Who can be person liable

Who can be person liable- Every person providing taxable service (service provider) shall pay tax @ prescribed rate , to be collected in prescribed manner. [section 68(1)]

- Service recipient is a person liable to pay service tax in certain cases [section 68 (2)]

- Defined in rule 2(1)(d) of Service Tax Rules, 1994 and 2(m) of POP Rules, 2012

- Service provider

- Specified service receivers [Rule 2(1)(d)(i)(A to G)]

- Importer of service

Person liable to pay Service Tax under Section 68

In case of services covered under Section 68(2) read with 2(1)(d)

| Service | Liable to pay service tax |

| Insurance agent | Service Recipient (i.e. Insurance company) |

| GTA Specified personsIn other case | Person liable to pay fright GTA |

| Sponsorship service to body corporate / firm | Recipient of service |

| Arbitral tribunal / individual advocate/ firm of advocate | Recipient of service |

| Support service to Govt. / local authority subject to other conditions | Recipient of service |

| Director’s services to Companies | Recipient of service (i.e. Company ) |

| Rent-a-cab service subject to other conditions | Recipient of service |

| Supply of manpower service subject to other conditions | Recipient of service |

| Works contract service subject to other conditions | Recipient of service |

| Services provided from non-taxable territory to any person in taxable territory | Recipient of service |

1. Every person who is liable to pay service tax shall take registration under service tax as per section 69 of Finance Act, 1994

2. Service recipient shall obtain registration under service tax as recipient of service, pay service tax and file return

3. Assessees who have to take registration

- Service provider who has provided a taxable services of value exceeding Rs. 9 lakhs in the preceding financial year

- Service receiver liable to pay service tax under reverse charge mechanism u/s 68(2) / rule 2(1)(d)

- Input service distributor

- Importer of service being person liable u/s 68(2)

Service tax payment – different scenarios

- Normally, service tax is payable by person who provides the service

- Section 68(2) makes provision for reverse charge i.e. making person receiving the service liable to pay tax

- Authority for reverse charge u/s 68(2) of Finance Act, 1994

- W.e.f. 1.7.2012, a new scheme of taxation is applicable whereby the liability of payment of service tax shall be both on the service provider and the service recipient (Notification No. 30/2012-ST, dated 20.6.2012 )

- The extent to which tax liability has to be discharged by the service receiver is specified in Notification No. 30/2012-ST dated 20.6.2012.

- Renting of motor vehicles

- Manpower supply & security services

- Works contracts

- Insurance related services by agents

- Goods Transportation By Road

- Sponsorship

- Arbitral tribunals

- Legal services

- Company director’s services

- Services provided by Government / local authority excluding specified services

- Services provided by persons located in non-taxable territory to persons located in taxable territory.

- Liabilities of both the service provider and service receiver are statutory and independent of each other

- Liability cannot be shifted by mutual agreement

- Reverse charge will not apply where the service receiver is located in non-taxable territory

- Reverse charge shall not be applicable if provider of service was liable before 1.7.2012

- Service Tax will not be payable by service receiver under reverse charge, if service was provided prior to 1.7.2012, even if payment is made after 30.06.2012

- Credit of tax paid can be availed by service recipient if it is input service for him

- The credit of tax paid by the service recipient under partial reverse charge would be available on the basis on the tax payment challan (but invoice required)

- Service provider under RCM may claim refund of tax paid under rule 5(b) of CCR, 2004

- Service Tax under reverse charge to be paid within 6 months on actual payment (Rule 7 of POT Rules, 2011)

- Small scale benefit is available only to service provider (not to service receiver), if entitled

- Service receiver under reverse charge cannot avail exemption of Rs. 10 lakh under Notification No. 33/2012-ST dated 20.06.2012

- Valuation of services by services provider and service receiver can be on different principles, if permitted by law (e.g. works contract – Refer Notification No. 30/2012-ST, explanation II)

- Invoice to be prepared as per Rule 4A of Service Tax Rules, 1994

- It is a statutory obligation (not contractual) on the service recipient to pay Service Tax, whether under full or proportional reverse charge

- Service Tax under reverse charge has to be paid only by cash vide GAR Challan No. 7 and it cannot be paid by way of utilization of Cenvat Credit.

- Once paid, Cenvat credit can be taken for paying eligible input service

- Service receiver liable only for his portion

Important Points in Joint Reverse Charge Mechanism

- Individual

- Hindu undivided family (HUF)

- Firm (including limited liability partnerships)

- Association of persons

If both the above conditions are not satisfied in respect of these three services, Service Tax shall be payable by the service provider in ordinary course.

| Service Provider | Service Receiver | Service Tax Payable by |

| Individual /HUF/ Partnership firm /AOP | Business entity – body corporate | Joint |

| Individual /HUF/ Partnership firm /AOP | Individual /HUF/ partnership firm /AOP | 100 % by service provider |

| Business entity –Body Corporate / Company | Individual /HUF/ Partnership firm /AOP | 100 % by service provider |

| Business entity –Body Corporate | Business entity – Body Corporate | 100 % by service provider |

- For three specified services provided by business entities being company, society, co-operative society, trust etc, reverse charge will not apply.

- Reverse charge will also not apply where the service recipient is any person or business entity not being a body corporate in case of three specified services

- “Business Entity” means any person ordinarily carrying out any activity relating to industry, commerce or any other business or profession

- “Body Corporate” means the meaning assigned to in clause (7) of Section 2 of the Companies Act, 1956 and section 2(11) of 2013 Act.

- Company , corporation and LLP are ‘body corporate’

- Firm, HUF, Trust and Co-operative society are not ‘body corporate’

- But firm includes LLP for Service Tax

Reverse Charge Mechanism under various Services

|

Sr. No |

Description of Service |

Service Provider |

Service Receiver |

|

1. |

Services provided by an insurance agent to any person carrying on insurance business |

Nil |

100% |

|

2. |

Services provided by a goods transport agency in respect of transportation of goods by road |

Nil |

100% |

|

3. |

Services provided by way of sponsorship |

Nil |

100% |

|

4. |

Services provided by an arbitral tribunal |

Nil |

100% |

|

5. |

Services provided by individual advocate or a firm of advocates by way of legal services |

Nil |

100% |

|

5A. |

in respect of services provided or agreed to be provided by a director of a company to the said company ( w.e.f 7.08.2012) |

Nil |

100% |

|

6. |

Services provided by Government or local authority by way of support services excluding,- 1. renting of immovable property, 2. postal services 3. transport of goods / passengers 4. air craft or vessel |

Nil |

100% |

|

7. |

Hiring of Motor Vehicle (a) renting of a motor vehicle designed to carry passengers on abated value to any person not engaged in the similar line of business (b) renting of a motor vehicle designed to carry passengers on non abated value to any person who is not engaged in the similar line of business |

Nil 60% |

100 % 40% |

|

8. |

Services provided by way of supply of manpower for any purpose or security services (w.e.f 07.08.2012) |

25% |

75 % |

|

9. |

Services provided in service portion in execution of works contract |

50% |

50% |

|

10. |

Services provided by any person who is located in a non-taxable territory and received by any person located in the taxable territory |

Nil |

100% |

Service Specific Issues under RCM

Director’s Services

- Vide entry No. 5A of N. No. 30/2012 as amended by N. No. 45 and 46/2012

- Service tax is payable under reverse charge by companies who receive services from their directors who are not in employment

- Sitting fees, commission, bonus, etc. are subject to service tax

- WTDs /MDs /EDs who are under contractual employment with the company and receive salary or remuneration from the company will not be covered – considered as employees of the company

- Director can be appointed either in an individual capacity or as a nominee for company , association or any other entity including Government.

- Interest on loan by director to company, dividend on shares, other professional charges on account of services not rendered as a director (in professional capacity) are not liable to Service Tax

- In case of nominee director, the nominating company who receives fees will be liable to pay service tax.

- The invoice / receipt to be issued by the directors within 30 days

- In case of nominee directors, the invoice will be issued by the nominating company

- In the case of Government nominees, the services shall be deemed to be provided by the Government but liable to be taxed under reverse charge basis

|

Particulars |

Position upto 6.8.2012 |

Position w.e.f. 7.8.2012 |

|

Individual Director in his individual capacity |

To be registered and pay service tax |

Service tax paid by the company |

|

Nominee Director |

Paid by the nominee director’s company |

Paid by the nominee director’s company |

Manpower Supply Services

- Service is manpower supply service if under command of principal employer

- Cleaning service, piece basis / job basis contract is not manpower supply service

- Service tax will be applicable on salary plus PF, ESI, commission of labour contractor and other chargesž

- Employees sent on deputation are also covered under manpower supply services

Security Services

- Security services means services relating to the security of any property, whether movable or immovable, or of any person, in any manner and includes the services of investigation, detection or verification, of any fact or activity

- CA services are not security services

- Distinction between manpower supply & security services

Rent-a-cab Service

- In case of renting of motor vehicles to carry passengers where abatement is also available, reverse charge basis is proportional depending upon the abatement on the condition that no Cenvat Credit has been availed. The service provider should provide a certificate, either in the invoice itself or separately.

- In case of renting of motor vehicle to carry passengers, reverse charge applies only where service receiver is not engaged in same business.

- Reverse charge will be applicable when renting to a person who is not in similar line of business

- Service receiver will pay on 40% in every case whether abatement is claimed or not

- No Cenvat credit (not an input service)

Goods Transport Service

- Service tax liability arise when consignment note is issued

- GTA will be liable to pay tax only when both service provider and service receiver are individuals

- Tax on 25% (abated value), if GTA does not avail Cenvat Credit, otherwise tax on 100% value

Legal Services

| Service Provider | Service Receiver |

| Individual Advocate / Firm / LLP | Business entity with turnover > Rs 10 lakhs in preceding financial year |

| Arbitral Tribunal | Business entity with turnover > Rs 10 lakh in previous financial year |

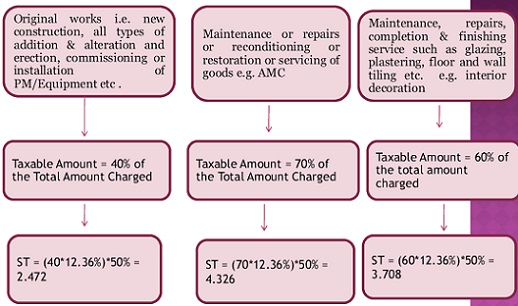

Works Contract Services

Services provided by Government / local authority

1. Reverse charge applicable to all services except specified services

2. Government Department needs to be registered and pay tax on support services of –

- Renting of immovable properties

- Speed post, express parcel, life insurance.

- Transport of goods and/ or passengers

- Services in relation to vessel or aircraft

3. Services to be provided to any business entity located in taxable territory

Invoice/ Bill/ Challan in RCM

- Amount of Service Tax based on his share of Service Tax liability, if any, (which service recipient is required to pay to the service provider) – in case of joint or proportionate reverse charge liability.

- Fact that entire amount of Service Tax on the invoice is payable by the service recipient under reverse charge (if so).

- Invoice amount is inclusive / exclusive of applicable Service Tax.

- Alternatively, in case of proportionate reverse charge, service provider should charge Service Tax only on that part of the invoice for which he is liable to pay and wants to recover from the service recipient and mention that balance amount is payable by the service recipient.

Author Bio

I have paid service tax in 2012 to a service provider. But he did not pay the amount to the govt. I have received notice from the dept. to pay the service tax because of default of the service provider, because he has not registered nor paid the tax collected by him from me. Am I liable to pay the service tax alongwith interest,almost 5 years later ?

Is RCM applicable on rent paid?

The owner of the building is exempted from GST as his turnover is less than 20 lakhs.

The payer of the rent is registered under GST

Is RCM applicable on rent paid?

The owner of the building is exempted from GST as his income is less than 20 lakhs.

The payer of the rent is registered under GST

Depends upon which type of service u (individual) provided ????

Dear sir,

We have recruited a new employee in our organization through placement agency. Sir please let me know who is responsible to pay service tax. There is no service tax registration number on the bill of placement agency.

Plz. clarify.

Good evening sir, could you please clarify me in this regard. i am proving the turnover details

Total Turnover : Rs. 15Lakhs

Service provider : Individual

Service Recievers :

1) XYZ Ltd

2) Individual

Reciepts From XYZ Ltd — RS. 8,00,000 /-

Reciepts from Individual —- Rs. 7,00,000 /-

—————

— Rs 15,00,000 /-

Now the XYZ Ltd is paying Service Tax on Reverse Charge Basis on the amount of Rs.8,00,000/-

is it need to pay Service Tax on balance Rs.7,00,000/- from service provider point of view ?, as reverse charge is not apply to individual (service Reciever) and service Tax registration is applicable to Service Provider, if it first year in which the Service Provider crossed 9 lakhs Turn over ?

Dear Sir

i have received GTA service and then given same GTA service to another client, the another client is covered under reverse charge mechanism and i also covered under same mechanism. can i pay service tax under reverse charge under similar service

With reference to the Sr. No. 10 in table “Reverse Charge Mechanism under various Services” copied below, it is mentioned that it is the responsibility of service recipient to register and pay 100% of the service tax to the department.

“Services provided by any person who is located in a non-taxable territory and received by any person located in the taxable territory”

Is this applicable to any kind of service? Service in my case is renting of commercial building. I am the service provider not living in India.

1) As per my tax consultant: I don’t have to register for service tax, don’t have to collect and pay the same. Per RCM the tenant should register and pay service tax directly to the department.

2) Tenant is saying they can’t register and can’t pay the service tax to the department. They want me to send them invoice for service tax.

Who is correct?

Appreciate your views.

sir Thanks for ur wonderful article , i have one query in case of partial reverse charge is compulsory to follow or it is optional i means if service provider want to paid wholle amount then is any problem in this …… pls suggest me one of my clinet collect whole amont of service tax ……..

My client is a pvt. ltd.company and has been paying service tax on 25% of freight under GTA but as u mentioned above that liability to service tax will arise if both the service provider and receiver are individuals which means my above client is exempt from paying service tax under RCM being a pvt. Ltd.company. Kindly clarify.

Dear Sir,

thank u very much 4 ur article. But, i have an query…..

what if, under 100% reverse charge, SERVICE PROVIDER charged service tax in the invoice and service receiver paid 100% to service provider?

We are service recipient (Pvt. Ltd.) under GTA service. Earlier we are paying service tax to transporter due to service tax claim & charge on Consignment Note. We have paid the amount against money receipt & details are disclosed on that money receipt. When we asked to transporter then they said we have already paid service tax centrally. Now department had claim repayment the service tax amount & reverse the input credit to department. Please advice in this situation what we shall do?

As a director I am getting sitting fees of Rs. 12,00,000/- from a Co. where Co. pays service tax to Govt. on my director sitting fees and I am also providing professional services of Rs.3,00,000/- to others.

So my question is that I have to get Service Tax Registration or not. ??

Will my director sitting fees be consider for getting Service Tax Registration or will I be covered within the exemption limit??

“Body Corporate” has the meaning assigned to it in clause (7) of Section

2 of the Companies Act, 1956 (1 of 1956);Hence LLP is considered as body corporate and not as firm for payment of service tax under reverse charge mechanism.

sir , we are (pvt Ltd)service receiver of manpower from propriter ship concern, they are charging service tax on 25% of service value, can i take that much service input

is reverse charge mechanism applicable to service provided by courier agency.

Dear Sir,

thank u very much 4 ur article. But, i have an query…..

what if, under 100% reverse charge, SERVICE PROVIDER charged service tax in the invoice and paid to the government?????

Sir,

Your article is very nice.

Pls clarify whether a State Govt department who is the service receiver of manpower from a partnership firm is liable to pay service tax under joint reverse charge mechanism? If has to pay, will the departement has to take separate PAN Card? Or the TAN of the DDO is sufficient for registration?

Its very well drafted, please confirm Reverse charge on manpower and security service etc applicable to LLP.

Sir, I have a query regarding manpower supply ( Security Services) service provider & receiver both are the Pvt. Ltd. Company. Pls tell me a the service tax liability of service taker or giver.

Thanks

Dear Sir,

Thank you for your informative article. Request you to please put more light as to how service tax has to be paid by the recipient when they do not fall in the service tax ambit. What are the steps so that 100% of the service tax is paid by the service receipient ?

i am taken service tax registration on GTA and during the year i am received rent on commercial property amounting to Rs. 120000/- . whether i am laible to pay service tax on rent.?

Sir, ours is a proprietory concern doing works contract & dealing with Government works(client is A.P.Govt) on turnkey basis. We have charged service tax 12.36% on labour portion agst bill. The Dept. has deducted service tax amount and asked us to produce serive tax challan before releasing the service tax deduction amount.

But ours is a proprietory concern and Service tax liability is only 50%

and balance 50% shall be paid by the Dept. Is this correct sir?

Suppose If we do not pay service tax then the client (as mentioned above) will pay entire amount?

Can we take input tax on that bill recovery of 50% Service tsx?

2) If the both companies are corporate sector, giving construction of civil works to the other company.The liability of service tax should be paid by serive reciever? 50% or 100% of Service tax How much amount has ot pay? Here RCM is applicable in this case?

Your valuable reply in this regard is highly appreicaited

We have paid reverse charges on manpower service on 75 % of billing can we take this amount 100% cenvat in same year?

Thank you for you detailed explanation on RCM , OUR QUERY IS , IN CASE OF WORKS CONTRACT THE ABATEMENT AT 60% (TAXABLE VALUE AT 40% ) IS COMPULSORY OR THE CONTRACTOR CAN ASCERTAIN THE COST OF MATERIAL AND SERVICE PORTION SEPARATELY BASED ON HIS BILLING AND PAY TAX ON THE COMPONENT OF SERVICE UNDER S.TAX AND ON MATERIAL UNDER VAT

Sir,

I wanna ask that wthether a pvt. ltd. co. can apply service tax reverse mechanism on professional service received from individual and another is on rent paid by co. for office premises to an individual.

please guide me accordingly.

Sir, is Government Department is liable to pay service tax under RCM on hiring of advocate and manpower etc.

Sir,

can a Service Tax Distributor pay Service Tax Under Reverse Charge Mechanism & take Cenvat Credit to Distribute to other Unit.

Dear Sir

Please explain more on the condition to make payment of reverse charge after 6 month.

Thanks

Dear Sir,

our company MNC company so we want lot of manpower in the plant , one man power supplier supplied man power to our company and they rice the bill in the name of “Susheel Manpower Services” but they not mentioned Service Tax Portion because they telling not applicable for us .

Please give a clarification for this issue

Will GTA include courier services also. And if service tax has already been charged on consignment note by the service provider does then service receiver’s liability arise to pay service tax.

Hello Sir,

In case of services fallng under Reverse Charge Mechanism, Point of Taxation commences from the date of payment of the RCM bill provided payment is made within six months of the date of invoice as per Rule 7 of POT Rules 2011. However, if not made, whether the burden of interest payment will shift to much earlier date as Rule 7 is not applicable in such cases.

CA Subrath Meka

9850011996

Thanks u sir,for such a nice Explanation abt RCM…

Sir,

Very good overview on reverse charge mechanism.

but

if u can through some light also on Import of service.

Even though it was covered under reverse charge earlier also,

there is bit confusion being going on at many places regarding whether nexus of service being provided in India is important or just booking of expenses as import of service, by a Indian company is only a criteria.

This is also effected also on the Place of Provision.

Thank you for the article Sir. I have a query regarding applicability of manpower supply provisions in case of piece rate basis contracts. Can you please provide any legal provisions to support the view that the same is not covered under manpower supply?