#NAA

Log in to FollowEvery article filed under the “NAA” tag — analysis, news and updates.

454 articlesGoods and Services Tax

Goods and Services Tax

Anti-profiteering provisions not attracted if no GST tax rate reduction

Goods and Services Tax

Goods and Services Tax

No profiteering if no decrease in Tax Rate & no increase in profit Margin

Goods and Services Tax

Goods and Services Tax

Non reduction of Chocolate price after GST Rate reduction is Profiteering: NAA

Goods and Services Tax

Goods and Services Tax

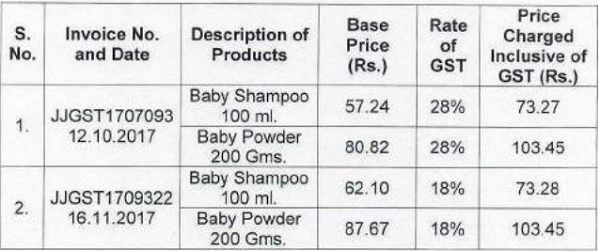

Johnson Product dealer guilty of profiteering for not reducing price despite Tax Reduction: NAA

Goods and Services Tax

Goods and Services Tax

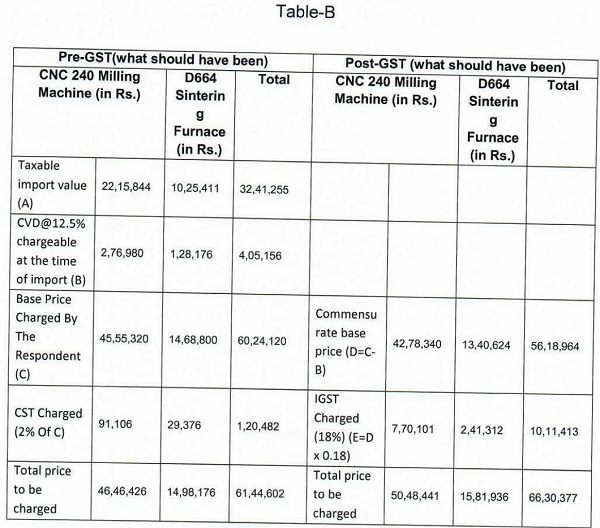

Anti profiteering established as ITC of erstwhile CVD not passed

Goods and Services Tax

Goods and Services Tax

Increase in base price by McDonald to deny benefit of Tax reduction is profiteering: NAA

Goods and Services Tax

Goods and Services Tax

No profiteering if reduction in base price is more than additional eligible ITC

Goods and Services Tax

Goods and Services Tax

Anti Profiteering Upheld In Noodles Case

Goods and Services Tax

Goods and Services Tax

No action can be taken if no specific evidence of profiteering: NAA

Goods and Services Tax

Goods and Services Tax