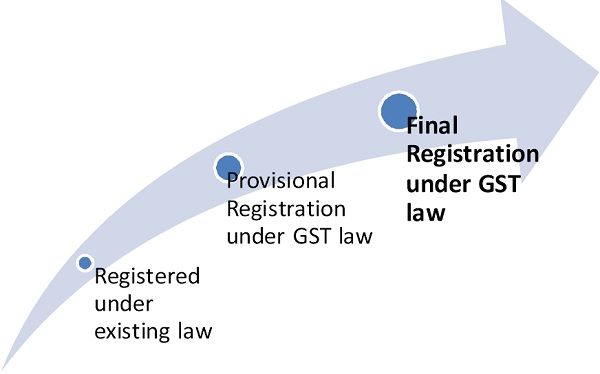

Provisional registration to existing tax payers:-

Every person who is registered under existing law will be granted registration on provisional basis. The enrollment has already started for State VAT from different dates all over India. The enrollment is nothing but a process to gather the information of existing tax payers in a one pool. The data collected shall be used to provide provisional certificate.

Registration of existing tax payers under GST law

On the appointed day (Expected to be 01-07-2017), every person who is registered under any of the earlier laws (e.g. Service tax, Excise, State VAT, Luxury tax, etc.) and having a valid PAN shall be granted a registration on a provisional basis and certificate of registration in FORM GST REG -21. Every person who has been granted the provisional registration shall submit an application electronically in FORM GST REG–20 duly signed along with documents specified in such form within 6 Months from the date of issue of provisional certificate. On the basis of documents furnished, the proper officer may issue the Final certificate of registration under Form GST REG-06. The same shall be available on the common portal.

Cancellation of provisional certificate

The tax payer shall be issued a provisional certificate. If he is not liable to be registered under GST, then he may file an application under Form GST REG 24 at the common portal that he is not liable to be registered under GST and the proper officer may, after conducting such enquiry, cancel the provisional certificate.

Opt for Composition scheme

A person to whom a certificate of registration has been issued on a provisional basis and who is eligible to pay tax under section 9, may opt to do so while filing the application for final registration.

Fresh Registration under GST law:

Person liable to be registered under GST:

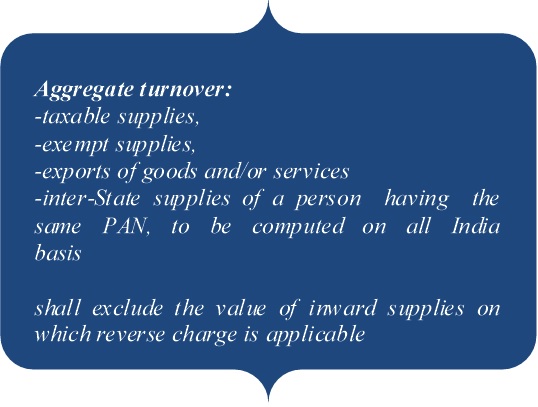

A person having aggregate turnover of INR 20 Lakhs or more during the financial year shall be required to be registered under GST. This limit is reduced to INR 10 Lakhs for special category states. Registration application shall be filed within 30 days from the date such person becomes liable to be registered.

Further, there is a list of categories of persons who are required to be registered irrespective of their turnover. The list includes:

- Inter-state taxable supplier of services/goods,

- Casual taxable person,

- Non-resident taxable person,

- Person who is required to pay tax under reverse charge,

- Person who will deduct the tax,

- Person who will collect the tax,

- Input service distributer,

- E commerce operator,

- An agent or otherwise person who supply goods/services on behalf of other taxable persons,

| Casual taxable person: a person who occasionally undertakes transactions involving supply of goods and/or services in the course or furtherance of business whether as principal, agent or in any other capacity, in a taxable territory where he has no fixed place of business.

Non-resident taxable person: a taxable person who occasionally undertakes transactions involving supply of goods and/or services whether as principal or agent or in any other capacity but who has no fixed place of business in India. |

Fresh Registration process under GST law

Registration of casual taxable person or Non-resident taxable person

- Initial registration for lesser of 90 days or period in application

- Application for registration before 5 days of commencement of business

- Advance payment of estimated tax liability

- Extension up to 90 days

- Advance payment of estimated liability of extended period

- Casual taxable person will apply in GST REG 01

- Non-resident taxable person will apply in GST REG 10

Necessary forms for registration under GST Law:

| All applicants Except

1) Non-resident 2) Tax deductor and person required to collect tax |

GST REG-01 |

| Tax deductor or a person required to collect tax at source | GST REG-07 |

| Special entities applying for UIN | GST REG-09 |

| Non-resident taxable person | GST REG-10 |

| Application form | GST REG-01,07,09,10 |

| Acknowledgement | GST REG-02 |

| Notice for Seeking Additional Information / Clarification/ Documents relating to Application for <<Registration/Amendment/Cancellation>> | GST REG-03 |

| Application for filing clarification/additional information/document for <<Registration /Amendment/Cancellation/Revocation of Cancellation>> | GST REG-04 |

| Order of Rejection of Application for <Registration /

Amendment / Cancellation/ Revocation of Cancellation>> |

GST REG-05 |

| Registration Certificate | GST REG-06 |

FAQs:

1. I am having 2 branches in one state. Whether I am required to take 2 separate registration?

No, you can take one registration for both your branches showing one as principal place of business and another one as additional place of business. However, you have an option to apply for separate registration for your separate business vertical within same state.

2. I am a service provider. I am registered under service tax under centralized registration since I have multiple of branches all over India. Should I need to apply for separate registration in different states under GST?

As per the model law, there is no option to get the centralized registration. Therefore, you will be required to apply for separate registration in every state wherever you have branches from where you provide the services or goods.

| Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the authors are personal view and this cannot be quoted before any authority without the written permission of the authors. This article is meant for general guidance and no responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in this article will be accepted by authors. It is recommended that professional advice be sought based on the specific facts and circumstances. This article does not substitute the need to refer to the original pronouncements on GST.

(Authors – CA Neeraj Kumar and CA Deepak Arya, RAPG & Co. Chartered Accountants from Delhi and can be reached at info@rapg.in, 9999836182/9818449179) |

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the authors are personal view and this cannot be quoted before any authority without the written permission of the authors. This article is meant for general guidance and no responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in this article will be accepted by authors. It is recommended that professional advice be sought based on the specific facts and circumstances. This article does not substitute the need to refer to the original pronouncements on GST.

(Authors – CA Neeraj Kumar and CA Deepak Arya, RAPG & Co. Chartered Accountants from Delhi and can be reached at info@rapg.in, 9999836182/9818449179)

Sir my client is a Charitable trust and running school , simultaneously it rented marriage garden and total receipts from school and marriage garden is about 1.50 crore in which rent from marriage garden receipts is below 20.00 lacs Now is it compulsory to get registration in GST?

Dear Sir,

I have GST registration in tamilnadu, but i am providing service in punjab, do i need to take another registration in punjab.

my turnover for the service in punjab would cross 50 lacs.

Sir,

renting immovable property, have been registered with Service Tax since yr. 2007. which form has to be filled

Sir, as per the schedule V of revised model GST law, a person is required to be registered in a state from where he makes a taxable supply of goods and/or services if the aggregate turnover in FY is more than Rs. 20 Lakhs. Please note that supply includes the supply of goods by principal to his agent where the agent undertakes to supply such goods on behalf of the principal. It can be said supply by principal to agent is one supply and agent to customer/other person is different supply on which GST shall be charged by such agent.

As per the above provisions, it can be concluded that the registration shall be required to be taken from such agent is making the supply. In case you still have some queries, kindly discuss.

i have my office at mumbai & rental godown at bhiwandi. I AM CONSIGNMENT AGENT OF VARIOUS suppliers IN RAJASTHAN & AHMEDABAD. I AM GIVING THEM “F” FORM AGAINST PURCHASES. whether i am required to take registration for consignment agent seperately ?