Case Law Details

In re Refex Industries Ltd (NCLT Chennai)

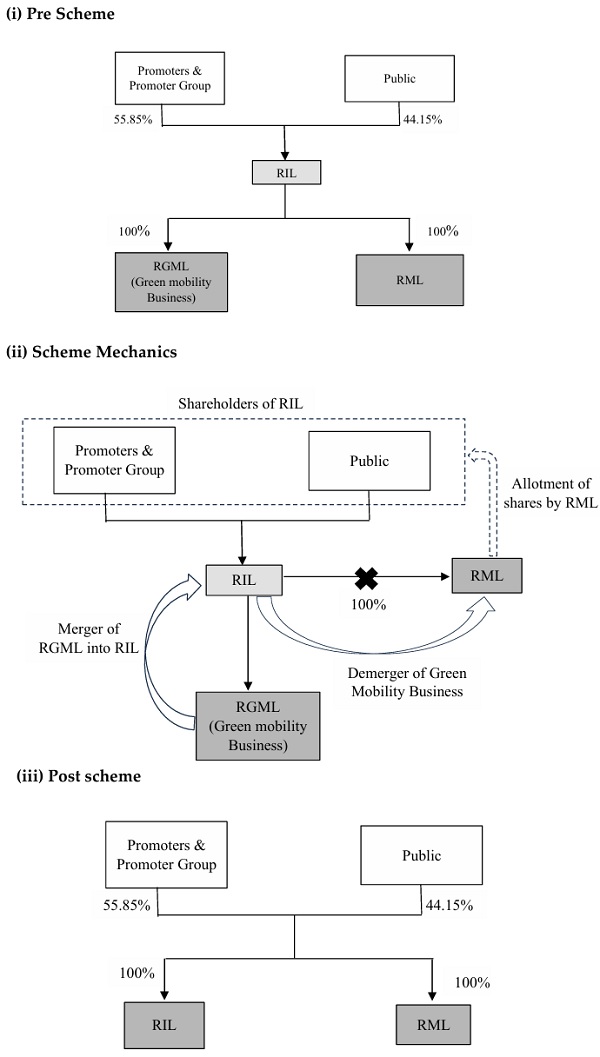

The National Company Law Tribunal (NCLT), Chennai Bench, considered an application filed by Refex Industries Limited (RIL), the Transferee and Demerged Company, seeking approval to proceed with a Composite Scheme of Amalgamation and Arrangement under Sections 230 to 232 of the Companies Act, 2013. The Scheme involved three companies: Refex Green Mobility Limited (RGML), Refex Industries Limited (RIL), and Refex Mobility Limited (RML). RGML and RML are wholly owned subsidiaries of RIL.

The Scheme proposed three principal steps. First, RGML would amalgamate with RIL, resulting in the cancellation of the entire share capital held by RIL in RGML without the issuance of any new shares. Second, the Green Mobility Business Undertaking, which would vest in RIL following the amalgamation, would be demerged into RML. Under the Scheme, RML would issue one fully paid equity share of ₹2 for every one fully paid equity share of ₹2 held by shareholders of RIL on the record date. Third, the existing 50,000 equity shares of RML held by RIL would be cancelled without payment, with the reduction credited to the capital reserve of RML, and without requiring a separate process under Section 66 of the Companies Act.

The rationale presented for the Scheme stated that RIL operates businesses in ash and coal handling, green mobility, and wind power. According to the application, the businesses have different financial profiles, risk characteristics, and growth opportunities. The Scheme was intended to create an independent listed entity focused exclusively on the Green Mobility Business, enabling dedicated management, separate investment opportunities, independent capital raising, collaboration with strategic partners, and enhanced value for shareholders.

The Tribunal also noted developments concerning share warrants. At the time of filing, RIL had ten warrant holders. However, since the remaining 75% subscription amount was not paid within the exercise period, the initial subscription money was forfeited, leaving no outstanding warrant holders. Updated certificates from a Chartered Accountant and confirmations from former warrant holders were placed on record.

The Board of Directors of RIL approved the Composite Scheme on 22 September 2025. The company also filed a valuation report, a fairness opinion from an independent SEBI-registered merchant banker, auditor certificates confirming compliance with accounting standards, and observation letters issued by both BSE and NSE regarding the draft Scheme.

By an earlier order dated 9 June 2026, the Tribunal sought several clarifications. These included whether the Scheme required modification due to the absence of outstanding warrants, details of assets and liabilities proposed to be transferred at each stage of the Scheme, and compliance with disclosure requirements specified by BSE and NSE. The stock exchanges had required disclosures relating to ongoing investigations, enforcement actions, assets and liabilities before and after the Scheme, revenue impact, rationale, cost-benefit analysis, revised shareholding patterns, latest financial statements, and other relevant information to enable shareholders to make informed decisions.

In response, RIL clarified that no modification to the Scheme was necessary because the provisions regarding warrants would apply only if warrants remained outstanding on the record date, which was not the case. The company also submitted charts detailing the assets and liabilities proposed to be transferred, information regarding ongoing investigations and enforcement actions, updated financial information, reports explaining the Scheme’s rationale and expected business synergies, and revised shareholding patterns for the transferor, transferee, and resulting companies. RIL further stated that the Scheme would not adversely affect its revenue-generating capacity because the assets transferred to RIL through the merger would subsequently be demerged into RML, while enabling enhanced managerial focus.

After hearing the applicant and examining the documents, the Tribunal concluded that the clarifications sought had been adequately addressed.

Accordingly, the NCLT directed that meetings of RIL’s stakeholders be convened. The Tribunal noted that the company had 97,015 equity shareholders, eight secured creditors, and 388 unsecured creditors. It directed that meetings of equity shareholders, secured creditors, and unsecured creditors be held on 5 August 2026 at specified times, either at the registered office, through video conferencing, or at another Tribunal-approved venue.

The Tribunal prescribed quorum requirements of 30 equity shareholders, three secured creditors, and 30 unsecured creditors. It appointed a Chairperson and a Scrutinizer for conducting the meetings, fixed their remuneration, and laid down detailed procedural directions. These included adjournment provisions where quorum was not met, compliance with applicable MCA circulars, issuance of individual notices at least 30 days before the meetings, publication of advertisements in specified English and Tamil newspapers, reporting of voting results, service of notices on statutory authorities and regulators, furnishing copies of the Scheme upon request, filing affidavits confirming compliance with directions, and strict adherence to the Companies Act, 2013 and the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016.

Finding the application and accompanying material satisfactory, the Tribunal allowed the application on the stated terms and issued directions for convening the stakeholder meetings in connection with the proposed Composite Scheme of Amalgamation and Arrangement.

FULL TEXT OF THE NCLT JUDGMENT/ORDER

Under consideration is a Company Application viz., CA(CAA)/43(CHE)/2026 filed by Refex Industries Limited (hereinafter “Second Applicant Company” / “Transferee company” / “Demerged Company” / “RIL”) seeking approval of Composite Scheme of Amalgamation and Arrangement (hereinafter referred to as the “SCHEME”) involving three companies viz., Refex Industries Limited, Refex Green Mobility Limited, (hereinafter “First Applicant Company” / “Transferor Company” / “RGML”) and Refex Mobility Limited (“Third Applicant Company” / “Resulting company” / “RML”) their respective shareholders and creditors under Section 230-232 of Companies Act, 2013, and other applicable provisions of the Companies Act, 2013 (hereinafter “The Act”) read with Companies (Compromises, Arrangements and Amalgamations) Rules, 2016. The Scheme is appended as “Annexure A1” of the application.

2. RGML and RML are wholly owned subsidiaries of RIL. RIL is a company incorporated on 13.09.2002 under the Act and is primarily engaged in the business of ash & coal handling amongst other activities. RIL, through its subsidiaries is also engaged in green mobility business and has recently started wind power business. The equity shares of RIL are listed on the Bombay Stock Exchange (“BSE”) and the National Stock Exchange (“NSE”).

3. The Applicant Company in this Company Application has sought for the following reliefs;

| Equity

Shareholders |

Secured Creditors |

Unsecured Creditors |

|

| Second Applicant Company/ Transferee Company/ Demerged Company |

Convening the meeting |

Convening the Meeting | Convening the meeting |

4. The Applicant has filed Memo dated 25.05.2026 and Memo dated 26.05.2026 wherein it is stated that at the time of filing the Application, RIL had 10 (ten) Warrant Holders. The consent affidavits of 4 (four) Warrant Holders constituting 76% of the total value of warrant holders was placed on record.

5. It is stated that RIL had received an amount of Rs.1,30,68,90,000/-(Rupees One Hundred Thirty Crores Sixty-Eight Lakhs Ninety Thousand Only) as upfront payment, representing 25% of the initial subscription amount from the warrant holders, however, the payment of the remaining 75% of the amount was not received by the Company before the expiry of the exercise period of 06.05.2025. Hence, the initial subscription money received from the warrant holders was forfeited by RIL. In light of above developments at present, there are no warrant holders in the Company. The Applicant has filed an updated list of warrant holders as on 12.05.2026 certified by Chartered Accountant stating that there are NIL share-warrant holders. The Chartered Accountant Certificate is annexed and placed in the 2 to 3 of the Memo dated 26.05.2026.

6. The Applicant, vide Memo dated 01.06.2026 has filed the confirmations from the respective warrant holders acknowledging that the warrants held by them have been forfeited. The same is annexed and placed at 120-129.

Steps Involved in the Scheme

7. It is stated that the Scheme is presented under Sections 230-232 and other applicable provisions of the Companies Act, 2013, rules and regulations thereunder. Steps involved in the Scheme are as under:

i. Amalgamation of Refex Green Mobility Limited (‘RGML’) with Refex Industries Limited (‘RIL’);

a. The Transferor Company, RGML, is a wholly owned subsidiary of the Transferee Company / Demerged Company. On Amalgamation of RGML with RIL the entire share capital of the Transferor Company held by Transferee Company/ Demerged Company shall stand cancelled under Clause 15 Part B of the Scheme and no new shares of the Transferee Company/ Demerged Company shall be issued to the shareholders of the Transferor Company/ Demerged Company.

ii. Demerger of the Green Mobility Business Undertaking of RIL (vested in RIL pursuant to amalgamation of RGML with RIL) into Refex Mobility Limited (‘RML’);

a. On Demerger the Demerged Undertaking from RIL into RML, the Resulting Company, RML, shall issue and allot to the shareholders of the Demerged Company whose name appears in the register of members of the Demerged Company as on the Record Date, shares in ratio provided in Clause 28 of Part C of the Scheme, as extracted hereunder:

a. Issue of shares of the Resulting Company to the Equity Shareholders of the Demerged Company:

“1 (One) fully paid-up Equity Share of Rs. 2 each of the Resulting Company shall be issued and allotted as fully paid up for every 1 (One) Equity Shares of Rs. 2 each fully paid up held in the Demerged Company.”

iii. The Reduction and cancellation of existing equity shares of the RML held by RIL under Clause 29 of Part C of the Scheme;

a. Upon the Scheme becoming effective and upon the issue of shares by the Resulting Company in accordance with Clause 28.1 of the Scheme, the existing 50,000 equity shares of Rs. 2/- each of the Resulting Company held by the Demerged Company, as on the Effective Date, shall without any application or deed, stand cancelled without any payment.

b. The reduction/cancellation of share capital of the Resulting Company held prior to implementation of the Scheme will result in mirroring the shareholding pattern of the Demerged Company in the Resulting Company. The reduction of share capital of Resulting Company shall be effected as an integral part of this Scheme and Resulting Company shall not be required to follow the process under Section 66 of the Act or any other provisions of Applicable Law separately. Further, the above reduction/cancellation of share capital will be credited to the capital reserve in the books of Resulting Company.

Rationale of the Scheme

8. The rationale of the scheme is provided in Clause 4 of Part A as under:

i. “RIL is primarily engaged in the business of Ash & Coal handling amongst other activities. RIL through its subsidiaries is also engaged in Green mobility business and has recently started Wind power business.

ii. Each of the varied businesses carried on by RIL either by itself or through strategic investments in subsidiaries have significant potential for growth and profitability.

iii. The nature of risk and competition, financial profiles and return ratios involved in the Ash & Coal handling business of RIL are distinct from Green Mobility Business presently undertaken through its wholly subsidiary RGML.

iv. The Green Mobility Business is capable of attracting a different set of investors, lenders, strategic partners and other stakeholders and have significant potential for growth and profitability. In order to unlock value for all stakeholders, the group plans to have the Green Mobility Business Undertaking as a separate listed entity parallel to RIL which is proposed to be undertaken as follows:

a. Merger of RGML into RIL;

b. Demerger of the Green Mobility Business Undertaking (merged with RIL) into RML and independently list RML.

v. The following benefits shall accrue on the scheme;

a. Creation of an independent global scale company focusing exclusively on Green Mobility Business Undertaking and taking advantage of the growth potential in the said respective sector;

b. Enabling greater focus of management in the relevant businesses (in RIL and RML) thereby allowing new opportunities to be explored for each business efficiently and allowing a focused strategy in operations;

c. Both RIL and RML can attract different sets of investors, strategic partners, lenders, and other stakeholders enabling independent collaboration and expansion at their end;

d. Enabling investors to separately hold investments in respective businesses (either in RIL or RML) with different investment characteristics thereby enabling them to select investments which best suit their investment strategies and risk profiles;

e. Enabling focused and sharper capital market access (debt and equity) and thereby unlocking the value of the Green Mobility Business Undertaking and creating enhanced value for shareholders.”

Graphical Representation of the Scheme

9. The Transferee Company/ Demerged Company has filed its Memorandum and Articles of Association inter alia delineating its object clauses. The Transferee Company has filed its last available Audited Financial Statements as on 31.03.2025 and Unaudited Financial Statements as on 31.12.2025 and the same is placed at Page No. 103-179. The object of the Applicant is set out in Clause III of the Memorandum of Association. The extracts of the main objects, inter alia, are briefly as under:

“1. “To manufacture, fill in cylinders or tankers, store, import, export, distribute, sell or otherwise deal in industrial gases, refrigerant gases, coolants and gases of all kinds and description.

2. To manufacture, buy, sell, import, export or otherwise deal in cylinders and other accessories used in the manufacture, storage, filling and refilling of gases of all kinds and description.

3. To construct, renovate, modify, improve, demolish, dispose of or otherwise deal in storage tanks used in the storage of gases of all kinds and description.

4. To engage in the business of electric power supply generation and establishment of power supply stations and sub stations und works, including running and managing them based on all forms of conventional and non-conventional source of energy including wind power, solar power, Thermal, Hydro, Coal and Lignite based generation among others and also to engage in distribution and supply of power to end users either directly by laying down of cables, wires and lines or through agencies, including governmental, both central government and state governments and local government and municipal corporations.

5. To Enable, Facilitate, Initiate, Engage and carry on the business of purchase and sale of all forms of electrical Power/Energy, both conventional, nonconventional and Renewable, within India amongst Power users, Producers, State Electricity Boards, Power Utilities Generating Companies, Distribution and all other Traders including import and export of Electrical Power, Supply and Trading of Electrical Power/Energy across all local State Boundaries and Various Union Territories within the geographical borders of the Country and also across National borders, wherein trading of Such Electrical Power is permitted by law of both the Buyers and Sellers country of Origin and the infrastructure for carrying out such Electrical Power trading is existing and permitted.

‘5A. To Facilitate and carry on other allied services including but not limited to the sale, purchase trading of Carbon Credits, CDM (Clean Development Mechanisms), ES Certs, CER (Carbon Emission Reduction), all other forms of Renewable Energy Certificates (RE Certs) and any other Certificates to Power users within geographical borders of Country.

5B. To carry on Consultancy services in the field of power trading, supply of electricity, and other related services to Power users, Producers, State Electricity Boards, Power Utilities Generating Companies and Distribution companies.

5C. ‘To obtain a license for the development of a transparent, neutral, and automated Power Exchange and/or technology platform for the trading of electrical power.

6. To act as a contractor for installing power plants and grids on behalf of third parties or actual users.

7. To engage in the business of dealers and traders in machineries, equipment’s, panels, components and systems and for all other types of materials including raw materials, intermediaries required in connection with the generation, supply and distribution of electricity through both conventional and non-conventional means, Infrastructural projects relating to roads laying, building constructions, selling up of airports, seaports and Railway projects.

8. To carry on the business of purchasers, promoters, developers, Vendors, builders, and real estate brokers of land and building sites, flats, apartments, dwelling houses, resorts, commercial complexes, offices, shops, and properties or building and engineering consultants.

9. To carry on the business of buying, selling, reselling, importing, exporting, transporting, storing, developing, promoting, marketing or supplying, trading, dealing in any manner whatsoever in all type of goods on retail well as on wholesale basis in India or elsewhere.

10. To act as broker, trader, agent, C & F agent, shipper, commission agent, distributor, representative, franchiser, consultant, collaborator, stockiest, to liaison, job worker, export house of goods, merchandise and services pf all grades, specifications, descriptions, applications, modalities, fashions, including by products scraps or accessories thereof, on retail as well as on wholesale basis.”

10. The authorized, issued, subscribed and paid-up capital of the Transferee company/ Demerged Company as on 31.12.2025 are as follows:

| Particulars | Amount in INR |

| Authorised Capital | |

| Equity shares (47,50,00,000 Nos of Rs. 2 each) | 95,00,00,000 |

| Preference Shares (5,00,000 Nos of Rs. 100 each) | 5,00,00,000 |

| Total | 100,00,00,000 |

| Subscribed and Paid up | |

| Equity shares (13,71,29,532 Nos of Rs. 2 each) | 27,42,59,064 |

| Total | 27,42,59,064 |

11. The summary of the latest financial position of the Transferee Company/ Demerged Company as on 31.12.2025, is as follows:

| Particulars | Amount in INR Lakhs |

| Net Worth | 1,34,527.50 |

| Share warrants – Pending allotment | 13,068.90 |

| Turnover | 1,33,817.20 |

| Current Assets | 1,79,588.27 |

| Non-Current Assets | 40,372.95 |

| Current Liabilities | 63,868.94 |

| Non-Current Liabilities | 8,495.89 |

12. The Board of Directors of the Transferee Company/ Demerged Company has at its meeting held on 22.09.2025, approved and adopted the Composite Scheme of Amalgamation and Arrangement.

13. The Valuation Report dated 22.09.2025 issued by the Registered Valuer recommending fair equity share entitlement ratio for the proposed amalgamation of RGML with RIL and fair equity share entitlement ratio and warrant entitlement ratio for the demerger of green mobility business undertaking of RIL into RML, has been filed the Fairness Opinion Report dated 22.09.2025 issued by Kroll Advisory Private Limited an independent SEBI registered Merchant Banker (“Fairness opinion”), has also been filed.

14. An affidavit in support of the above application sworn in, on behalf of the Transferee Company/ Demerged Company has been filed by Ankit Poddar in the capacity of Authorised Signatory. It is represented that the registered office of the Transferor Company is situated at Chennai, Tamil Nadu and therefore it is within the jurisdiction of this Tribunal.

15. The Appointed date as specified in the Scheme is 01.04.2025.

16. The Statutory Auditors of the Transferee Company have examined the Scheme in terms of provisions of Section 232 of Companies Act, 2013 and the Rules made thereunder and certified that the Accounting Standards are in compliance with Section 133 of the Companies Act, 2013. The Accounting Treatment Certificate for the Transferor Company is annexed along with the Application as “Annexure A13”.

17. It is stated that the observation letter of the draft scheme of amalgamation and arrangement has been issued by BSE on 16.03.2026 vide letter DCS/AMAL/RD/R37/4123/2025-26. It is placed at Page No. 250-254 of the application. Observation letter of the draft scheme of amalgamation and arrangement has been issued by NSE on 16.03.2026 vide letter NSE/LIST/51151. It is placed at Page no. 255-259 of the application.

18. This Tribunal vide order dated 09.06.2026 sought clarifications from the Applicant, extracted as under:

“1. As per the Memo dated 01.06.2026, there are no warrant holders on date as their rights have been forfeited. Whether the Composite Scheme has to be modified including para 28.2 and 28.3? If so, revised scheme along with changes in ‘Share Capital & Net worth’ of the applicant be provided.

2. It is observed that assets and liabilities of Transferor Company are initially transferred to transferee company and thereafter the same are transferred by way of demerger to resulting company. A chart containing the value of list of assets and liabilities being transferred/ demerged in the books of i) Transferor Company, ii) Transferee/ Demerged undertaking and iii) Resulting company be submitted with explanatory statements wherever required.

3. As per the Observation letters issued by BSE and NSE,

i. The listed company should disclose all details of ongoing adjudication & recovery proceedings, prosecution initiated and all other enforcement action taken, if any, against the Company, its promoters and directors, before NCLT and shareholders, while seeking approval of the scheme.

ii. The listed Company shall ensure that the following additional disclosure to the public shareholders as a part of explanatory statement or notice or proposal accompanying resolution to be passed to be forwarded by the Company to the shareholders while seeking approval u/s 230 to 232 of the Companies Act 2013, to enable them to take an informed decision.

1. Details of assets, liabilities, net worth and revenue of the companies involved, pre and post scheme

2. Impact of scheme on revenue generating capacity of listed entity

3. Need and Rationale of the scheme, Synergies of business of the companies involved in the scheme, Impact of the scheme on the shareholders and cost benefit analysis of the scheme

4. Value of assets and liabilities of Transferor Company that are being transferred to Transferee Company

5. Value of assets and liabilities of Demerged Company that are being transferred to Resultant Company

6. Latest financials of Transferor, Transferee and Resulting companies should be updated on the also to be disclosed Website and same in the explanatory statement

7. Revised shareholding and pattern of Transferor, Transferee Resulting companies Pre and Post-Scheme

8. Pre and Post scheme shareholding Transferor, of Transferee and Resulting companies as on the date of notice of Shareholders meeting along with rationale for changes, if any, occurred between filing of Draft Scheme to Notice to Shareholders

9. Disclose all pending actions against the entities involved in the scheme its promoters/directors/KMPs and possible impact of the same on the Transferee Company to the shareholders

10. The Company shall that ensure applicable additional information, if any to be submitted to SEBI along with draft scheme of arrangement as advised by email dated March 16, 2026 shall form part of disclosures to the shareholders”

19. The Applicant submitted the clarifications by Memo dated 18.06.2026 vide S.R. No. 2622. The clarifications are as below:

a. It is stated that Clause 28.2 of the Scheme provides that, Refex Mobility Limited (“Resulting Company” or “RML”) shall allot share warrants, convertible into equity shares, in respect of such warrants of the Demerged Company that are outstanding as on the Record Date (as defined in the Scheme), in accordance with the Warrant Entitlement Ratio (as defined in the Scheme), as consideration for the vesting of the Demerged Undertaking(as defined in the Scheme). However, no warrants remain outstanding as on the Record Date, accordingly, the obligation to allot corresponding share warrants by the Resulting Company would not arise. Since the Scheme contemplates the treatment of outstanding warrants as on the Record Date, no modification to the Scheme is required. The current status of outstanding warrants of the Demerged Company, as disclosed in Annexure-1 of the Scheme is provided below:

| Particulars | No of warrants | Issue price per warrant in INR | Current status |

| Promoter/Promoter Group: | |||

| Refex Holding Private Limited | 75,75,000 | 125 | Converted into equity shares on October 03, 2025 |

| Ugamdevi Jain | 26,50,000 | 468 | Forfeited on May 06, 2026 |

| Dimple Jain | 26,50,000 | 468 | |

| Yash Jain | 26,45,000 | 468 | |

| Public | 32,25,000 | 468 | |

| Total | 1,87,45,000 |

b. It is stated that a chart setting out the details of the assets and liabilities as on the Appointed Date i.e., 01.04.2025 proposed to be transferred/demerged, in the books of (i) the Transferor Company, (ii) the Transferee/Demerged Undertaking, and (iii) the Resulting Company, is annexed hereto and marked as Annexure 1 of the Memorandum.

c. With respect to the observations made by BSE and NSE, it is stated that the list of ongoing material investigations, adjudication and recovery proceedings, prosecutions initiated, and all other enforcement actions taken against the applicant companies and their directors and promoters as on 16.06.2026, is enclosed as Annexure 2. The details of assets, liabilities, net worth and revenue of the companies as submitted with NSE and BSE while obtaining their no objection to the Scheme is enclosed as Annexure 3.

d. It is stated that the Scheme is not anticipated to adversely generating affect on the revenue-capacity of the Transferee/Demerged Company. Since all assets and liabilities transferred to the Transferee Company pursuant to the merger under Part B of the Scheme are subsequently proposed to be demerged into the Resulting Company under Part C of the Scheme, it does not affect the revenue generating capacity of the listed company (i.e., RIL). Further, as outlined in Point 2 of Paragraph 4.5 of the Scheme, one of the key benefits envisaged is enhanced managerial focus on the relevant business segments of RIL following the implementation of the Scheme.

e. It is stated that the need and rationale for the scheme, business synergies between the companies involved, impact on shareholders, and cost-benefit analysis have been detailed in the report adopted by the Board of Directors of the Transferee Company vide dated 22.09.2025. The report is annexed and marked as Annexure 4 of the Memo thereto.

f. It is stated that latest financials of the Transferor Company, Transferee/Demerged Company and Resulting Company as on 31.12.2025 are enclosed as Annexure 5. It is also stated that the annual report for the FY 2025-26 which consists of the financials as on 31.03.2026, is under preparation.

g. The shareholding pattern of the respective companies as on 16.06.2026, is provided as under;

“RGML/Transferor Company:

Pre Scheme:- The Transferor Company is a wholly owned subsidiary of Transferee Company.

Post Scheme:- Post the merger under Part B, the Transferor Company ceases to exist the, hence the post scheme shareholding pattern is not applicable.

RIL/Transferee/Demerged Company:

Pre Scheme shareholding pattern of the Transferee/Demerged Company:

| Category | No. of equity shares of INR 2 each | Paid up share capital in INR | % of equity shares |

| Promoter and Promoter group | 7,66,23,085 | 15,32,46, 170 | 55.84% |

| Public | 6,05,96,363 | 12,11,92, 726 | 44.16 % |

| Total | 13,72,19, 448 | 27,44,38, 896 | 100% |

Post Scheme shareholding pattern of the Transferee/Demerged company:

| Category | No. of equity shares of INR 2 each | Paid up share capital in INR | % of equity shares |

| Promoter and Promoter group | 7,66,23,085 | 15,32,46, 170 | 55.84% |

| Public | 6,05,96,363 | 12,11,92, 726 | 44.16 % |

| Total | 13,72,19, 448 | 27,44,38, 896 | 100% |

Note: The pre and post Scheme shareholding is indicative and based on the current shareholding as on date. However, it is subject to change based on the shareholding as on the Record Date (as defined in the Scheme).

RML/Resulting Company:

Pre scheme shareholding pattern of Resulting Company:

| Category | No. of equity shares of INR 2 each | Paid up share capital in INR | % of equity shares |

| Promoter and Promoter group | 50,000* | 1,00,000 | 100% |

| Public | – | – | – |

| Total | 50,000 | 1,00,000 | 100% |

*including 6 (six) equity shares held by the Demerged Company through its nominee holders

Post scheme shareholding pattern of Resulting Company:

| Category | No. of equity shares of INR 2 each | Paid up share capital in INR | % of equity shares |

| Promoter and Promoter group | 7,66,23,0 85 | 15,32,46, 170 | 55.84% |

| Public | 6,05,96,3 63 | 12,11,92, 726 | 44.16 % |

| Total | 13,72,19, 448 | 27,44,38, 896 | 100% |

*The existing shareholding held by the Demerged Company in the Resulting Company will be cancelled pursuant to Clause 29 of the Scheme.

h. It is stated that there have been no changes in the shareholding patterns of (Transferor Company) RGML and RML (Resulting Company) from the date of filing of the Scheme up to the present date. For the Transferee/Demerged Company/RIL, a separate note of the shareholding pattern along with the changes therein post the time of filing of the scheme is provided in Annexure 6.

i. The applicable additional information, as prescribed in Annexure L of the stock exchange checklist in the application submitted to the NSE and BSE pursuant to Regulation 37 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, as advised by NSE and BSE in their observation letters dated 16.03.2026 conveying their no adverse observations/no-objection is provided at Annexure 7.

20. We have heard the Ld. Counsel for the Applicant and perused the documents placed on record.

21. This Tribunal is satisfied that the clarifications sought have been adequately addressed.

22. Taking into consideration the Application filed by the Transferee Company / Demerged Company and the documents filed therewith as well as the position of law, this Tribunal issues the following directions:

A. REFEX INDUSTRIES LIMITED

(Second Applicant Company / Transferee Company/ Demerged Company)

I. EQUITY SHAREHOLDERS

(i) There are 97,015 (Ninety-Seven Thousand and Fifteen) Equity Shareholders in the Applicant Company. The Certificate dated 17.03.2026 issued by the Chartered Accountant certifying the shareholding pattern of the Equity Shareholders as on 31.12.2025 is placed at Page No.201 of the application. It has sought for convening the meeting.

(ii) Since there are 97,015 (Ninety-Seven Thousand and Fifteen) Equity Shareholders for Transferee Company/ Demerged Company, it will be appropriate to convene, hold and conduct the meetings of the equity shareholders of the Transferee Company/ Demerged Company. The meeting is directed to be held on 05.08.2026 at 11.00 A.M. at the registered office of the Transferee Company/ Demerged Company or through video conferencing or at any other suitable place for which prior approval shall be sought from this Tribunal within a period of 7 days from the date of this order and prior to the issue of notices.

II. SECURED CREDITORS

(i) There are 8 (Eight) Secured Creditors. The Certificate dated 17.03.2026 issued by the Chartered Accountant certifying the list of secured creditors as on 31.12.2025 is placed at Page No.202 of the application. It has sought for convening the meeting.

(iii) Since there are 8 (Eight) Secured Creditors for Transferee company, it will be appropriate to convene, hold and conduct the meetings of the secured creditors of the Transferee Company. The meeting is directed to be held on 08.2026 at 11.30 A.M. at the registered office of the Transferee Company or through video conferencing or at any other suitable place for which prior approval shall be sought from this Tribunal within a period of 7 days from the date of this order and prior to the issue of notices.

III. UNSECURED CREDITORS

(i) There are 388 (Three Hundred and Eighty-Eight) Unsecured Creditors of the Transferee Company. The Certificate dated 17.03.2026 issued as on 31.12.2025 by the Chartered Accountant certifying the list of Unsecured Creditor is placed at Page No. 203 of the application.

(ii) Since there are 388 (Three Hundred and Eighty-Eight) Unsecured Creditors for Transferee company, it will be appropriate to convene, hold and conduct the meetings of the unsecured creditors of the Transferee Company. The meeting is directed to be held on 05.08.2026 at 12.00 P.M. at the registered office of the Transferee Company or through video conferencing or at any other suitable place for which prior approval shall be sought from this Tribunal within a period of 7 days from the date of this order and prior to the issue of notices.

23. The quorum for the meeting of the Transferee company shall be as follows;

| S.No. | Class | Quorum | Date & Time of the Meeting |

| 1. | Equity Shareholders of Transferee Company/Second Applicant Company | 30 | 05.08.2026 at 11.00 A.M. |

| 2. | Secured Creditors of Transferee Company/Second Applicant Company | 3 | 05.08.2026 at 11.30 A.M. |

| 3. | Unsecured Creditors of Transferee Company/Second Applicant Company | 30 | 05.08.2026 at 12.00 P.M. |

i) The Chairperson appointed for the above said meetings shall be U.K. Sirohi, (Mob: 9873294066). The Fee of the Chairperson for the aforesaid meetings shall be Rs.1,50,000/- (Rupees One Lakh Fifty Thousand only) in addition to meetings his incidental expenses if any. The Chairperson(s) will file the reports of the meetings within a week from the date of holding of the above said meetings.

ii) Mr. Kishore P, (Mob: 9362959697), appointed as a Scrutinizer and would be entitled to a fee of Rs.75,000/- (Rupees Seventy-Five Thousand only) for services in addition to meeting incidental expenses if any.

iii) In case the quorum as noted above, for the above meeting of the Transferee Company/ Demerged Company is not present at the meeting, then the meeting shall be adjourned by half an hour, and thereafter the person(s) present and voting shall be deemed to constitute the quorum. For the purpose of computing the quorum the valid proxies shall also be considered, if the proxy in the prescribed form, duly signed by the person entitled to attend and vote at the meeting, is filed with the registered office of the applicant company at least 48 hours before the meeting. The Chairperson appointed herein along with Scrutinizer shall ensure that the proxy registers are properly maintained. However, every endeavour should be made by the Transferee company to attain at least the quorum fixed, if not more in relation to approval of the scheme.

iv) The meetings shall be conducted as per applicable procedure prescribed under the MCA Circular MCA General Circular Nos. (i)20/2020 dated 5th May, 2020 (AGM Circular), (ii) 14/2020, dated 08.04.2020 (EGM Circular-I) and (iii) 17/2020 dated 13.04.2020 (EGM Circular-II);

v) That individual notices of the above said meetings shall be sent by the Transferee Company/ Demerged Company through registered post or speed post or through courier or e-mail, 30 days in advance before the scheduled date of the meeting, indicating the day, date, the place and the time as aforesaid, together with a copy of Scheme, copy of explanatory statement, required to be sent under the Companies Act, 2013 and the prescribed form of proxy shall also be sent along and in addition to the above any other documents as may be prescribed under the Act or rules may also be duly sent with the notice.

vi) That the Transferee Company/ Demerged Company shall publish advertisement with a gap of at least 30 clear days before the aforesaid meetings, indicating the day, date and the place and time as aforesaid, to be published in the English Daily “The Indian Express” (All India Edition) & “Makkal Kural” (Tamil Nadu Edition) in Vernacular stating the copies of Scheme, the Explanatory Statement required to be furnished pursuant to Section 230 of the Companies Act, 2013 and the form of proxy shall be provided free of charge at the registered office of the respective Applicant Companies.

vii) The Chairperson shall as afore stated be responsible to report the result of the meeting within a period of 3 days of the conclusion of the meeting with details of voting on the proposed scheme.

viii) The company shall individually send notice to concerned Regional Director, MCA, Registrar of Companies, Official Liquidator and the Income Tax Authorities as well as other sectoral regulators who may have significant bearing on the operation of the applicant companies or the Scheme per se along with copy of required documents and disclosures required under the provisions of Companies Act, 2013 read with Companies (Compromises, Arrangements, Amalgamations) Rules, 2016.

ix) The Applicant Company shall further furnish a copy of the Scheme free of charge within 1 day of any requisition for the Scheme made by every creditor or member of the applicant companies entitled to attend the meetings as aforesaid.

x) The Authorized Representative of the Applicant Company shall furnish an affidavit of service of notice of meetings and publication of advertisement and compliance of all directions contained herein at least a week before the proposed meetings.

xi) All the aforesaid directions are to be complied with strictly in accordance with the applicable law including forms and formats contained in the Companies (Compromises, Arrangements, Amalgamations) Rules, 2016 as well as the provisions of the Companies Act, 2013 by the Applicants.

24. This Application stands allowed on the aforesaid terms.

Author Bio