Case Law Details

ITO Vs Smark Securities Limited (ITAT Hyderabad)

Hyderabad ITAT Quashes Reassessment: Section 148 Notice Invalid Without Approval of Competent Authority Under Section 151(ii)

Summary: The ITAT Hyderabad dismissed the Revenue’s appeal and allowed the assessee’s cross-objection to the extent of quashing the reassessment framed under Sections 147 read with 144B for AY 2018-19. The Tribunal held that the notice under Section 148 dated 28.04.2022, issued after more than three years from the end of the relevant assessment year, required prior approval from the authority specified under Section 151(ii), namely the Principal Chief Commissioner, Principal Director General, Chief Commissioner or Director General. However, the Assessing Officer had obtained approval only from the Principal Commissioner of Income Tax, who was not the specified authority under the law applicable from 01.04.2021. The Tribunal, relying on the Telangana High Court decision in Deloitte Consulting India Private Limited v. The Assessment Unit, Income Tax Department and referring to the Supreme Court’s decision in Union of India & Ors. v. Ashish Agrawal, held that the assessment lacked valid assumption of jurisdiction and quashed the reassessment. Having quashed the assessment on jurisdictional grounds, the Tribunal did not examine the Revenue’s grounds challenging the deletion of the addition relating to alleged bogus long-term capital gains.

The Hyderabad ITAT quashed the reassessment proceedings for AY 2018-19, holding that the notice issued under section 148 was without valid jurisdiction as it had been approved by the Principal Commissioner of Income Tax, whereas under section 151(ii), where more than three years had elapsed from the end of the relevant assessment year, the approval was required from the Principal Chief Commissioner/Principal Director General/Chief Commissioner/Director General. The Tribunal rejected the Revenue’s contention that the exclusion of the period allowed under section 148A(b), introduced by the Finance Act, 2023, could be retrospectively applied to compute the three-year period. Relying on the Telangana High Court’s decision in Deloitte Consulting India Pvt. Ltd. and the Supreme Court’s ruling in Union of India v. Ashish Agrawal, the Tribunal held that the defect went to the root of the assumption of jurisdiction and consequently quashed the reassessment itself. Since the assessment was annulled on jurisdictional grounds, the Tribunal did not examine the merits of the Revenue’s challenge relating to the alleged bogus long-term capital gains on penny stock transactions, leaving those issues open.

Cases Discussed:

- ITO Vs Smark Securities Limited, ITAT Hyderabad, Order pronounced on 08.07.2026.

- Deloitte Consulting India Private Limited vs. The Assessment Unit, Income Tax Department, Civil Writ Petition No. 4061 of 2024, dated 25/09/2025.

- Union of India & Ors. Vs. Ashish Agrawal, Civil Appeal No. 3005/2022, dated 04.05.2022.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

The captioned appeal filed by the Revenue is directed against the order passed by the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, Delhi (for short, “CIT(A)”), dated 07/10/2025, which in turn arises from the order passed by the Assessing Officer (for short, “AO”) under section 147 r.w.s 144B of the Income Tax Act, 1961 (for short, “the Act”), dated 08/03/2024. The Revenue has assailed the impugned order of the CIT(A) on the following grounds of appeal:

“1) The order of the Ld. CIT(A) is erroneous both on facts and in law

2) On the facts and circumstances of the case, the Ld. CIT(A) failed to appreciate that the assessing officer has categorically established the LTCG on sale of shares of SEIL was non-genuine and there were no financial credentials to justify such a significant increase in price of shares in short period and the assessee had a windfall Long Term capital gains of Rs. 5,41,41,408/-.

3) The Ld. CIT(A) erred in deleting the addition made by assessing officer whereas the stock sold was proved as penny stock during the course of search & seizure proceedings.

4) Whether on facts and circumstances of the case, the Ld. CIT(A) erred in ignoring the statement recorded during the course of search & Seizure proceedings of Shri Naresh Jain.

5) The appellant craves leave to add, alter, amend or withdraw any of the above grounds of appeal at the time of hearing.”

Also, the assessee company is before us as a cross objector on the following grounds:

“1. The learned Commissioner of Income-Tax (Appeals) ought to have quashed the notice u/s 148 of the Act:

a) Issued without any tangible material suggesting escapement of income and without providing any such information to the Respondent.

b) Issued by the JAO but not the FAO, in contravention of the provisions of S.151A of the Act and the E-Assessment of Income Escaping Assessment, 2022 notified u/s 151A of the Act.

c) Issued without approval from appropriate authority in terms of S.151 (ii) of the Act.

2. Without prejudice to the above, the learned Commissioner of Income-Tax (Appeals) is justified in deleting the addition of Rs.5,41,41,408 made by the Assessing officer u/s 69 of the Act by considering the Long-Term Capital Gains on sale of shares as unexplained investment of the Respondent.

3. Any other ground of cross-objection that may be raised at the time of hearing.”

2. Succinctly stated, the assessee company had e-filed its return of income for AY 2018-19 on 30/03/2019, declaring an income of Rs. NIL, along with carry forward of loss of Rs. 12,61,919/-. Thereafter, the case of the assessee company was reopened under section 147 of the Act. Notice under section 148 of the Act, dated 28/04/2022, was duly served upon the assessee company.

3. Thereafter, the AO vide his order passed under section 147 r.w.s 144B of the Act, dated 08/03/2024, after declining the claim of the assessee company for exemption of “Long term capital gains” (LTCG) under section 10(38) of the Act of Rs. 5,41,41,408/-, determined its income at Rs. 5,28,79,489/-.

4. Aggrieved, the assessee company carried the matter in appeal before the CIT(A), who deleted the addition made by the AO towards alleged bogus long-term capital gains and partly allowed the appeal.

5. The Revenue, aggrieved with the order of the CIT(A) has carried the matter in appeal before us.

6. We have heard the Learned Authorised Representatives of both parties, perused the orders of the lower authorities and the material available on record. As the Ld. AR, based on his cross-objection, has assailed the validity of the jurisdiction assumed by the AO for framing the impugned assessment; we deem it apposite to first deal with the said material aspect.

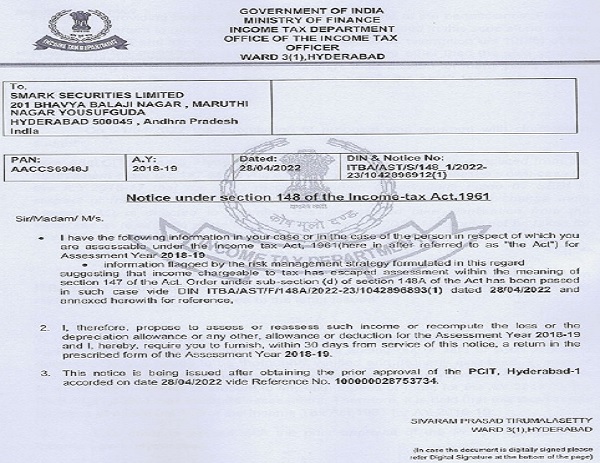

7. Shri GVN Hari, Advocate, Learned Authorised Representative (for short, “Ld. AR”) for the assessee respondent, at the threshold of hearing of the appeal, submitted that the AO had erred in framing the assessment vide his order passed under section 147 r.w.s. 144B of the Act, dated 08/03/2024, without valid assumption of jurisdiction. Elaborating on his contention, the Ld. AR submitted that the AO had issued the notice under section 148 of the Act, dated 28/04/2022, without obtaining the approval of the specified authority as contemplated under section 151(ii) of the Act. The Ld. AR, to buttress his contention, had drawn our attention to the notice under section 148 of the Act, dated 28/04/2022, issued by the ITO, Ward-3(1), Hyderabad, which revealed that the notice was issued after obtaining the prior approval of the Principal Commissioner of Income Tax, Hyderabad-1, accorded on 28/04/2022, vide Reference No.100000028753734. Apart from that, the order passed under section 148A(d) of the Act, dated 28/04/2022, also stated that it was passed with the prior approval of the Principal Commissioner of Income Tax-1, Hyderabad. For the sake of clarity, we deem it fit to cull out the notice u/s 148 dated 28/04/2022, as under:-

8. At this stage, it will be relevant to point out that nothing has been placed on our record by the Ld. DR to rebut the aforesaid factual position as has been brought to our notice.

9. Apropos the challenge by the Ld. AR regarding the validity of the jurisdiction assumed by the A.O. for initiating proceedings u/s. 147 of the Act, i.e., without obtaining the approval of the specified authority u/s. 151(ii) of the Act, we find substance in the same. Admittedly, the reassessment proceedings u/s. 147 of the Act had been revamped vide the Finance Act, 2021 w.e.f. 01.04.2021. The substituted Sections 147 to 149 and Section 151 of the Act, applicable w.e.f. 01.04.2021 are culled out as under:

“Income escaping assessment-

147. If any income chargeable to tax, in the case of an assessee, has escaped assessment for any assessment year, the Assessing Officer may, subject to the provisions of sections 148 to 153, assess or reassess such income or recompute the loss or the depreciation allowance or any other allowance or deduction for such assessment year (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year).

Explanation.—For the purposes of assessment or reassessment or recomputation under this section, the Assessing Officer may assess or reassess the income in respect of any issue, which has escaped assessment, and such issue comes to his notice subsequently in the course of the proceedings under this section, irrespective of the fact that the provisions of section 148A have not been complied with.”.

Issue of notice where income has escaped assessment

148. Before making the assessment, reassessment or recomputation under section 147, and subject to the provisions of section 148A, the Assessing Officer shall serve on the assessee a notice, along with a copy of the order passed, if required, under clause (d) of section 148A, requiring him to furnish within such period, as may be specified in such notice, a return of his income or the income of any other person in respect of which he is assessable under this Act during the previous year corresponding to the relevant assessment year, in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed; and the provisions of this Act shall, so far as may be, apply accordingly as if such return were a return required to be furnished under section 139:

Provided that no notice under this section shall be issued unless there is information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment in the case of the assessee for the relevant assessment year and the Assessing Officer has obtained prior approval of the specified authority to issue such notice.

Explanation 1.—For the purposes of this section and section 148A, the information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment means,—

(i) any information flagged in the case of the assessee for the relevant assessment year in accordance with the risk management strategy formulated by the Board from time to time;

(ii) any final objection raised by the Comptroller and Auditor General of India to the effect that the assessment in the case of the assessee for the relevant assessment year has not been made in accordance with the provisions of this Act.

Explanation 2.—For the purposes of this section, where,—

(i) a search is initiated under section 132 or books of account, other documents or any assets are requisitioned under section 132A, on or after the 1st day of April, 2021, in the case of the assessee; or

(ii) a survey is conducted under section 133A, other than under subsection (2A) or subsection (5) of that section, on or after the 1st day of April, 2021, in the case of the assessee; or

(iii) the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner, that any money, bullion, jewellery or other valuable article or thing, seized or requisitioned under section 132 or under section 132A in case of any other person on or after the 1st day of April, 2021, belongs to the assessee; or

(iv) the Assessing Officer is satisfied, with the prior approval of Principal Commissioner or Commissioner, that any books of account or documents, seized or requisitioned under section 132 or section 132A in case of any other person on or after the 1st day of April, 2021, pertains or pertain to, or any information contained therein, relate to, the assessee, the Assessing Officer shall be deemed to have information which suggests that the income chargeable to tax has escaped assessment in the case of the assessee for the three assessment years immediately preceding the assessment year relevant to the previous year in which the search is initiated or books of account, other documents or any assets are requisitioned or survey is conducted in the case of the assessee or money, bullion, jewellery or other valuable article or thing or books of account or documents are seized or requisitioned in case of any other person. Explanation 3.—For the purposes of this section, specified authority means the specified authority referred to in section 151.”

Conducting inquiry, providing opportunity before issue of notice under section 148-

“148A. The Assessing Officer shall, before issuing any notice under section 148,—

(a) conduct any enquiry, if required, with the prior approval of specified authority, with respect to the information which suggests that the income chargeable to tax has escaped assessment;

(b) provide an opportunity of being heard to the assessee, with the prior approval of specified authority, by serving upon him a notice to show cause within such time, as may be specified in the notice, being not less than seven days and but not exceeding thirty days from the date on which such notice is issued, or such time, as may be extended by him on the basis of an application in this behalf, as to why a notice under section 148 should not be issued on the basis of information which suggests that income chargeable to tax has escaped assessment in his case for the relevant assessment year and results of enquiry conducted, if any, as per clause (a);

(c) consider the reply of assessee furnished, if any, in response to the showcause notice referred to in clause (b);

(d) decide, on the basis of material available on record including reply of the assessee, whether or not it is a fit case to issue a notice under section 148, by passing an order, with the prior approval of specified authority, within one month from the end of the month in which the reply referred to in clause (c) is received by him, or where no such reply is furnished, within one month from the end of the month in which time or extended time allowed to furnish a reply as per clause (b) expires:

Provided that the provisions of this section shall not apply in a case where,—

(a) a search is initiated under section 132 or books of account, other documents or any assets are requisitioned under section 132A in the case of the assessee on or after the 1st day of April, 2021; or

(b) the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner that any money, bullion, jewellery or other valuable article or thing, seized in a search under section 132 or requisitioned under section 132A, in the case of any other person on or after the 1st day of April, 2021, belongs to the assessee; or

(c) the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner that any books of account or documents, seized in a search under section 132 or requisitioned under section 132A, in case of any other person on or after the 1st day of April, 2021, pertains or pertain to, or any information contained therein, relate to, the assessee.

Explanation.—For the purposes of this section, specified authority means the specified authority referred to in section 151.”

Time limit for notice-

“149. (1) No notice under section 148 shall be issued for the relevant assessment year,—

(a) if three years have elapsed from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if three years, but not more than ten years, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax, represented in the form of asset, which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more for that year:

Provided that no notice under section 148 shall be issued at any time in a case for the relevant assessment year beginning on or before 1st day of April, 2021, if such notice could not have been issued at that time on account of being beyond the time limit specified under the provisions of clause (b) of subsection (1) of this section, as they stood immediately before the commencement of the Finance Act, 2021:

Provided further that the provisions of this subsection shall not apply in a case, where a notice under section 153A, or section 153C read with section 153A, is required to be issued in relation to a search initiated under section 132 or books of account, other documents or any assets requisitioned under section 132A, on or before the 31st day of March, 2021:

Provided also that for the purposes of computing the period of limitation as per this section, the time or extended time allowed to the assessee, as per show cause notice issued under clause (b) of section 148A or the period during which the proceeding under section 148A is stayed by an order or injunction of any court, shall be excluded:

Provided also that where immediately after the exclusion of the period referred to in the immediately preceding proviso, the period of limitation available to the Assessing Officer for passing an order under clause (d) of section 148A is less than seven days, such remaining period shall be extended to seven days and the period of limitation under this subsection shall be deemed to be extended accordingly.

Explanation.—For the purposes of clause (b) of this subsection, “asset” shall include immovable property, being land or building or both, shares and securities, loans and advances, deposits in bank account.

(2) The provisions of subsection (1) as to the issue of notice shall be subject to the provisions of section 151.’

Sanction for issue of notice-

“151. Specified authority for the purposes of section 148 and section 148A shall be—

(i) Principal Commissioner or Principal Director or Commissioner or Director, if three years or less than three years have elapsed from the end of the relevant assessment year;

(ii) Principal Chief Commissioner or Principal Director General or where there is no Principal Chief Commissioner or Principal Director General, Chief Commissioner or Director General, if more than three years have elapsed from the end of the relevant assessment year.”

10. The Hon’ble Apex Court in the case of Union of India & Ors. Vs. Ashish Agrawal, Civil Appeal No.3005/2022, dated 04.05.2022, after deliberating at length on the aforesaid amended provisions, had, inter alia, observed as under:

“5. We have heard Shri N. Venkataraman, learned ASG appearing on behalf of the Revenue and Shri C.A. Sundaram and Shri S. Ganesh, learned Senior Advocates and other learned counsel appearing on behalf of the respective assessee.

6. It cannot be disputed that by substitution of sections 147 to 151 of the Income Tax Act (IT Act) by the Finance Act, 2021, radical and reformative changes are made governing the procedure for reassessment proceedings. Amended sections 147 to 149 and section 151 of the IT Act prescribe the procedure governing initiation of reassessment proceedings. However, for several reasons, the same gave rise to numerous litigations and the reopening were challenged inter alia, on the grounds such as (1) no valid “reason to believe” (2) no tangible/reliable material /information in possession of the assessing officer leading to formation of belief that income has escaped assessment, (3) no enquiry being conducted by the assessing officer prior to the issuance of notice; and reopening is based on change of opinion of the assessing officer and (4) lastly the mandatory procedure laid down by this Court in the case of GKN Driveshafts (India) Ltd. Vs. Income Tax Officer and ors; (2003) 1 SCC 72, has not been followed.

6.1 Further pre Finance Act, 2021, the reopening was permissible for a maximum period up to six years and in some cases beyond even six years leading to uncertainty for a considerable time. Therefore, Parliament thought it fit to amend the Income Tax Act to simplify the tax administration, ease compliances and reduce litigation. Therefore, with a view to achieve the said object, by the Finance Act, 2021, sections 147 to 149 and section 151 have been substituted.

6.2 Under the substituted provisions of the IT Act vide Finance Act, 2021, no notice under section 148 of the IT Act can be issued without following the procedure prescribed under section 148A of the IT Act. Along with the notice under section 148 of the IT Act, the assessing officer (AO) is required to serve the order passed under section 148A of the IT Act. section 148A of the IT Act is a new provision which is in the nature of a condition precedent. Introduction of section 148A of the IT Act can thus be said to be a game changer with an aim to achieve the ultimate object of simplifying the tax administration, ease compliance and reduce litigation.

6.3 But prior to pre-Finance Act, 2021, while reopening an assessment, the procedure of giving the reasons for reopening and an opportunity to the assessee and the decision of the objectives were required to be followed as per the judgment of this Court in the case of GKN Driveshafts (India) Ltd. (supra).

6.4 However, by way of section 148A, the procedure has now been streamlined and simplified. It provides that before issuing any notice under section 148, the assessing officer shall (i) conduct any enquiry, if required, with the approval of specified authority, with respect to the information which suggests that the income chargeable to tax has escaped assessment; (ii) provide an opportunity of being heard to the assessee, with the prior approval of specified authority; (iii) consider the reply of the assessee furnished, if any, in response to the showcause notice referred to in clause (b); and (iv) decide, on the basis of material available on record including reply of the assessee, as to whether or not it is a fit case to issue a notice under section 148 of the IT Act and (v) the AO is required to pass a specific order within the time stipulated.

6.5 Therefore, all safeguards are provided before notice under section 148 of the IT Act is issued. At every stage, the prior approval of the specified authority is required, even for conducting the enquiry as per section 148A(a). Only in a case where, the assessing officer is of the opinion that before any notice is issued under section 148A(b) and an opportunity is to be given to the assessee, there is a requirement of conducting any enquiry, the assessing officer may do so and conduct any enquiry. Thus if the assessing officer is of the opinion that any enquiry is required, the assessing officer can do so, however, with the prior approval of the specified authority, with respect to the information which suggests that the income chargeable to tax has escaped assessment.

6.6 Substituted section 149 is the provision governing the time limit for issuance of notice under section 148 of the IT Act. The substituted section 149 of the IT Act has reduced the permissible time limit for issuance of such a notice to three years and only in exceptional cases ten years. It also provides further additional safeguards which were absent under the earlier regime preFinance Act, 2021.

7. Thus, the new provisions substituted by the Finance Act, 2021 being remedial and benevolent in nature and substituted with a specific aim and object to protect the rights and interest of the assessee as well as and the same being in public interest, the respective High Courts have rightly held that the benefit of new provisions shall be made available even in respect of the proceedings relating to past assessment years, provided section 148 notice has been issued on or after 1st April, 2021. We are in complete agreement with the view taken by the various High Courts in holding so.

8. However, at the same time, the judgments of the several High Courts would result in no reassessment proceedings at all, even if the same are permissible under the Finance Act, 2021 and as per substituted sections 147 to 151 of the IT Act. The Revenue cannot be made remediless and the object and purpose of reassessment proceedings cannot be frustrated. It is true that due to a bonafide mistake and in view of subsequent extension of time vide various notifications, the Revenue issued the impugned notices under section 148 after the amendment was enforced w.e.f. 01.04.2021, under the unamended section 148. In our view the same ought not to have been issued under the unamended Act and ought to have been issued under the substituted provisions of sections 147 to 151 of the IT Act as per the Finance Act, 2021. There appears to be genuine nonapplication of the amendments as the officers of the Revenue may have been under a bonafide belief that the amendments may not yet have been enforced. Therefore, we are of the opinion that some leeway must be shown in that regard which the High Courts could have done so. Therefore, instead of quashing and setting aside the reassessment notices issued under the unamended provision of IT Act, the High Courts ought to have passed an order construing the notices issued under unamended Act/unamended provision of the IT Act as those deemed to have been issued under section 148A of the IT Act as per the new provision section 148A and the Revenue ought to have been permitted to proceed further with the reassessment proceedings as per the substituted provisions of sections 147 to 151 of the IT Act as per the Finance Act, 2021, subject to compliance of all the procedural requirements and the defences, which may be available to the assessee under the substituted provisions of sections 147 to 151 of the IT Act and which may be available under the Finance Act, 2021 and in law. Therefore, we propose to modify the judgments and orders passed by the respective High Courts as under:

(i) The respective impugned section 148 notices issued to the respective assessees shall be deemed to have been issued under section 148A of the IT Act as substituted by the Finance Act, 2021 and treated to be showcause notices in terms of section 148A(b). The respective assessing officers shall within thirty days from today provide to the assessees the information and material relied upon by the Revenue so that the assessees can reply to the notices within two weeks thereafter;

(ii) The requirement of conducting any enquiry with the prior approval of the specified authority under section 148A(a) be dispensed with as a onetime measure visàvis those notices which have been issued under Section 148 of the unamended Act from 01.04.2021 till date, including those which have been quashed by the High Courts;

(ii) The assessing officers shall thereafter pass an order in terms of section 148A(d) after following the due procedure as required under section 148A(b) in respect of each of the concerned assessees;

(iii) All the defences which may be available to the assessee under section 149 and/or which may be available under the Finance Act, 2021 and in law and whatever rights are available to the Assessing Officer under the Finance Act, 2021 are kept open and/or shall continue to be available and;

(iv) The present order shall substitute/modify respective judgments and orders passed by the respective High Courts quashing the similar notices issued under unamended section 148 of the IT Act irrespective of whether they have been assailed before this Court or not.

9. There is a broad consensus on the aforesaid aspects amongst the learned ASG appearing on behalf of the Revenue and the learned Senior Advocates/learned counsel appearing on behalf of the respective assessees.

We are also of the opinion that if the aforesaid order is passed, it will strike a balance between the rights of the Revenue as well as the respective assesses as because of a bonafide belief of the officers of the Revenue in issuing approximately 90000 such notices, the Revenue may not suffer as ultimately it is the public exchequer which would suffer.

Therefore, we have proposed to pass the present order with a view avoiding filing of further appeals before this Court and burden this Court with approximately 9000 appeals against the similar judgments and orders passed by the various High Courts, the particulars of some of which are referred to hereinabove. We have also proposed to pass the aforesaid order in exercise of our powers under Article 142 of the Constitution of India by holding that the present order shall govern, not only the impugned judgments and orders passed by the High Court of Judicature at Allahabad, but shall also be made applicable in respect of the similar judgments and orders passed by various High Courts across the country and therefore the present order shall be applicable to PAN INDIA.

10. In view of the above and for the reasons stated above, the present Appeals are ALLOWED IN PART. The impugned common judgments and orders passed by the High Court of Judicature at Allahabad in W.T. No. 524/2021 and other allied tax appeals/petitions, is/are hereby modified and substituted as under:

(i) The impugned section 148 notices issued to the respective assessees which were issued under unamended section 148 of the IT Act, which were the subject matter of writ petitions before the various respective High Courts shall be deemed to have been issued under section 148A of the IT Act as substituted by the Finance Act, 2021 and construed or treated to be showcause notices in terms of section 148A(b). The assessing officer shall, within thirty days from today provide to the respective assessees information and material relied upon by the Revenue, so that the assessees can reply to the showcause notices within two weeks thereafter;

(ii) The requirement of conducting any enquiry, if required, with the prior approval of specified authority under section 148A(a) is hereby dispensed with as a onetime measure visàvis those notices which have been issued under section 148 of the unamended Act from 01.04.2021 till date, including those which have been quashed by the High Courts. Even otherwise as observed hereinabove holding any enquiry with the prior approval of specified authority is not mandatory but it is for the concerned Assessing Officers to hold any enquiry, if required;

(iii) The assessing officers shall thereafter pass orders in terms of section 148A(d) in respect of each of the concerned assessees; Thereafter after following the procedure as required under section 148A may issue notice under section 148 (as substituted);

(iv) All defences which may be available to the assesses including those available under section 149 of the IT Act and all rights and contentions which may be available to the concerned assessees and Revenue under the Finance Act, 2021 and in law shall continue to be available.

11. The present order shall be applicable PAN INDIA and all judgments and orders passed by different High Courts on the issue and under which similar notices which were issued after 01.04.2021 issued under section 148 of the Act are set aside and shall be governed by the present order and shall stand modified to the aforesaid extent. The present order is passed in exercise of powers under Article 142 of the Constitution of India so as to avoid any further appeals by the Revenue on the very issue by challenging similar judgments and orders, with a view not to burden this Court with approximately 9000 appeals. We also observe that present order shall also govern the pending writ petitions, pending before various High Courts in which similar notices under Section 148 of the Act issued after 01.04.2021 are under challenge.

12. The impugned common judgments and orders passed by the High Court of Allahabad and the similar judgments and orders passed by various High Courts, more particularly, the respective judgments and orders passed by the various High Courts particulars of which are mentioned hereinabove, shall stand modified/substituted to the aforesaid extent only.

All these appeals are accordingly partly allowed to the aforesaid extent.

In the facts of the case, there shall be no order as to costs.

(emphasis supplied by us)

11. Apart from that, we find that the CBDT vide Instruction No.01/2022 while directing the implementation of the judgment of the Hon’ble Supreme Court in the case of Union of India & Ors. v. Ashish Agrawal, Civil Appeal No.3005/2022, dated 04.05.2022, while laying down the procedure that is required to be followed by the jurisdictional Assessing Officers/Assessing Officer had, inter alia, held that if it is a fit case to issue notice u/s. Under Section 148 of the Act, the Assessing Officer shall serve a notice on the assessee u/s 148 after obtaining approval of the specified authority u/s. 151 of the new law.

12. Apropos, the Learned DR’s contention that for the purpose of computing the period of three years from the end of the relevant Assessment Year as provided in section 151 of the Act, the period allowed to the assessee, as per show cause notice issued under clause (b) of section 148A of the Act, shall be excluded, we are unable to concur with the same. We say so, for the reason that as the “proviso” to section 151 of the Act (as was then available on the statute) inter alia, contemplating the exclusion of the time period allowed to the assessee, as per show cause notice issued under clause (b) of section 148A, as mentioned in the “fifth proviso” to section 149 of the Act, had been made available on the statute vide Finance Act, 2023, w.e.f. 01/04/2023; therefore, the same cannot be applied to the case of the present assessee before us.

13. At this stage, we may herein observe that our aforesaid view that in a case where a period of more than three years have elapsed from the end of the relevant assessment year, then, approval for issuing the notice under section 148 of the Act has to be taken from the Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General for issuing the notice under section 148 of the Act is supported by the recent judgment of the Hon’ble High Court of Telangana in Deloitte Consulting India Private Limited vs. The Assessment Unit, Income Tax Department, Civil Writ Petition No. 4061 of 2024, dated 25/09/2025. For the sake of clarity, we deem it apposite to cull out the observations of the Hon’ble jurisdictional High Court in the case of Deloitte Consulting India Private Limited vs The Assessment Unit, Income Tax Department (supra), as under:

“48. The proviso to Section 151 has been introduced by the Finance Act, 2023 with effect from 01.04.2023. The relevant Section 151 with its proviso is applicable to the case of the petitioner is quoted hereunder:

151. Sanction for issue of notice:- Specified authority for the purposes of Section 148 and Section 148A shall be,-

(i) Principal Commissioner or Principal Director or Commissioner or Director, if three years or less than three years have elapsed from the end of the relevant assessment year;

(ii) Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General, if more than three years have elapsed from the end of the relevant assessment year:

Provided that the period of three years for the purposes of clause (i) shall be computed after taking into account the period of limitation as excluded by the third or fourth or fifth provisos or extended by the sixth proviso to sub-section (1) of Section 149.

49. In the present case, the order under Section 148A(d) and notice under Section 148 have been issued on 07.04.2022 relatable to the relevant Assessment Year 2018- 19 i.e., after more than three years from the end of the relevant assessment year. The approval before passing the order under Section 148A(d) of the Act and before issuing of notice under Section 148 of the Act has been taken from the Principal Commissioner of Income Tax by the respondent No.1, which is permissible only if three years or less than three years have lapsed from the end of the relevant assessment year. In the present case, the relevant three years lapsed on 31.03.2022. Therefore, the prior approval of the Principal Chief Commissioner or Principal Director General or the Chief Commissioner or the Director General was required to be obtained before passing of the order under Section 148A(d) or before issuance of the notice under Section 148 of the Act.

50. Learned counsel for the respondent has relied upon the proviso to Section 151 of the Act inserted by the Finance Act, 2023 with effect from 01.04.2023 quoted above to contend that the period of seven days furnished to the assessee to submit reply to the notice under Section 148A(b) issued on 23.03.2022 has to be excluded for counting the period of three years. It is submitted that the proviso is clarificatory in nature and as such, it would operate from the date when the amended Section 151 was brought into force i.e., 01.04.2021. However, such a contention is fit to be rejected since the proviso to Section 151 has been inserted by the Finance Act, 2023 only with effect from 01.04.2023. It, therefore, cannot be applied retrospectively to exclude the period of seven days in furnishing the reply to the notice under Section 148A(b) of the Act by the assessee.

The Assessing Officer could not have assumed exclusion of such a period while passing the order under Section 148A(d) of the Act or issuing notice under Section 148 of the Act on 07.04.2022 that such a proviso excluding the period consumed in furnishing the reply is going to be brought into the statute book by amendment by the Finance Act, 2023 with effect from 01.04.2023. In taxing statutes, intendment cannot be assumed unless specifically expressed in the provision enacted by the legislature. Therefore, the reopening of assessment without sanction/approval of the specified authority in accordance with Section 151 of the Act was bad in law. Consequently, reassessment order dated 16.01.2024 also is bad in law.”

(emphasis supplied by us)

14. We find that the Hon’ble High Court in its aforesaid order had not only observed that in the case of the assessee before them ie., for AY 2018-19, the specified authority for granting approval under section 151 of the Act was the Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General as a period of more than three years had lapsed from the end of the relevant Assessment Year, but had also rejected the claim of the revenue that the “proviso” to section 151 of the Act as had been made available on the statute vide the Finance Act, 2023 w.e.f. 01/04/2023 was to be given a retrospective effect.

15. We, thus, in terms of our aforesaid observation, concur with the Ld. AR that in the present case before us for A.Y. 2018-19, wherein notice under Section 148 of the Act was issued on 28/04/2022, i.e., beyond a period of three years from the end of the assessment year, the A.O. was statutorily obligated to have obtained the approval from either of the authorities specified u/s. 151(ii) of the law as was then available on the statute, viz. Principal Chief Commissioner or Principal Director General or where there is no Principal Chief Commissioner or Principal Director General, Chief Commissioner or Director General. However, as the A.O. had obtained the approval from the Pr. Commissioner of Income Tax, i.e., an authority who was not vested with the requisite jurisdiction as per the mandate of Section 151 of the Act (as made available on the statute w.e.f 01.04.2021); therefore, the assessment so framed by him u/s. 147 r.w.s. 144B of the Act, dated 08/03/2024, being devoid of any valid assumption of jurisdiction, cannot be sustained on that count itself and is liable to be quashed. Accordingly, finding substance in the cross-objection no. 1(c) raised by the assessee before us, we, in terms of our aforesaid observations, quash the assessment framed by the A.O. under Section 147 r.w.s. 144B of the Act, dated 08/03/2024.

16. As we have quashed the assessment framed by the A.O. under Section 147 r.w.s.. 144B of the Act, dated 08/03/2024, for want of a valid assumption of jurisdiction for issuing notice u/s. 148 of the Act in the absence of a valid approval under section 151(ii) of the Act by the appropriate authority, we therefore refrain from adverting to and dealing with the other contentions based on which the revenue has assailed the CIT(A) order before us, which, thus, having been rendered as academic, are left open.

17. In the result, appeal filed by the Revenue is dismissed and the Cross Objection filed by the assessee company, to the extent mentioned above, is allowed.

Order pronounced in the open court on 08th July, 2026.

Author Bio