Case Law Details

India Radiators Limited Vs Mercantile Ventures Limited (NCLT Chennai)

The National Company Law Tribunal (NCLT), Chennai, considered a joint company petition filed by India Radiators Limited (Transferor Company) and Mercantile Ventures Limited (Transferee Company) under Sections 230 to 232 of the Companies Act, 2013, read with the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016, seeking sanction of a Scheme of Amalgamation between the two companies.

In the first motion application, the petitioners sought directions regarding convening or dispensing with meetings of shareholders and creditors. By order dated 02.02.2026, the Tribunal dispensed with the meetings of the Preference Shareholders and Unsecured Creditors of the Transferor Company and directed meetings of the Equity Shareholders of both companies and the Unsecured Creditors of the Transferee Company. The meetings held on 13.03.2026 recorded the prescribed quorum and substantial approval in favour of the Scheme. The second motion petition seeking sanction of the Scheme was filed on 21.03.2026.

The Scheme provided for the amalgamation of India Radiators Limited with Mercantile Ventures Limited. The rationale stated in the Scheme included reduction of administrative and operational costs, elimination of duplication, better utilisation of resources, enhancement of business efficiency, strengthening of the business, and availability of combined assets, cash flows and manpower. The Boards of Directors of both companies had proposed the Scheme.

By order dated 01.04.2026, the Tribunal directed issuance of notices to statutory and regulatory authorities and publication of notices in newspapers. Notices were served on the Regional Director, Registrar of Companies, Official Liquidator, Income Tax Department and other regulators.

The Regional Director filed a report on 01.06.2026 setting out observations relating to the appointed date, employee continuity, share exchange ratio, accounting treatment, dissolution of the Transferor Company without winding up, ROC records, auditor observations, compliance with Sections 240 and 232(3)(i) of the Companies Act, 2013, and other matters. The ROC reported that both companies had filed financial statements and annual returns up to 31.03.2025 and that no inquiry, inspection, investigation, complaint or prosecution was pending. The petitioners responded that the observations relating to the Scheme were factual, acknowledged the ROC report, and undertook to comply with Sections 240 and 232(3)(i).

The Income Tax Department stated that issuance of notice was a procedural requirement and did not affect its right to initiate proceedings under the Income Tax Act, 1961, including reopening assessments or taking recovery proceedings. Relying upon Marshall Sons & Co India Ltd Vs Income Tax Officer, it reserved its rights to proceed independently under the Income Tax Act. It also stated that it had no objection to the proposed Scheme subject to all existing and future tax liabilities of the amalgamating company being borne by the amalgamated company in accordance with Section 170 of the Income Tax Act.

The Official Liquidator sought undertakings regarding protection of employees in service on the appointed date, fixation of the record date after sanction of the Scheme, prohibition on modification of the Scheme without Tribunal approval, and cancellation of inter-se investments only as on the appointed date. The Official Liquidator further stated that the affairs of the Transferor Company appeared not to have been conducted in a manner prejudicial to its members or to public interest, subject to the stated representations. The petitioners furnished affidavits undertaking compliance with each of these observations.

The petitioners also placed on record the statutory auditors’ certificate stating that the accounting treatment in the Scheme complied with applicable Indian Accounting Standards. They filed a valuation report dated 31.03.2025 prepared by two registered valuers, which provided the equity share exchange ratio of ten equity shares of the Transferee Company for every thirty-six equity shares of the Transferor Company.

While considering the reports, the Tribunal observed that the Regional Director had raised no objections. It noted that the appointed date of 01.01.2025 fell within one year of filing the application and therefore remained unchanged. The Tribunal also recorded the petitioners’ undertaking to comply with Sections 240 and 232(3)(i). Regarding the Official Liquidator’s observations, it found that the petitioners had furnished undertakings on employee protection, fixation of the record date, non-modification of the Scheme without Tribunal approval, and cancellation of inter-se investments as on the appointed date, and therefore no further directions were required on those issues. With respect to the Income Tax Department, the Tribunal observed, referring to an earlier NCLT New Delhi order and the decision in Vodafone Essar Gujarat Limited v. Department of Income Tax, that the Department remained at liberty to undertake appropriate recovery proceedings in accordance with law.

After analysing the Scheme, the Tribunal held that it appeared beneficial to the companies and was not detrimental to the interests of their shareholders. In the absence of material objections and after finding that the requisite statutory compliances had been fulfilled, the Tribunal sanctioned the Scheme of Amalgamation. It clarified that the sanction did not prevent action for any statutory violation or deficiency discovered subsequently and did not grant exemption from payment of stamp duty, taxes or other statutory charges or from compliance with other legal requirements.

The Tribunal ordered transfer and vesting of the Transferor Company’s business, assets, liabilities, duties and obligations in the Transferee Company, allotment of shares under the Scheme, continuation of pending proceedings by or against the Transferee Company, transfer of employees without interruption of service, filing of revised constitutional documents where required, filing of the order with the Registrar of Companies within thirty days, dissolution of the Transferor Company without winding up upon registration, liberty to interested persons to seek directions from the Tribunal, and approval of the Scheme subject to the directions contained in the order. The company petition was disposed of accordingly.

FULL TEXT OF THE NCLT JUDGMENT/ORDER

1. This Joint Company Petition has been filed by INDIA RADIATORS LIMITED (hereinafter referred as 1st Petitioner Company / Transferor Company), and MERCANTILE VENTURES LIMITED (hereinafter referred as 2nd Petitioner Company / Transferee Company) under section 230-232 of the Companies Act, 2013, and other applicable provisions of the Companies Act, 2013 read with Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 (for brevity ‘the Rules’) for approval of the Scheme of Amalgamation (hereinafter referred to as the ‘SCHEME’) proposed between the Petitioners Company. The Scheme is appended as “Annexure – 3” at Page Nos. 192-219 of the Petition typeset.

2. 1ST MOTION APPLICATION

2.1 The Petitioner Companies had filed First Motion Application vide CA (CAA) / 103 (CHE) / 2025 and sought directions for Dispensation/ Convening the meeting of its Members/ Shareholders and Creditors regarding approval of the proposed Scheme, which is extracted as follows:

| Company | Equity Shareholders | Preference Shareholders | Secured Creditors | Unsecured Creditors |

| Transferor Company | Convene Meeting | Dispense With | NA | Dispense With |

| Transferee Company | Convene Meeting | NA | NA | Convene Meeting |

2.2 Based on the submissions, this Tribunal vide Order dated 02.02.2026 ordered to dispense of the meetings of Preference Shareholders and Unsecured Creditors of Transferor Company, and to convene the meetings of Equity Shareholders of both Companies and Unsecured Creditors of Transferee Company. The same is reproduced as follows:

II. Report of Chairman and Scrutinizer in Brief – Meeting Details

Report of Chairman filed before Tribunal: Date 17-03-2026 & Sr. No. 3305118041452025

Particulars |

Transferor Company Meeting Date |

QUORUM |

% of Person Present & Voting |

Name of Chairperson & Scrutinizer |

||

No. of Persons Present and Voting |

Total % of Voting in Terms of the Value of Shares/Credit |

Favour |

Against |

|||

Equity Shareholders |

13-03-2026 |

35 |

47.13% |

10% |

NIL |

K Gaurav Kumar – Chairperson; A U Maithreyi – Scrutinizer |

Preference Shareholders |

Dispensed with |

|||||

Secured Creditors |

Not applicable |

|||||

Unsecured Trade Creditors |

Dispensed with |

|||||

Unsecured Loan Creditors |

Not applicable |

|||||

Others (if any) |

None of Public shareholders voted against the resolution as per SEBI Circular |

|||||

Transferee Company

Particulars |

Transferee Company Meeting Date |

QUORUM |

% of Person Present & Voting |

Name of Chairperson & Scrutinizer |

||

No. of Persons Present and Voting |

Total % of Voting in Terms of the Value of Shares/Credit |

Favour |

Against |

|||

Equity Shareholders |

13-03-2026 |

62 |

89.96% |

99.997% |

0.00003% |

K Gaurav Kumar (Chairperson); A U Maithreyi (Scrutinizer) |

Preference Shareholders |

Not applicable |

|||||

Secured Creditors |

Not applicable |

|||||

Unsecured Trade Creditors |

13-03-2026 |

14 |

78.45% |

100% |

— |

K Gaurav Kumar (Chairperson); A U Maithreyi (Scrutinizer) |

Unsecured Loan Creditors |

||||||

Others (if any) |

99.9993% of public shareholders who voted for the meeting voted for the resolution as per SEBI Circular |

|||||

2.3. Subsequently, the second motion petition was filed before this Tribunal by the Petitioner Company on 21.03.2026 for sanction of the Scheme of Arrangement (Amalgamation) by this Tribunal.

3. SCHEME SUMMARY

The Scheme provides for the Arrangement between INDIA RADIATORS LIMITED With MERCANTILE VENTURES LIMITED their respective Shareholders and Creditors. Both the Petitioner Companies come under the jurisdiction of this Tribunal.

4. RATIONALE OF THE SCHEME

The rationale and benefits of the Scheme are briefed in Clause C of the Part A of the Scheme as follows,

RATIONALE FOR THE SCHEME OF AMALGAMATION:

“a) By this amalgamation, it is expected that the administrative and operational costs will be considerably reduced and the Transferee Company will be able to operate and run the business/operations more effectively and economically resulting in better turnover and profits.

b) It is expected that the proposed Scheme of Amalgamation will benefit the Transferee Company in the usual economies of a centralized and a large company including elimination of duplication of work, reduction in overheads, better and more productive utilization of human and other resource and enhancement of overall business efficiency and will bring in synergies for the Transferee Company post amalgamation. It will help the Transferee Company to use the combined managerial and operating strength, to build a wider capital and financial base and to promote and secure overall growth of the business, thereby it will make available to the Transferee Company, the benefit of technical and marketing expertise of both the companies.

The said Scheme of Amalgamation will contribute in fulfilling and furthering the objects of these companies. It will strengthen, consolidate and stabilize the business of these companies and will facilitate further expansion and growth of their business.

The Transferee Company will have the benefit of the combined assets, cash flows and man-power of both the companies. These combined resources will enhance its capability to expand and improve its efficiency of operations.”

It is stated that the Board of Directors of both the Petitioner Companies have proposed the Scheme of Amalgamation. This Scheme provides for various other matters consequential or otherwise integrally connected herewith.

5. In the second motion Petition filed by the Petitioner Companies, this Tribunal vide order dated 01.04.2026 directed the Petitioner Companies to issue notice to the Statutory / Regulatory Authorities concerned and to issue paper publication.

6. In compliance with the said directions issued by this Tribunal, the Petitioner Companies effected paper publications in “Business Standard” in English (All India Edition) and “Dina Thanthi” in Tamil (Tamil Nadu Edition) on 10.04.2026.

7. The notices were also served to

(i) Regional Director, Southern Region, Chennai,

(ii) Official Liquidator,

(iii) Income Tax Department and other regulators.

It is also seen that notices have been also served to

| S.No | Statutory authorities | Date of Notice |

| 1. | Regional Director, Southern Region, Chennai | 06.04.2026 |

| 2. | Registrar of Companies, Chennai | 06.04.2026 |

| 3. | Income Tax Department | 06.04.2026 |

| 4. | Official Liquidator | 06.04.2026 |

Pursuant to the service of notice of the petition, the following statutory authorities have responded.

8. STATUTORY / REGULATORY AUTHORITIES

8. 1. REGIONAL DIRECTOR

8.1.1. The Regional Director (RD), Southern Region to whom the notice was served, has filed its report on 01.06.2026 and has expressed its ‘Observations’. The same are as follows,

| Para | Observations |

| 4 | As per Clause 4 of Part A of the Scheme, “Appointed Date” means 1st January 2025, or such other date as may be fixed or approved by the Tribunal or such other competent authority. |

| 5 | As per Clause 5 of Part II of the Scheme, all permanent employees (including deputed employees) of the Transferor Company shall become employees of the Transferee Company on such date as if they were in continuous service without any break or interruption in service, and on terms and conditions relating to employment and remuneration that are not less favourable than those on which they are engaged or employed by the Transferor Company, become the employees of the Transferee Company as and from the Appointed Date. The Scheme also provides that the Transferee Company undertakes to continue to abide by any agreement/settlement, if any, validly entered into by the Transferor Company with any union/employee of the Transferor Company recognized by the Transferor Company. |

| 6 | Clause 8 of Part II of the Scheme provides that upon the Scheme becoming effective and in consideration of the transfer and vesting of the Transferor Company in the Transferee Company in terms of the Scheme, the Transferee Company shall, subject to the provisions of the Scheme and without any further application or deed, issue and allot Equity Shares to shareholders, administrators, and legal representatives determined as on the Record Date, whose names are recorded in the register of members of the Transferor Company, in the following proportion:“10 (Ten) equity shares of the Transferee Company with the face value of INR 10/- each fully paid up for every 36 (Thirty-Six) equity shares of the Transferor Company with a face value of INR 10/- each fully paid up.” |

| 8 | Clause 10.1 Part Il of the scheme provides that, upon the Scheme becoming effective, the Transferor Company and the Transferee Company being under common control, the Amalgamation of the Transferor Company with the Transferee Company shall be accounted by the Transferee Company as per the “Pooling of interest Method provided under Appendix C of Ind AS 103, ‘Business Combinations’ notified under Section 133 of the Act.

Clause 10.2 Part II of the scheme provides that, upon the scheme coming into effect, all the assets and liabilities of the Transferor Company shall be transferred to and vested in the Transferee Company and shall be recorded at their respective book values. Clause 10.3 Part II of the scheme provides that, upon the scheme coming into effect, the difference between the amount recorded as share capital issued by Transferee Company (Securities issued will be recorded at their nominal value) and the amount of share capital of the Transferor Company shall be transferred to capital reserve of the Transferee Company. |

| 9 | Clause 13.1 Part II of the scheme provides that, upon the effectiveness of this Scheme, the Transferor Company shall be dissolved without winding up, and the Board of Directors and any committees thereof of the Transferor Company shall without any further act, instrument or deed stands dissolved. |

| 11 | The ROC Chennai vide report dated 04.05.2026 stated that the petitioner Companies have filed financial statements and Annual Returns up to 31.03.2025. It is further stated that No Inquiry/ Inspection/ Investigation/ Complaint/ Prosecution is pending.

It is observed from the audited Balance Sheet year ended 31.03.2025 of Transferor and Transferee company, there are no undisputable dues and statutory dues pending with the Transferor company As per the Independent Auditor’s report of the Transferee company, the company has disclosed the impact of pending litigations on its financial position vide No.31. In the Transferee Company, the independent auditor has reported vide para iii (c) of Annexure B that in respect of loans and advances in the nature of loans, wherever the schedule of repayment of principal and payment of interest is stipulated by the company, the repayments are regular except for Rs.3,32.77 lakhs where the repayment for interest and principal is not as stipulated by the company. The company has provided Rs.337.16 Lakhs as Expected Credit Loss in respect of such loans. It is also stated that the Transferor and Transferee companies have filed BEN 2. |

| 12 | The Petitioner Companies may be directed to undertake to comply with the provisions of Section 240 of the Companies Act, 2013 and provisions of Section 232(3)(i) of the Companies Act, 2013. |

8.1.2 It is submitted by the RD that the petition may be disposed of on merits after considering the submissions made in para 11 and 12.

Response to the RD Report:

8.1.3 The Petitioners have filed response to the RD Report dated 10.06.2026. The response to the report of the RD is tabulated hereunder:

| Para | Observations |

| 1 to 9 | It is stated the observations made from Paras 1 to 9 are the details of the scheme, which are factual in nature. So, there have no remarks for the same. |

| 10 | It is stated that this para is an affirmation given by Registrar of Companies and no adverse remarks have been made by ROC in its report. |

| 12 | The petitioner companies hereby declare and undertake to comply with the provisions of Section 240 of the Companies Act, 2013 and provisions of Section 232(3)(i) of the Companies Act, 2013 |

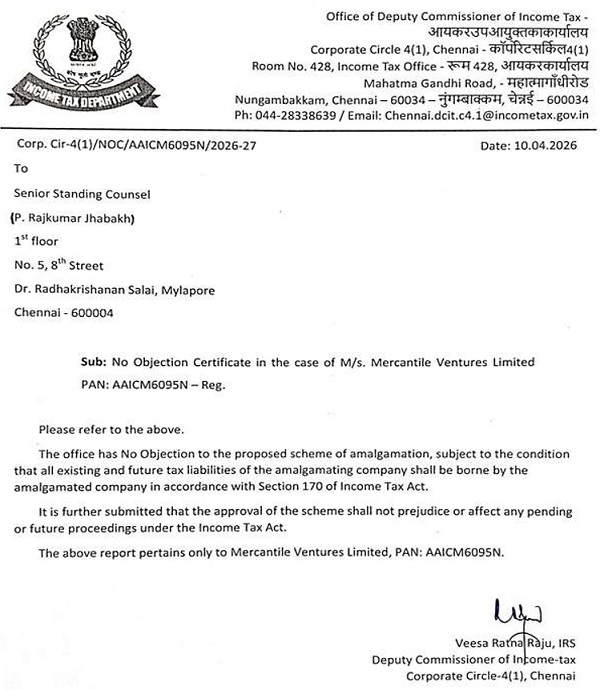

8.2. INCOME TAX DEPARTMENT

8.2.1 The Income Tax Department to whom the notice was served has filed its report on 13.04.2026 and has expressed its ‘Observations’ as follows:

8.2.2 The requirement to send notice to the concerned department is a procedural requirement and as such does not impact the right of the Department to proceed in accordance with the provisions of the Income Tax Act, 1961. It is prayed that this Tribunal may take the objections on record without prejudice to the rights of the Department to take all appropriate proceedings under the provisions of the Income Tax Act, 1961 to protect the interest of the government including the right to reopen the assessment. Therefore, by way of filing of this memo and the report, the Income Tax Department shall not have deemed to waive its rights to undertake all proceedings under the Income Tax Act, 1961.

8.2.3 Reliance is placed on the judgement of the Hon’ble Supreme Court in Marshall Sons & Co India Ltd Vs Income Tax Officer (AIR 1997SC1763 & MANU/SC/0407/1997). It is stated that the Income Tax Department reserves its right to proceed against the Petitioner Companies through independent proceedings under the provisions of the Income Tax Act, 1961 and pass orders in accordance with law. The relevant para 17 of the Judgement is extracted as under:

“17. We, however, make it clear that we have not expressed any opinion on the plea of the learned Counsel for the Revenue that the amalgamation itself is a device designed to evade the taxes legitimately payable by the subsidiary company. If the Income Tax authorities think that, they are entitled to raise this question in the proceedings under the Income Tax Act, it is open to them to do so by way of a separate proceeding according to law.“

(emphasis supplied)

8.2.4 It is stated that in line with the judgment of Hon’ble Supreme Court, the Income Tax Department reserves its right to proceed against the Petitioner Companies through independent proceedings under the provisions of the Income Tax. It is reiterated that filing of the present memo shall not in any manner amount to waiving its rights to proceed against the Petitioner Companies and pass orders in accordance with law.

8.2.5 It is stated that the office has no objections to the proposed scheme of amalgamation, subject to the condition that all existing and future tax liabilities of the amalgamating company shall be borne by the amalgamated company in accordance with Section 170 of Income Tax Act. The letter to this effect is reproduced as under:

8.3. OFFICIAL LIQUIDATOR

8.3.1 The Official Liquidator to whom the notice was served, has filed its report on 23.04.2026 and has expressed its ‘Observations’ to the Scheme as follows:

| Para | Observations |

| 3(i) | The clauses 1.h and 5.1 of Part I (Definitions) of the Scheme seeks to protect all permanent employees of the Transferor Company only if they are in service as on effective date, and hence, this Tribunal may be pleased to direct the companies to submit an undertaking to this Tribunal to the effect that there would be no retrenchment of any employee who were in service as on Appointed Date (01.01.2025) as well except in the event of their resignation on their own before the Effective Date. |

| 3(ii) | The record date as defined in clause 1.m of Part I (Definitions) of the scheme does not provide for fixing the record date mutually by the respective board of directors of both transferor company and transferee company. In this regard, this Tribunal may direct the companies to submit an undertaking that it would be fixed mutually and they would fix the record date immediately after sanction of the scheme and before the effective date / dissolution date or subject to the SEBI guidelines since Transferee Company is a listed company. |

| 3(iii) | The clause 14.3 provides for auto modification of content of the scheme, post its sanction by this Tribunal, it is submitted that such auto modification of the content of the scheme to be in compliance with Income Tax Law etc., without the previous approval / sanction of this Tribunal will be in violation of section 231(1)(b) of the Companies Act, 2013 as every modification of the content of the Scheme requires approval by this Tribunal. Hence, this Tribunal may be pleased to direct the Transferor and Transferee Companies to delete / modify the 14.3 of the scheme by way of amendment to the scheme proposed, so as to ensure that no such auto amendment / modification of the Scheme takes place, post its sanction by this Tribunal or to submit an undertaking to this Tribunal to the effect that such auto modification of the content of the scheme will not be implemented without prior approval of this Tribunal. |

| 3(iv) | Clause 8.2 of the scheme, states that the inter-se investments as existed on Effective Date are proposed to get cancelled as per scheme. It is submitted that the inter se investments as existed as on appointed date only will get cancelled and not any subsequent transactions, as the same would be considered as transactions of the transferee alone, upon sanction of the scheme. Hence the clause 8.2 of the scheme need amendment to provide for cancellation of inter se investments as on appointed date only or to submit an undertaking to this Tribunal to the effect that inter se investments as existed as on appointed date only will get cancelled |

8.3.2 It is stated that the Official Liquidator is of the opinion that the affairs of the Transferor Company appear to have not been conducted in a manner prejudicial to the interest of its members or to public interest subject to representation in para 3 above.

8.3.3 The Official Liquidator has sought to take on record the report. He has also sought to fix the remuneration payable to the Auditor who has investigated into the affairs of Transferor Company.

Response to the OL Report:

8.3.5 The Petitioners have filed response to the OL Report dated 05.05.2026. The response to the report of the OL is tabulated hereunder:

| Para | Observations |

| 1 | In the affidavit submitted by the petitioner companies, it is stated that the transferee company undertakes to that the staff, workmen and employees of the Transferor Company in permanent service on the Appointed Date and they shall become the staff, workmen and employees of the Transferee Company on such date without any break or interruption in service and on the terms and conditions and not in any way less favourable to them than those subsisting with reference to the Transferor Company as the case may be on the said date. |

| 2 | The companies undertake that the record date would be fixed after approval of the Board of both the transferor Company and the transferee Company. |

| 3 | The companies undertake that the Board of the Transferee Company will not undertake any modification to the Scheme without the prior approval of this Tribunal. |

| 4 | The companies undertake that the inter-se investments as on the appointed date only would get cancelled as any further transactions will be considered as transactions on behalf of the Transferee Company only. |

9. ACCOUNTING TREATMENT

The Petitioners have stated that the Statutory Auditors have examined the Scheme and certified that the Accounting Treatment contained in the proposed Scheme of Arrangement is compliant with the Applicable Indian Accounting Standards. The Certificate issued by the Statutory Auditors certifying the Accounting Treatment of the Petitioner Companies are placed at Annexure 8 of the typed set.

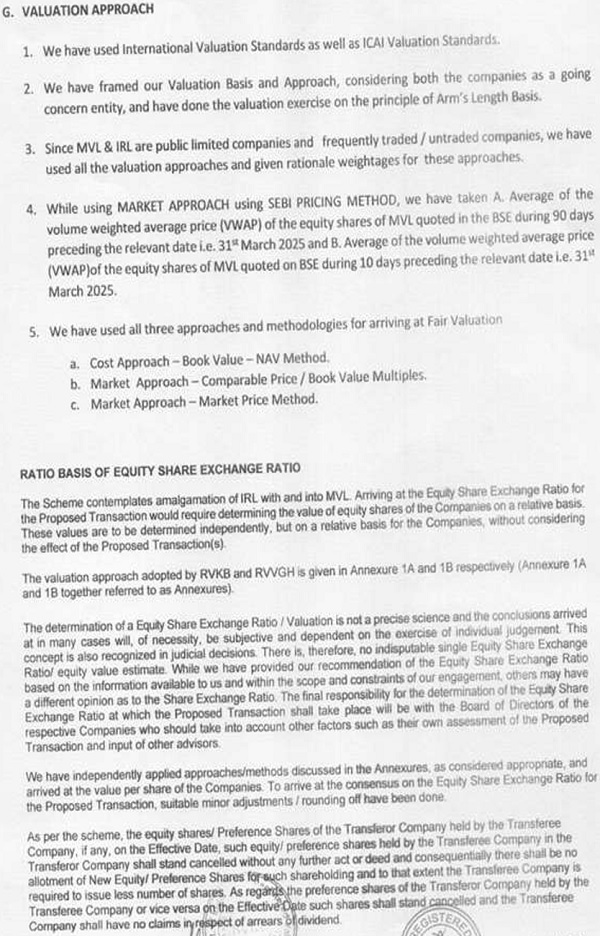

10. VALUATION

The Petitioner Company has filed Valuation Report obtained from two Registered Valuer, namely, Kalyanam Bhaskar and V. G. Hareesh. The valuation report dated 31.03.2025 is placed as Annexure 5 of the Petition typeset. The Valuation Approach and the Share Entitlement Ratio Analysis of the Independent Valuer is extracted hereunder for reference,

Equity Share Exchange Ratio:

“10 (Ten) equity shares of MVL of INR 10/- each fully paid up for 36 (Thirty-Six) equity shares of IRL of INR 10/- each fully paid up.”

Our Valuation Report and Equity Share Exchange Ratio is based on the equity share capital structure of the MVL Limited and IRL Limited as mentioned earlier in this report. Any variation in the equity capital of the Companies may have material impact on the Equity Share Exchange Ratio.

It should be noted that we have not examined any other matter including economic rationale for the Proposed Transaction per se or accounting, legal or tax matters involved in the Proposed Transaction.

11. OBSERVATIONS OF THIS TRIBUNAL:

11.1 REGIONAL DIRECTOR:

11.1.1 This tribunal observes that no objections have been raised by the RD in his report.

11.1.2 With respect to the Appointed Date of the Scheme, it is noted that Clause 4 stipulates the Appointed Date as 01.01.2025. The application in CA(CAA)/103(CHE)/2025 came to be filed before this Tribunal on 11.12.2025. 11.1.3 As per MCA General Circular No. 09/2019, if the chosen appointed date precedes the date of filing the application for the Scheme with the NCLT by more than one year, the specific justification for doing so must be adequately disclosed in the Scheme. The same is extracted as follows:

“c) where the ‘appointed date’ is chosen as a specific calendar date, it may precede the date of filing of the application for scheme of merger/amalgamation in NCLT. However, if the ‘appointed date’ is significantly ante-dated beyond a year from the date of filing, the justification for the same would have to be specifically brought out in the scheme and it should not be against public interest.”

11.1.4 Here, the Appointed Date falls within one year from the date of filing the application under Section 230 of the Companies Act, 2013.

11.1.5 Hence, the Appointed Date shall remain as 01.01.2025, as specified in Clause 1(c) of the Scheme.

11.1.6 It is also noted that the petitioner have furnished an undertaking to the observation made in Para 12 to comply with the provisions of Section 240 and Section 232(3)(i) of the Companies Act, 2013.

11.2 OFFICIAL LIQUIDATOR:

11.2.1 This Tribunal now analyses the objections raised by the Official Liquidator (hereinafter, OL) and the submissions made by the Petitioner.

11.2.2 Employee Protection Undertaking

This tribunal observes that the OL seeks an undertaking for the protection of employees as envisaged in Clause 1.h and 5.1 of Part I of the Scheme. In compliance with the same, the petitioner companies have filed an affidavit undertaking the protection.

11.2.3 Record Date

The OL has made an observation seeking the petitioners to undertake that they will mutually fix the Record date immediately after the sanction of the scheme. It is observed that the Petitioners have undertaken that the Record Date shall be fixed mutually and immediately after the sanction of the Scheme and prior to the dissolution of the Transferor Company.

11.2.4 Auto Modification of scheme without prior consent of tribunal:

It is stated that Clause 14.3 of the scheme provides for auto modification of content of the scheme in case it is found to be violation of Section 2(1B) and Section 47 of the Income Tax, 1961, post its sanction by this Tribunal. Hence, it is submitted that such auto modification of the content of the scheme without the sanction of this Tribunal will be in violation of section 231(1)(b) of the Companies Act, 2013. The petitioners in their undertaking have stated that the Transferee Company shall not undertake any modification without the prior approval of the tribunal. In view of the said undertaking, the objection does not survive and no further directions are required in this regard.

11.2.5 Cancellation of Inter-se Investments

It is stated by the OL that Clause 8.2 of the scheme provides that inter-se investments as existed on Effective Date are to be cancelled on appointed date. It is submitted by the petitioners in their affidavit that the inter-se investments as on appointed date only would get cancelled as any further transactions will be considered as transactions on behalf of Transferee Company. In view of the said undertaking, the objection does not survive and no further directions are required in this regard.

11.3 DEPARTMENT OF INCOME TAX

11.3.1 In Company Petition CAA-284/ND/2018 vide Order dated 12.11.2018, the NCLT New Delhi has made the following observations with regard to the right of the IT Department in the Scheme of Amalgamation,

“taking into consideration the clauses contained in the Scheme in relation to liability to tax and also as insisted upon by the Income Tax and in terms of the decision in RE:

Vodafone Essar Gujarat Limited v. Department of Income Tax (2013)353 ITR 222 (Guj) and the same being also affirmed by the Hon’ble Supreme Court and as reported in (2016) 66 taxmann.com.374(SC) from which it is seen that at the time of declining the SLPs filed by the revenue, however stating to the following effect vide its order dated April 15,2015 that the Department is entitled to take out appropriate proceedings for recovery of any statutory dues from the transferor or transferee or any other person who is liable for payment of such tax dues, the said protection be afforded is granted. With the above observations, the petition stands allowed and the scheme of amalgamation is sanctioned.”

11.3.2 Hence, the Income tax Department is at liberty to undertake appropriate recovery proceedings in accordance with law.

12. After analysing the Scheme in detail, this Tribunal is of the view that the Scheme as contemplated amongst the Petitioner Companies seems beneficial to the Companies and will not be in any way detrimental to the interest of the shareholders of the Companies. In the absence of any other objections having been placed on record, this Tribunal sanctions the Scheme as well as the prayer made therein.

13. Notwithstanding the above, if there is any deficiency found or, violation committed qua any enactment, statutory rule or regulation, the sanction granted by this Tribunal will not come in the way of action being taken, albeit, in accordance with law, against the concerned persons, directors and officials of the petitioners.

14. While approving the Scheme as above, it is clarified that this order should not be construed as an order in any way granting exemption from payment of stamp duty, taxes or any other charges, if any, payment is due or required in accordance with law or in respect to any permission/compliance with any other requirement which may be specifically required under any law.

15. This Tribunal is of the view that the scheme as contemplated by the Petitioner companies seems to be prima facie not, in any way detrimental to the interest of the members of the Companies. In view of the absence of any material objections from any statutory authorities and since all the requisite statutory compliances have been fulfilled, this Tribunal sanctions the Scheme of Amalgamation as well as the prayer made therein.

16. Notwithstanding the above, if there is any deficiency found or, the violation committed qua any enactment, statutory rule or regulation, the sanction granted by this Tribunal will not come in the way of action being taken, albeit, in accordance with the law, against the concerned persons, directors and officials of the petitioners.

17. While approving the Scheme as above, it is clarified that this order should not be construed as an order in any way granting exemption from payment of stamp duty, taxes or any other charges, if any, payment is due or required in accordance with law or in respect to any permission/ compliance with any other requirement which may be specifically required under any law.

18. THIS TRIBUNAL DO FURTHER ORDER

(i) That the entire business and undertaking of the Transferor Company shall, under the provisions of Section 230 to 232 of the Companies Act, 2013, without further act or deed, be transferred to and vest in or be deemed to have been transferred and vested in the Transferee Company.

(ii) That all the assets of the Transferor Company shall be transferred to the Transferee Company, without further deed or instrument of conveyance and accordingly the same become the property of the Transferee Company.

(iii) That all the debts, liabilities, duties and obligations of the Transferor Company shall be transferred to the Transferee Company and accordingly the same become the liabilities and duties of the Transferee Company.

(iv) That the Transferee Company do without further application allot to such members of the Transferor Company, as have not given such notice of dissent, as is required by Clause 13 of the SCHEME herein the shares in the Transferee Company to which they are entitled under the said Scheme.

(v) That the Appointed date for the Scheme shall be 01.2025 as mentioned in Clause 1(C) of the Scheme.

(vi) That all proceedings now pending by or against the Transferor Companies be continued by or against the Transferee Company.

(vii) That all the employees of the Transferor Company in service from the Appointed Date till the date on which the Scheme finally takes effect, shall become the employees of the Transferee Company without any break or interruption in their service.

(viii)That the Transferee Company shall file the revised Memorandum and Articles of Association with the Registrar of Companies and further make the requisite payments of the differential fee (if any) for the enhancement of authorized capital of the Transferee Company after setting off the fees paid by the Transferor Company.

(ix) That the Transferor Company and the Transferee Company, shall within thirty days of the date of receipt of this order cause a certified copy of this order to be delivered to the Registrar of Companies for registration. That as per Clause 16(iii) of the Scheme, on such certified copy being so delivered, the Transferor Company shall be dissolved without the process of winding up and the Registrar of Companies shall place all documents relating to the Transferor Company registered with him on the file kept by him in relation to the Transferee Company and the files relating to the said company shall be consolidated accordingly.

(x) That any person interested shall be at liberty to apply to the Tribunal in the above matter for any directions that may be necessary.

19. The Scheme is approved subject to the directions issued above.

20. Company Petition CP(CAA)/24(CHE)2026 in CA(CAA)/103(CHE)2025 accordingly, stands disposed of on the aforementioned terms.

Author Bio