Question:

What is the need for the Place of Supply of Goods and Services under GST?

Answer:

The basic principle of GST is that it should effectively tax the consumption of such supplies at the destination thereof or as the case may at the point of consumption. So place of supply provision determines the place i.e. taxable jurisdiction where the tax should reach. The place of supply determines whether a transaction is intra-state or interstate. In other words, the place of Supply of Goods or services is required to determine whether a supply is subject to SGST plus CGST in a given State or union territory or else would attract IGST if it is an inter- state supply.

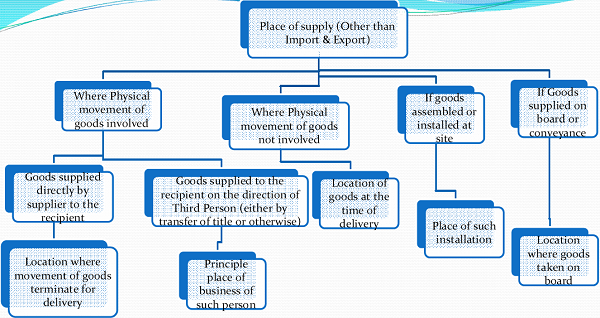

Place of Supply of Goods other than goods

imported into or exported outside india

Section (10)

√ In Case of goods imported into India, Place of supply shall be the location of importer.

√ In case of goods exported from India, place of supply shall be the location outside India.

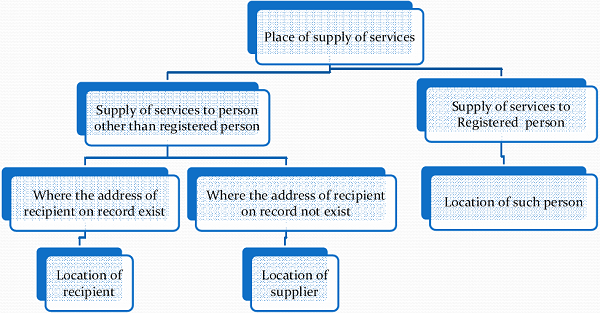

Place of Supply of services where location

of supplier & recipients is in India

Section (12)

√ This section shall apply where the location of supplier & recipient of service is in India.

√ The place of supply of services, except the services specified in sub-section (3) to (14) is as follows (i.e. General provision)

√ In case of immovable property

– If any service provided in relation to an Immovable property including services by architects, interior decorators etc or services provided by way of right to use of immovable property or construction work or by way of lodging accommodation by a hotel, inn etc including property for marriage function, social or official meeting etc.

→ If immovable property is located in India:- Place of supply shall be location of Immovable Property.

→ If immovable property is located outside India:– Place of supply shall be location of the recipient.

√ In case of restaurant and catering services, personal growing, fitness, beauty treatment, health service including cosmetic and plastic surgery, Place of supply shall be the location where services is actually performed.

√ In case of services in relation to training and performance appraisal, Place of supply shall be

→ If service provided to registered person:- location of such person

→ If service provided to other than registered person:- location where services are actually performed

√ In case of services provided by way of admission to a cultural,artistic, sporting, scientific, educational or amusement park or other place and service ancillary thereto.

→ Place of supply shall be where the event is actually held or where the park or such other place is located

√ In case of services provided by way of Organisation of a cultural, artistic, sporting, scientific, educational or entertainment event including supply of services in relation to a conference, fair, exhibition or service ancillary to organisation to any of the events or assigning of sponsorship to such events

→ If service provided to registered person:- location of such person

→ If service provided to other than registered person:– location where the event is actually held and If event is held outside India, then the place of supply shall be location of the recipient.

√ In case of service by way of transportation of goods, including by mail or courier, then the place of supply shall be

→ If service provided to registered person:- location of such person

→ If service provided to other than registered person:- location where passenger embarks for a continuous journey. If the point of embarkation is not known at the time of issue of right to passage, then general provision shall be applicable.

√ In case of passenger transportation services

→ If service provided to registered person:- location of such person

→ If service provided to other than registered person:– location where passenger embarks for a continuous journey. If the point of embarkation is not known at the time of issue of right to passage, then general provision shall be applicable.

√ In case of supply of service on board a conveyance including train, aircraft etc., place of supply shall be location of first scheduled point of departure of that conveyance for the journey.

√ In case of telecommunication service including data transfer, broadcasting etc.

→ If services provided by way of fixed telecommunication line, leased circuit, dish etc. :- Place of supply shall be location of recipient where such connection is installed.

→ In case of mobile connection provided on post-paid basis:- Place of supply shall be location of billing address of the recipient.

→ In case of mobile connection provided on pre-paid basis

– If supplied through selling agent or re-seller :– place of supply shall be address of such selling agent.

– If supplied to final subscriber :– Place of supply shall be where such pre- payment is received.

→ In other cases :- Place of supply shall be address of the recipient as per the records. If address is not available, place of supply shall be location of supplier of services.

If such pre-paid service is availed through internet banking or other electronic mode of payment, place of supply shall be location of recipient of services on records of the supplier.

√ In case of supply of banking or other financial services including stock broking service, place of supply shall be location of recipient of service on records of supplier. If location of recipient is not known, place of supply shall be location of supplier of services.

√ In case of Insurance services

→ If service provided to registered person:- location of such person

→ If service provided to other than registered person:- location of recipient of

Place of Supply of Services where location of supplier or location of recipients is outside india

(Sction 13)

√ This section shall apply where the location of supplier & recipient of services is Outside India.

√ The place of supply of services, except the services specified in sub- section (3) to (13), shall be location of recipient of services. In case location of recipient of services is not available, place of supply shall be location of supplier.

√ The place of supply of the following services shall be the location where services are actually performed :-

→ Services supplied in respect of goods which are required to be made physically available by the recipient to the supplier of service. If services provided from remote location by way of electronic means,

→ Services supplied wherein physical presence of recipient or person acting on his behalf.

√ In case of immovable property

– If any service provided in relation to an Immovable property including services by architects, interior decorators etc or services provided by way of right to use of immovable property or construction work or by way of lodging accommodation by a hotel, inn etc including property for marriage function, social or official meeting etc., Place of supply shall be the location where such property is located or intended to be located.

√ In case of services provided by way of admission to a cultural, artistic, sporting, scientific, educational or amusement park or other place and service ancillary, place of supply shall be the location where the event is Jactually held.

√ If any of the above mentioned specific services under sec 13 is supplied at more than one location including taxable territory, place of supply shall be the location in taxable territory.

√ The place of supply of the following services shall be the location of supplier of services :-

→ Services provided by banking company, NBFC etc to account holders

→ Intermediary services

→ Services consisting of hiring of means of transport, including yachts but excluding aircrafts and vessels, up to a period of one month.

√ In case of transportation of goods, other than mail or courier, place of supply shall be the place of destination of such goods.

√ In case of Passenger transportation services, other than mail or courier, place of supply shall be the place where passenger embarks for continues journey.

√ In case of supply of service on board a conveyance during the course of a passenger transport operation, place of supply shall be first scheduled point of departure of that conveyance for the journey.

√ In case of online information and database access or retrieval services, place of supply shall be the location of recipient of services. (Refer sec 13(12) & sec 14 for detailed knowledge).

Yadi koi vyakti ka Firm ya company Uttar Pradesh ke bahar kisi anya Pradesh me registered hai aur wah vyakti ya firm apne Veh. Ka repair maintenance Uttar Pradesh me karwata hai to uska repair & maintenance ke bill par SGST AUR CGST LAGEGA ya IGST jabki goods aur Service ka place of supply Lucknow Uttar Pradesh me hai