There could be a situation where one entity is having significant influence over the other by holding some portion of equity capital (assuming other conditions are met) and at the same time the other entity also having significant influence over the first entity by holding some shares.

Ind-As 28 “Investment in Associates and Joint Ventures” defines certain important definations which can be read as below –

Para 3 defines Associates as “Associates is an entity over which the investor has significant influence” ;

Para 3 defines Significant Influence as “Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control of those policies;

Para 3 defines that Equity Method as “The equity method is a method of accounting whereby the investment is initially recognised at cost and adjusted thereafter for the post-acquisition change in the investor’s share of the investee’s net assets. The investor’s profit or loss includes its share of the investee’s profit or loss and the investor’s other comprehensive income includes its share of the investee’s other comprehensive income.”

Now,

A question comes as mentioned above what would be the share of profit to use to pickup as equity portion in case of such cross holding situations. Standard does not talk about specifically about such cross holdings; however one can read the definition of Equity method where standard states that “Investor share” (Red marked) which essentially means a share other than already held by another entity or an effective shareholding. This could be just an interpretation and common industry practice which is being followed in such situations.

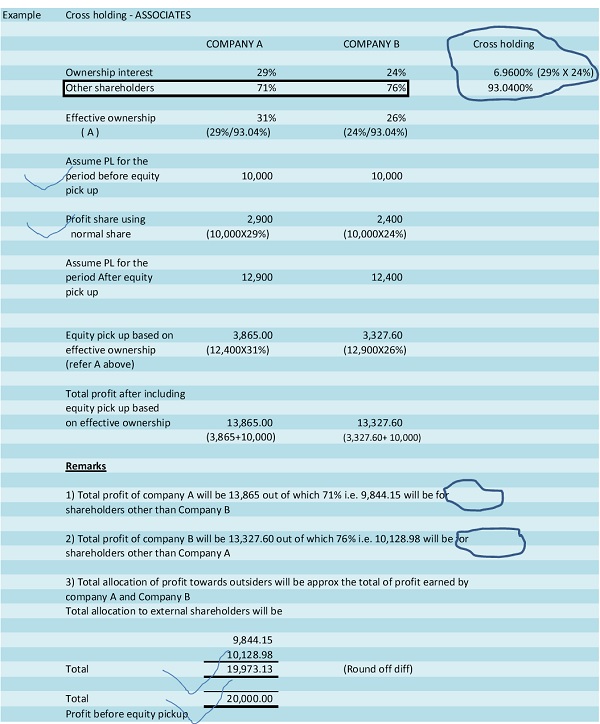

Let’s understand with a numerical example about the treatment of equity method in case of Cross Shareholding –

Now,

One can have a situation while calculating goodwill/ capital reserve on the date of Investments where a) Both the Companies made investment on the same date or b) Investment date if different?

Let’s understand first how the goodwill arises in case of equity accounted investment. On the date of Equity accounted investee, fair values are attributed to the investee’s identifiable assets and liabilities Which mean “”””ATTRIBUTED TO”” means we need to use effective holding as discussed in the example above.

Coming to the second part, if the date of acquisition is different, now suppose company A was only having investment in Company B and Company was accounted as equity invested investment in the books of Company A. Then after the investment made by Company B into A in later date will create increased portion of holding (as effective holding will be higher than actual in case of cross holdings between associates, refer example above), then the increased portion will be used as increase in shareholding in equity accounted investment keeping the equity accounting. In such case entity should use partial step up approach where goodwill is calculated on the incremental portion acquired comparing to the net assets value of that date to arrive additional goodwill/ capital reserve if any.

A reader will appreciate about the main objective of the standard and an approach which one can follow while keeping in mind the basis of origin of such requirements. There could possibly be some specific situations or circumstances where the interpretation of any standard will be different as we should always keep in mind that IND-AS is principle based standards and lot more areas need management judgment in line with the standards relevant interpretation and best practices.

One has to look into all related facts and patterns before concluding this type of assessment based on this concept. Readers are requested not to take this article as any kind of advice (it is not exhaustive in nature) and should evaluate all relevant factors of each individual cases separately.

For any further discussion please feel free to drop an email on anujagarwalsin@gmail.com or whats-app on +91- 9634706933

You may send your questions to anujagarwalsin@gmail.com

Author Bio

what will be the treatment of consolidation when Company A is holding 21.5% in company B (thus, company B is associate of Company A) and company B is holding 15% in company A ?.

An urgent clarification is requested.