Service Tax is levied under Section 66B[1] of the Finance Act, 1994 as amended up to date. Section 68(1)[2] confers liability to pay service tax on service provider but section 68(2)[3], which has overriding effect over section 68(1), confers liability to pay service tax on the receiver of such taxable service as notified by Central Government.

Service Tax is levied under Section 66B[1] of the Finance Act, 1994 as amended up to date. Section 68(1)[2] confers liability to pay service tax on service provider but section 68(2)[3], which has overriding effect over section 68(1), confers liability to pay service tax on the receiver of such taxable service as notified by Central Government.

The reverse charge mechanism (RCM) was first introduced effectively from 01-01-2005 vide Notification No. 36/2004-ST dt. 31-12-2004 read with Rule 2(1)(d) of Service Tax Rules, 1994. With effect from 01-07-1012 a new mechanism of reverse charge (RCM) and partial reverse charge or joint charge (PRCM / JCM) was introduced with the introduction of negative list regime of service tax.

Some fundamental concepts of reverse/partial charge mechanism are;

1. Applicability of RCM/PRCM is dependent on the status & location of Service Receiver (SR) and Service Provider (SP) and taxability of service. RCM does not apply on non-taxable and exempted services but applies on abated services and where value is determined by valuation rules.

2. No threshold exemption of Rs. 10 lacs is available to Service Receiver (SR) as this exemption is available to Service Providers only. (refer NN 33/2012-St dt. 20-06-2012)

3. Service Receiver is liable to pay service tax under this mechanism from very first invoice received under this category. It means SR is liable to pay ST even when SP is within the ambit exemption limit under NN 33/2012-ST.

4. This service tax liability has to be met in cash i.e. no Cenvat Credit facility is available to meet out this liability as Cenvat Credit facility is available for output services only while it will be input service for SR. Rule 2(p) of Cenvat Credit Rules, 2004 (as amended by NN 28/2012-CE (NT) dt. 20-06-2012, the term output service means any service provided by SP located in taxable territory but shall not include a service;

(a) Specified in section 66D of the Finance Act, 1994, or

(b) Where whole of ST liability is of SR i.e recipient of service.

As a result, who is engaged in providing taxable services falling under full RCM, will not be able to take Cenvat Credit of ED & ST in respect of ‘input’/’capital goods’ and ‘input services’ respectively.

5. Service Receiver is liable to discharge service tax liability under Rule 7 of Point of Taxation Rules, 2011 (NN 18/2011-ST as amended by NN 25/2011-ST, NN 41/2011-ST, NN 4/2012-ST and NN 37/2012-ST)

6. In case of Service Providers (SP) rendering the services all of which falls within the ambit of complete reverse charge mechanism; he cannot avail Cenvat credit of input or input services.

But, Service Receiver (SR) who is paying service tax under RCM can avail Cenvat credit as per Rule 4(7) of CCR, 2004 for any output service [refer Rule 3(4)(e) of CCR, 2004] on the basis of challan evidencing payment of ST [refer Rule 9(1)(e) inserted by NN 18/2012-CE (NT)].

7. The golden rule of Cenvat is that SP cannot claim refund of Cenvat if he is not able to utilise Cenvat credit against its output ST liability. There are two exception to this rule;

(a) Export of service (Rule 5A of CCR, 2004)

(b) A service provider also discharging ST liability under section 68(2), is unable to utilise such Cenvat credit against his ST liability on output services, refund is admissible as per Rule 5B of CCR, 2004 as amended by NN 28/2012-CE (NT) dt 20-06-2012[4] but CBEC has not notified its claiming procedure so far so practically it can’t be claimed till date. It is pertinent to mention here that Rule 5B does not cover refund of Cenvat credit availed on capital goods.

Following services are covered under reverse charge/partial reverse charge mechanism under Rule 2(2)(d)(i) read with Notification No. 30/2012-ST as updated by NN 45/2012-ST, NN 46/2012-ST & NN 10/2014-ST:

1. Insurance Agent Service

1A. (Banking) Recovery Agent Service (w.e.f. 11-07-2014)

2. Goods Transport Agency Service

3. Sponsorship Service

4. Legal Service

5. Arbitral Tribunal Service

6. Services by Directors of the company body corporate to the company body corporate (w.e.f. 07-08-2012 11-07-2014)

7. Support Services provided by Government/Local Authority

8. Rent-a-Cab Service

9. Manpower Supply Service

10. Security Service (w.e.f 07-08-2012)

11. Service portion in execution of Works Contract

12. Import of Taxable Services

1. Analysis of Insurance Agent Service:

NN 30/2012-ST (as amended up to date)

| SL | NATURE OF SERVICE | PROVIDER | RECEIVED | |||

| Who? | How much? | Who? | How much? | Effective Rate | ||

| 1 | Insurance Agent Service | Any insurance agent (any person)located in the taxable territory | 0% | Any person carrying on insurance business i.e. insurance company located in the taxable territory | 100% | 12.36% |

Rule 2(1) [(d) of Service Tax Rules 1994: “person liable for paying service tax”, –

(i) in respect of the taxable services notified under sub-section (2) of section 68 of the Act, means,-

(A) in relation to service provided or agreed to be provided by an insurance agent to any person carrying on the insurance business, the recipient of the service;

(i). Exemption vide Clause number 29(g) of Mega-Exemption NN 25/2012-ST: Services by the following persons in respective capacities –

(g) business facilitator or a business correspondent to a banking company or an insurance company, in a rural area

(ii). As per rule 9 of Place of Provision of specified services, (w.e.f. 01-10-2014): The place of provision of following services shall be the location of the service provider;

………(c) Intermediary services; (as amended by NN 14/2012-ST dt 11-07-2014)

So it becomes non taxable service.

1A. Analysis of (Banking) Recovery Agent Service:

1A. Analysis of (Banking) Recovery Agent Service:

NN 30/2012-ST (as amended by NN 10/2014-ST Dated 11-07-2014)

| Sl. No. | Description of a service | Percentage of service tax payable by the person providing service | Percentage of service tax payable by the person receiving the service |

| 1A | in respect of services provided or agreed to be provided by a recovery agent to a banking company or a financial institution or a non-banking financial company[5] | Nil | 100% |

Rule 2(1) [(d) of Service Tax Rules 1994: “person liable for paying service tax”, –

(AA) in relation to service provided or agreed to be provided by a recovery agent to a banking company or a financial institution or a non-banking financial company, the recipient of the service;

2. Services provided by Goods Transport Agency (GTA):

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the person providing service | Percentage of ST payable by the person receiving the service | |

| By | to | ||||

| 2. | Goods Transport Agency (Applicable to transport by road) | Goods Transport Agents located in the taxable territory | Persons specified in Rule 2(1)(d)(i)(B) of Service Tax Rules, 1994located in the taxable territory | NILEffective Rate *(in case of abatement) 0% | 100%Effective Rate *(in case of abatement)3.09% |

Reverse Charge: if the person liable to pay freight falls within the category of persons specified under Rule 2(1)(d)(i)(B), reverse charge apply.

Under Rule 2(1)(d)(i)(B) if the person liable to pay freight is;

(I) any factory registered under or governed by the Factories Act, 1948 (63 of 1948);

(II) any ‘society’ registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India;

(III) any ‘co-operative society’ established by or under any law;

(IV) any ‘dealer of excisable goods’ who is registered under the Central Excise Act, 1944 (1 of 1944) or the rules made thereunder;

(V) any ‘body-corporate’ established, by or under any law; or

(VI) any ‘partnership firm’ whether registered or not under any law including association of persons;

any person who pays or is liable to pay freight either himself or through his agent for the transportation of such goods by road in a goods carriage is liable to pay service tax.

Provided that when such person is located in a non-taxable territory (i.e. in J&K or abroad), the provider of such service (i.e. GTA) shall be liable to pay service tax.

Non-applicability of reverse charge i.e. GTA is liable to pay service tax:

a. If consigner or consignee, who pays or is liable to pay freight either himself or through his agent, does not falls in above mentioned categories of specified,

b. If consigner or consignee, who pays or is liable to pay freight either himself or through his agent, is located in a non-taxable territory (i.e. in J&K or abroad), [refer Rule 2(1)(d)(B) of Service Tax Rules, 1994]

*Exemptions for GTA vide Clause 21 of NN 25/2012-ST: Services provided by a goods transport agency, by way of transport in a goods carriage of,-

(a) agricultural produce;

(b) goods, where gross amount charged for the transportation of goods on a consignment transported in a single carriage does not exceed one thousand five hundred rupees;

(c) goods, where gross amount charged for transportation of all such goods for a single consignee does not exceed rupees seven hundred fifty;

(d) foodstuff including flours, tea, coffee, jaggery, sugar, milk products, salt and edible oil, excluding alcoholic beverages;

(e) chemical fertilizer and oilcakes;[6]

(e) chemical fertilizer, organic manure and oil cakes;

(f) newspaper or magazines registered with the Registrar of Newspapers;

(g) relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishap; or

(h) defence or military equipments;”[7]

(i) cotton, ginned or baled.[8]

*75% Abatement for GTA Service vide NN 26/2012-ST:

| Sl. No. |

Description of taxable service |

Percent-Age Taxable | Conditions |

| (1) | (2) | (3) | (4) |

| 7 | Services of goods transport agency in relation to transportation of goods. | 25 | CENVAT credit on inputs, capital goods and input services, used for providing the taxable service, has not been taken by the service provider[1] under the provisions of the CENVAT Credit Rules, 2004. |

[1] Inserted by NN 8/2014-ST dt 11/07/2014

3. Analysis of Sponsorship Service:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the personproviding service | Percentage of ST payable by the personreceiving the service | |

| By | to | ||||

| 3. | Sponsorship Service | Any person located in the taxable territory | Body Corporate or Partnership Firm located in the taxable territory, | NIL | 100% |

Rule 2(1) [(d) of Service Tax Rules 1994: “person liable for paying service tax”, –

(C) in relation to service provided or agreed to be provided by way of sponsorship to anybody corporate or partnership firm located in the taxable territory, the recipient of such service

Note: When service provider is located in a non-taxable territory (i.e. in J&K or abroad), the receiver of such service shall be liable to pay service tax under reverse charge mechanism in all cases.

4. Analysis of Arbitral Tribunal Service:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the person providing service | Percentage of ST payable by the person receiving the service | |

| By | To | ||||

| 4. | Arbitral Tribunal Service | Arbitral Tribunal located in the taxable territory | Any business entity located in the taxable territory, | NIL | 100% |

Note: When service provider is located in a non-taxable territory (i.e. in J&K or abroad), the receiver of such service shall be liable to pay service tax under reverse charge mechanism in all cases.

I would also like to discuss mega exemption notification 25/2012-ST, entry no. 6(a) & (c) which exempts the following taxable services from the whole of the service tax leviable thereon under section 66B of the said Act and reverse charge mechanism does not apply over exempted services.

Services provided by-

- (a) an arbitral tribunal to –

(i) any person other than a business entity; or

(ii) a business entity with a turnover up to rupees ten lakh in the preceding financial year;

- (c) a person represented on an arbitral tribunal to an arbitral tribunal;

5. Analysis of Legal Service:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the personproviding service | Percentage of ST payable by the personreceiving the service | |

| By | to | ||||

| 5. | Legal Service | Individual Advocate or a Firm of Advocates by way of support serviceslocated in the taxable territory | Any business entity located in the taxable territory, | NIL | 100% |

Note: When service provider is located in a non-taxable territory (i.e. in J&K or abroad), the receiver of such service shall be liable to pay service tax under reverse charge mechanism in all cases.

I would also like to discuss mega exemption notification 25/2012-ST, entry no. 6(b) & (c), which exempts the following taxable services from the whole of the service tax leviable thereon under section 66B of the said Act and reverse charge mechanism does not apply over exempted services.

Services provided by-

- (a) an individual as an advocate or a partnership firm of advocates by way of legal services to,-

(i) an advocate or partnership firm of advocates providing legal services ;

(ii) any person other than a business entity; or

(iii) a business entity with a turnover up to rupees ten lakh in the preceding financial year; or

- (c) a person represented on an arbitral tribunal to an arbitral tribunal;

6. Analysis of Services by Directors:

NN 30/2012-ST (as amended by NN 45/2012-ST NN 10/2014-ST)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the person providing service | Percentage of ST payable by the person receiving the service | |

| By | to | ||||

| 5A. | Service provided by Directors of Company / Body Corporate | Directors (Part time/ Independent/ Nominee) | Company / Body Corporate located in the taxable territory, | NIL | 100% |

Note: Payments made by the company to its Managing Director/Working Director by any nomenclature, like commission etc., amounts to salary and therefore out of ambit of service tax being employer-employee relationship among the company and such directors. Refer CBEC instruction letter [Dy. No. 324/Comm (Service Tax)/2008 dated 01-12-2008]

Relevant Definitions: Section 65(14) of Finance Act, 1994 and Rule 2(bc) of STR, 1994: “body corporate” has the meaning assigned to it in clause (7) of section 2 of the Companies Act, 1956 (1 of 1956);

Relevant Definitions: Section 65(14) of Finance Act, 1994 and Rule 2(bc) of STR, 1994: “body corporate” has the meaning assigned to it in clause (7) of section 2 of the Companies Act, 1956 (1 of 1956);

Section 2(7) of the Companies Act, 1956: “body corporate” or “corporation“ includes a company incorporated outside India but does not include

(a) a corporation sole ;

(b) a co-operative society registered under any law relating to co-operative societies; and

(c) any other body corporate (not being a company as defined in this Act), which the Central Government may, by notification in the Official Gazette, specify in this behalf;

New definition of Body Corporate as per the Companies Act, 2013 is yet not applicable here which is as hereunder;

Section 2(11) of the Companies Act, 2013: “body corporate” or “corporation” includes a company incorporated outside

India, but does not include—

(i) a co-operative society registered under any law relating to co-operative societies; and

(ii) any other body corporate (not being a company as defined in this Act), which the Central Government may, by notification, specify in this behalf;

Director is not defined in Service Tax Law. Director has been defined in Section 2(13) of the Companies Act, 1956 as hereunder;

“director” includes any person occupying the position of director, by whatever name called;

7. Analysis of Support Service provided by Government or Local Authority:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the person providing service | Percentage of ST payable by the person receiving the service | |

| By | to | ||||

| 6 | Support Service* | Government or Local Authority | Any Business Entitylocated in taxable territory | Nil | 100% |

(*) Note: This reverse charge mechanism does not apply in case of specified services as referred in clause I(A)(iv)(C) (1) & (2) of NN 30/2012-ST dated 20-06-2012 rendered by Government or Local Authority to any business entity located in taxable territory.

Clause (1): Renting of Immovable Property And

Clause (2): Specified Services are as specified in clause (i), (ii) & (iii) of Section 66D(a) under negative list, ………..which are as hereunder;

(i): services by the Department of Posts by way of speed post, express parcel post, life insurance, and agency services provided to a person other than Government;

(ii): services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport; or

(iii): transport of goods or passengers;

8. Analysis of renting/hiring of motor vehicle [complete and partial reverse charge]:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the personproviding service | Percentage of ST payable by the personreceiving the service | |

| By | to | ||||

| 7 | Renting / hiring any motor vehicle designed to carry passenger motorcab on abated * value | (i) any individual(ii) HUF(iii) Proprietary firm(iv) partnership firm(v) Association of Personslocated in the taxable territory | (i) Any company registered under the Companies Act(ii) business entity registered as body corporatewhich is not in similar line of businesslocated in the taxable territory | Nil | 100 % |

| Renting / hiring any motor vehicle designed to carry passenger motorcab on non-abated value | (i) any individual(ii) HUF(iii) Proprietary firm(iv) partnership firm(v) Association of Personslocated in the taxable territory | (i) Any company registered under the Companies Act(ii) business entity registered as body corporatewhich is not in similar line of businesslocated in the taxable territory | 60% (60% of 12.36%) =7.416% w.e.f 1/10/1450%

(50% of 12.36%) = 6.18% |

40% (40% of 12.36%) =4.944% w.e.f 1/10/1450%

(50% of 12.36%) = 6.18% |

|

(*) Note: NN 26/2012-ST dated 20/06/2012 provides 60% abatement on gross value. NN 10/2014-ST dt 11-07-2014 (effective from 01-10-2014)

9 & 10. Analysis of Manpower Supply Service and Security Services:

NN 30/2012-ST (as amended up to date)

Sl.No. |

Description of service |

Provided |

Percentage of ST payable by the personproviding service |

Percentage of ST payable by the personreceiving the service |

|

By |

to |

||||

8. |

Supply of Manpower for any purposeORSecurities Services (added by NN45/2012-ST) |

(i) any individual(ii) HUF(iii) Proprietary firm(iv) partnership firm(v) Association of Personslocated in the taxable territory |

(i) Any company registered under the Companies Act(ii) business entity registered as body corporatelocated in the taxable territory |

25%Effective rate(25% of 12.36)3.09% |

75 %Effective rate(75% of 12.36)9.27% |

11. Analysis of Service portion in execution of Works Contract:

NN 30/2012-ST (as amended up to date)

Sl.No. |

Description of service |

Provided |

Percentage of ST payable by the personproviding service |

Percentage of ST payable by the personreceiving the service |

|

By |

to |

||||

9. |

Works Contract |

(i) any individual(ii) HUF(iii) Proprietary firm(iv) Partnership firm(v) Association of Personslocated in the taxable territory |

(i) Any company registered under the Companies Act(ii) business entity registered as body corporatelocated in the taxable territory |

50% EffectiveST Rate: Case (i)12.36*40%*50% =2.472%Case (ii)12.36*70%*50% =4.326% |

50% EffectiveST Rate: Case (i)12.36*40%*50% =2.472%Case (ii)12.36*70%*50%=4.326% |

Works Contract |

(i) Government(ii) Local Authoritylocated in the taxable territory |

(i) business entitylocated in the taxable territory |

NIL |

100% |

|

Note: When service provider is located in a non-taxable territory (i.e. in J&K or abroad), the receiver of such service shall be liable to pay service tax under reverse charge mechanism in all cases.

Valuation of service rendered [NN 24/2012-ST]

|

Where Works Contract is for… | Value of the Service portion shall be.. |

| 1 | Execution of original contracts | 40% of the total amount charged for the works contractEffective ST Rate:

|

| 2 | Maintenance or repair or reconditioning or restoration or servicing of any goods | 70% of the total amount charged including such gross amountEffective ST Rate:

|

| 3 | In case of other works contracts, not included in S. No. 1 & 2 above, including contracts for maintenance, repair, completion and finishing services such as glazing, plastering, floor and wall tiling, installation of electrical fittings.[1] | 60% of the total amount charged for the works contract |

Valuation of service rendered NN 26/2012-ST [as amended by 02/2013-ST (applicable up to 07/05/2013)]

| “12. | Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly, except where entire consideration is received after issuance of completion certificate by the competent authority,- | (i) CENVAT credit on inputs used for providing the taxable service has not been taken under the provisions of the CENVAT Credit Rules, 2004; | |

| (a) for a residential unit satisfying both the following conditions, namely:–(i) the carpet area of the unit is less than 2000 square feet; or(ii) the amount charged for the unit is less than rupees one crore; | 25 | (ii) The value of land is included in the amount charged from the service receiver.”. | |

| (b) for other than the (a) above. | 30 | ||

| “12. | [F. No. 334 /3/ 2013-TRU]w.e.f. 8th May, 2013Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly, except where entire consideration is received after issuance of completion certificate by the competent authority,- | (i) CENVAT credit on inputs used for providing the taxable service has not been taken under the provisions of the CENVAT Credit Rules, 2004; | |

| (a) for a residential unit satisfying both the following conditions, namely:–(i) the carpet area of the unit is less than 2000 square feet; and(ii) the amount charged for the unit is less than rupees one crore; | 25 | (ii) The value of land is included in the amount charged from the service receiver.”. | |

| (b) for other than the (a) above. | 30 |

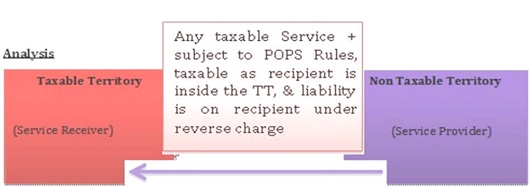

12. Analysis of taxable service provided by person located in a non-taxable territory to a person located in a taxable territory:

NN 30/2012-ST (as amended up to date)

| Sl.No. | Description of service | Provided | Percentage of ST payable by the personproviding service | Percentage of ST payable by the personreceiving the service | |

| By | to | ||||

| 10 | any taxable services i.e. imported | any personlocated in a non-taxable territory | any personlocated in the taxable territory | Nil | 100% |

1. Exception to general rule that no one could render service to himself [Explanation(3) to Section 65B(44)]:

If a person has two establishments/branches, one in taxable territory and another in non-taxable territory, both shall be treated as two distinct establishments of two distinct people[11].

2. Exemptions vide Clause 34 of Mega Exemption NN 25/2012-ST. Services received from a provider of service located in a non- taxable territory by-

(a) Government, a local authority, a governmental authority or an individual in relation to any purpose other than commerce, industry or any other business or profession;

(b) an entity registered under section 12AA of the Income tax Act, 1961 (43 of 1961) for the purposes of providing charitable activities; or

(c) a person located in a non-taxable territory.

3. As per rule 9 of Place of Provision of specified services, (w.e.f. 01-10-2014): The place of provision of following services shall be the location of the service provider;

………(c) Intermediary services; (as amended by NN 14/2012-ST dt 11-07-2014)

So it becomes non taxable service.

Para 10.1.6 of ST Education Guide: How is the service recipient required to calculate his tax liability under partial reverse charge mechanism? How will the service recipient know which abatement or valuation option has been exercised by the service provider?

The service recipient would need to discharge liability only on the payments made by him. Thus the assessable value would be calculated on such payments done. (Free of Cost material supplied and out of pocket expenses reimbursed or incurred on behalf of the service provider need to be included in the assessable value in terms of Valuation Rules) The invoice raised by the service provider would normally indicate the abatement taken or method of valuation used for arriving at the taxable value. However since the liability of the service provider and service recipient are different and independent of each other, the service recipient can independently avail or forgo an abatement or choose a valuation option depending upon the ease, data available and economics.

——————

[1] Section 66B. There shall be levied a tax (hereinafter referred to as the service tax) at the rate of twelve per cent. on the value of all services, other than those services specified in the negative list, provided or agreed to be provided in the taxable territory by one person to another and collected in such manner as may be prescribed.]

[2] Section 68 (1) Every person providing taxable service to any person shall pay service tax at the rate specified in section 66 in such manner and within such period as may be prescribed.

[3] Section 68(2) Notwithstanding anything contained in sub-section (1), in respect of such taxable services as may be notified by the Central Government in the Official Gazette, the service tax thereon shall be paid by such person and in such manner as may be prescribed at the rate specified in section 66 and all the provisions of this Chapter shall apply to such person as if he is the person liable for paying the service tax in relation to such service.

Provided that the Central Government may notify the service and the extent of service tax which shall be payable by such person and the provisions of this Chapter shall apply to such person to the extent so specified and the remaining part of the service tax shall be paid by the service provider.

[4] Rule 5B of CCR, 2004: Refund of CENVAT credit to service providers providing services taxed on reverse charge basis. – A provider of service providing services notified under sub-section (2) of section 68 of the Finance Act and being unable to utilise the CENVAT credit availed on inputs and input services for payment of service tax on such output services, shall be allowed refund of such unutilised CENVAT credit subject to procedure, safeguards, conditions and limitations, as may be specified by the Board by notification in the Official Gazette.

[5] NN 10/2014-ST Dated 11-07-2014

[6] Substituted by NN 6/2014-ST Dated 11-07-2014

[7] Replaced by NN 3/2013-ST…Old Clause No. 21.Services provided by a goods transport agency by way of transportation of –

(a) fruits, vegetables, eggs, milk, food grains or pulses in a goods carriage;

(b) goods where gross amount charged for the transportation of goods on a consignment transported in a single goods carriage does not exceed one thousand five hundred rupees; or

(c) goods, where gross amount charged for transportation of all such goods for a single consignee in the goods carriage does not exceed rupees seven hundred fifty;

[8] NN 6/2014 Dated 11/07/2014

[9] Inserted by NN 8/2014-ST dt 11/07/2014

[10] NN 11/2014-ST dt 11-07-2014

[11] Section 65B(44)Explanation(3): For the purposes of this Chapter……(b) an establishment of a person in the taxable territory and any of his other establishment in a non-taxable territory shall be treated as establishments of distinct persons.

(Author- CA Kamlesh Singh Chauhan-FCA, LL B, DISA(ICA), E-mail: ks_chauhans@yahoo.com, Mobile: +91 9839 094 094)

Plse give information on Organic manures tax percenage .CHapter 31 is fertilssers.

as a trader/importer, ST of 1.4% of CIF value, paid by us is cenvatable or not. i am not registered under service tax. do we have to register. is RCM applicable ?

Hello

I am an exporter of services.

Can i take refund of service tax paid ( 50%) on the non abated value of commute service availed by my Company

Does it qualify for refund

Thanks

Ganesh

Is RCM for manpower and Security services applicable to trust and NPO

Service Receiver is liable to pay service tax under this mechanism from very first invoice received under this category. It means SR is liable to pay ST even when SP is within the ambit exemption limit under NN 33/2012-ST. Please clarify the above.

Dear Sir

We have paid for legal service for X amount…. which falls under notification NO 30/2012. According to the rule I have to pay the service tax on behalf of my SP. As our company is new, we already have excess Cenvat Credit then payable amount of Service Tax. My question is do I have to Pay service tax for the said legal service or I can adjust against the excess cenvat credit !

Pls Reply

Thanks

we are running ltd company ( milk dairy) and taking service from one firm for fabrication and repair work ( All material supplied by us- his work is only fitting that material with help of his owned machines like welding machine etc) , now our confusion is service provider ( firm) applying 14.5% ST to his invoice mentioned as Labhour Bill, when he was produced labhour bill, we ( Ltd company) treated this as a man power supply. but as per ST rule service receiver is liable to pay Service tax full i e 14.5% ST to Govt……. but provider is not agreed for this rule, he is telling that it is come under works contract it my liability. between us there is any agreements made for work purpose. PLEASE HELP US who is eligible to pay service Tax and if you have latest notification please produce, about works contract and man power supply clarify the rules

I would like to know that if any company is obtained a External Commercial Borrowing from Foreign Bank, the amount paid as expenses to various agencies situated at India and abroad, the Expenses paid to them is liable to pay service tax under RCM (on borrower company) or not?

Please advice the ST liability in pre and post Negative era.

Sir,

What should be the % of ST if there’s a delay in the payment of Service Tax, under RCM.

Entity is paying Freight Charges, but not deducting the ST from the previous year (i.e, 2014-15) Will the Tax rate differ? would the entity incurr Interest and Penalty?

a comapany received job work service but provide of service is not issue invoice stated service tax amount.company still liable to pay service tax under rcm

IF JOB WORK SERVICE PROVIDER PROVIDE SERVICE TO COMPANY AND HAS ISSUE INVOICE WITHOUT SERVICE TAX.CAN COMPANY STILL LIABLE TO PAY SERVICE TAX UNDER RCM,……

Can we avail the credit of service tax paid under RCM for imported service

Pl post quires and its answers also will be very helpful

I am paying service tax vide single challan for two different years. Moreover this challan contains payment under reverse charge and for output service also whether there is any circular regarding the same or any solution how i can fill my details in service tax return???

we are service receiver,we received a man power supply service from ABC Ltd, they are raise a bill value Rs.1,00,000/-(Inclusive ST).

Can anyone explain about what is the entry post on our books of accounts.Plz explain abt it.

Dear Sir,

i am receiving legal service by advocate of rs.3000/month. but my advocate have not service tax no. He is under exempt limit. then my question is what i have to pay service tax on amount. if yes then tell me what i am claim it.

Can Service tax liability under RCM be discharged using SEIS & MEIS scrip?

Sir/Madam,

I have received a service of transport, cargo, fright, multiple services from a Agency. agency is provides me such above mentined services from other transporters. Agency provide me a invoice contains ST on his agency commission only.

should i liable to ST on RCM basis over transport, cargo, fright services, which are reimbersment from me. or if not then should I have to deduct tds over full amount or only agency’s commission amount?

pls needful for same.

Thanking you.

Please provide analysis of amendments.

simply superb , your brain like our institute knowledge portal. THANK YOU Sir

Hello sir,

I took service from an immigration company, I’ve paid first instalment but they didn’t have provided me any service since January 2015 from last 2 months after a long chain of emails they agree to refund my money but now they are deducting service tax. So I want to know that whether I can get service tax back as I haven’t received any service from their end?? And on what grounds they are asking for service tax?

sir , you are really serving the professionals with your knowledge bank.

nice article thanks.

The articles are so helpful

nice article

superb effort.

Sir, you have given the best summarized details of the above categories which are mainly in use in current scenario. These are easy to understand to new freshers who are jut joining corporate for service tax.

Please inform whether ST reverse charge mechanism applicable for security services received from lilited company?

mzaa aagya…(y)

My client is a SSI Company, not otherwise covered under Service Tax due to threshold limit. Whereas to discharge his liability under RCM, does he need to Register and avail Service Tax Registration Number? Or a monthly payment of Service Tax vide challan will be sufficient? Is it mandatory to file Service Tax returns?

If (Professional)service provider is individual and doesn’t have service tax number, at the same time service taker is a company and is there chance to apply of reversal mechanism?

Please change div id CONTENT WRAP to at least 950px as the table are not visible

best one

Sir

I want to knaow, Is it necessary for service recceiver to pay service tax in

case of Rent a Cab or Legal Service, even if the service provider is not

registered.. As an example an Individual Legal professional or a individual

taxi operater providing Taxi service to a Limited Company.

Thanks & Regards

R.K. Dutta

Is there is any Difference Between Insurance Agent and Insurance Broker For the Purpose of RCM???

Is there is any difference between Insurance Broker and Insurance Agent for RCM Purpose??

A service provided by an individual of providing meal or supply of food. which is coming in reverse charge mechanism. Any other bank had done the payment on behalf of my client. We are reimbursing the Amount to bank as per their claiming sheet. service provider is coming in exemption limit. but on bills he had written my Client’s Name… So my question is.. service tax should levied or not under RCM..??

superb…

Good article. Clarifying so many implied and hidden provisions. Sir you are requested to always keep updating us by your lucid interpretation of laws and conclusion thereon in matters relating to service tax.

Very good article. Clarifies many queries.

Absoluetly superb . Efforts deserve great appreciation.

All the very best

REgards

Great Sir, Very useful article

Well updated information about various services under RCM as well as PRCM, it is a good for those assessee, who is covered under this category of scheme.

Very well written article………

Sir you are requested to always keep updating us by your lucid interpretation of laws and conclusion thereon in matters relating to service tax.

Good article. Clarifying so many implied and hidden provisions.

Nice one

Quite Impressive article