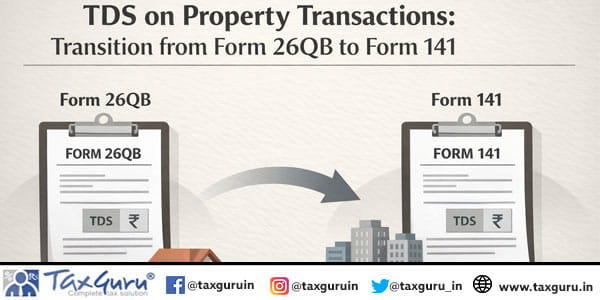

TDS reporting for property transactions is evolving with the transition from Form 26QB to Form 141. Meeting TDS requirements on immovable property purchases under Section 194-IA is often difficult, especially in transactions with multiple buyers and sellers, where many Forms 26QB must be filed, raising the risk of reporting mistakes.

Incorrect reporting of property value, the buyer’s share of consideration (the agreed payment amount for the property), or stamp duty value (the value estimated by authorities for stamp duty) often led to mismatches between tax records and the notices issued to buyers.

To address these practical difficulties, the Income-tax Act, 2025, introduced Form 141, which consolidates multiple TDS reporting requirements into a single filing system.

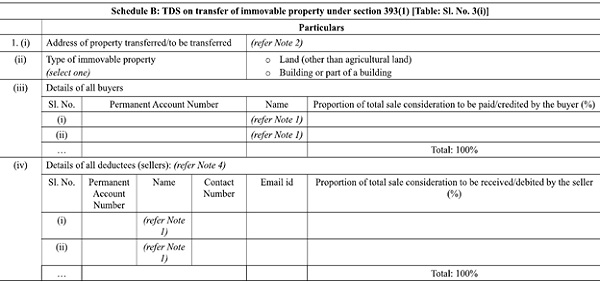

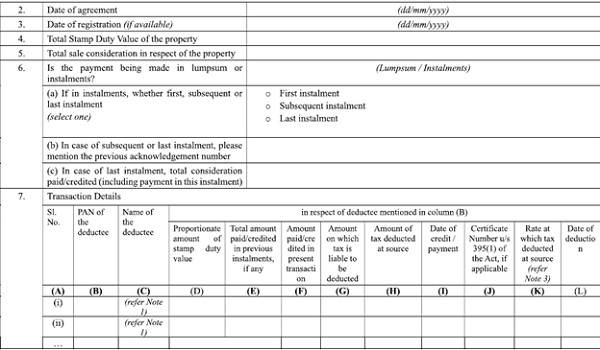

The form is divided into four schedules (A-D), each covering different categories of TDS reporting. Schedule B of Form 141 specifically relates to TDS on the purchase of immovable property, which was previously reported through Form 26QB.

The newly introduced Form 141 is expected to enhance clarity in reporting property transactions, especially those involving multiple buyers and sellers, thereby making the compliance process more transparent and organized.

A draft extract of Schedule B of Form 141 is displayed below to illustrate this transition.

–

Before examining issues with Form 26QB and how Form 141 addresses them, it is helpful to briefly review the legal provisions governing TDS on property transactions. This legal context sets the foundation for understanding the practical challenges discussed next.

Legal Framework Section 194-IA of the Income-tax Act, 1961 (corresponding to Section 393 of the Income-tax Act, 2025) states that any person responsible for paying consideration for the transfer of immovable property (excluding agricultural land) must deduct TDS at a rate of 1% if the consideration exceeds ₹50 lakhs.

TDS is deposited with the Central Government via Form 26QB, which will be replaced by Form 141 from 1 April 2026. Payment is due within 30 days of deduction.

Key TDS Compliance Points: Property buyers should note the following essential TDS requirements:

(a) Threshold for Joint Purchases: TDS applies if the total property value exceeds ₹50 lakhs, regardless of each buyer’s share.

(b) TDS must be deducted if the total consideration for the property is ₹50 lakhs or more.

(c ) Include incidental charges such as membership fees, parking, utilities, and maintenance when calculating consideration for transfer.

(d) Each buyer is required to deduct and deposit TDS and file the prescribed form even if the purchase is financed through a loan. (A housing loan is a loan taken from a bank or lender to buy property.)

(e ) Exclude GST from the consideration amount when determining TDS.

(f) TDS should be deducted in accordance with the ownership share specified in the agreement and not based on the source of payment. Ensure ownership ratios are defined in all sale documents.

Practical Challenges under Form 26QB and the Improvements Introduced by Form 141: While the legal provisions appear straightforward, taxpayers often face several practical difficulties while reporting TDS through Form 26QB. Some common issues and the improvements introduced through Form 141 are discussed below, providing important context for the new requirements.

Practical Issue 1: Incorrect Reporting of “Amount Paid/Credited” One of the most common mistakes in filing Form 26QB relates to the incorrect reporting of the “Amount Paid/Credited” field.

Illustration: Mr Ajay and his wife jointly purchased a flat for ₹80 lakhs. After the final payment, the seller delayed handing over possession, citing discrepancies in tax records. The seller noticed the property transaction appeared nearly double in his Form 26AS, leading to the refusal of possession.

Upon investigation, it was discovered that, while filing Form 26QB, both buyers reported the amount paid/credited as ₹80 lakhs each, rather than their respective shares. As a result, the seller’s tax records reflected a transaction value of ₹1.6 crore rather than the actual ₹80 lakhs.

Form 141 addresses this confusion by separating the reporting of total property value from each buyer’s share. Sl. No. 5 requires total sale consideration disclosure, while Sl. No. 1(iii) reports each buyer’s proportion and PAN, helping accurately reflect the total transaction value.

Practical Issue 2: Payment by One Buyer but Ownership by Two. In many cases, the entire payment for the property may be made from a single buyer’s bank account, or the housing loan EMI may be serviced by a single co-buyer. This often leads to confusion regarding TDS compliance.

Illustration: Mr Bijoy and his wife jointly purchased a property for ₹75 lakhs using a housing loan. Mr Bijoy paid the entire EMI and deducted TDS only in his name. Afterwards, he received a notice since two buyers were named in the agreement. Both were required to deduct TDS and file separate forms, emphasizing that TDS is based on ownership, not payment source.

The Schedule B format in Form 141 captures each buyer’s details and share, aligning reporting with the ownership reflected in the agreement. This reinforces that TDS compliance follows ownership, not payment source.

Practical Issue 3: Multiple Buyer–Seller Combinations: Another frequently overlooked requirement concerns transactions involving multiple buyers and sellers.

Illustration: Mr Ramesh bought a property from two joint sellers. He deducted 1% TDS on the total amount and filed a single Form 26QB, only to later learn that separate filings were required for each buyer–seller combination, whereas Form 141 allows a single filing for multiple sellers.

Correction of Errors in Form 26QB or Form 141. If incorrect details are reported in Form 26QB or Form 141, such as errors in PAN (Permanent Account Number), consideration amount, or property value, the mistakes can be rectified by submitting a correction request through the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal.

The buyer (deductor) can access the TRACES portal either by logging in directly or through internet banking and submit a correction request to rectify the relevant details.

Timely correction ensures proper TDS credit in the seller’s tax records, helping avoid disputes and compliance problems.

Conclusion: Property buyers often focus on financing, documentation, and possession, while TDS compliance is often overlooked. Errors in TDS reporting through Form 26QB can lead to mismatches in tax records, departmental notices, and complications for both parties.

With the introduction of Form 141, effective for transactions from 1 April 2026 onwards, the TDS reporting framework for property transactions is expected to become more structured and transparent.

A clear understanding of the reporting requirements under Schedule B of Form 141 will therefore play an important role in ensuring smooth and error-free compliance. Staying informed and proactive about these changes will help taxpayers manage TDS obligations efficiently as the new era of property transaction reporting unfolds.

FAQs on TDS Reporting for Property Transactions under Form 141

Q.1 What is Form 141 and how does it differ from Form 26QB?

Ans. Form 141 is the new TDS reporting form introduced under the Income-tax Act, 2025 to replace Form 26QB with effect from 1 April 2026. Schedule B of Form 141 specifically deals with TDS on the purchase of immovable property and is designed to simplify reporting, particularly in transactions involving multiple buyers and sellers.

Q.2 When is TDS required to be deducted on the purchase of immovable property?

Ans. Under Section 393 of the Income-tax Act, 2025 (corresponding to Section 194-IA of the Income-tax Act, 1961), the buyer must deduct TDS at 1% where the consideration for the transfer of immovable property (other than agricultural land) is ₹50 lakh or more. The threshold applies to the total value of the property, even in joint purchase transactions.

Q.3 How does Form 141 simplify reporting in transactions involving multiple buyers or sellers?

Ans. Unlike Form 26QB, which generally required separate filings for each buyer-seller combination, Form 141 enables consolidated reporting by separately capturing the total sale consideration and each buyer’s ownership share and PAN, thereby reducing duplication and minimizing reporting errors.

Q.4 Is TDS compliance based on the source of payment or ownership of the property?

Ans. TDS compliance is based on the ownership share specified in the sale agreement, not on who actually makes the payment or repays the housing loan. Each buyer is required to deduct and deposit TDS according to their ownership share, irrespective of the source of funds.

Q.5 Can mistakes made while filing Form 26QB or Form 141 be corrected?

Ans. Yes. Errors relating to details such as PAN, property value, or consideration amount can be corrected by submitting a orrection request through the TRACES portal. Timely correction helps ensure that the seller receives the correct TDS credit and reduces the likelihood of tax notices or compliance issues.

*****

Disclaimer: The article is intended for educational purposes only.

The author can be approached at [email protected]

What in case here if seller is a private ltd company. Will the Heading wll be corproration tax 0020 instead of 0021?

(f) TDS should be deducted in accordance with the ownership share specified in the agreement and not based on the source of payment. Ensure ownership ratios are defined in all sale documents…. Never seen any agreement or document where ownership ratio is provided. Practically ITD considers the proprotion of the payment by each owners to decide the ownership ratio and of course also how the treatment in the personal ITRs is given in resepctive owners. So source of payment is the criteria currently observed by the iTD…my personal views..