Case Law Details

Vodafone Idea Limited & Anr. Vs Regional Provident Fund Commissioner II (Calcutta High Court)

The matter involved two writ petitions concerning proceedings under the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. In WPA 27424 of 2024, Vodafone Idea Limited challenged a notice dated 6 November 2024 issued by the Regional Provident Fund Commissioner seeking recovery of provident fund dues as the principal employer. In WPA 27799 of 2024, the contractor challenged the assessment order dated 6 April 2023 passed under Section 7A of the EPF Act.

Vodafone Idea had entered into a service agreement with the contractor in 2014 for rendering services, which continued until August 2018. By order dated 6 April 2023 passed under Section 7A of the EPF Act, the Regional Provident Fund Commissioner determined provident fund dues of Rs.1,81,34,381 payable by the contractor. The proceedings were conducted only against the contractor, and Vodafone Idea was admittedly neither issued notice nor heard.

The Section 7A order recorded that the contractor repeatedly delayed production of records and that there was suspected wage splitting through excessive conveyance allowance to reduce EPF liability. The authority also found that labour payments had been made through subcontractors, assessed liabilities on the basis of enforcement reports, financial records, salary sheets, work orders and agreements, and recorded that the contractor accepted the quantified dues during the hearing on 23 January 2023.

Subsequently, Vodafone Idea received a communication from the contractor claiming that it was liable to make payment to the contractor’s employees. Thereafter, by notice dated 6 November 2024, the Provident Fund authorities called upon Vodafone Idea, treating it as the principal employer, to pay Rs.1,49,89,347 by referring to the Section 7A assessment order and Section 8A(1) of the EPF Act.

The contractor contended that the principal employer was responsible for payment by relying on paragraph 30(3) of the EPF Scheme and asserted that it had not received wages and statutory dues from the principal employer. The Court noted that paragraph 30(2) places responsibility upon the contractor to recover employees’ contributions and pay them to the principal employer.

The Court examined the service agreement between Vodafone Idea and the contractor. Clause 3.1 expressly provided that the service provider would be responsible for paying salaries and that Vodafone Idea would not be responsible for salaries or any other outgoings to the employees. Clause 3.2 required the service provider to raise invoices inclusive of taxes, levies and statutory payments. The Court held that these clauses placed responsibility for payment of salaries and statutory dues upon the contractor.

The Court further observed that the findings recorded in the Section 7A order corroborated that the contractor had paid salaries and had manipulated wage components by excessive conveyance allowance to reduce provident fund liability. The assessment order itself showed that the contractor had accepted the quantified dues. The Court therefore rejected the contractor’s contention that it could not pay provident fund dues because the principal employer had failed to make payment.

The Court also noted that the Section 7A assessment referred to several principal employers and that the contractor itself had admitted in its writ petition that it supplied manpower and services to various government entities, public sector undertakings and private companies, including Vodafone Idea, WBSEDCL, RITES, Ministry of External Affairs, Zee Entertainment Enterprises Ltd., Tractor India (now Gainwell India), and others. The assessment order itself recorded that the assessed dues related to employees who had worked under various principal employers, one of whom was Vodafone Idea.

The Court held that Vodafone Idea had not been made a party to the Section 7A proceedings and therefore the subsequent notice dated 6 November 2024 fastening liability upon it amounted to an abuse of the process of law. It also observed that despite findings regarding engagement of subcontractors by the contractor, the Provident Fund authorities invoked Section 8A(1) against Vodafone Idea without addressing those findings. Holding that the notice suffered from erroneous findings and was bad in law, the Court quashed and set aside the notice dated 6 November 2024 and allowed WPA 27424 of 2024.

With respect to WPA 27799 of 2024 filed by the contractor, the Court found that the contractor had earlier filed WPA 21772 of 2023 challenging the same Section 7A order but had expressly stated before the Court that it was not interested in questioning the assessment order and accepted the determination. The Court had granted time for payment, but the writ petition was dismissed after the contractor failed to establish its bona fides. The Division Bench, while dismissing MAT 41/42 of 2025, held that the contractor could not resile from its unequivocal undertaking to pay the assessed amount, observed that reopening the assessment was impermissible, and held that the attempt amounted to abuse of the process of court.

The Court held that despite those earlier proceedings and orders, the contractor had again challenged the same assessment order while suppressing the earlier litigation. Describing such conduct as contemptuous and an abuse of the process of law, the Court dismissed WPA 27799 of 2024. The connected application was disposed of and interim orders, if any, were vacated.

FULL TEXT OF THE JUDGMENT/ORDER OF CALCUTTA HIGH COURT

1. The petitioners case herein is that in the year 2014, Vodafone Idea Limited (hereinafter referred to as “the petitioner no.1”) entered into a service agreement with M/s Shomuk Engineering 85 Consultancy Services (hereinafter referred to as “the private respondent”) as a service provider for the purpose of rendering services to the petitioner no.1 as and when required. The service agreement was subsisting till the period of August, 2018.

2. On 6th April, 2023, an order was passed by the Regional Provident Fund Commissioner- I / Recovery Officer, Employees’ Provident Fund Organization, Ministry of Labour and Employment, Union of India, in a proceeding being E-Court Diary No. 83/2017, wherein the private respondent was directed to pay an amount of Rs. 1,81,34,381/- (Rupees One Crore Eight ne Lakhs Thirty Four Thousand and Three Hundred and Eighty-One) to the respondent no. 2 in lieu of the statutory contributions for some of its employees under Section 7A of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952.

3. Admittedly in the said proceeding the petitioners were not put on notice and thus were not heard.

4. The proceeding under Section 7A of the EPF Act was conducted in respect of the private respondent no. 4’s establishment herein, the contractor who was engaged by the petitioner no. 1 herein and thus the petitioner no. 1 became the principal employer.

5. In the proceeding under Section 7A of the EPF Act, the authority observed/held in respect of the respondent no. 4’s establishment as follows:-

“The hearings were prolonged mainly due to delayed submission of necessary records by the establishment. It did not submit the records required in the hearings easily and repeated adjournments were sought for tracing the documents leading to prolonging the Instant hearing. The proceedings under section 7A were continued from 30.10.2017 to 13.03.2019 due to non appearance of establishment and non submission or partial submission of necessary records. Srl T. P. Niroula, E.O. submitted his report on 12.03.2019 which was placed in the 7A hearing dated 13.03.2019. The report of E. 0. was found to be Incomplete. It was found that the basic wages of EPF members were kept very low and rest of the remuneration was paid in form of different allowances for which EPF was not paid by the employer. Therefore, the element of subterfuge in wage splitting was apprehended.”

6. Finally it has been recorded in the order as follows:-

“9. Sri Sanjay Biswas, (EO), submitted his final report on 18.01.2023 copy of which was forwarded to the establishment. In the 7A hearing dated 23.01.2023 the proprietor of the establishment, Sri Aniruddha Banerjee accepted the receipt of the report dated 18.01.2023. Sri Banerjee further stated that the establishment has no objection on the finding of the Enforcement Officer and the quantum of dues payable. Accordingly the hearings were closed.

12 a) The establishment M/ S Shomuk Engineering & Consultancy Services is a Sole Proprietorship concern having five units. These five units have separate EPF Code numbers issued by different Regional Offices in different Political States. A single Balance Sheet is maintained for all these five units and therefore scrutiny of Balance Sheet for the whole establishment is of little use for assessing EPF liabilities of its Kolkata Unit having EPF Code Number WB/PRB/40096.

b) The business activities of Kolkata Unit of the establishment are supply of Manpower to certain other establishment and execution of engineering and construction work.

c) The EPF liabilities of the Kolkata Unit of the establishment having Code No. WB/PRB/40096 for the notice period have been assessed on the basis of report of Enforcement Officer dated 07.09.2017 (based on which the instant 7A proceedings have been initiated), EO report dated 03.05.2019, records of financial transactions of the establishment like Ledger Head Site Expenses, Vouchers and Bills, Salary Sheet of labour charges involved, copies of work orders/agreements made by the establishment with different parties, clarifications about different types of expenses incurred by the establishment and the comprehensive report of Sri Sanjay Biswas, E. 0. dated 18.01.2023 and his clarification dated 10.03.2023.

d) Salary Sheet of on roll employees deployed in various establishments reveal that conveyance allowances paid to the employees are abnormally high, varying from 18% to 65% of Basic Pay. This is obvious case of subterfuge on part of the establishment to reduce its PP liability. Hence EPF liability is being assessed on conveyance allowances paid to the employees over and above 10% limit of Basic Pay subject to statutory ceiling of Rs 15000 per month. Month wise dues assessed for EPF chargeable conveyance allowance (greater than 10% of basic salary) from September 2014 to August 2017 has been summarised in Annex-A, copies of which has already been provided to employer. The employer has accepted the dues payable on hearing dated 23.01.2023.

e) Ledger head of the establishment for the period 07/2015 to 03/2016 and for the period 04/2016 to 12/2016 shows that labour payment was made at Rajarhat Site by ongoing sub contractors. Since details of labour charges are available in office records, assessment of liability of the establishment has been made. Contractor wise and Month wise EPF dues for evaded employees (by their name) has been summarised in Annex-B. Copy of the said list has been provide to the employer and the dues payable by the employer has been accepted on hearing dated 23.01.2023.

j) Similarly other dues like month wise cite expense dues and dues to several sub-contractors have been summarised in Annex – C, D, E and F. These figures have been provided to the establishment and the same has been accepted by it on hearing dated 23.01.2023.

14. Accordingly, I, Tushar Kant Mukherjee, Regional Provident Fund Commissioner-I in exercise of the powers conferred on me under Section 7A of the Act, having gone through the facts of the case and submissions made hereby determine an amount of Rs. 1,81,34,381/- (Rupees One Crore Eighty One Lakh Thirty Four Thousand Three Hundred and Eighty One Only) to be paid by the establishment M/S Shomuk Engineering L and Consultancy Services under section 7A of the EPF and MP Acts, 1952.”

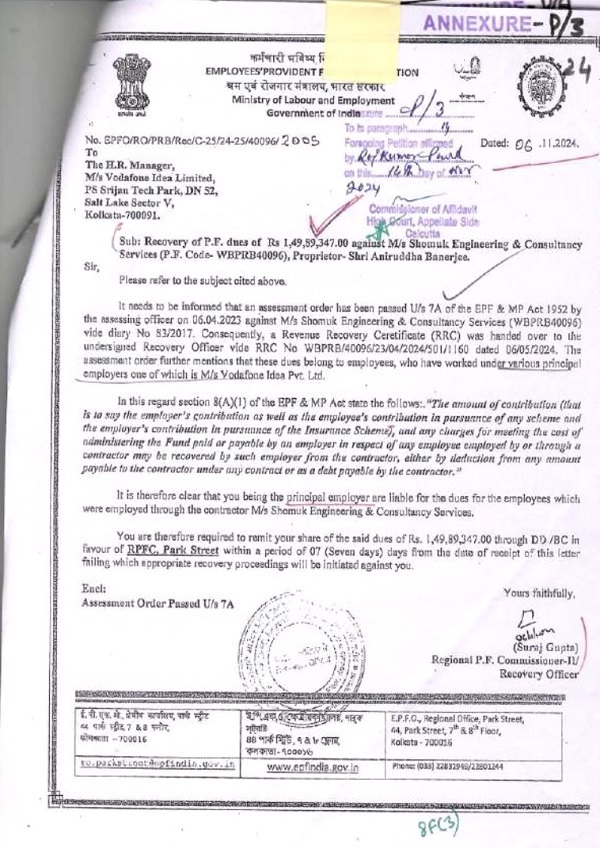

7. On 3rd September, 2024, the petitioner no.1 received a letter from the private respondent, which stated that the petitioner no.1 was liable to make certain payment to the employees of the private respondent. No reason was given in the letter as to the basis for raising such claim on the erstwhile Vodafone entities/petitioner no.1 especially when all due and payable amounts were paid by the petitioner no. 1 to the private respondent.

8. The impugned notice carried an attachment being a purported assessment order bearing Reference E-Court Diary No. 83/2017 dated 6th April, 2023 passed by the respondent no. 2 whereby the private respondent was directed to pay an amount of Rs. 1,81,34,381/- to the respondent no. 2 in lieu of non-payment of statutory contributions for some of its employees.

9. The impugned notice referred to in the impugned order, had been passed solely against the private respondent. Despite this, vide the impugned notice dated 6th Nov, 2024, the petitioner no.1 was called upon to clear the dues of the employees of the private respondent in the capacity of a principal employer. The petitioner no.1, was further directed to remit its alleged share of the said purported dues of Rs. 1,49,89,347/- through DD/BC in favour of Regional Provident Fund Commissioner (“RPFC”).

10. The impugned letter herein dated 06.11.2024, issued by the respondent P.F. authorities is scanned and reproduced herein:-

11. The authority has referred to Section 8(A)(1) of the EPF 85 MP Act, which refers to how a principal employer has to recover the statutory dues from the contractor, who is liable to pay the same, after the principal employer pays the outstanding dues (liability) of the contractor.

11. The authority has referred to Section 8(A)(1) of the EPF 85 MP Act, which refers to how a principal employer has to recover the statutory dues from the contractor, who is liable to pay the same, after the principal employer pays the outstanding dues (liability) of the contractor.

12. The respondent no. 4 herein, being the petitioner in WPA 27799 of 2024 has challenged the order under Section 7A of the EPF 85 MP Act dated 06.04.2023, on the ground that the establishment/contractor herein has not received the wages including total statutory dues from the principal employer and as such is not in a position to pay any amount.

13. The respondent no. 4 relies upon the provision of Para 30(3) of the EPF scheme, to state that it is the responsibility of the principal employer to pay both the contribution.

14. It appears that as per Para 30(2) of the scheme, the duty of the contractor herein is to recover the contribution payable by such employees and pay the same to the principal employer.

15. The authority then in the order dated 06.04.2023 under Section 7A of the Act, proceeded to probe into the issue of manipulation of wages by the establishment (contractor respondent no. 4 herein) to eliminate possibility of subterfuge.

16. While doing so, it appears that the authority considered copies of agreements made by the establishment (contractor respondent no. 4 herein) with the petitioner Vodafone and with WBSEDCL.

17. On 16.10.2019, establishment/respondent no. 4 submitted copies of invoices of sub contractors and cash vouchers for the period under reference, before the F. authorities.

18. The findings in Para 12(d) of the said order under Section 7A of the Act shows that salary sheets were placed in respect of on roll employees deployed in various establishment, which also showed there was subterfuge on part of the establishment to reduce it’s PF liability. This proves that the establishment was duly paid by the principal employer, the petitioner no. 1 herein and the salary sheets submitted by the establishment, shows the disbursement of salary along with allowances by the establishment herein in various establishments.

19. It further appears that a single balance sheet is maintained for the five units of the respondent no. 5 in different states.

20. In Para 12(d), the employer/contractor/respondent no. 4 has accepted the dues payable on the hearing dated 23.01.2023 and the same has been also recorded in Para 12(1) as follows:-

f) Similarly other dues like month wise cite expense dues and dues to several sub-contractors have been summarised in Annex – C, D, E and F. These figures have been provided to the establishment and the same has been accepted by it on hearing dated 23.01.2023.

21. Para 12(e) in the said order shows there were sub contractors engaged.

e) Ledger head of the establishment for the period 07/2015 to 03/2016 and for the period 04/2016 to 12/2016 shows that labour payment was made at Rajarhat Site by ongoing sub contractors. Since details of labour charges are available in office records, assessment of liability of the establishment has been made. Contractor wise and Month wise EPF dues for evaded employees (by their name) has been summarised in Annex-B. Copy of the said list has been provide to the employer and the dues payable by the employer has been accepted on hearing dated 23.01.2023.

22. On hearing, the parties and considering the materials on record, the issue in WPA 27424 of 2024 is taken up for consideration.

23. The service agreement between the parties being part of the writ petition contains the clauses relevant herein, which are:-

“3.1 The service provider shall be responsible for paying salary to the associates for the services rendered by the associates to Vodafone under this Agreement and Vodafone shall not be responsible for paying salary or any other outgoings to the associates.

3.2 The Service Provider shall raise an invoice every month on respective Vodafone Entities for the respective Telecom Service Areas detailing the Service Fee & other reimbursement which, shall be inclusive of all taxes, levies and statutory payments except the service tax which shall be extra.”

24. These clauses clearly show that the petitioner no. 1 herein did not have the responsibility to pay salary or any other outgoings to the associates (employees) including statutory payments.

25. The responsibility was of the respondent no. 4 (service provider) in the agreement and as per clause 3.2, the service provider would raise invoice for reimbursement on the respective principal employers which would include statutory payments.

26. The fact that salary was paid by the establishment/respondent no. 4 has been corroborated by the findings of the authority under Section 7A EPF 85 MP Act as discussed earlier herein.

27. Thus the contention of the respondent no. 4 that as the petitioner did not make payment, they could not do so, is not correct. Not only was salary paid by the respondent no. 4, manipulation of wages and subterfuge was also found on the part of the establishment by the authority on hearing the establishment.

28. Admittedly the petitioner no. 1 herein was not made a party to the proceeding under Section 7A of the EPF 85 MP Act and as such the claim of the respondent no. 4 (establishment) and that of the F. Authorities herein vide their letter dated 06.11.2024 is a clear abuse of the process of law.

29. The said letter dated 06.11.2024 refers to the assessment order under Section 7A of the Act against the establishment/respondent no. 4 herein, in which the petitioner admittedly was not a party.

30. The assessment order further mentions that “these dues belong to employees, who have worked under various principal employers one of which is M/s Vodafone Idea Put. Ltd.” and this shows that the petitioner herein is not the only/sole principal employer for the dues as assessed.

31. This again is a vague observation, which puts the liability upon the petitioner no. 1 herein, in spite of holding that:-

i. The assessment order under Section 7A of the EPF 85 MP Act was against the establishment/respondent no. 4.

ii. The dues in the said assessment order belong to employees, who have worked under various principal employers, one of which is the petitioner herein as admitted by the respondent no. 4 as petitioner in WPA 27799 of 2024.

32. In WPA 27799 of 2024, the Petitioner is a proprietorship concern and a supplier of Management Services, Manpower Service and Works Contract Service to Government, Local Authority, Non-Government entities, etc. The details of the parties are as per following:-

(a) The West Bengal Power Development Corporation Limited (GSTIN 19AABCT3027C1DZ);

(b) WBSEDCL, Midnapore Zonal Office (GSTIN 19CALM05977G1D0);

(c) West Bengal State Electricity Distribution Company Limited (GSTIN 19CALW029

(d) Ministry of External Affairs;

(e) RITES Ltd;

(f) Tractor India (now Gainwell India);

(g) Zee Entertainment Enterprises Ltd;

(h) Vodafone Spacetel Ltd; and

(i) Vodafone Idea Limited, Kolkata.

It is stated that many of these companies are managed and owned either by the Government of India or any of the State Governments or big MNCs.

33. The reference to Section 8(A)(1) of the EPF 85 MP Act, in the letter/order dated 06.11.2024, remains a question, considering the reference/findings in the order under Section 7A of Act, as to sub-contractors being engaged by the establishment (contractor), in which case the contractor becomes the principal employer to the said sub contractors.

34. In spite of such finding, the authority has referred to the provisions under Section 8(A)(1) of the EPF 85 MP Act in the letter/order dated 06.11.2024, while putting the liability on the petitioner no. 1 herein for the dues of the respondent no. 4, which is also against the terms and conditions in the service agreement between the parties and also the fact that the assessment was made in respect of various principal employers.

35. As such the impugned order dated 06.11.2024, which suffers from erroneous findings as noted above being bad in law is hereby quashed and set aside.

36. WPA 27424 of 2024 is thus allowed.

37. In respect of the WPA 27799 of 2024, the establishment/contractor has not made the principal employer a party to the writ application but has prayed for leave to add Vodafone Idea limited, prayer (d), Tractor India (now Gainwell India Ltd.) prayer (e) and Zee Entertainment Enterprises Ltd., prayer (1) as parties.

38. Respondent no. 5 Rail India Technical and Economic Services (RITES) and Respondent no. 6 West Bengal State Electricity Board are already on record as added respondents.

39. In the present writ application, the establishment as petitioner, has admitted that he works as immediate employer with contractor/ several companies/governmental agencies (principal employers) even though in WPA 27799 of 2024, the argument by the learned counsel for the respondent no. 4 therein being the petitioner herein, is that, only the petitioner Vodafone Idea Ltd. therein, is liable for the dues, even though the assessment was admittedly done in respect of various principal employers by the authority and as admitted by the establishment petitioner herein.

40. The relief prayed for is that the respondents/P.F. authorities should not proceed against the establishment beyond the amount/sum of Rs. 38,09,646 and for setting aside of the assessment order dated April 06, 2023, under Section 7A of the EPF 85 MP Act.

41. Mr. Majumder, learned senior counsel has placed several copies of order sheets and a list of dates in WPA 27424 of 2024 and submits that WPA 27799 of 2024 has been filed challenging the same impugned order dated 06.04.2023 and a prayer claiming limited liability by suppressing that the issue were raised in an earlier writ application being WPA 21772 of 2023 wherein also Vodafone was not a party.

42. The establishment in the said writ application (WPA 21772 of 2023) prayed for installment facility considering that it had accepted/admitted the dues assessed under Section 7A of the Act before the authority and the authority had recorded the same in the said order.

43. In the order dated 20.09.2023 in WPA 21772 of 2023, it was recorded by the Court as follows:-

“Mr. Bhattacharyya, learned advocate representing the petitioner submits that the petitioner is not interested to question the order dated 6th April, 2023, passed under Section 7A of the said Act and the petitioner accepts the determination made.”

44. The Court directed that the establishment/petitioner therein to place a cheque for a sum of Rs. 50,00,000/- in the name of RPF.

45. On the next date fixed for hearing an undated cheque was placed. The Court on noting that the petitioner there in could not establish his bonafide, dismissed the writ application.

46. In appeal, being MAT 41/42 of 2025, the Hon’ble Division Bench vide order dated 14.01.2025 recorded as follows:-

“6. The September 20, 2023 order recorded that the petitioner, as represented by his counsel, was not interested to question the impugned order dated April 6, 2023 passed under Section 7A of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952.

8. Under such circumstances, on November 26, 2024, the proprietor of the appellant-firm, who was present in court, instructed his learned senior counsel to pray for time for two weeks within which he shall unconditionally (emphasis in original order) pay the assessed amount under the impugned assessment order dated April 6, 2023 to the Provident Fund Authority after adjustment of the amount already paid by the contractor to the Provident Fund Authority.

18. The appellant, unequivocally gave undertaking several times over before the learned Single Judge that he was not interested in assailing the impugned order of assessment but would unconditionally pay the amount within a limited period, which was further extended from time to time at the behest of the appellant himself.

19. Thus, after having specifically submitted before the learned Single Judge that he does not intend to challenge the assessment order, the appellant cannot be permitted to resile from such specific undertaking given before the court on the flimsy pretext that there cannot be any estoppel against the law. The assessment order cannot be reopened at this stage at the behest of the appellant himself.

21. The undertaking which was given unequivocally before a court of law to obtain the advantage of buying time for the purpose of making payment in terms of the assessment order is not restricted to estoppel but has crystallized into an order of court based on the appellant’s concession. The present appeals are, thus a clear attempt to resile from the same, which tantamounts to nothing less than contempt of court.

23. A larger underlying factor involved here is that the delay in making such payments directly and adversely affects the concerned employees, who are being deprived of their provident fund dues, which is also one of the considerations which ought to be borne in mind while deciding the present appeals.

25. The learned Single Judge was perfectly within his rights and jurisdiction to accept the undertaking of the appellant in good faith and merely grant further time to make payments to the appellant on the latter’s plea to make such payments of the assessed amount.”

47. The appeals were then dismissed by the Hon’ble Division Bench.

48. In spite of such findings by the Hon’ble Division Bench, the petitioner (establishment) has once again approached this Court, assailing the self same order dated 06.04.2023 under Section 7A of the EPF 85 MP Act by suppressing the orders passed in the earlier writ application and appeals, which is still in force and holds good till date.

49. The said conduct/suppression by the establishment /petitioner is not only contemptuous, but is also abuse of the process of law, in /before a Court of law.

50. Considering the said facts, the writ application being WPA 27799 of 2024 having no merit is dismissed on contest.

51. Connected application, if any, stands disposed of.

52. Interim order, if any, stands vacated.

53. Urgent Photostat certified copy of this Order, if applied for, be supplied to the parties expeditiously after due compliance.

Author Bio