Case Law Details

Himadri Speciality Chemical Limited Vs Commissioner of CGST & Central Excise (CESTAT Ahmedabad)

The CESTAT Ahmedabad allowed the appeal against the Commissioner (Appeals)’ order dated 16.05.2018, which had upheld a service tax demand of ₹1,67,291, interest and penalty under the reverse charge mechanism (RCM) in respect of alleged manpower supply services. The demand arose from audit findings that loading and unloading charges paid to a contractor attracted service tax under Notification No. 30/2012-ST. The appellant challenged the demand on jurisdiction, merits and limitation.

The Tribunal identified two issues: whether the show cause notice issued by Vadodara Audit-III Commissionerate and adjudicated by Valsad Commissionerate was without jurisdiction in view of the appellant’s centralized service tax registration with Kolkata Commissionerate, and whether the contract with the contractor constituted manpower supply service liable to service tax under RCM.

On jurisdiction, the Tribunal noted there was no dispute that the appellant held centralized registration with the Kolkata Service Tax Commissionerate. Relying on decisions in MIRC Electronic Ltd. and Larsen and Toubro Ltd., it held that the action of Vadodara Audit-III Commissionerate in issuing the show cause notice and Valsad Commissionerate in confirming the demand was beyond jurisdiction. On this ground alone, the service tax demand was held to be unsustainable.

On merits, the Tribunal examined the work order and found that the contractor was entrusted with loading, unloading, batch charging and cargo handling work, with payment on a per metric tonne basis. The contractor remained responsible for supervision, control and safe execution of the work, including liability for damage caused by improper handling. The Tribunal held that the contract was for execution of specified work and not for supply of manpower. Relying on Gokul Ram Gurjar, Shailu Traders and Ramadhar Singh, it concluded that the services did not fall within the category of manpower supply service. Accordingly, the demand did not survive on merits. The impugned order was set aside and the appeal was allowed.

FULL TEXT OF THE CESTAT AHMEDABAD ORDER

M/s. Himadri Chemicals & Industries Ltd., Vapi (Appellant) filed the present appeal against impugned order dated 16.05.2018 passed by learned Commissioner (Appeals), Surat.

1.1 As per the facts, Audit officers scrutinized the records and balance sheet of the company and found that the appellant had incurred expenses under miscellaneous head towards loading and unloading charges paid to Mr. Shyam B. Mandel, who supplied man power to the appellant. Revenue alleged that as per Notification No.30/2012-ST dated 20.06.2012, the appellant was required to pay service tax on 75% of the value of man power supply service on reverse charge basis (RCM). Accordingly, show cause notice dated 27.11.2015 was issued to appellant by invoking extended period of limitation under proviso to Section 73(1) of the Finance Act, 1994 for demanding service tax of Rs.1,67,291/- for the year 2012-2013 to 2014-2015 under man power supply service on RCM basis along with interest under Section 75 of the Finance Act, 1994 and penalty under Section 78(1) of the said Act. It was alleged that they have suppressed the fact of receipt of manpower supply service from the department and thus, evaded payment of service tax. The show cause notice mentioned that the appellant was having centralized service tax registration with Kolkata Service Tax Commissionerate.

1.2 The matter was decided by the Assistant Commissioner vide order dated 04.05.2017 wherein, he confirmed the service tax demand of Rs.1,67,291/-along with interest and also imposed equal penalty under Section 78. Aggrieved with this order, the appellant filed appeal before the Commissioner (Appeals) who upheld the order of the lower authority by rejecting their appeal. Hence, the present appeal before this Tribunal.

2. In their appeal, the appellant took following grounds:-

- Learned Commissioner (Appeals) grossly erred in completely brushing aside their appeal dated 03.08.2017. Therefore, impugned order is passed without proper consideration of their submissions and verification of details and hence, liable to be set aside.

- They are having centralized registration with Kolkata Service Tax Commissionerate which fact has also been admitted in the show cause notice. In their case, show cause notice for demanding service tax can only be issued by Kolkata Service Tax Commissionerate. Therefore, show cause notice issued by Vadodara Audit-III Commissionerate and the order passed by CGST, Division-II, Valsad are beyond jurisdiction. This contention on the aspect of jurisdiction has simply been brushed aside by the Adjudicating Authority as well as Appellate Authority.

- Under man power supply service, service tax is applicable only when one or more person is supplied under a contract. They have entered into a contract with Mr. Shyam B. Mandal for loading and unloading purpose and charging of raw materials in the plant during manufacturing process. The contractor is responsible for the said work who undertakes necessary supervision during the process of loading and unloading and ensures that materials are lifted properly, within time and with due care. The contractor is paid on the basis of agreed per MT rate of loading, unloading and charging of materials. As per the nature of contract, service tax on such service is not payable and so, demand of service tax on reverse charge basis under Notification No.30/2012-ST dated 20.06.2012 without providing any evidence and document is unsustainable.

- Learned Commissioner (Appeals) falsely alleged that the present case attracts manufacturing process, and so, the above transactions attract central excise duty and does not attract service tax. Payment to the contractor on the basis of specific contract given for loading and unloading and charging of material is governed under the Finance Act, 1994 and they being receiver of service, cannot be asked to pay service tax under reverse charge mechanism.

- Both the lower authorities have deliberately ignored CBIC Circular No.190/9/2015- ST dated 15.12.2015 which clarifies the difference between supply of man power service vis-à-vis service contract.

- Learned Commissioner (Appeals) has justified invocation of extended period of limitation when there is no willful mis-statement or suppression of fact in this case. Had they paid service tax under reverse charge mechanism, they would have been entitled to the Cenvat Credit. Therefore, as held by Hon’ble Supreme Court in the case of Nirlon Ltd reported at 2015 (320) ELT 22 (SC), there cannot be any question of evasion of duty in case of revenue neutrality. These principles were further followed by Hon’ble Madras High Court in the case of CCE Vs. Tenneco RC India Pvt. Ltd. reported at 2015 (323) ELT 299.

In view of the above, appellant pleaded for allowing their appeal by setting aside the impugned order.

3. During arguments, learned Advocate submitted that the contract entered into between the appellant and Mr. Shyam B. Mandal, makes it clear that the contract is on completion of work and payment is on Per MT basis. The entire work is to be done by the contractor by deputing suitable number of persons under his supervision and control. Revenue has no evidence that man power were supplied by the contractor who were under the supervisory control of the appellant. He placed reliance on CBIC Circular dated 16.12.2015 which clearly provides guidelines as to when a service can be considered as man power supply service. Learned Advocate also pleaded that since they are registered with Kolkata Service Tax Commissionerate vide registration No. AAACH7475HST001 for payment of service tax liability arising anywhere in the country under reverse/ forward charge and no separate registration was taken for their Vapi unit, the show cause notice for demanding service tax or it’s confirmation by Valsad Commissionerate is beyond the jurisdiction. Hence, on this ground itself, the demand confirmed by lower authorities does not survive.

3.1 Learned Advocate relied on the decision in the case of Gokul Ram Gurjar Vs. CCE, Jaipur reported at 2018 (19) GSTL 269 (Tri. Del.) to plead that the rate contract provided in the work order clearly indicates that the amount shall be paid at a fixed basis and therefore, the service provided should not fall under taxable category of man power supply service. He also relied on the decision of CESTAT Delhi in the case of Shailu Traders Vs. CCE, Indore reported at 2018 (10) GSTL 462 (Tri.-Del) and decision in the case of Shri Ramadhar Singh Vs. CCE, Raipur reported at 2018 (9) GSTL 303 (Tri.-Del) to emphasize the above point.

3.2 On jurisdiction issue, he relied on the decision in the case of MIRC Electronic Ltd. Vs. CCE, Noida reported at 2019 (25) GSTL 120 (Tri.-All) and CCE Hyderabad Vs. Larsen and Toubro Ltd. reported at 2019 (24) GSTL 64 (Tri. Hyd). Learned Advocate also pleaded that extended period is not invocable in this case as there is no intention to evade payment of tax. He also invokes ground of revenue neutrality in the case. For this proposition, he relied on the decision of CESTAT Delhi in the case of Siddharth Polysacs Pvt. Ltd. Vs. Commissioner, CGST- Jaipur I reported at 2025 SCC Online CESTAT 3067, decision in the case of Nirlon Ltd reported at 2015 (320) ELT 22 (SC) and decision in case of CCE Vs. Tenneco RC India Pvt. Ltd. (cited supra).

4. Countering the arguments, learned AR reiterated the findings of the lower authority. He justified that the contract with Mr. Shyam B. Mandal was for supply of labour for loading/ unloading and not for specific job with defined quantum of work. The recipient exercises control over the labour and the payment was linked to the provision of person rather than completion of specific measurable output. Regarding jurisdiction, he states that the taxable event i.e. receipt of manpower supply service and payment to the contractor occurred at Vapi plant, hence, Valsad Commissionerate has rightly exercised their jurisdiction. He also defended invocation of extended period on the ground that the appellant failed to disclose these transactions in ST-3 returns and the same could only be found out by the officers during audit of their records. Learned AR pleaded that the impugned order be upheld and the appeal filed by the appellant be set aside.

5. We have heard the rival submissions. We find that there are two main issues in this case-

(a) Whether action to issue show cause notice by Vadodara Audit- III Commissionerate and it’s adjudication by Valsad Commissionerate is beyond jurisdiction as the tax payer was centrally registered with Kolkata Service Tax Commissionerate?

(b) Whether in the facts of the case, appellant has received man power supply service from Mr. Shyam B. Mandal and is liable to pay service tax on reverse charge basis?

5.1 On the first issue, we find that CESTAT Allahabad in the case of MIRC Electronic Ltd. Vs. CCE, Noida (cited supra) has clearly held that authorities at Noida had no jurisdiction to raise demand on tax payer having centralized registration at Mumbai. The Commissioner (Appeals) in this case had held that from the copy of registration, claim of centralized registration made by the appellant was not correct. The Tribunal in this case, observed that the finding of learned Commissioner (Appeals) is factually incorrect and therefore, it set aside the impugned order and remanded the matter to Commissioner (Appeals) for fresh decision on the issue of jurisdiction.

5.2 In the case of Commissioner of Customs, Central Excise and Service Tax, Hyderabad-II Vs. Larsen and Toubro Ltd. (cited supra), the Tribunal held that the Commissionerate where centralized registration has been obtained has the jurisdiction to issue the demand even when services provided outside the territorial jurisdiction of that Commissionerate. In this case, the appellant had challenged the jurisdiction of Hyderabad-II Commissionerate, where they obtained centralized registration on the ground that the services have been provided outside the jurisdiction. The Tribunal in para-6 of the said decision reproduced below:-

“6. As far as the jurisdiction is concerned, we do not find any merits [in] the appellants arguments, as they have themselves applied for and got Centralized Registration with Hyderabad Commissionerate-H, and the Commissionerate has jurisdiction to issue the demand even when the services are provided outside territorial jurisdiction of Hyderabad Commissionerate-H, which comes out clearly from statement of Mr. Udaybhasker, that they have been granted Centralized Registration even for A. P. & Chattisgarh. Further it is not in dispute that all the records and accounts relating to RIL project are maintained by appellant at its Hyderabad office. Thus, the jurisdiction of Hyderabad Commissionerate cannot be questioned.”

5.3 We find that there is no dispute that the appellant is having centralized registration with Kolkata Service Tax. Revenue has not supported their say by any decision which could justify legality of action taken by Vadodara Audit III Commissionerate in issuance of show cause notice and of Valsad Commissionerate in confirming the demand against the appellant despite their centralized registration at Kolkata. We therefore, agree with the contention of the appellant and hold that the action to issue show cause notice by Vadodara Audit III and demand confirmation order passed in this case by Valsad Commissionerate are beyond jurisdiction. On this ground itself, the demand of Service Tax does not survive.

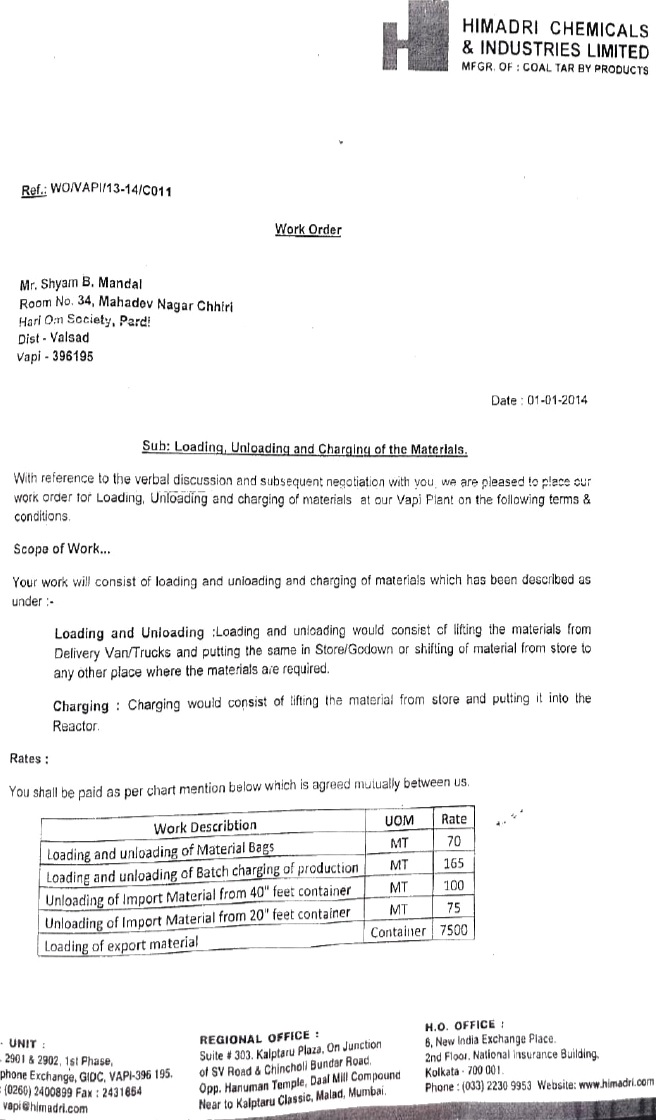

5.4 On merits, we find that the appellant had entered into a contract with Mr. Shyam B. Mandal for loading and unloading of material, batch charging of production, unloading of import material and loading of export goods in containers etc. Copy of one such work order dated 01.01.2014 is reproduced below:-

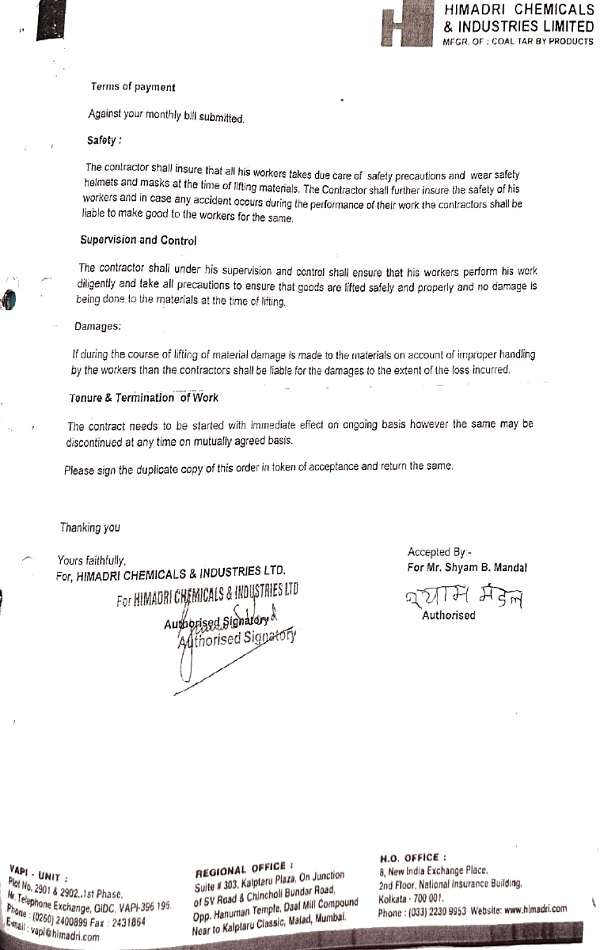

As per above contract, the work entrusted to the contractor was for loading and unloading of material bags, loading and unloading of batch charging for production and loading of export cargo and unloading of import cargo on behalf of the appellant. The payment to the contractor was on per MT basis. Under the heading, “Supervision and Control”, it is mentioned that “the contractor shall under his supervision and control shall ensure that his workers perform his work diligently and take all precautions to ensure that goods are lifted safely and properly and no damage is being done to the materials at the time of lifting.” It is also mentioned that if there is any damage to materials on account of improper handling by the workers, then the contractors shall be liable for the damages to the extent of the loss incurred. The language of the contract clearly reveals that it is not for supply of manpower and only specific work was assigned to the contractor for completion.

5.5 We find that CESTAT Delhi in the case of Gokul Ram Gurjar Vs. CCE, Jaipur (cited supra) has held that the scope of work described in work orders determines classification of service. In this case, work relates to washing of cans/crates and packing of milk. Since, there was no specific mention about deployment of labour/ work force, the services provided by the appellant should not fall under the taxable category of man power supply service. The work order clearly indicates that the amount shall be paid on per liter for per pack basis. Since, there is no specific mention about payment or reimbursement of wages and salaries to the work man, the services provided should not fall under the taxable category of service.

5.6 Similarly, in the case of Shailu Traders (cited supra), the Tribunal held that the activities of material handling and shifting within the premise does not fall within the ambit of man power supply service. The relevant para-6 of the said decision is reproduced below:-

“6. On perusal of the conditions contained in the agreement, it reveals that the manpower/employees deployed for executing the assigned task were under the control and supervision of the appellant and the activities undertaken pursuant to the agreement relate to the work of material handling and shifting. Since the appellant was in no way connected with any recruitment or supply of manpower to the client, rather the manpower/employees were under the active control and supervision of the appellant and were deployed for undertaking the assigned job work entrusted by the principal, in our considered view, such service should not fall under the taxable category of ‘Manpower Recruitment and Supply Agency Service’.”

5.7 Similar findings have been given by CESTAT Delhi in the case of Ramadhar Singh Vs. CCE, Raipur (cited supra). In this case also, the appellant was executing various jobs relating to production and maintenance of furnace. It was held that since essence of contract is execution of assigned work and control over the workman and supervision was always with the appellant, it cannot be said that the activities undertaken by the appellant fall under the category of man power recruitment or supply agency service, for levy of service tax.

5.8 Relying on above decisions, we hold that the present contract is not for man power supply service. Therefore, demand of service tax from the appellant does not survive on merits also. In view of the above, revenue’s case does not survive on both the counts. Accordingly, we set aside the impugned order dated 16.05.2018 and allow the appeal filed by the appellant.

6. The appeal is allowed.

(Pronounced in the open court on 02.06.2026)

Author Bio