Month: January 2026

2,391 articlesIncome Tax

Income Tax

Cash Advance Adjusted Through Tripartite Deal Not Unexplained Cash Credit U/s 68

Income Tax

Income Tax

Final Assessment Ignoring DRP Directions Held Void; No Post-Limitation Cure Permissible

Income Tax

Income Tax

Section 153C Assessments Beyond Ten-Year Block Invalid: Deemed Search Date Starts from Satisfaction Note

Income Tax

Income Tax

Investor Funds of Company Cannot Be Taxed as Director’s Personal Unexplained Money u/s 69A

Corporate Law

Corporate Law

₹18,000 Monthly Limit Set to Define Supervisory Employees as Workers

Custom Duty

Custom Duty

Once DGFT Issues EODC, Customs Cannot Deny Advance Authorization Benefits: CESTAT Chennai

Corporate Law

Corporate Law

If Liquidation Is Final, CIRP Must Work: Lessons from 2025 IBBI Amendment

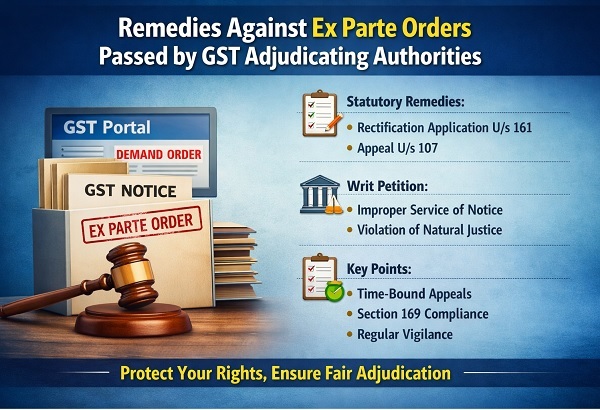

Goods and Services Tax

Goods and Services Tax

GST Overhaul for Sin Goods from Feb 2026: MRP Valuation Takes Over

Goods and Services Tax

Goods and Services Tax

जनवरी 2026 से RCM ITC पर नया GST वैलिडेशन नियम

Goods and Services Tax

Goods and Services Tax