Background

The Goods and Services Tax (GST) Council on 16-01-2017 broke a deadlock over issues of administrative control over assessees and broadly agreed to more realistic roll out the GST from July 1, 2017. As the dark cloud on GST is almost over and GST is likely to realty, we need to understand the impacts of GST well on time. In this article we have tried to cover the impact of decentralized registration under this article.

Impacts of Model GST law on Service providers having Centralized registrations

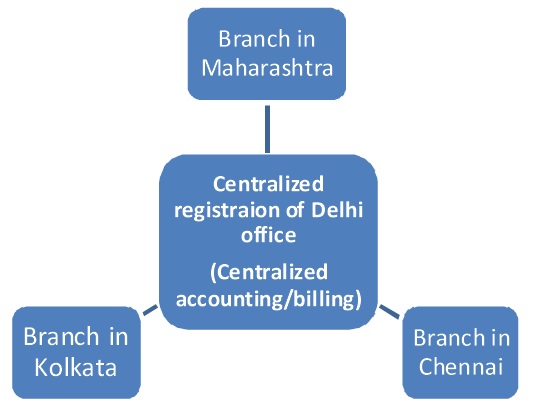

As per Rule 4(2) of the Service Tax Rules, 1994,a facility is provided to the provider of output service to opt for a centralized service tax registration instead of having of a separate registration of all premises located in different states.

Centralized registration under Service tax law:

Presently, only Central Government is empowered to tax the services and service tax rules, 1994 provides the option to the provider of output services a facility to get a centralized registration under above mentioned rule. In fact, most of the service providers, having presence at multiple location, have opted for centralized registration and enjoyingthe benefits like availing input credits, issuing output invoices, discharging service tax liability, undergoing audits and applying for refunds from a chosen centralized location. No doubt such class of service providers is presently enjoying this benefit to a great extent and also can handle litigations at single location from the central place thereby reducing the compliance cost to a great extent.

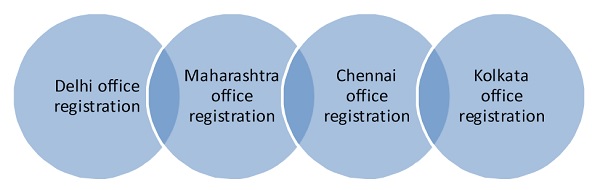

Decentralized system in GST law and more compliance:

Compliance requirements are going to increase tremendously as under Model GST law, registration is required in each State from where the supply of services are being made. Hence, companies would need to obtain separate registrations in each such State where they have a place of business providing services. This will increase the compliance burden to a great extent. Compliances will therefore move from a centralized system as at present, to a decentralized system, leading to multiplicity of returns, refunds, credit pools, etc. This would also require sufficient preparation from an IT systems perspective for the companies to manage these compliances.

Time for action:

Either way, the service provider would need to map the relevant place of supply for each supply and report compliance on that basis. An important related aspect in this regard is for the service provider to ensure that input tax credit pertaining to the supplies shall be captured and availed in the location from where output liability on such supply is paid. Furthermore, accounts and records shall also be maintained State-wise.Specifically, the outward and inward supplies as well as undergoing audits, investigations and assessments across States (where the service provider has a presence) would enhance the burden of compliances on service providers.

One of the major Impacts:

Under the current taxation regime, a service provider needs to file half yearly return. Therefore service provider who provides services on PAN India basis is required to file only 2 half yearly return in a year.

However under the GST regime the supplier of taxable supply of services would require to file 37 returnsduring a financial year for each such State from where the supplier provides the services. Under GST regime, every regular supplier of taxable service would need to file the following returns on monthly/annual basis:

| GST Return Form | Particulars | Periodicity | Due Date |

| GSTR – 1 | Detail of Outward Supplies | Monthly | 10th of next month |

| GSTR – 2 | Detail of Inward supplies | Monthly | 15th of next month |

| GSTR – 3 | Final return along with

tax payment |

Monthly | 20th of next month |

| GSTR – 8 | Annual return | Annual | 31st December of next year |

Let suppose, a service provider who is providing services from 10 states and is enjoying the benefit of centralized registration is filing only 2 returns in a financial year. However, under GST regime such person will be required to file 370 returns in a financial year. This shows how far the Compliances under GST regime will increase tremendously.

What to do!!!

In this backdrop, a transition into a GST regime that entails taxation of services at the State level will certainly pose great level of compliance challenges for the industry. Companies having centralized registration needs to do the following:

a. To do cost benefit analysis of each branch as every branch would lead to significant compliance burden

b. To prepare its infrastructure to account for the transactions on state level basis

c. To revamp the existing accounting software to make them compatible for GST

d. To split the pan India contract to state level based on respective supplies from each state

e. To change the existing contract terms in respect of billing, payments and taxes wherever contracts are entered by the Head Office in one state and executed by the branches in other state

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the authors are personal view and this cannot be quoted before any authority without the written permission of the authors. This article is meant for general guidance and no responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in this article will be accepted by authors. It is recommended that professional advice be sought based on the specific facts and circumstances. This article does not substitute the need to refer to the original pronouncements on GST.

(Authors – CA Neeraj Kumar and CA Deepak Arya, RAPG & Co. Chartered Accountants from Delhi and can be reached at info@rapg.in, 9999836182/9818449179)

Respected sir,

Please answer my query

I Rahul resident of lucknow, would like to ask that,

I am going to open the franchisee of play school at lucknow form July 2017 onwards and in addition to this, I would also sale the school products that includes dress material, books etc to the school children’s.

The school products used to sale is the one that I am going to purchased from the Delhi head office (whose franchisee I m going to set up).

Also, I m expecting that, I would able to generate a turnover of Rs 15, 00,000/- in a year only in lucknow.

Therefore, on the basis of above mentioned information, please let me know whether I require registering myself in GST or NOT?