Month: January 2026

2,391 articlesGoods and Services Tax

Goods and Services Tax

No Profiteering as Post-GST ITC Ratio Fell Below Pre-GST Level: GSTAT

Custom Duty

Custom Duty

CAAR Mumbai Rejected Advance Ruling Due to Pending Custom Classification Dispute

Income Tax

Income Tax

Unsecured Loans Through Banking Channels Accepted; Section 68 Addition of ₹2.87 Cr Deleted

Goods and Services Tax

Goods and Services Tax

GST First Appeal – Practical Insights

Income Tax

Income Tax

ITAT Delhi Quashed Reassessment for Invalid Sanction Beyond Three Years

Finance

Finance

Trump’s Board of Peace and “Parallel UN” Proposal

Company Law

Company Law

Penalty Levied for Failure to Attach Valuation Report in Securities Allotment

Income Tax

Income Tax

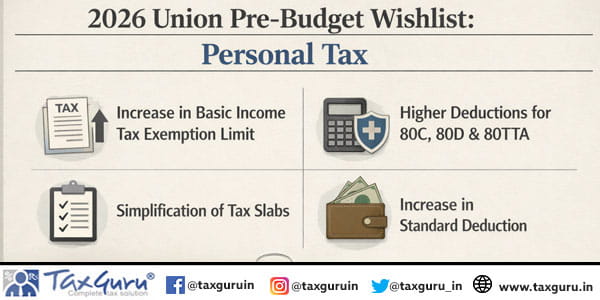

2026 Union Pre-Budget Wishlist: Personal Tax

Goods and Services Tax

Goods and Services Tax

GST: SC Rulings Apply Retrospectively Unless Stated Otherwise: Calcutta HC

Income Tax

Income Tax