Case Law Details

Assam Logistics Vs ITO (ITAT Delhi)

The Income Tax Appellate Tribunal Delhi allowed the appeal filed against the order of the Commissioner of Income Tax (Appeals), NFAC, concerning additions made in the hands of a dissolved partnership firm for Assessment Year 2017-18. The dispute arose after the Assessing Officer reopened the assessment under Sections 147 and 144 of the Income Tax Act on the basis that contractual receipts of ₹18.37 crore from Maruti Suzuki Ltd., along with interest income of ₹75,723, were reflected in the PAN of the erstwhile partnership firm and no return of income had been filed.

The assessee contended that the partnership firm had already been dissolved with effect from 28.04.2015 through a dissolution deed. Under the deed, three partners retired, while the surviving partner, Shri Raja Singh, continued the transportation business under the same trade name, “Assam Logistic,” as a proprietorship concern. According to the assessee, the receipts from Maruti Suzuki India Ltd. were actually received and accounted for in the books of the proprietorship concern operated by Shri Raja Singh. It was further submitted that the receipts were credited into the proprietorship firm’s HDFC Bank account and duly reflected in its financial statements.

The Assessing Officer observed that the proprietorship concern had disclosed turnover of ₹4.28 crore in its Profit and Loss Account and therefore concluded that the contractual receipts of ₹18.37 crore remained taxable in the hands of the erstwhile partnership firm. Applying a profit rate of 8%, the Assessing Officer made an addition of ₹1.47 crore and also added the interest income. On appeal, the Commissioner (Appeals) upheld the additions substantially, though the profit rate was reduced from 8% to 5.76%, resulting in confirmation of an addition of ₹1.05 crore.

Before the Tribunal, the assessee reiterated that the dissolved partnership firm was not in existence during the relevant assessment year and therefore could not be taxed on the receipts. The assessee produced the dissolution deed, bank statements, audit reports, and financial statements of Shri Raja Singh’s proprietorship concern. It was explained that the gross receipts of ₹37.97 crore, including freight receipts of ₹16.61 crore and ₹21.35 crore, were recorded in the books of the proprietorship concern. After deducting freight expenses of ₹33.68 crore, the balance amount of ₹4.28 crore was disclosed as net turnover in the Profit and Loss Account. The assessee also stated that this method of presenting net turnover had been consistently followed in earlier years.

The Tribunal noted that the surviving partner had demonstrated that the receipts from Maruti Suzuki India Ltd. formed part of the gross receipts already declared and taxed in his proprietorship concern. The Tribunal also took note of an affidavit filed by Shri Raja Singh confirming that the entries appearing in Form 26AS of the dissolved partnership firm actually related to his proprietorship concern and had been included in its gross turnover. The affidavit remained uncontroverted.

The Tribunal observed that the sole basis for taxing the receipts in the hands of the dissolved firm was a communication received from Maruti Suzuki Ltd. However, the Tribunal found that the company had merely stated that payments were made to “Assam Logistics” and had not denied that the payments related to the proprietorship concern. According to the Tribunal, because the dissolution of the partnership firm had not been updated in the records of Maruti Suzuki Ltd., the payments and corresponding TDS under Section 194C continued to be reflected against the PAN of the erstwhile partnership firm. The assessee had also placed on record emails sent to Maruti Suzuki Ltd. requesting correction of the TDS records.

After considering the material, the Tribunal held that no addition could be made in the hands of a partnership firm that had already been dissolved in the preceding year when the receipts had already been offered to tax by the surviving partner in his proprietorship business operating under the same name and style. The Tribunal held that making another addition in the hands of the dissolved firm would amount to double taxation of the same income, which was not permissible.

Accordingly, the Tribunal directed deletion of the addition of ₹1.05 crore sustained by the Commissioner (Appeals) and allowed the appeal of the assessee.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal is filed by the Assessee against the order of Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi [CIT(A) in short], dated 29.05.2025 in Appeal No. NFAC/2016-17/10259264 arising out of the order passed u/s 147 r.w.s. 144 of the Income Tax Act, 1961 (the Act, in short) dated 17.05.2023 for Assessment Year 2017-18.

2. Brief facts of the case are that assessee is a partnership firm having four partners and as per the claim of the assessee, it stood dissolved with effect from 28.04.2015 in terms of the dissolution deed executed on the said date, according to which three partners namely Shri Taranjeet Kaur, Shri Deepak Kumar and Harinder Singh got retired and running business of the partnership firm was taken over by the surviving partner namely Sh. Raja Singh and continued the business under the same name and style i.e. Assam Logistic under his proprietorship. The AO has information that during the year under appeal, the erstwhile partnership firm i.e. the appellant had received contractual receipts of Rs.18,37,94,110/- from Maruti Suzuki Ltd. on which TDS u/s 194C was deducted. Besides this interest of Rs.75,723/- was also credited subject to TDS u/s 194A and since no return of income was filed by the assessee firm, the case was reopened by issue of notice u/s 148 on 22.07.2022 after concluding the proceedings u/s 148A of the Act. In response, assessee claimed that the said receipts were duly recorded in the books of accounts of the proprietorship firm run by surviving partner Sh. Raja Singh and since principle i.e. M/s Maruti Suzuki India had made correction in its records to give effect of the dissolution of the partnership firm, inadvertently TDS was deducted and deposited in the PAN of the erstwhile partnership firm. The AO observed that the proprietorship firm of the assessee has declared total turnover of Rs.4,28,39,469.45 in the Profit and Loss Account and therefore, the amount received from M/s Maruti Suzuki India of Rs.18,37,94,110/- remained to be taxed in the hands of the assessee firm and, accordingly, by applying profit rate of 8% on such receipts, an addition of Rs.1,47,03,528/- was made by the AO. The addition on account of interest was also made.

3. Against the said order, assessee preferred an appeal before the Ld. CIT(A) wherein the same facts were submitted, however, Ld. CIT(A) confirmed the findings of the AO and rejected the contentions raised by the assessee and reduced the profit rate from 8% to 5.76% which has resulted into the confirmation of addition of Rs.1,05,86,540/- as against addition of Rs.1,47,03,528/- made by the AO. Further the addition on account of interest income was also confirmed.

4. Aggrieved by the said order, assessee is in appeal before the Tribunal in the present appeal.

5. All the grounds of appeal taken by the assessee are with respect to the confirmation of the addition made by the AO by alleging that turnover of Rs.18,37,94,110/- is related to the assessee company.

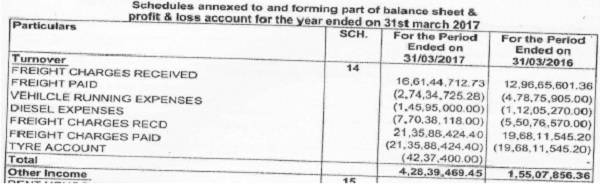

6. Heard both the parties at length and perused the material available on record. The claim of the assessee was that the assessee firm stood dissolved in terms of the dissolution deed made and executed on 28.04.2015, placed at PB page 100 to 104. As per the same, three partners namely Smt. Taranjeet Kaur, Shri Deepak Kumar and Shri Harinder Singh were retired from the firm with immediate effect and the surviving partner namely Shri Raja Singh having PAN AONPS1502G continued the running business of partnership firm in the same name and style and continued its main business of transportation of vehicles manufacture by M/s Maruti Suzuki India in his proprietorship firm. Assessee further claimed that all the receipts from M/s Maruti Suzuki India Ltd. were duly credited in the bank account with HDFC Bank Account No. 50200012485111 which is the account of the proprietorship firm of Shri Raja Singh and a copy of bank statement is placed at pages 107 to 123 of PB. Assessee further claimed that all the receipts are duly recorded in the books of accounts of the Sh. Raja Singh. In support of the claim, audit financial statements of Sh. Raja Singh were also filed wherein as per the P&L Account, net turnover was shown of Rs.4,28,39,469/- and details of the same was disclosed in Schedule -14 attached to the Balance Sheet, placed at page 247 of the PB. From the perusal of which the breakup of gross turnover is as under:

Assessee claimed that in Schedule-14, freight charges of Rs.16,61,44,712/- and Rs. 21,35,88,424/- were declared, thus gross receipts declared were of Rs. 37,97,33,136/- as recorded in the books of account and after reducing the freight charges paid at Rs. 33,68,93,667/-, balance amount of Rs.4,28,39,469/- was carried over to the P&L Account as net turnover. As per the assessee the practice of disclosing the net turnover in the Profit & Loss account was consistently followed by him as could be evident from the figures of immediately preceding year appearing. The AO has failed to appreciate this fact and wrongly observed that Sh. Raja Singh has declared contract receipts of only Rs. 4,28,39,469/- and, thus treated the receipts of Rs.18,37,94,110/- as income of the erstwhile partnership which stood dissolved in preceding assessment years and was not in existence for even a single day during the Assessment Year under appeal.

7. After considering these facts, in our considered opinion, action of the lower authorities in holding the receipts from M/s Maruti Suzuki Ltd as income of the erstwhile partnership firm is not correct, more particularly when surviving partner Shri Raja Singh has been able to demonstrate that these receipts are forming part of the gross receipts declared by him and due tax were paid after claiming expenditure on account of freight charges paid. This facts have not been properly appreciated by the lower authorities and the affidavit confirming these effect filed by Shri Raja Singh, placed at PB pages 209-210 remained uncontroverted, wherein Shri Raja Singh has accepted that the entries appearing in 26AS statement of the erstwhile partnership firm i.e. the appellant before us, actually related to his proprietary firm and included in his gross turnover. Sole basis for treating the said receipts as income of erstwhile partnership is the letter received from M/s Maruti Suzuki which is reproduced by the Ld. CIT(A) in its order however, from the perusal of the same, it is observed that nowhere in the reply filed by M/s Maruti Suzuki Ltd., it had denied making the payment to the firm M/s Assam Logistic Ltd. and simply stated that it had made payments to Assam Logistics. Since the effect of dissolution of partnership firm M/s Assam Logistics was not recorded by the company M/s Maruti Suzuki Ltd, it had recorded the payments and corresponding TDS on the PAN of erstwhile partnership firm with same name & style as was of the proprietorship firm of Shri Raja Singh. In the Paper Book, assessee also placed the copies of emails sent to M/s Maruti Suzuki Ltd for making necessary correction in TDS certificate issued which are available at PB pages 197 to 206.

8. In view of these facts, we are of the considered opinion that no addition could be made in the hands of the assessee firm which has already been dissolved in preceding year for the contract receipts from M/s Maruti Suzuki India which are offered for tax by the surviving partnership Sh. Raja Singh in his proprietorship under the same name & style as M/s Assam Logistics. Any further addition for the same receipts in the hands of the assessee firm tantamount to double taxation of an income which is not permitted. Thus we direct the AO to delete the addition of Rs.1,05,86,540/- uphold by ld. CIT(A) as income of the assessee firm. Accordingly, all the grounds of appeal raised by the assessee are allowed.

9. In the result, the appeal of the assessee is allowed.

Order pronounced in the open Court on 24.04.2026.

Author Bio