In the realm of Goods and Services Tax (GST), works contract services play a pivotal role in the construction and real estate sectors. Defined by Section 2(119) of the Central Goods and Services Tax Act, 2017, these contracts encompass diverse activities related to immovable property. This article navigates the complexities of works contracts, shedding light on their definition, taxability, valuation rules, and recent notifications. As the GST landscape continually evolves, understanding the nuances of works contract services becomes imperative for businesses and professionals operating in this dynamic and vital segment of the economy.

- What is works contract?

- As per the above definition following are the essentials of works contract:-

- Whether Works Contract is taxable under GST as supply of goods or supply of service?

- whether GST is payable on sale of land?

- valuation under GST

- Rate of GST

- Notification No. 4/2018 CENTRAL TAX (RATE) Dated 25.01.2018

- Explanation to the above notification:

What is works contract?

As per section 2(119) of Central goods and service tax Act,2017

“Works Contract means,

A contract for building, Construction, Fabrication, Completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods(whether as goods or in some other form) is involved in the execution of such contract.

As per the above definition following are the essentials of works contract:-

- Construction

- Fabrication

- Completion

- erection

- installation

- fitting out

- improvement

- Modification

- repair

- maintenance

- Renovation

- alteration or commissioning of any immovable property

- Wherein transfer of property in goods is involved.

- Thus, from the above it can be seen that the term works contract has been restricted to contract for building construction, fabrication etc of any immovable property only.

- Any such composite supply undertaken on goods say for example a fabrication or paint job done in automotive body shop will not fall within the definition of term works contract under GST. Such contracts would continue to remain composite supplies, but will not be treated as a Works Contract for the purposes of GST.

- Rates of GST Pertaining to works contract will only applicable in respect of immovable property only.

Whether Works Contract is taxable under GST as supply of goods or supply of service?

- SCHEDULE II OF CENTRAL GOODS AND SERVICE TAX ACT,2017 provides for which activities to be treated as supply of goods or as supply of services.

- As per Para 6 (a) of Schedule II to the CGST Act, 2017, works contracts as defined in section 2(119) of the CGST Act, 2017 shall be treated as a supply of services

- construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

- That means, if the entire consideration is received after issuance of completion certificate or

- if the entire consideration is received after its first Occupation then NO GST

- Thus, there is a clear demarcation of a works contract as a supply of service under GST.

whether GST is payable on sale of land?

As per Schedule III of CENTRAL GOODS AND SERVICE TAX ACT,2017 sale of land is not liable for GST.

valuation under GST

- Valuation of a works contract service is dependent upon whether the contract includes transfer of property in land as a part of the works contract.

- In case of supply of service, involving transfer of property in land or undivided share of land, as the case may be, the value of supply of service and goods portion in such supply shall be equivalent to the total amount charged for such supply less the value of land or undivided share of land, as the case may be, and the value of land or undivided share of land, as the case may be, in such supply shall be deemed to be one third of the total amount charged for such supply.

Explanation. –

For the above purpose, “total amount” means the sum total of,-

(a) consideration charged for aforesaid service; and

(b) amount charged for transfer of land or undivided share of land, as the case may be.

Rate of GST

The rate of GST for Works Contract service has been prescribed in serial number 3 of Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017 as amended by Notification No. 20/2017-Central Tax (Rate) dated 22.08.2017 & notification no. 24/2017-Central Tax (Rate) dated 21.09.2017 and is as under:

| (i) | Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier. (Provisions of paragraph 2 of this notification shall apply for valuation of this service) | 9% CGST +

9% SGST |

| (ii) | composite supply of works contract as defined in clause 119 of section 2 of Central Goods and Services Tax Act, 2017 | 9% CGST +

9% SGST |

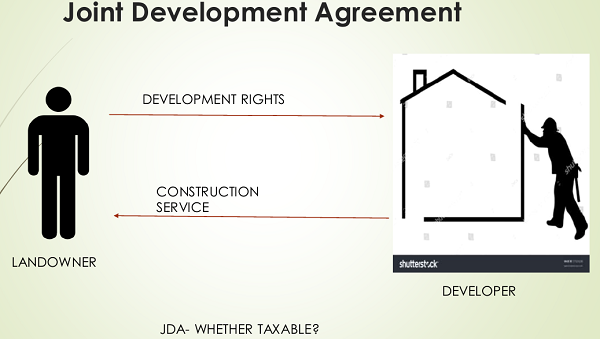

Notification No. 4/2018 CENTRAL TAX (RATE) Dated 25.01.2018

G.S.R……(E).- In exercise of the powers conferred by section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, hereby notifies the following classes of registered persons, namely :-

(a) registered persons who supply development rights to a developer, builder, construction company or any other registered person against consideration, wholly or partly, in the form of construction service of complex, building or civil structure; and

(b) registered persons who supply construction service of complex, building or civil structure to supplier of development rights against consideration, wholly or partly, in the form of transfer of development rights,

as the registered persons in whose case the liability to pay central tax on supply of the said services, on the consideration received in the form of construction service referred to in clause (a) above and in the form of development rights referred to in clause (b) above, shall arise at the time when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter).

Explanation to the above notification:

When GST Law was enacted as on 01.07.2017 it was not ample clear to the builders and developers as to whether the transfer of development rights attract GST ??

As It can be considered as a barter transaction, because Landowner is giving his land for development (Development rights)to the developer or builder in return of which developer providing construction service i.e, constructed area as a consideration to the landowner. And Barter transactions are supply U/s 7 OF CGST ACT,2017 hence, GST attract.

But, in between before publishing this notification in the official gazette landowner was not paying GST on development rights given to the developer as it is given in various decisions Chheda Housing Development Corporation vs. Bibijan Shaikh Farid (APPEAL NO.1081 OF 2005) (the “Hon’ble Bombay High Court”) that development rights are nothing but a benefits arising out of land

However, it would be important to consider the provisions of Section 3(p) of the Right to Fair Compensation, Transparency in Land Acquisition, Rehabilitation Act, 2013 (the “Fair Compensation Act”), which defines “land” as under:

““land” includes benefits to arise out of land, and things attached to the earth or permanently fastened to anything attached to the earth”

Hence, GST is not attracted.

Hence, for clearance on this issue government come up with this notification and attract GST on such type of transactions.

On which GST is payable when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter).

On valuation part on such type of transactions no clear calculations has not been provided from the government.

One more point this notification can be raised whether GST is applicable in case of revenue sharing agreements? As this notification is only relating to area sharing, it is not yet clear. But, one view can be taken if area sharing is taxable then revenue sharing is also taxable, needs more clearance on this part.

sir,

I have 1 doubt Mr.X has some 2500sqy land & Mr.Y has 1600sqy land. If they go individually for construction they will get 4 of 5 floors only. So they went for Joint construction for 15 floors. IN this case Mr.X will construct the building and Mr.Y reimburse the cost and this is commercial complex what is the Gst applicable for this case

sir,

if x is a builder and Y is a sub contractor of X on running progress bill payment basis then-

What will Y do for input of GST for raising his bills to X ( is it 12 % of services only ). Can Y get back GST on purchase of goods he has done before the billing period.

Who is liable to pay GST on Works Contract?? Whether such liability can be transferred to any other person. i.e. Flat Purchaser or any other person.

inputs of raw-material purchased like purchase of cement bricks etc can be taken as input tax under gst works contract

I am a builder and having all plots (Plotted development). I construct house at my own cost and then sell the house after taking completion certificate from nagar nigam. I do not book or sell under construction property. DO I REQUIRE GST REGISTRATION ?

is this gst rate is 12% now or 18%. please reply

If one Contractor gets the contract of Erection of Electric towers & line. Would it be covered under definition of works contract?

Whether Erected Electric Tower are considered immovable property?

usefull

CA Pooja Ji

one piece of land was registered in the name of a X. He formed a partnership by taking Y as partner. And land of X was taken as his capital contribution. They then developed the housing project over the said land. What is the consequence. Please advise.

Under GST regime, the earlier works contract tax @2% applicable for contracts exceeding the specified limit are those rules still in existence or abolished.