers is generally not sufficient and (b) as discussed above, if you buy policy after diagnosis of any disease those diseases will not be covered for the Gestation Period (generally, three years) and the Health Insurance Premium Amount will be higher.

d) Other covenants

Check all the covenants and fine print. Especially the sub limits, room rent capping clause, maternity expenses coverage clause which may reduce your claim significantly. Go for policies which do not have such capping clauses.

Always Remember, buying a Health Insurance is like buying a Fire Extinguisher.

1. You wish that you will Never have to use it.

2. You don’t ask for a refund when it expires. You refill (renew) it.

3. If need be it will help you and your family in time of difficulty.

In this Literate India, Financial Literacy is very less..

Share this article and Thoughtful Thursday Series and help us in our mission to spread Financial Literacy in India.

CA Nitesh Buddhadev

CA Mitsu Buddhadev

Nimit Wealth Management

For feedback or suggestions, you may reach out to us at info@nimitwealthmanagement.com

Most of the Pvt companies dont have room rent sub limit clause

There are many other factors needs to be considered and it depends upon individual’s preference like OPD cover, Maternity Cover etc..

You can go for Cigna TTK, Start health, Apollo Munich, Etc..

Respected Sir,

Let me know the name of policy and insurance company which does not have such clasuses:

Check all the covenants and fine print. Especially the sub limits, room rent capping clause, maternity expenses coverage clause which may reduce your claim significantly. Go for policies which do not have such capping clauses.