WHAT IS A WORKS CONTRACT?

Works Contract is

* a composite contract

* where there is transfer of property in goods along with supply of services

* which are interrelated with each other.

* An agreement of building, construction, manufacture, processing, fabrication, erection, installation, repair or commissioning of any movable or immovable property may be called a works contract.

TAXABILITY OF WORKS CONTRACT UNDER PREVIOUS TAX REGIME

- Various provisions were in place to separately determine the value of taxable goods and taxable services in the total consideration of a works contract.

- VAT was charged on the value of sale of goods component and Service Tax was charged on the value of service component

- Cascading effect of different taxes. For Eg. Software

- Confusions and legal disputes

- WORKS CONTRACT HAS BEEN DEFINED IN SECTION 2(119) OF CGST ACT,

- contracts involving constructions of immovable properties are only kept within the purview of works contract under GST Law

- A contract in relation to movable property, however, would be treated as a ‘composite supply’ of goods or services depending on the principal supply.

( WORKS CONTRACT IS NOT A WORKS CONTRACT IN GST IF IT RESULTING IN MOVABLE PROPERTY)

IMMOVABLE PROPERTY

– GST Law recognizes only two classes of Immovable property.

– Sch III Entry 5-

a)Land &

b)Building (other than under construction sale of flats/unit)

SCHEDULE II OF THE CGST ACT, 2017

- Schedule II of the CGST Act, 2017, deals with the classification of Activities into Supply of Goods and Services.

- Entry number 5(b) of Schedule II mentions clearly that the “construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly…” will be treated as a Supply of Service.

Rate of construction services where value of land is included:

| Ch | Sec | Heading | Description of service | Rate |

| 99 | 5 | 9954 | (i) Sale of under construction flats involving transfer of property in land or undivided share in land | 18% after deduction of 1/3rd of total amount charged as the value of land or undivided share in land |

- Further, Entry number 6(a) of Schedule II reads as follows: “The following composite supplies shall be treated as a supply of services, namely:—(a) works contractas defined in clause (119) of section 2;”

Rate of Works Contract Service-

| Ch | Sec | Heading | Description of service | Rate |

| 99 | 5 | 9954 | ii) Composite supply of works contract as defined in clause 119 of section 2 of CGST, 2017. | 18% |

| (iii) Specified composite supply of works contract | 12% | |||

| (iv) construction services other than (i) and (ii) Above | 18% |

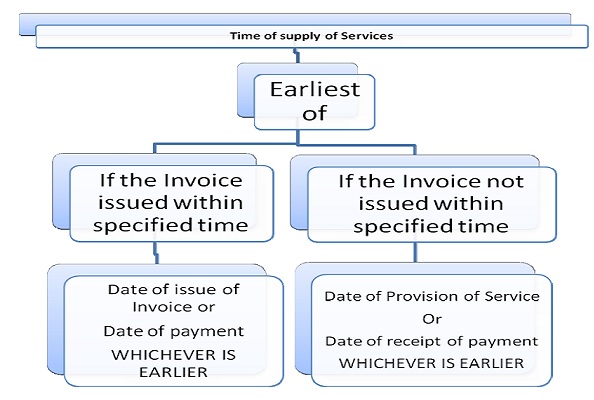

CONTINUOUS SUPPLY OF SERVICE

It means a supply of services which is provided or will be provided continuously or on recurrent basis under a contract for a period exceeding three months with periodic payment obligations

| Where the due date of payment is ascertainable from the contract | Time of supply shall be the due date of payment.. |

| Where the due date of payment is not ascertainable from the contract | Time of supply it will be earliest of

1)date of receipt of payment or 2)the date of issue of invoice |

| Where payment is linked to the completion of an event | Time of supply it will be earliest of

1)date of receipt of payment Or 2) completion of event where payment is linked to completion of event. |

TIME OF SUPPLY OF SERVICE

PLACE OF SUPPLY IN GST

- The place of supply of the service is the location of the immovable property.

e.g.If site is at New Delhi and office is at Gujrat. Immovable property is build up in New Delhi, hence It will be the place of supply of services.

INPUT TAX CREDIT ON WORKS CONTRACT UNDER GST

- Input Tax Credit of GST paid on Works contract will be allowed if

- the output supply is also Works Contract, and;

- When the Contract is for construction of Plant and Machinery.

Apart from the above two, no Input Tax Credit will be available for works contracts for construction of immovable property. For Eg- Hotel.

Input Tax Credits – Implications

| Procurement | Pre-GST position | Post-GST position |

| Materials | •No Cenvat of excise duty, CVD, etc paid on materials

• No VAT credit on materials |

Full ITC available |

| Input Services | Cenvat credit of service tax was available | Full ITC available |

| Capital Goods | Cenvat credit of excise was available in two trenches | Full ITC available in the year of receipt |

ABATEMENT AND COMPOSITION SCHEME

- No abatement is till now available for works contracts under GST.

- Works Contractor cannot opt for composition scheme as a works contract is treated as a supply of services.

- For supply of services, only restaurant business are allowed to be registered under Composition Scheme.

PRE & POST GST

| Particulars

|

Service Tax

|

VAT | TOTAL

|

GST

|

| Sale of Flats and Units- Under Construction | 4.50% | 1% | 5.50% | 18% (1/3 Reduction of Land) |

| Joints Development- Owner Area | 4.50% to 6% | NIL | 4.50% to 6% | 18% (1/3 Reduction of Land) |

| Rehabilitation of Flats | 6% | NIL | 6% | 18% |

ISSUES

Pre GST- Joint Development (Area Sharing)

Land Owner transfers certain percentage of development potential to Developer

In return Developer gives owners flat to Land Owner, also developer sales his developed flats to customers.

Present regime:

1. Service tax:

* Flats allotted to Land owner – service tax payable under works contract category or construction service on the value of development potentials received

* Saleable flats – service tax payable on sale of under construction units

2. VAT:

* Not payable on flats allotted to land owner as it amounts to barter

* Payable on saleable flats under construction

Post GST – Joint Development (Area sharing)

Taxability of flats allotted to Land Owner:

- Supply includes all barter and exchanges

- Flats allotted to land owner will be a taxable supply liable to GST where consideration is received in kind form of development potentials

- Time of supply:

* Receipt of development rights amounts to advance receipt of consideration in kind

* Hence, date when irrevocable rights are received will be time of supply

* Receipt voucher has to be issued by developer to owner on receipt of development right

- Valuation to be done as per GST Valuation Rules

- Taxable @ 18% or 18% (after deducting land value) depending on facts of the case

- Area Sharing Agreement- Section 7(1) a, “ Supply Means” Supply made and Agreed to be made

Taxability of saleable flats:

- Taxable on transaction value under construction service category @ 18% (after deducting land value)

Taxability of development rights in the hands of owner

- Transfer of development rights by landlord can be said in course or furtherance of business

- As per Sch II Entry (2) License to occupy land to builder is supply

Refund to customer on cancellation

Present regime:

- Rule 6(3) of Service tax Rules, 1994 permits Builder to adjust service tax refunded to customer on cancellation of flats/ units against his tax liability of the month in which refund is made

- No time limit for such adjustment

GST regime:

- Whether builder is entitled to issue credit note u/s 34 and claim the tax adjustment? Provision speaks of deficiency of service and not “non-provision of service”

- Does this mean that adjustment of GST refunded on advance against GST liability is not permissible?

- Section 54(8)(c) permits refund of tax paid on supply which is not provided either wholly or partially

Debit note and Credit note in Works Contract- DN and CN should be issued by supplier only U/s 34 of GST Act

Sale of Completed flats – Reversal of ITC

- Section 17(2) provides that where goods or services are used partly for effecting taxable supplies and partly for exempt supplies, ITC credit attributable to taxable supplies can only be taken

- Exempt Supply is defined u/s 2(47)] to include non-taxable supply

- Non-taxable supply is defined u/s 2(78) of the Act to mean:

- Supply of goods or services or both

- Which is not liable to tax under CGST or IGST Act

- Section 17(3) specifically includes sale of building and sale of land as exempt supply

- Sale of completed flat will be exempt supply for the purpose of reversal of ITC u/s 17(2) of the Act from start of the project.

- Also builder may liable to pay interest on such reversal of credit for the period starting from the date of completion certificate till date of actual reversal.

Free Supplies by the Builder to the contractor

- A supply without consideration to non-related persons is not “supply” as defined u/s 7 of CGST Act

- As such activity is not a supply, same will not be liable to GST

- It is not an exempted supply as defined u/s 2(47) of CGST Act

- It is not wholly exempt u/s 11 of CGST Act

- It is not a Nil rated supply

- It is not a non-taxable supply as defined u/s 2(78) of CGST Act

ITC reversal may not be required

ITC Overflow- Refund

Not allowed in capacity of builder. Builder can use overflow credit,

- In other project as set off or

- Get Income tax deduction as write off to Profit and Loss account.

Subcontract of construction

Subcontractor are not works contractor but composite supplier. Hence ITC overflow is not applicable to subcontractor he will get refund.

Impact on ongoing projects

The provisions relating to treatment of ongoing contracts on appointed day are contained in Section 142 (10) and 142 (11) of the CGST Act 2017

1) If the goods or services are being supplied on or after the appointed date in pursuance of the contract entered prior to the appointed date, then tax would be levied under GST.

2)If the goods or services are supplied before the appointed date and VAT was leviable on such transaction on account of Sale of goods or Service Tax was leviable on account of provision of services, no tax will be required to be paid under GST.

3)If the consideration has been received prior to appointed date in respect of such supply and tax has already been paid under current regime, no tax would be required to discharged /paid under GST.

4) If any VAT and Service Tax has been paid on any supply under the existing laws, but the supply of goods and/or services is to be received under GST scheme, then the tax already paid shall be allowed as credit under GST and the supplies when made shall be taxed under GST as well. This clause covers specifically works contract transactions. For example: If an invoice is raised on 30th June 2017 and the supply is for the month of June 2017 and July 2017 and VAT and Service Tax have been paid, then such VAT and Service Tax paid shall be allowed as credit in GST proportionate to the month of July 2017; and when supplies are made in July 2017, they shall be put to tax under GST.

IMPACT ON CONSTRUCTION AND REAL ESTATE SECTOR-

- Positive Impact

- Easy Compliance

- Availability of Input Tax Credit

- Possible reduction in prices

- Excise Duty, VAT, Service tax get replaced by GST

All labour suppliers get registered due to RCM provisions

Hlw queries h ye h:-

1st:- supposed that mai builder hu nd koi person muje 5,00,000 rupee deta h building bnane ke liye …. To us per gst rate kitna lagega jo bhi mai construction krne ke liye saman leta hu nd kya muje gst pay Krna pdega or muje ITC milega

2nd:- mai ek builder hu or mai land purchase ker usper ek building bnata hu nd use sold kr deta hu … To gst per kya effect hoga.

Hi Vivek,

Really informative article. I am wondering if you have updates on this after recent changes made in applicability of GST on construction and real estate viz. 5% GST without ITC. I would like to understand how the sector (construction cost) will be impacted due to this. Also, can you please throw some light of applicability of GST on TDR please?

Many thanks,

Mehul

I am Builder from Hyderabad and doing ventures on Joint development basis. In which the land owner provides me land and I develop that in to Residential apartments. When I sell the flats to prospective buyers I will collect the GST @12% of Sale agreement value. My doubt is about the GST on part of Land Owner. Whether he have to pay GST in the following cases. Case-1: If Land Owner sells the flats during construction and before receiving Occupancy Certificate, How much GST he has to pay? Case-2: In case Land Owner retains flats and he will not sell to any one, How much GST he has to pay? Case -3:After receiving the Occupancy Certificate what is the role of land owner share in paying of GST? Case -4: Whether builder has to extend the benifit of In put Credit to Land Owner?

I request you guide me and send the answers to my mail.

Hello reader you can also watch following video for extra information

https://youtu.be/YDrZP_SkRxQ

Sir,

We are Contractors providing Works Contract Services to sub-divisions of a Local Authority/Municipality (let’s call it ABC).

ABC is registered under GST and has a valid GST number.

Its sub-divisions (let’s call it EE) to which we actually provide such services are NOT registered under GST.

Payments have been received from EE for works completed before 01.07.2017 in the months of October-November 2017.

We had charged GST @ 18% on balance payments of such outward supplies (i.e. Works Contract Services supplied prior to 01.07.2017) by raising invoices with GST number of ABC for same in months of October-November 2017.

On the basis of such invoices, payments of such GST had been made to us after deducting our 3% DVAT liability (which they have not deposited with DVAT Department nor TDS certificate issued).

We have already submitted & filed our GSTR 3B for the month of October 2017 and acknowledgement number has also been received.

Outward tax liability has been adjusted with our available ITC.

Now, ABC is saying that it had erroneously paid us GST and would now be recovering the GST from us that it had paid to us for Works Contract Services supplied prior to 01.07.2017.

Option to revise GSTR 3B for month of October 2017 is not available.

And we are yet to file our GSTR 3B for the month of November 2017.

If we file GSTR 1 for October & November 2017 with invoice details issued to ABC, we will be at a huge loss since we will be paying GST on outward supplied from our own pocket and ABC will profit from same after claiming ITC of same and also recovering already paid GST from us.

Can we file GSTR 1 for October & November 2017 by showing outward supplies to EE (unregistered) under RCM i.e. we deposit the GST on outward supplies and also claim ITC for it?

Or is there any other solution to this problem?

Please help.