In recent times, a concerning trend has emerged across the banking sector where Chartered Accountants are increasingly being asked to issue various certificates that go far beyond their professional mandate. These include end-use of loan certificates, KYC confirmations, certifications for opening current accounts, utilisation of funds declarations, signing or validating financial statements, and even confirmations regarding borrower intent or future conduct. While these demands may appear procedural at first glance, they represent a systemic shift of responsibility from banks to professionals—without any clear legal backing.

At the heart of the issue lies a fundamental professional principle: a Chartered Accountant’s certification must always be grounded in facts, records, and verifiable evidence. It cannot be based on assumptions, intentions, or future conduct. A Chartered Accountant can verify past transactions, examine books of accounts, and rely on documentary evidence, but cannot certify how funds will be used in the future or guarantee the behaviour of a borrower.

The concept of end-use certification, as currently demanded by banks, is therefore fundamentally flawed. Banks are increasingly requiring CAs to confirm that loan funds “will be used” for specific purposes such as working capital or business expansion. However, future utilisation is inherently uncertain and depends entirely on the borrower’s actions. No audit procedure or professional standard allows a Chartered Accountant to validate such future events. What is being sought, therefore, is not certification of fact, but certification of intent—something that falls completely outside the professional domain.

The issue does not stop at end-use certification. Banks are now demanding a wide range of additional certificates such as KYC certification by CAs, despite KYC being a statutory obligation of the bank itself. Similarly, certificates are sought for opening current accounts, confirming business activities beyond available documents, and even certifying financial statements that are not subject to audit. In some cases, CAs are asked to confirm that funds will not be used for illegal or speculative purposes—again requiring them to certify behavioural outcomes rather than verifiable facts. Such practices are clearly not in conformity with ICAI guidelines, which mandate that certifications must be evidence-based and within the scope of professional competence.

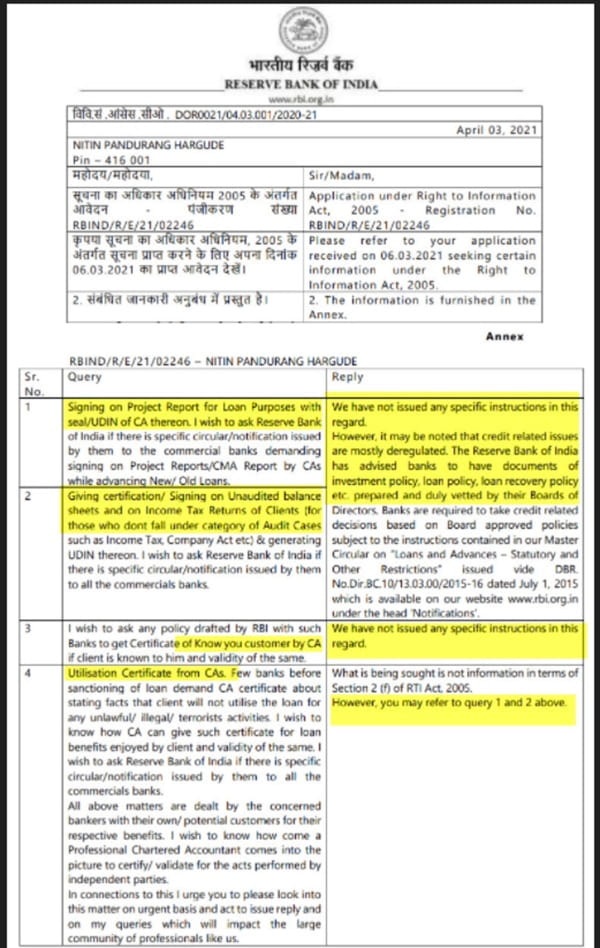

Recognising the widespread confusion and professional discomfort surrounding this issue, CA Nitin Pandurang Hargude sought clarity through a Right to Information (RTI) application filed with the Reserve Bank of India. The queries raised included whether RBI had issued any circulars or instructions requiring banks to obtain such certificates from Chartered Accountants, particularly in relation to project reports, CMA reports, unaudited financial statements, KYC certification, and utilisation certificates.

In its reply dated 03 April 2021, the Reserve Bank of India categorically stated that it has not issued any specific instructions in this regard. The RBI further clarified that credit-related matters are largely deregulated and are handled by banks based on their own internal policies, subject to broad regulatory frameworks. Even with respect to utilisation certificates, the RBI confirmed that no specific instructions have been issued. This response is crucial, as it establishes that there is no regulatory mandate requiring such certifications from Chartered Accountants.

The implication of this RTI response is significant. It clearly demonstrates that these certificates are being demanded by banks without any statutory requirement or regulatory backing. Instead, they appear to be driven by internal practices, convenience, or an attempt to shift responsibility onto professionals. This raises serious concerns about the legality and appropriateness of such demands.

In practical experience as well, when approached by a private bank for issuing such a certificate, a request was made to provide the internal regulation or circular that mandated such certification. The bank was unable to furnish any such document. This further reinforces the conclusion that these requirements are often imposed without any formal authority or documented policy, making them arbitrary in nature.

A typical example of such demand is the “End Use Declaration Certificate,” wherein the borrower declares the purpose of the loan and the Chartered Accountant is required to sign alongside. The format usually includes statements confirming that the loan will be used for working capital, business expansion, or debt consolidation, and that it will not be used for speculative purposes. However, the inclusion of the Chartered Accountant’s signature in such a document creates an implied assurance that goes beyond mere attestation and effectively places the CA in a position of validating the borrower’s future conduct.

This blending of borrower declaration with CA certification is inherently problematic. It blurs the distinction between a self-declaration by the borrower and an independent professional certification. It lacks any mention of the basis of verification, does not define the scope of the CA’s responsibility, and fails to include necessary disclaimers or limitations. In effect, it exposes the Chartered Accountant to undue legal and professional risk.

If, at a later stage, the borrower diverts funds or violates the stated purpose, the CA may be unnecessarily drawn into litigation or regulatory scrutiny. From a disciplinary perspective as well, issuing certificates without adequate basis may amount to professional misconduct under ICAI regulations. Even where no wrongdoing is established, the reputational impact of such associations can be significant.

This practice is therefore not only conceptually flawed but also professionally unsustainable. Banks, instead of strengthening their internal credit appraisal and monitoring systems, appear to be outsourcing a part of their responsibility to Chartered Accountants. This is neither legally justified nor aligned with sound governance principles.

The correct approach is straightforward. If banks require assurance regarding the end-use of funds, they should obtain clear and unambiguous undertakings directly from the borrower, supported by affidavits where necessary. The responsibility of monitoring utilisation should remain with the bank through its internal mechanisms. The role of the Chartered Accountant should be limited strictly to certifying historical data and verifying records where appropriate.

Chartered Accountants, on their part, must exercise professional caution and avoid issuing certificates that require them to certify future events, intentions, or actions beyond their control. Wherever any certification is issued, it must be supported by documentary evidence, clearly define the scope, and include appropriate disclaimers. Blindly complying with such requests not only undermines professional standards but also exposes the CA to avoidable risk.

In conclusion, the increasing demand for end-use certificates and similar declarations from Chartered Accountants is a practice that lacks legal sanction, contradicts professional principles, and creates unnecessary exposure. The RBI has itself clarified that no such guidelines exist. It is therefore imperative for both banks and professionals to align their practices with regulatory intent and professional ethics.

Members of the profession are strongly advised to carefully review the RTI response obtained by CA Nitin Pandurang Hargude and refrain from issuing certificates that are not in conformity with ICAI standards. Professional integrity lies not in agreeing to every request, but in drawing a clear boundary between verification and assumption.

Frequently Asked Questions (FAQs)

Q.1. Can a Chartered Accountant certify the future end-use of a bank loan?

Ans. No. A Chartered Accountant can certify only facts supported by books of account, records, and verifiable documentary evidence. Certifying how a borrower will use loan funds in the future involves validating future intentions or conduct, which falls outside the professional scope of a CA.

Q.2. Has the Reserve Bank of India (RBI) mandated banks to obtain end-use certificates or similar certificates from Chartered Accountants?

Ans. No. As per the RBI’s RTI reply dated 03 April 2021, the RBI has clarified that it has not issued any specific instructions requiring banks to obtain certificates from Chartered Accountants for project reports, CMA reports, unaudited financial statements, KYC certification, or utilisation certificates. Such requirements are generally based on individual banks’ internal policies.

Q.3. Why are end-use declaration certificates considered professionally risky for Chartered Accountants?

Ans. Such certificates often require a Chartered Accountant to certify future utilisation of funds or borrower conduct without any verifiable basis. This may expose the CA to legal disputes, regulatory scrutiny, and disciplinary proceedings if the borrower subsequently misuses the funds or violates the stated purpose.

Q.4. What is the appropriate role of a Chartered Accountant in bank certification matters?

Ans. A Chartered Accountant’s role should be limited to verifying historical financial information, examining records, and certifying matters that can be substantiated through documentary evidence. Any certification issued should clearly define its scope, specify the basis of verification, and contain appropriate disclaimers where necessary.

Q.5. What should banks do instead of seeking future end-use certificates from Chartered Accountants?

Ans. Banks should obtain clear declarations or undertakings directly from borrowers, supported by affidavits wherever appropriate, and monitor the utilisation of loan funds through their own internal credit appraisal and monitoring mechanisms rather than shifting this responsibility to Chartered Accountants.

Author Bio